Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

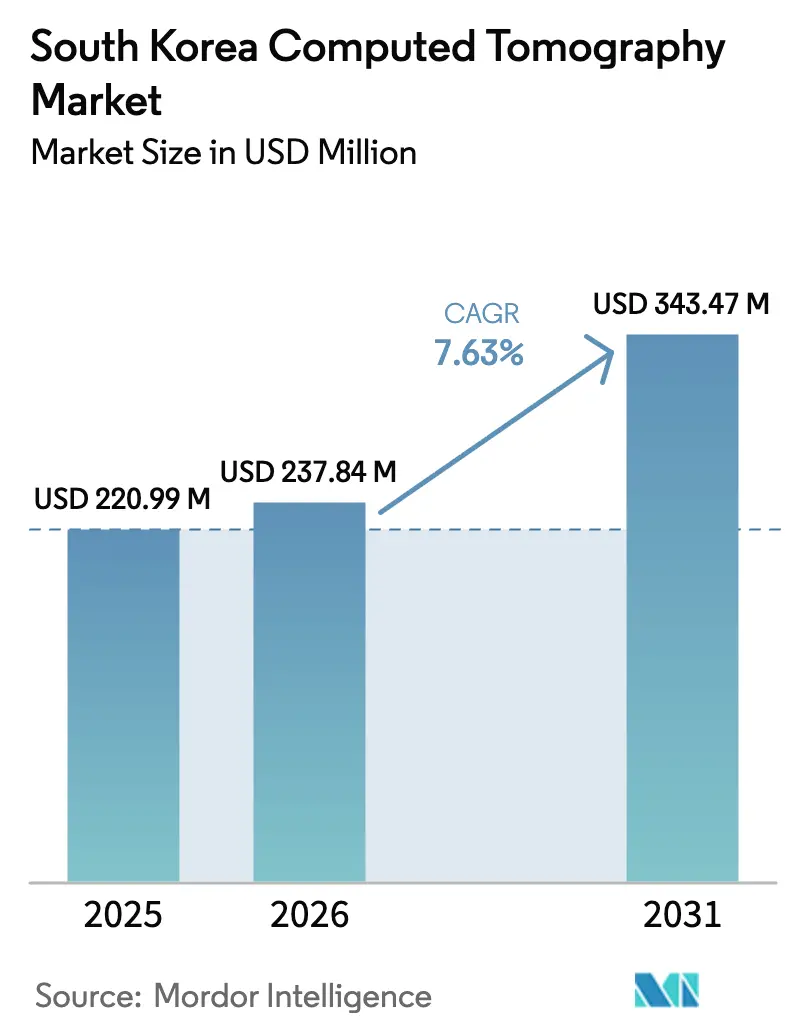

| Base Year Market Size (2025) | USD 220.99 Million |

| Market Size (2026) | USD 237.84 Million |

| Market Size (2031) | USD 343.47 Million |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Computed Tomography Market Analysis by Mordor Intelligence

South Korea computed tomography market size in 2026 is estimated at USD 237.84 million, growing from 2025 value of USD 220.99 million with 2031 projections showing USD 343.47 million, growing at 7.63% CAGR over 2026-2031. The steady rise reflects national policies that channel KRW 10 trillion into hospital upgrades, generous NHIS reimbursement, and a CT scanner density of 44.5 units per million residents that surpasses the OECD average. A broad transition toward AI-enabled image-reconstruction platforms has already cut radiation dose in routine protocols by 75% while preserving diagnostic clarity. Mobile CT fleets that proved critical during COVID-19 outbreaks now support rural outreach programs, and large hospitals use 5G-linked teleradiology to balance workload across metropolitan hubs. Oncology continues to dominate procedure volume, yet neurology scans are expanding fastest as stroke centers proliferate and geriatric screening intensifies nationwide.

Key Report Takeaways

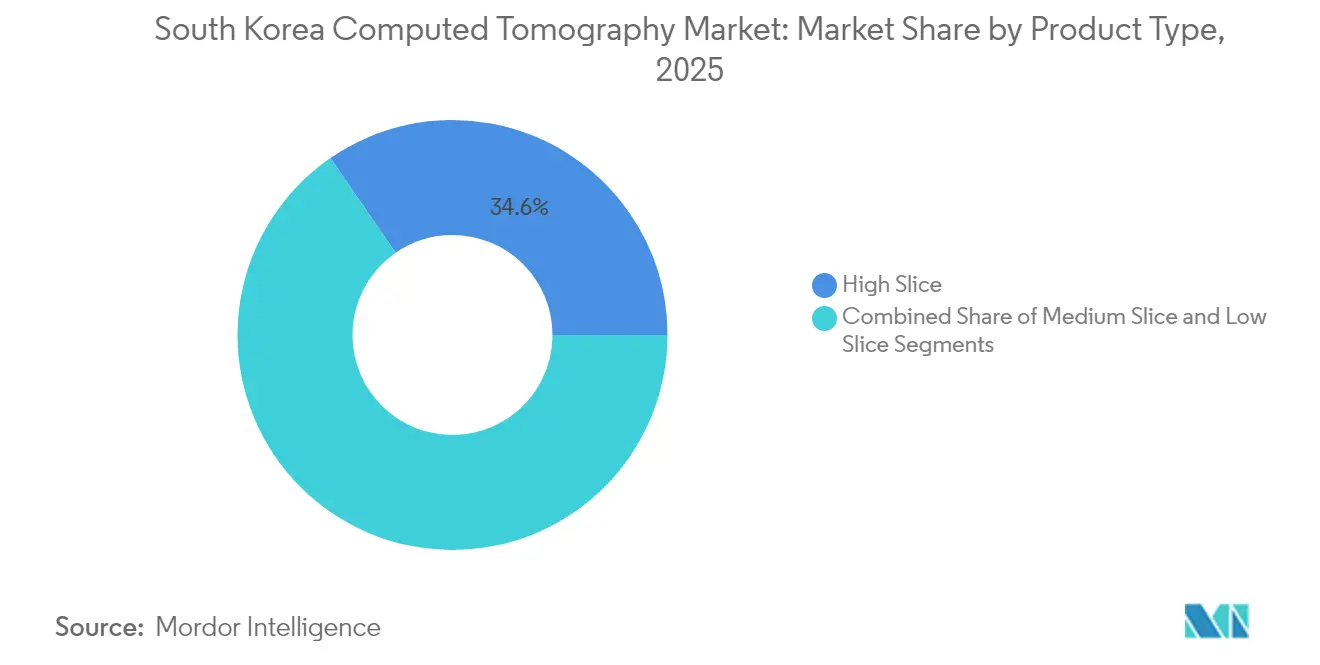

- By product type, high-slice systems led with 34.62% revenue share in 2025, whereas medium-slice scanners are projected to grow at 8.16% CAGR to 2031.

- By application, oncology accounted for 32.10% of the South Korea computed tomography market size in 2025; neurology is poised for the fastest 8.32% CAGR through 2031.

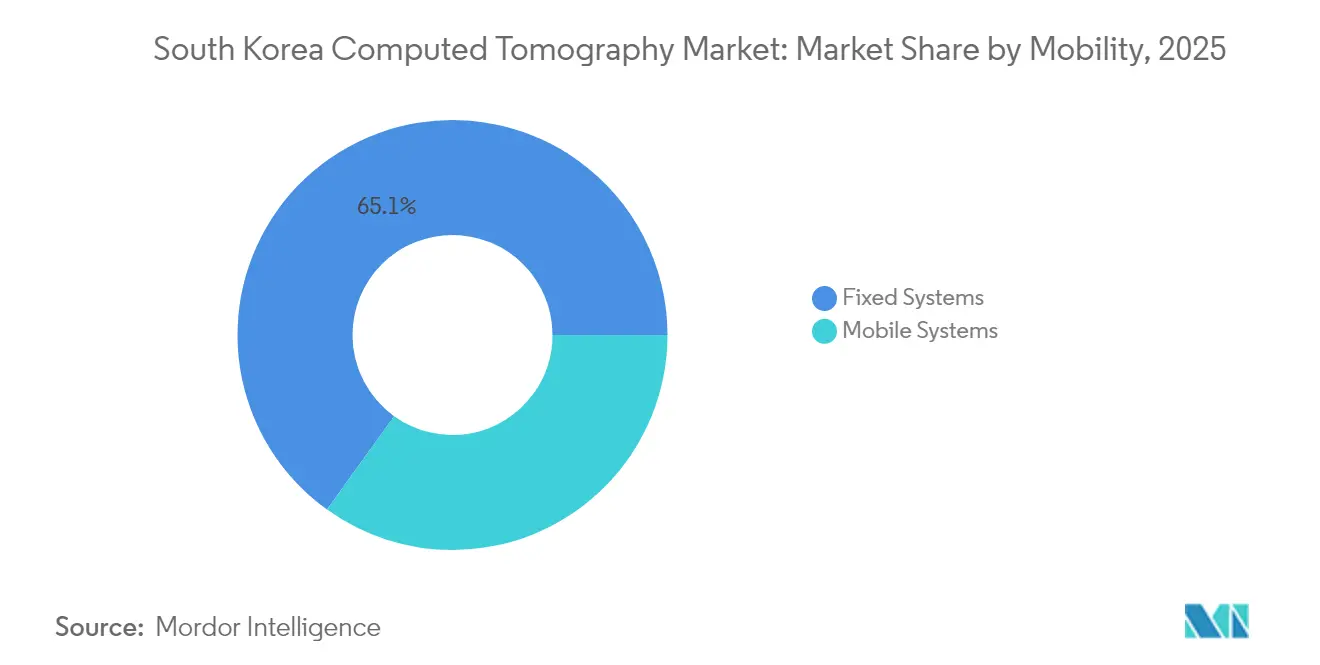

- By mobility, fixed installations held 65.08% of the South Korea computed tomography market share in 2025, while mobile units record an 8.54% CAGR on expanding rural deployments.

- By end user, hospitals represented 48.55% of 2025 revenue, but diagnostic imaging centers are growing at 8.42% CAGR on privatization and patient-convenience trends.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Computed Tomography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of chronic diseases | +1.8% | Seoul–Incheon corridor and other urban clusters | Medium term (2-4 years) |

| Rising geriatric population & screening need | +2.1% | Nation-wide, acute in rural provinces | Long term (≥ 4 years) |

| Government NHIS expansion for CT procedures | +1.5% | Pan-national roll-out | Short term (≤ 2 years) |

| Rapid AI-driven workflow upgrades | +1.2% | Major tertiary hospitals in metropolitan areas | Medium term (2-4 years) |

| Carbon-ion and proton therapy planning | +0.6% | Seoul–Gyeonggi specialized cancer centers | Long term (≥ 4 years) |

| Private 5G networks enabling remote scans | +0.5% | Initially metropolitan; scaling to secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic Diseases

The national burden of cancer, cardiovascular illness, and chronic lung disorders is shifting CT from episodic investigation to routine surveillance. The lung-cancer screening arm of the National Health Screening Program offers low-dose CT to smokers aged 55-74, and participation jumped 28% in 2025 after policy refinements that added never-smokers at elevated risk. Cardiac CT is now a first-line gatekeeper for stable chest pain, replacing invasive angiography in many centers and easing waiting lists for catheter labs. Oncology follow-up programs standardize thin-slice contrast protocols to detect sub-centimeter lesions that earlier scanners missed, fuelling steady hardware upgrades. Diagnostic imaging centers in suburban districts have responded by extending hours and adding dual-source CT suites dedicated to outpatient scans. These patterns ensure that the South Korea computed tomography market will remain integral to chronic-disease management nationwide.

Rising Geriatric Population & Screening Demand

South Korea crossed the “super-aged” threshold in 2025, and CT volumes mirror the demographic pivot. The Transitional-Age Screening Program now reimburses thoraco-lumbar CT for osteoporosis in women aged 66, normalizing CT as a preventive tool rather than a last-resort test. Emergency departments report a spike in head CT for falls and cerebrovascular events among seniors, while facial bone CT grew 3,118% over the past decade. Dose-reduction algorithms grounded in deep learning alleviate clinician concern about cumulative exposure, permitting frequent follow-up scans for chronic subdural hematoma and other age-linked conditions. Mobile CT caravans outfitted with 64-slice scanners now travel to provincial clinics on fixed schedules, closing the urban–rural imaging gap.

Government NHIS Expansion Covering CT Procedures

NHIS policy updates effective January 2025 cut patient copayments to 10% for most CT-based cancer checks and broadened reimbursement to include AI-assisted image reconstruction. The Health Insurance Review & Assessment Service simultaneously raised facility fees for CT, improving hospital ROI and hastening replacement of legacy single-slice units. Public hospitals immediately tendered for medium-slice platforms that embed smart-scan protocols to meet mandated radiation benchmarks. Vendors partner with provincial authorities to pilot bulk-procurement schemes that align payment with dose-performance metrics, ensuring rapid adoption even in smaller county hospitals.

Rapid AI-Based Workflow & Image-Quality Upgrades

Deep-learning reconstruction now reduces radiation by 75% while preserving lesion conspicuity on sub-millimeter sections. Clinical trials at Samsung Medical Center showed a 33% rise in referral rates after AI triage flagged incidental pulmonary nodules in out-patient scans, underscoring AI’s role in case-finding. High-performance GPUs embedded in new CT consoles accelerate iterative reconstruction, trimming average thorax scan time from 12 minutes to under 5. Hospital groups integrate AI dashboards into EMRs, allowing radiologists to batch-approve normal studies and focus on flagged cases. These gains drive green-lighting for capital projects even under the stricter 2025 Digital Medical Products Act because buyers can demonstrate improved productivity and patient safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront & lifecycle scanner costs | -1.4% | Pronounced in small hospitals and rural facilities | Short term (≤ 2 years) |

| Stringent MFDS regulatory oversight | -0.8% | Uniform across the country | Medium term (2-4 years) |

| Radiation-dose concerns among clinicians | -0.7% | National, heightened for pediatric follow-up | Medium term (2-4 years) |

| Market saturation in large urban clinics | -0.5% | Seoul–Incheon metropolitan area | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront & Lifecycle Costs of CT Scanners

Capital outlays remain the single biggest hurdle for district hospitals, where 23.6% of installed scanners are older than 10 years. New photon-counting CT systems cost up to USD 2.3 million, and service contracts can exceed USD 150,000 annually, straining operating budgets. Facilities often extend scan hours to amortize equipment faster, a practice that risks marginal indications creeping into routine use. Service-life uncertainty compounds the burden: software obsolescence now arrives in five-year cycles, forcing recurrent upgrade negotiations or the prospect of network isolation. The government’s depreciation allowance and low-interest borrowing schemes partly cushion the impact, yet smaller providers still hesitate to purchase leading-edge systems.

Stringent MFDS Regulatory & Reimbursement Review

The Ministry of Food and Drug Safety re-classified AI-embedded CT scanners as Class IV devices under the 2025 Digital Medical Products Act, requiring dossier submissions that include multi-center clinical validation and real-world post-market surveillance plans [1]Ministry of Food and Drug Safety, "Approval Process," mfds.go.kr. Approval timelines have lengthened to 12-18 months, delaying product launches and squeezing vendor marketing cycles. Simultaneously, the reimbursement gatekeeper demands cost-effectiveness evidence, pushing manufacturers to bundle AI software licenses with hardware under usage-based pricing. While patients ultimately benefit from higher safety thresholds, the regulatory load can stall refreshing of aging fleets, especially in non-profit provincial hospitals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type – Medium Slice Systems Drive Technology Transition

Medium-slice scanners commanded significant unit demand in 2025, and they are set to expand at 8.16% CAGR as hospitals seek high-throughput performance without premium-tier price tags. The South Korea computed tomography market size for medium-slice platforms is projected to climb steadily alongside outpatient imaging-center openings. Enhanced cooling systems and integrated dual-energy modes now allow 80-slice models to match diagnostic reach once limited to 128-slice equipment.

High-slice systems still capture 34.62% of revenue by enabling whole-heart imaging in a single beat and ultra-low-dose pediatric protocols. Their dominance is reinforced by tertiary hospitals that rely on multi-phase oncology staging and trauma algorithms requiring sub-second rotation times. Low-slice units remain viable for extremity studies and interventional suites but their share erodes as refurbished 64-slice devices undercut entry-level models. Competitive pricing from Siemens Healthineers’ Somatom Pro.Pulse lowers capital barriers, ensuring medium-slice scanners remain the workhorse segment of the South Korea computed tomography market .

By Application – Neurology Accelerates Amid Stroke-Care Expansion

Oncology preserved 32.10% revenue in 2025 as national screening mandates anchor CT in tumor detection, staging, and radiotherapy planning. The South Korea computed tomography market share for oncology will stabilize as PET-CT gains ground, yet absolute scan counts rise with a growing survivor population needing quarterly follow-ups .

Neurology outpaces every specialty at 8.32% CAGR, fueled by nationwide hyper-acute stroke centers that demand 24/7 CT perfusion and angiography. AI-powered large-vessel-occlusion detection assists junior residents during night shifts, trimming door-to-needle times. Cardiovascular indications maintain a reliable baseline, with coronary CT-angiography replacing treadmill tests in many health-check packages. Musculoskeletal requests climb on sports-injury management and geriatric fractures. Emerging fields such as CT-guided pain therapies and pediatric congenital-heart imaging keep broadening the clinical map for the South Korea computed tomography market.

By Mobility – Mobile Systems Gain Traction Through Pandemic-Proven Flexibility

Fixed rooms remain the backbone, contributing 65.08% of revenue and handling poly-trauma, multi-phase oncology, and large-volume emergency loads. Their permanence facilitates radiation-shielding optimization and smooth integration with pneumatic-tube specimen systems.

Mobile CT posts an 8.54% CAGR as provincial governments fund truck-mounted units that visit county clinics on rotation schedules. During 2024, mobile scanners in Busan processed more than 6,000 chest CTs and cut patient transfer by 37%, validating the model’s economics. Remote control consoles let central radiologists protocol and read studies in real time over secure 5G links. Manufacturers are now releasing 128-slice mobile variants with battery-assist generators, extending service windows during power outages and disaster relief deployments.

By End User – Diagnostic Centers Capitalize on Privatization Trends

Hospitals commanded 48.55% revenue in 2025 because emergency, oncology, and inpatient pathways rely on in-house CT. Proton-therapy planning further entrenches large academic centers, which demand sub-millimeter isotropic datasets compatible with carbon-ion dose-calculation engines.

Diagnostic imaging centers exhibit 8.42% CAGR, boosted by consumer preference for shorter wait times and transparent pricing. Operators invest in AI-enhanced scheduling platforms that cut idle gantry time below 5% and support extended evening clinics. Other users—research institutes, veterinary hospitals, and device-trial sites—remain small in value but innovative in scope, piloting photon-counting detectors and novel contrast media. Their experiments shape future procurement standards for the South Korea computed tomography market.

Geography Analysis

The capital megaplex of Seoul, Incheon, and Gyeonggi generated well over half of 2025 CT revenue, reflecting dense population, multi-hospital clusters, and the earliest adoption of dual-source and spectral technologies. High-profile academic centers such as Asan Medical and Seoul National University Hospital act as reference sites, catalyzing peer adoption across the South Korea computed tomography market.

Secondary metros—Busan, Daegu, and Gwangju—now log double-digit scan growth as city councils co-fund equipment upgrades to retain patients who previously traveled to Seoul. Rural provinces, although starting from a smaller installed base, present the fastest percentage gains owing to KRW 10 trillion in central grants earmarked for regional hospital modernization. Mobile CT caravans bridge long travel distances, performing nearly 40% of annual scans in Gangwon’s mountainous districts.

Medical tourism adds an international layer: 606,000 foreign patients entered South Korea in 2024, a 144.2% rise year-on-year. Many select premium health-check packages that combine coronary CT-angiography with low-dose lung and abdomen studies, sustaining high-end scanner utilization in urban flagship clinics. Government targets of 700,000 inbound patients by 2027 should further widen the South Korea computed tomography market across hospitality-linked medical complexes.

Competitive Landscape

Global multinationals dominate hardware revenue, yet competition hinges on AI differentiation more than detector rows. GE HealthCare introduced Revolution Vibe in 2025, bundling an AI-driven motion-correction suite and unlimited one-beat cardiac imaging—features calibrated to Korea’s high arrhythmia prevalence. Siemens Healthineers’ Somatom Pro.Pulse pursues mid-tier buyers with 20% lower power draw, aligning with energy-efficiency incentives from Korea Electric Power Corporation. Philips’ CT 5300, launched in late 2024, markets workflow orchestration that lets technologists pre-populate patient demographics through QR codes, easing EMR integration.

Domestic AI specialists Lunit and VUNO partner with OEMs to preload nodule-detection and bone-age modules at factory level, shortening validation cycles for MFDS approval. Lunit’s collaboration with Radiobotics blends Korean chest-X-ray analytics with European musculoskeletal expertise, bolstering export prospects.

Service-contract innovation intensifies: subscription models now bundle uptime guarantees with continuous AI-software updates, spreading costs across five-year terms. Hospitals evaluate vendors not just on gantry speed but on demonstrated reductions in repeat scans, report-turnaround improvements, and radiation-dose transparency. Such metrics frame purchasing committees’ scoring sheets, shaping the next growth phase of the South Korea computed tomography market.

South Korea Computed Tomography Industry Leaders

-

Canon Medical Systems Corporation (Toshiba Corporation)

-

GE Healthcare

-

Koninklijke Philips NV

-

Siemens Healthineers AG

-

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GE HealthCare and Kalbe inaugurated a CT-scanner production plant to reinforce supply chains for the Asian market, including South Korea.

- September 2024: Philips Korea introduced the Philips CT 5300, an AI-enabled system focused on workflow streamlining for radiologists.

- January 2024: AB-CT installed its first nu:view breast-CT scanner in South Korea, providing pain-free, non-compression imaging for breast cancer diagnosis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea computed tomography market as the total annual revenue generated by new, fixed and mobile CT scanners installed for human diagnostic imaging across all public and private healthcare settings. Equipment based on cone-beam or micro-CT architecture serving dental or industrial use is excluded.

(Scope Exclusion: Veterinary, industrial and cone-beam CT units fall outside this estimate.)

Segmentation Overview

-

By Product Type

- Low Slice

- Medium Slice

- High Slice

-

By Application

- Oncology

- Neurology

- Cardiovascular

- Musculoskeletal

- Other Applications

-

By Mobility

- Fixed Systems

- Mobile Systems

-

By End User

- Hospitals

- Diagnostic Imaging Centers

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed radiologists, biomedical engineers, procurement heads, and MFDS reviewers across Seoul, Busan, and Daejeon. These conversations clarified replacement cycles, budgeting realities, and the pace at which photon-counting upgrades will diffuse beyond tertiary centers, letting us reconcile secondary signals with day-to-day decision factors.

Desk Research

We began with trusted public sources such as the Ministry of Food and Drug Safety device registry, Korean Statistical Information Service hospital census, National Health Insurance Service reimbursement schedules, OECD Health Data on imaging rates, and publications from the Korean Society of Radiology. These sources quantify installed base, utilization, and tariff evolution that anchor historical demand. Supplemental context arrived from peer-reviewed journals on low-dose protocol adoption and from news in Dow Jones Factiva and device-maker filings that disclose average selling prices and product mix shifts. Finally, customs shipment records and selected views from D&B Hoovers validated import trends for high-slice systems. The references named illustrate our desk research universe; several additional outlets were reviewed to round out data collection and cross-checks.

Market-Sizing & Forecasting

A top-down model starts with national scan volumes and average reimbursement, reconstructing demand pools that are further filtered through equipment utilization norms and capacity targets. Selective bottom-up tests, such as supplier roll-ups and sampled ASP × unit counts, validate totals and expose any divergence. Key variables include aging population growth, cancer screening participation, CT scans per 1,000 inhabitants, average selling price spread between 64-slice and >=128-slice units, and replacement interval lengthening tied to AI-enabled software upgrades. Multivariate regression informed the 2025-2030 outlook, while scenario analysis captured policy-driven swings in dose-ceiling rules. Where bottom-up evidence was sparse, install base proxies and trade data bridged gaps.

Data Validation & Update Cycle

Outputs pass variance checks against import data and insurance spending, then undergo multi-analyst peer review. Reports refresh every twelve months, with interim revisions if reimbursement, safety, or macro events materially shift demand. A final pre-publish audit ensures clients receive the latest calibrated view.

Why Mordor's South Korea Computed Tomography Baseline Commands Reliability

Published estimates often diverge because firms choose different equipment scopes, currency bases, and refresh cadences. We observe the biggest gaps arise when portable scanners or cone-beam units are omitted, when aggressive ASP erosion is assumed without supplier proof, or when forecast drivers ignore Korea's mandatory cancer screening volumes that buoy high-slice demand.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 220.99 M (2025) | Mordor Intelligence | - |

| USD 93.4 M (2024) | Regional Consultancy A | Covers only low- and mid-slice systems, excludes mobile CT, older currency base |

| USD 212.98 M (2023) | Trade Journal B | Applies flat 6% CAGR without validating ASP spread or replacement lag |

| USD 600 M (2023) | Global Consultancy C | Bundles cone-beam devices and research micro-CT, mixes export figures with domestic installs |

The comparison shows that once scope alignment and disciplined variable selection are applied, Mordor's balanced figure sits between conservative undercounts and inflated roll-ups, giving decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current size of the South Korea computed tomography market?

The South Korea computed tomography market is valued at USD 237.84 million in 2026 and is projected to reach USD 343.47 million by 2031 at a 7.63% CAGR.

Which product category leads the market today?

High-slice CT scanners command the largest 34.62% revenue share, while medium-slice units are expanding fastest at 8.16% CAGR.

Why are neurology scans growing faster than other applications?

The nationwide rollout of hyper-acute stroke centers and AI-assisted large-vessel-occlusion detection is driving an 8.32% CAGR for neurology CT.

How is mobile CT adoption influencing rural healthcare?

Mobile scanners operating on provincial circuits have cut patient transfer by 37% and underpin the fastest growth within the mobility segment at 8.54% CAGR.

What role does government reimbursement play in CT uptake?

NHIS now covers 90% of many CT procedures, and updated facility fees have accelerated hardware renewal, supporting consistent market growth.

Which vendors are shaping the competitive landscape?

GE HealthCare, Siemens Healthineers, and Philips lead hardware sales, while domestic AI innovators such as Lunit provide software differentiation that influences purchasing decisions.

Page last updated on: