Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

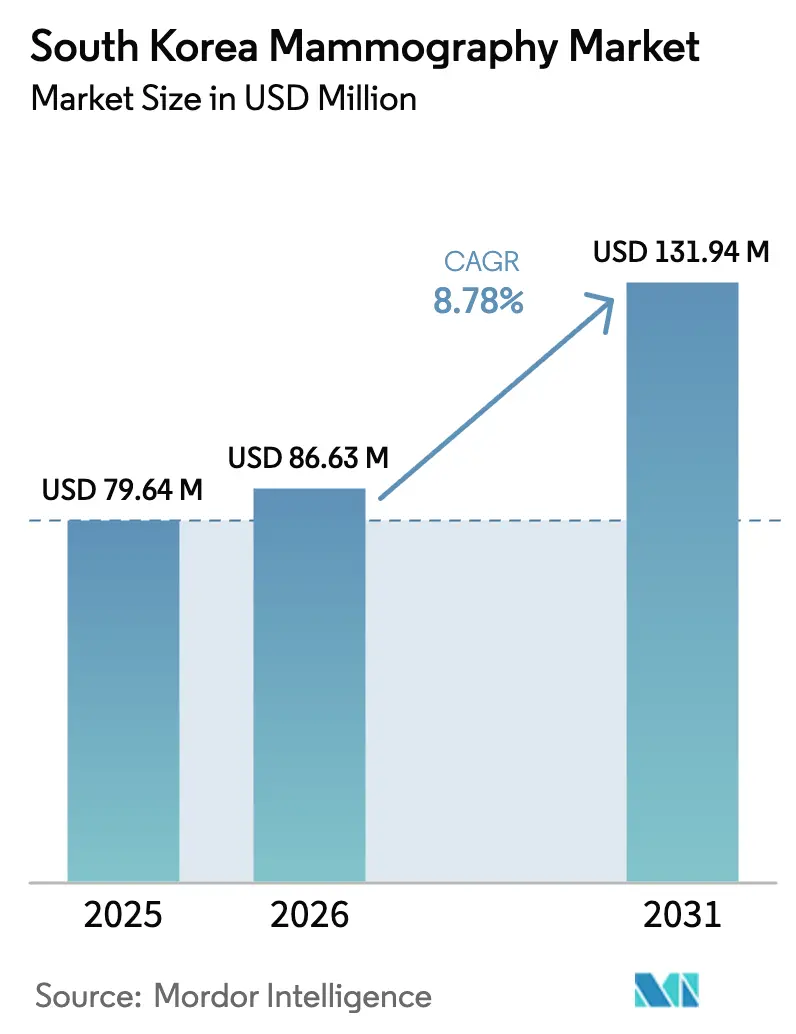

| Base Year Market Size (2025) | USD 79.64 Million |

| Market Size (2026) | USD 86.63 Million |

| Market Size (2031) | USD 131.94 Million |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Mammography Market Analysis by Mordor Intelligence

South Korea mammography market size in 2026 is estimated at USD 86.63 million, growing from 2025 value of USD 79.64 million with 2031 projections showing USD 131.94 million, growing at 8.78% CAGR over 2026-2031. Demographic aging, expanded National Cancer Screening Program (NCSP) reimbursement, and rapid uptake of artificial-intelligence (AI) tools are the central forces propelling the South Korea mammography market. Digital breast tomosynthesis (DBT) is replacing 2-D mammography as the clinical baseline, while 5G-enabled remote quality-assurance (QA) frameworks reduce geographic gaps in image interpretation. Hospitals still anchor procurement volumes, yet specialty breast clinics are drawing share by offering patient-centric workflows and shorter waiting times. Competitive positioning is shifting toward software-led value propositions, with local vendors leveraging regulatory familiarity to accelerate go-to-market cycles.

Key Report Takeaways

- By product type, digital mammography captured 61.72% of South Korea mammography market share in 2025; Breast tomosynthesis is forecast to expand at a 10.05% CAGR, the fastest rate among product segments through 2031.

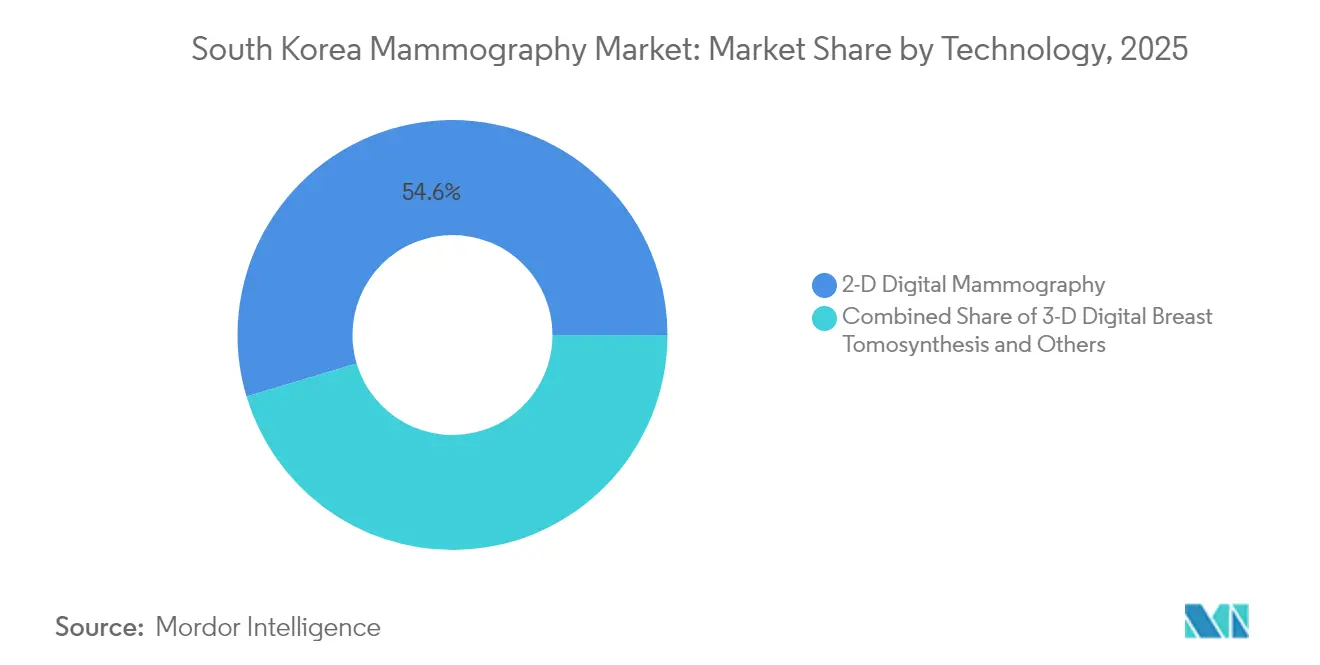

- By technology, 2-D systems held 54.62% share in 2025, while 3-D DBT advances at 9.83% CAGR to 2031.

- By end user, hospitals accounted for 48.25% of South Korea mammography market size in 2025, whereas specialty breast clinics are growing at 9.42% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising breast-cancer incidence | +2.1% | National, highest in urban districts | Long term (≥ 4 years) |

| NCSP biennial screening reimbursement | +1.8% | National, stronger in rural regions | Medium term (2-4 years) |

| Reimbursement for digital breast tomosynthesis | +2.3% | Early uptake in Seoul Capital Area | Short term (≤ 2 years) |

| AI-powered computer-aided detection | +1.9% | Tertiary hospitals nationwide | Medium term (2-4 years) |

| Blood-based screening tests | +0.8% | Pilot sites in metropolitan areas | Long term (≥ 4 years) |

| 5G-enabled rural QA networks | +0.4% | Remote provinces outside Seoul | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Breast Cancer Among Women

Breast-cancer cases reached 33,335 in 2025, making the disease the most common malignancy among Korean women [1]Kyu-Won Jung, “Prediction of Cancer Incidence and Mortality in Korea, 2025,” Cancer Research and Treatment, cancerresearchtreatment.org. Incidence rose 205.26% between 1990 and 2021, far outpacing regional averages. The 5-year relative survival rate climbed to 93.6% for the 2015-2019 cohort, underscoring the screening program’s clinical payoff. Women now delay childbirth and concentrate in urban settings, two established risk correlates. As the 50-59-year cohort expands, demand for mammography units rises, strengthening the South Korea mammography market.

Expansion of NCSP Reimbursement for Biennial Screening

NCSP now covers 90% of the cost for biennial mammography among women aged ≥ 40 years, eliminating out-of-pocket fees [2]National Health Insurance Service, “Insurance Benefits,” nhis.or.kr . Participation improved, recall rates fell from 17.2% in 2009 to 11.2% in 2020, and detection rates grew from 1.5 to 3.1 per 1,000 screens. Rural uptake rose fastest, narrowing historical access gaps. Policymakers are assessing ultrasound reimbursement for dense breasts, which could elevate screening throughput further.

Rapid Switch-Over to Digital Breast Tomosynthesis Since 2023 Reimbursement

Parity reimbursement for DBT began in 2023, enabling facilities to justify capital outlays of USD 400,000–600,000 per unit. DBT identifies 20–65% more invasive cancers than 2-D mammography, a critical advantage in a population where dense breast tissue exceeds 70% prevalence. Seoul leads adoption, but provincial hospitals follow as reimbursement de-risks investment.

AI-Powered CAD Improving Detection & Workflow

Lunit INSIGHT achieved area-under-curve performance of 0.91 in DBT datasets. In the AI-STREAM prospective study, radiologists aided by AI detected 140 cancers versus 123 without assistance, without increasing recall. AI also improves specificity to 93% in extremely dense breasts, tackling a key limitation of human readers. Hospitals integrate AI to manage 15-20% annual growth in screen volumes amid flat radiologist supply.

Blood-Based Tests Expanding Screening Funnel

MASTOCHECK measures three protein biomarkers and targets women with dense tissue where mammography is less sensitive. Pilot coverage inside urban clinics enlarges the screening funnel, creating supplementary demand for diagnostic mammography follow-up.

5G-Enabled Remote QA Networks for Rural Clinics

Samsung Medison and Lunit run QA networks that transmit DBT files via 5G, allowing urban radiologists to review rural images within minutes. Mobile connectivity cuts diagnostic reading time by 50%, reducing travel burdens on patients and opening new device-placement opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation-dose concerns in women aged 40s | −1.2% | Urban, higher education levels | Short term (≤ 2 years) |

| Uneven 3-D system distribution | −0.9% | Rural provinces | Medium term (2-4 years) |

| Patient discomfort favoring ultrasound/blood | −0.7% | National, younger demographics | Long term (≥ 4 years) |

| Escalating PACS storage for DBT files | −0.5% | High-volume facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Radiation-Dose Concerns Among Women in Their 40s

Average scatter radiation is only 0.87 mGy at the sternum, yet fear persists. Educational campaigns and dose-reduction software seek to reassure patients, but anxiety suppresses screening intent, constraining near-term uptake.

Patient Discomfort Shifting Preference to Ultrasound/Blood Tests

Surveys show greater comfort with ultrasound than DBT. Clinics now bundle ultrasound and blood tests with mammography to retain patient loyalty, diluting pure mammography volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Dominance Drives Premium Migration

The South Korea mammography market size for digital equipment led all product categories, holding 61.72% share in 2025. Analog units fade as hospitals modernize electronic medical record (EMR) systems that require digital images. Breast tomosynthesis revenue will grow at a 10.05% CAGR, supported by reimbursement parity and superior cancer-detection metrics. Although capital costs remain steep, workflow gains and lower recall rates shorten return-on-investment periods. Niche categories such as contrast-enhanced mammography gain clinical traction where specificity is paramount. The Ministry of Food and Drug Safety (MFDS) now requires AI integration disclosure under the 2025 Digital Medical Products Act, further tilting demand toward smart digital platforms.

Legacy 2-D systems continue to serve lower-volume clinics, yet replacement cycles accelerate as DBT becomes the clinical baseline. Corporate procurement teams justify premium equipment by citing 20–65% higher invasive detection rates, especially relevant for the 70% dense-breast prevalence cohort. Digital breast tomosynthesis adoption aligns with national AI strategies, amplifying software subscriptions linked to each installed unit. Vendors now bundle cloud PACS storage and AI-CAD licences, transforming one-time hardware sales into recurring revenue streams.

By End User: Specialty Clinics Capture Growth Premium

Hospitals commanded 48.25% of South Korea mammography market share in 2025, anchored by comprehensive oncology pathways. Yet specialty breast clinics post the fastest 9.42% CAGR as patients seek streamlined experiences and faster report turnaround. Clinics often install DBT or contrast-enhanced units earlier than public hospitals, positioning themselves as technology leaders. Diagnostic imaging centers remain essential in mid-sized cities but feel margin pressure as hospitals expand outpatient wings.

Specialty providers differentiate by integrating AI-CAD, patient-comfort paddles, and rapid online scheduling. Hospitals counter by building dedicated breast-imaging suites that inherit multidisciplinary referral flows. Imaging centers invest in mobile DBT units to reach employer-sponsored screenings, yet their share erodes where clinics and hospitals overlap. Consequently, procurement strategies diverge: hospitals prioritize scalability, clinics emphasize premium experience, and imaging centers weigh cost versus service differentiation.

By Technology: 3-D Tomosynthesis Reshapes Clinical Standards

Two-dimensional systems retained 54.62% installed share in 2025, yet 3-D tomosynthesis is advancing at 9.83% CAGR. Evidence shows DBT cuts false positives and improves detection in dense breasts, underpinning rapid replacement of 2-D fleets. Additional modalities such as contrast-enhanced mammography and automated breast ultrasound (ABUS) fill diagnostic niches but remain smaller contributors.

AI-enabled DBT platforms like Lunit INSIGHT received FDA 510(k) in 2023, boosting domestic credibility and export opportunities. Vendors now deliver integrated packages pairing DBT hardware with AI subscriptions, PACS storage, and on-site training. MFDS approval pathways under the Digital Medical Products Act shorten time-to-market for such combined offerings. Hospitals prefer these turnkey platforms because they minimize vendor coordination and accelerate staff competency.

Geography Analysis

Seoul Capital Area hosts the densest cluster of DBT installations, yet 19.8% of breast-cancer patients still travel from other provinces for initial treatment. Metropolitan secondary cities such as Busan, Daegu, and Incheon intensify upgrades to stem this medical tourism. Expanded 5G networks enable remote QA workflows, allowing provincial radiologists to consult Seoul experts without patient transfer.

Regional cancer-detection rates vary; metropolitan screening participation outruns rural areas, yet government subsidies for mobile DBT vans aim to narrow gaps. Provincial administrations offer tax incentives for clinics adopting AI-integrated devices. Diagnostics firms trial telerobotic ultrasound systems that connect local sonographers with off-site radiologists, further decentralizing care.

The South Korea mammography market increasingly emphasizes distributed service delivery. MFDS now streamlines approval for standardized DBT units to facilitate rural deployment. Combined with cloud-based AI and teleconsultation, this policy environment supports faster technology diffusion beyond Seoul.

Competitive Landscape

Market concentration is moderate. Global hardware leaders—Hologic, GE HealthCare, Siemens Healthineers—anchor high-end equipment portfolios. Domestic innovators such as Lunit and Samsung Medison differentiate with AI algorithms optimized for Korean dense-breast demographics. The locus of competition is shifting from hardware to holistic breast-health platforms that integrate imaging, analytics, and workflow orchestration.

In May 2024, Lunit acquired Volpara Health Technologies, expanding its installed base to 3,000 global sites and adding volumetric-density analytics to its platform [3]Lunit, “Lunit Completes Acquisition of Volpara,” lunit.io . Samsung Medison leverages 5G connectivity to deliver remote QA for rural clinics. Hologic continues strategic M&A, acquiring a breast-care rival for USD 310 million in 2024 to broaden its portfolio. Meanwhile, Bertis promotes its MASTOCHECK blood test, positioning as a complementary screen rather than a direct substitute.

White-space opportunities persist in rural service models, PACS optimization, and multimodal screening bundles. Compliance hurdles under the Digital Medical Products Act favor incumbents with established regulatory staff. As AI modules become table stakes, service contracts and data-management analytics emerge as the next competitive battleground.

South Korea Mammography Industry Leaders

Siemens AG

Fujifilm Holdings Corporation

Hologic Inc.

Planmed OY

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Lunit entered a five-year deal with Starvision Service to roll out AI solutions across 79 radiology sites.

- April 2025: SimonMed Imaging partnered with Lunit to deploy AI-powered breast-cancer detection across U.S. outpatient centers.

- March 2025: South Korea’s first large-scale prospective study confirmed Lunit AI enhances single-reading mammography accuracy.

- April 2024: German firm AB-CT installed its first nu:view breast-CT scanner in South Korea, delivering non-compression, pain-free imaging.

South Korea Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. South Korea Mammography Market is segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End Users (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Breast Tomosynthesis (3-D) |

| Other Product Types |

By End User

| Hospitals |

| Specialty Breast Clinics |

| Diagnostic Imaging Centers |

By Technology

| 2-D Digital Mammography |

| 3-D Digital Breast Tomosynthesis |

| Others |

| By Product Type | Digital Systems |

| Analog Systems | |

| Breast Tomosynthesis (3-D) | |

| Other Product Types | |

| By End User | Hospitals |

| Specialty Breast Clinics | |

| Diagnostic Imaging Centers | |

| By Technology | 2-D Digital Mammography |

| 3-D Digital Breast Tomosynthesis | |

| Others |

Key Questions Answered in the Report

How big is the South Korea Mammography Market?

The South Korea Mammography Market size is expected to reach USD 86.63 million in 2026 and grow at a CAGR of 8.78% to reach USD 131.94 million by 2031.

How fast is breast tomosynthesis growing in South Korea?

Breast tomosynthesis revenue is rising at a 10.05% CAGR, the fastest among product categories.

Who are the key players in South Korea Mammography Market?

Siemens AG, Fujifilm Holdings Corporation, Hologic Inc., Planmed OY and GE Healthcare are the major companies operating in the South Korea Mammography Market.

Which end-user segment is expanding quickest?

Specialty breast clinics post the highest growth at a 9.42% CAGR through 2031.

Page last updated on: