Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

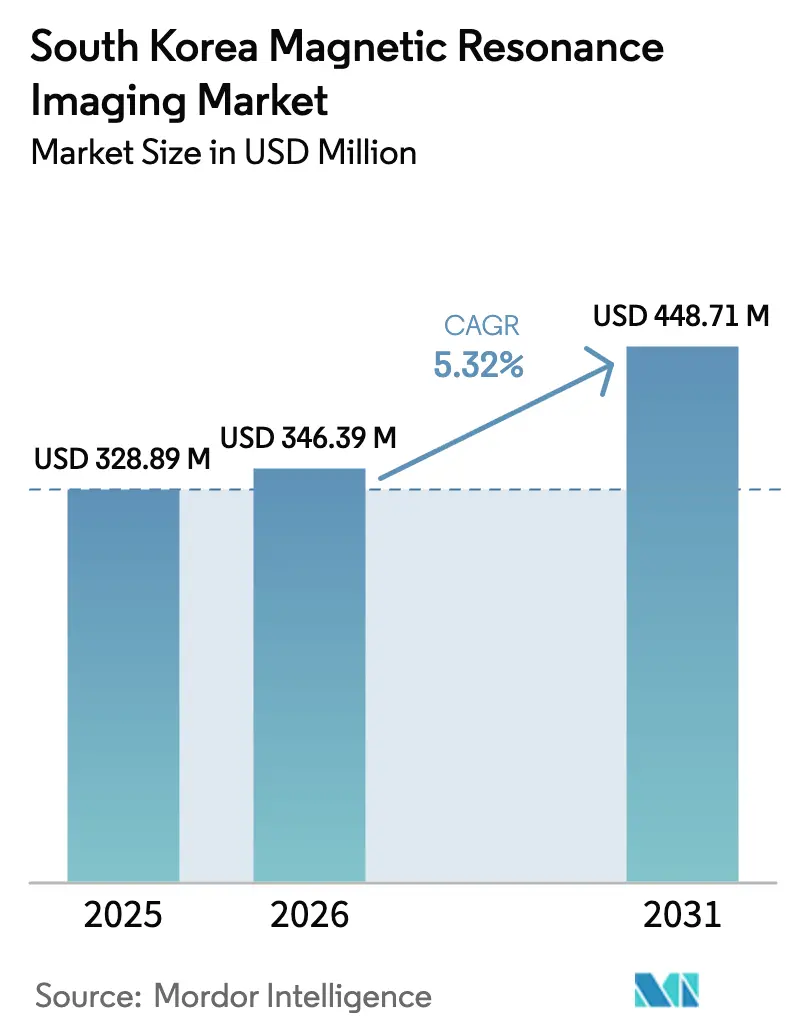

| Base Year Market Size (2025) | USD 328.89 Million |

| Market Size (2026) | USD 346.39 Million |

| Market Size (2031) | USD 448.71 Million |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

The South Korea MRI market size in 2026 is estimated at USD 346.39 million, growing from 2025 value of USD 328.89 million with 2031 projections showing USD 448.71 million, growing at 5.32% CAGR over 2026-2031. Steady digitization of healthcare, a surge in AI-enhanced diagnostic tools, and the government’s KRW 30 trillion (USD 22.9 billion) 2025 spending plan underpin demand. National Health Insurance coverage for 51.5 million residents guarantees a broad patient base, while hybrid and AI-assisted scanners shorten examination time and raise throughput. Closed high-field platforms remain the clinical workhorse, but open and very-high-field systems gain traction as patient-centered care and precision oncology expand. Capital-cost constraints and workforce shortages outside metro areas temper near-term growth yet open opportunities for point-of-care devices and service outsourcing. The South Korea MRI market continues to evolve through strategic alliances between global vendors and local AI start-ups that turn workflow efficiency into a competitive differentiator.

Key Report Takeaways

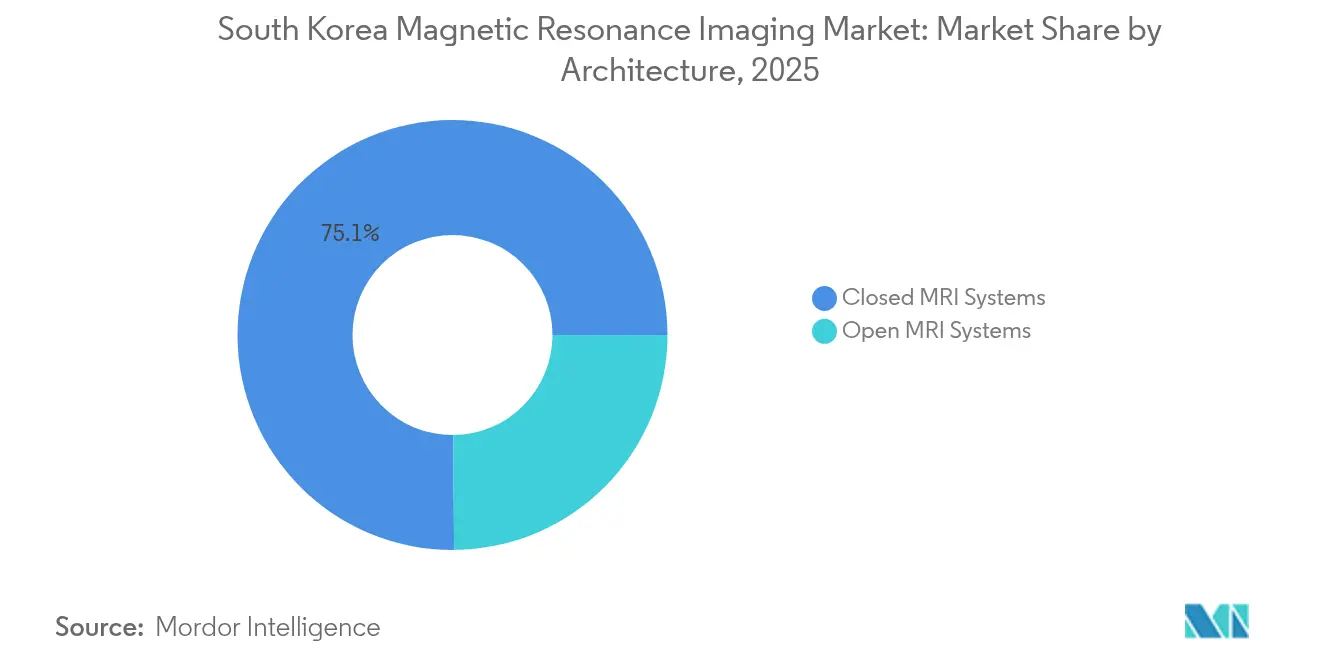

- By architecture, closed systems held 75.12% of the South Korea MRI market share in 2025, while open systems are projected to advance at a 5.94% CAGR to 2031.

- By field strength, 1.5 T scanners accounted for 55.63% of the South Korea MRI market size in 2025; 3 T and ≥ 7 T platforms are growing at 5.65% CAGR through 2031.

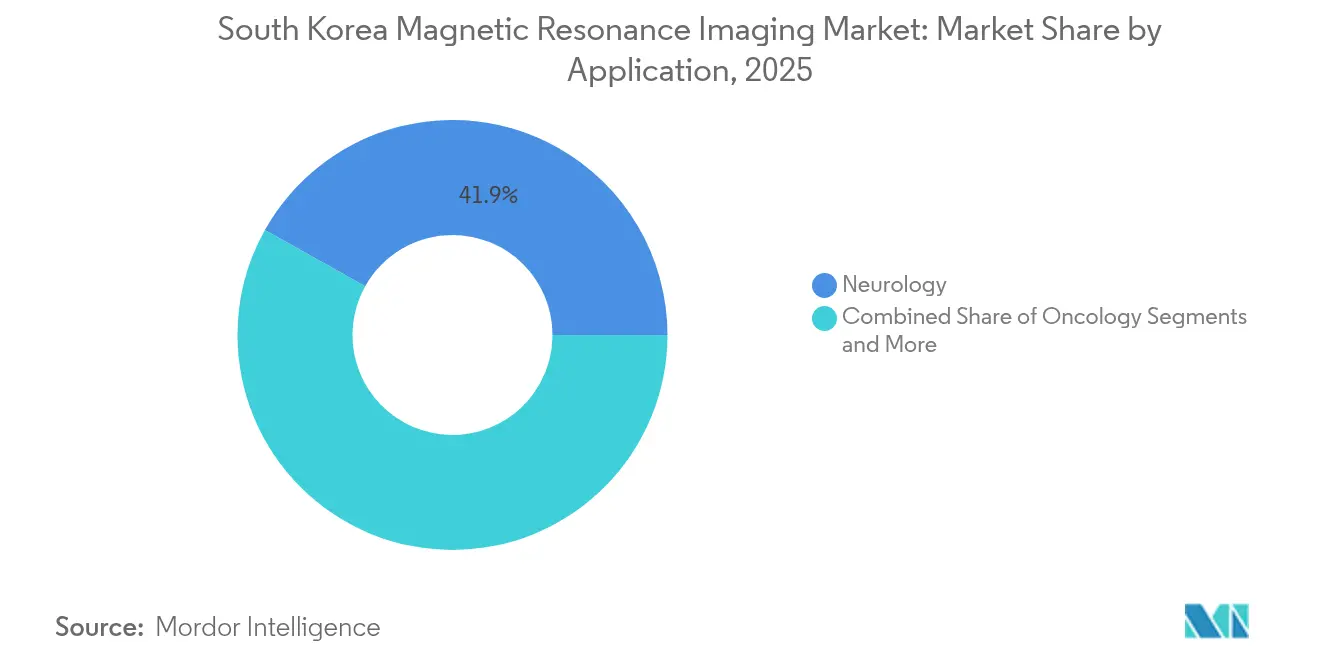

- By application, neurology contributed 41.88% revenue in 2025, whereas oncology is set to post the fastest 6.02% CAGR through 2031.

- By end user, hospitals captured 47.60% of the South Korea MRI market size in 2025; specialized clinics and imaging centers lead growth at 6.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Magnetic Resonance Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Introduction of Hybrid MRI Systems | +0.8% | National, concentrated in Seoul-Busan corridor | Medium term (2-4 years) |

| Rising Burden of Chronic Diseases & Geriatric Population | +1.2% | National, with higher impact in rural areas | Long term (≥ 4 years) |

| Mandatory Cancer Screening Expansions under South Korea's NHI | +0.9% | National, standardized implementation | Short term (≤ 2 years) |

| Adoption of AI-Based Image Reconstruction in Tertiary Hospitals | +1.1% | Metropolitan areas, expanding to secondary cities | Medium term (2-4 years) |

| Local Manufacturing Incentives for Advanced Medical Devices | +0.6% | Industrial complexes in Chuncheon, Gyeonggi | Long term (≥ 4 years) |

| Emergence of Office-based Point-of-Care MRI Pods | +0.4% | Urban centers, pilot implementations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Introduction of Hybrid MRI Systems

Hybrid MRI platforms combine magnetic resonance with PET or CT to deliver metabolic and anatomic insight in a single session, an approach prized in oncology treatment planning. The Korean ARPA-H program earmarks KRW 55 billion through 2029 for multimodal diagnostics, channeling early subsidy to tertiary centers in Seoul and Busan [1]Ministry of Health and Welfare, “Korean ARPA-H Project,” MOHW.GO.KR. Samsung Medical Centre integrates hybrid suites into its smart-hospital blueprint, citing reduced patient transfers and faster decision cycles. Vendors emphasize streamlined workflow, citing 15-20 minute savings per oncology case and 6% lower resCAN rates. Capital intensity and specialty-staff requirements remain hurdles, though public-funding offsets and vendor-financing packages are narrowing the adoption gap for regional cancer centers.

Rising Burden of Chronic Diseases & Geriatric Population

South Korea became a super-aged society in 2025, with ≥ 20% of citizens aged 65 years or older. Chronic diseases compel earlier, image-guided diagnosis, pushing average MRI studies per 1,000 inhabitants up 7% year-on-year in rural provinces. The Community Care Act steers investment toward transitional home-medical services, prompting tertiary facilities to procure portable scanners for follow-up imaging. Abbreviated protocols—breast MRI in under 10 minutes and zero-contrast knee exams—align with geriatric comfort needs and throughput objectives. Vendors that tailor workflow to mobility-impaired seniors gain preference in provincial tenders.

Mandatory Cancer Screening Expansions under South Korea’s NHI

Revised reimbursement rules effective January 2025 add new MRI procedure codes for liver, pancreatic, and prostate cancer staging, granting 80%–90% cost coverage when scans follow standardized pathways. Hospitals upgrading to multi-parametric oncology packages report 12% revenue lift per scanner and 18% faster payback. Rural coverage gaps persist, yet mobile MRI clinics funded under the Essential Healthcare Recovery Plan schedule quarterly tours to 30 underserved counties, expanding addressable volume by an estimated 11%. Screening mandates also spur demand for AI-enabled lesion detection tools that counterbalance radiologist shortages during peak sessions.

Adoption of AI-Based Image Reconstruction in Tertiary Hospitals

Deep-learning algorithms such as SwiftMR trim scan times up to 50% and raise signal-to-noise ratios on legacy hardware. Five of the six major university hospitals now embed AI recon into neuro, spine, and prostate protocols, freeing capacity for 3–4 additional slots per day. FDA 510(k) approvals granted in 2024 accelerate cross-border deployments and joint validation studies with U.S. centers, enhancing vendor credibility. Remaining challenges involve algorithm-specific training, cybersecurity assurance, and reimbursement differentiation for AI-enhanced versus conventional scans, topics the National Health Insurance Authority is evaluating for the 2026 fee schedule.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs | -0.9% | National, more pronounced in smaller facilities | Short term (≤ 2 years) |

| Shortage of Trained MRI Technologists Outside Metro Areas | -1.1% | Rural and secondary cities | Medium term (2-4 years) |

| Reimbursement Pressure on Low-Field Scans | -0.6% | National, affecting cost-sensitive segments | Short term (≤ 2 years) |

| Import-dependence for Super-conducting Magnets | -0.4% | National, supply chain vulnerability | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs

A new 1.5 T system costs USD 1.2–1.5 million, with service contracts consuming 8–12% of capital annually, straining budgets for non-tertiary hospitals [2]U.S. Department of Commerce, “South Korea – Medical Equipment and Devices,” TRADE.GOV. The 2024 medical-residency walkout dampened elective revenue, prompting procurement delays and multi-year leasing over outright purchase. Helium-free magnet designs promise 20% lifecycle-cost savings yet carry a 6–9-month lead time amid global supply bottlenecks. Provincial consortiums leverage pooled purchasing to secure volume rebates, but smaller private clinics still struggle to reach required thresholds.

Shortage of Trained MRI Technologists Outside Metro Areas

South Korea produces roughly 300 new MRI technologists annually, far short of the 500 required to meet projected 2027 demand, leaving vacancy rates of 14% in rural centers [3]Korea Economic Institute of America, “Addressing South Korea’s Provider-to-Patient Ratio Crisis,” KEIA.ORG . The 2024 enrollment-expansion dispute triggered attrition as clinicians shifted to metropolitan posts or private tele-consult firms. Facilities without full-time technologists resort to part-time staffing, limiting operating hours by up to 40% and elongating patient queues. Government incentives now subsidize relocation stipends and distance-learning refresher courses, yet impact will materialize only from the 2026–2027 academic cohorts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Preserve Dominance While Open Platforms Gain Momentum

Closed scanners commanded 75.12% of the South Korea MRI market share in 2025, reflecting clinician preference for 1.5 T and 3 T magnets that deliver high-resolution studies across neuro-oncologic pathways. The South Korea MRI market size tied to closed architecture is projected to expand at a 5.08% CAGR, supported by AI-assisted reconstruction that reduces table time and lowers break-even volume thresholds. Siemens’ helium-light MAGNETOM Flow and GE’s SIGNA Prime illustrate vendor push toward sustainability and install-distance flexibility, trimming plant-room costs by 10–12%.

Open systems, although holding a modest 24.88% revenue share, are forecast to outpace overall market growth at 5.94% CAGR as claustrophobia mitigation and intra-operative applications rise. Musculoskeletal surgeons favor open vertical fields that allow joint-specific positioning during real-time guidance, while pediatric departments cite lower sedation rates. Korean start-ups are integrating lightweight gradient coils with AI noise-reduction algorithms, elevating open-system image quality to near-1.5 T closed standards. As patient-centric care models spread, open scanners create a new competitive axis centered on comfort and access rather than sheer magnet strength, ensuring that the South Korea MRI market does not remain monolithic around closed platforms.

By Field Strength: 1.5 T Remains the Workhorse as 3 T Research Uptake Accelerates

High-field 1.5 T instruments captured 55.63% of the South Korea MRI market size in 2025, prized for balanced cost and versatility in routine brain, abdomen, and cardiac exams. Facilities report 96% first-time-right rates for diagnostic neuro indications, while energy-efficient gradients cut power consumption by 15% versus 2022 models. The plateauing of 1.5 T adoption encourages vendors to bundle mid-life upgrades—software-based SNR boosts and 64-channel coil arrays—to defend installed-base revenue.

Very-high-field 3 T and ultra-high ≥ 7 T segments recorded a combined 5.65% CAGR, driven by functional neuro-imaging and advanced oncology staging protocols. Research consortia such as the Korean Brain Connectome Project secure MOHW grants that cover up to 40% of acquisition cost for 7 T scanners, stimulating clinical-research crossover. Canon’s Vantage Galan 3 T Supreme Edition promises 20% faster diffusion studies and AI motion correction, announcing its first Korean installation at Pusan National University Hospital in 2025. While helium logistics remain a concern for ≥ 3 T suites, vendor adoption of cryo-coolers requiring ≤ 7 liters of helium per year eases operational budgeting.

By Application: Neurology Dominates, Oncology Registers Fastest Expansion

Neurology generated 41.88% of 2025 revenue, cementing its lead through MRI’s unmatched demyelination detection and stroke triage capacity. Functional MRI protocols, once confined to research, now inform surgical planning for epilepsy and glioma cases, raising reimbursement tiers under the 2025 fee revision. Investments in AI based seizure-focus localization cut radiologist read time by 30% and drive broader usage among secondary hospitals.

Oncology, the fastest-rising segment with a 6.02% CAGR, gains impetus from mandated screening for liver, pancreatic, and prostate cancers. Breath-hold liver DWI sequences reduced motion artifacts by 18%, enhancing lesion detectability in hepatocellular carcinoma prevalent regions. Hybrid PET/MRI suites, combined with radiomics-based tumor response monitoring, position MRI as an indispensable tool in precision-medicine protocols. Cardiology, gastroenterology, and musculoskeletal applications round out the modality mix, benefiting from algorithmic post-processing that widens the clinical envelope without hardware upgrades, reinforcing the diversified revenue base within the South Korea MRI market.

By End User: Hospitals Lead While Specialized Centers Capture Growth Upside

Hospitals controlled 47.60% of 2025 system revenue, driven by emergency coverage mandates, broad modality portfolios, and research affiliations that favor high-field installations. The Essential Healthcare Recovery Fund earmarks KRW 10 trillion for hospital imaging modernization, financing replacement cycles for magnets older than eight years.

Specialized imaging centers and single-specialty clinics account for just under one-third of value yet post a 6.18% CAGR, reflecting urban consumer demand for shorter wait times and transparent pricing. These centers often deploy one-or-two-room footprints in commercial complexes, leveraging AI scheduling to maximize gantry uptime. Portable point-of-care pods debut in orthopedic and sports-medicine chains, demonstrating same-day ankle and knee assessments without referral delays. Academic and research institutes, though the smallest buyer group, influence vendor roadmaps through collaborative AI algorithm validation and early adoption of 7 T prototypes.

Geography Analysis

Metropolitan clusters dominate MRI penetration, with Seoul, Incheon, and Busan hosting 61% of installed scanners by 2025. University hospitals in the Seoul Capital Area routinely operate 24/7 imaging shifts, driving per-scanner utilization above 3,500 exams yearly. Government sponsorship of digital-health corridors positions Incheon’s Songdo Bio-Cluster as a test bed for AI-reconstructed MRI workflows, thus reinforcing vendor preference for early commercial launches in the region.

Growth potential resides in Chungcheong, Gangwon, and Jeolla provinces where scanner density lags the national average of 37 units per million residents by roughly 30%. Rural hospitals leverage mobile MRI trailers under public–private partnerships that achieve 85% capacity utilization within eight months of deployment. The Act on Integrated Support for Community Care incentivizes provincial councils to co-finance imaging hubs, shrinking travel distance for seniors by 28 km on average.

Medical tourism exerts a moderate pull; although cosmetic and orthopedic procedures dominate arrivals, tertiary hospitals package full-body MRI check-ups into premium wellness itineraries targeting patients from Southeast Asia and the Middle East. Geopolitical supply-chain reassessments encourage local magnet manufacturing near Chuncheon’s upcoming 550,000 m² industrial complex, expected online in 2028, which could rebalance import dependence in favor of domestic value-add. Regional disparity remains tied to technician availability, leading vendors to bundle remote-operation consoles that allow metro-based specialists to guide scans in provincial facilities, an emerging model that promises to level care quality across the South Korea MRI market.

Competitive Landscape

International majors—Siemens Healthineers, Philips, GE HealthCare, and Canon Medical—collectively control an estimated 68% of annual sales, leveraging brand cachet, broad service networks, and R&D pipelines rich in helium-light magnets and AI toolkits. Siemens’ 2024 investment in superconducting-magnet capacity and its Korean R&D alliance with AI-cardiac firm Phantomics illustrate a dual play on component self-sufficiency and algorithmic differentiation. GE’s collaboration with provincial consortia to deploy compact 0.7 T point-of-care units extends reach into community clinics once deemed non-viable for conventional suites.

Local innovators inject competitive dynamism: AIRS Medical’s FDA-cleared SwiftMR algorithm retrofits multi-vendor fleets, winning service-contract add-ons even where hardware replacement is deferred. Samsung Ventures’ stake in Subtle Medical underscores domestic appetite for augmentation software that transcends OEM silos. Hyperfine pilots low-field bedside systems in emergency departments, potentially disrupting patient routing and follow-up imaging patterns.

Strategic moves in 2024–2025 revolve around ecosystem building rather than pure hardware. Philips signed a multi-year AI research deal with Mayo Clinic to refine cardiac MRI on implant-bearing patients, while Canon partnered with NVIDIA to accelerate reconstruction on the Vantage Galan 3 T. Competitive narratives highlight measurable throughput and cost metrics; for instance, Siemens publicizes a 20% reduction in site preparation costs for the MAGNETOM Flow versus prior 1.5 T models, shaping purchasing criteria beyond magnet strength alone. The South Korea MRI market’s moderate concentration favors suppliers that integrate hardware, software, and service into cohesive value propositions supportive of both metro megacenters and resource-strained provincial hospitals.

South Korea Magnetic Resonance Imaging Industry Leaders

-

Siemens AG

-

Canon Medical Systems

-

GE Healthcare

-

Fujifilm Holdings Corporation

-

Koninklijke Philips NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Siemens Healthineers Korea signs an MOU with Phantomics to integrate the Myomics AI cardiac MRI suite into clinical workflow.

- July 2025: AIRS Medical releases a major SwiftMR update, adding expanded protocol coverage and autonomous QC functions.

- February 2025: Incepto partners with AIRS Medical to distribute SwiftMR across Europe, targeting 50% scan-time reductions.

- November 2024: Lunit partners with Salud Digna to supply AI chest-X-ray and mammography systems to 230+ clinics in Mexico.

South Korea Magnetic Resonance Imaging Market Report Scope

As per the scope of this report, Magnetic resonance imaging is a medical imaging technique, which is used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body. South Korea Magnetic Resonance Imaging (MRI) Market is segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, Very High Field MRI Systems, and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications). The report offers the value (in USD million) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (< 1.5 T) |

| High-Field (1.5 T) |

| Very-High (3 T) & Ultra-High (≥ 7 T) |

By Application

| Oncology |

| Neurology |

| Cardiology |

| Gastroenterology |

| Musculoskeletal |

| Other Applications |

By End User

| Hospitals |

| Specialized Clinics & Imaging Centers |

| Research & Academic Institutes |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (< 1.5 T) |

| High-Field (1.5 T) | |

| Very-High (3 T) & Ultra-High (≥ 7 T) | |

| By Application | Oncology |

| Neurology | |

| Cardiology | |

| Gastroenterology | |

| Musculoskeletal | |

| Other Applications | |

| By End User | Hospitals |

| Specialized Clinics & Imaging Centers | |

| Research & Academic Institutes |

Key Questions Answered in the Report

How big is the South Korea Magnetic Resonance Imaging Market?

The South Korea Magnetic Resonance Imaging Market size is expected to reach USD 346.39 million in 2026 and grow at a CAGR of 5.32% to reach USD 448.71 million by 2031.

Which product category leads sales in Korean imaging suites?

Closed 1.5 T and 3 T systems held 75.12% revenue in 2025 and remain the dominant choice for broad clinical versatility.

Who are the key players in South Korea Magnetic Resonance Imaging Market?

Siemens AG, Canon Medical Systems, GE Healthcare, Fujifilm Holdings Corporation and Koninklijke Philips NV are the major companies operating in the South Korea Magnetic Resonance Imaging Market.

What drives the jump in oncology-focused MRI usage?

National Health Insurance now reimburses expanded cancer staging procedures, pushing oncology MRI to the fastest 6.02% CAGR through 2031.

Page last updated on: