Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

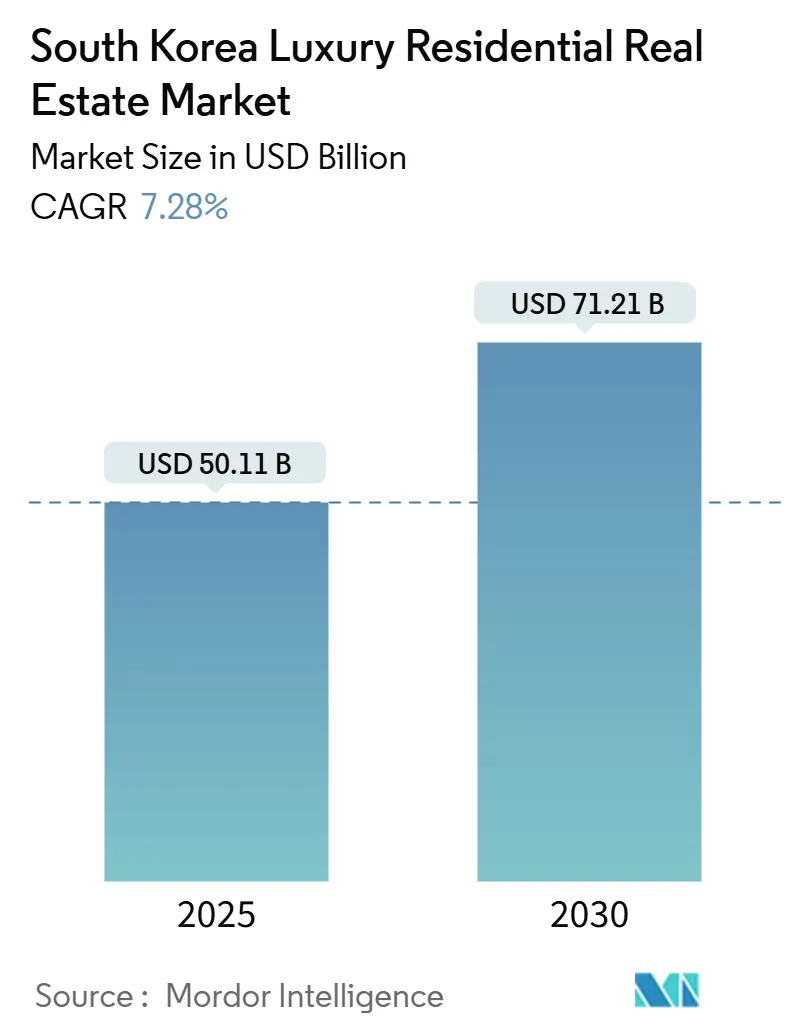

| Market Size (2025) | USD 50.11 Billion |

| Market Size (2030) | USD 71.21 Billion |

| Growth Rate (2025 - 2030) | 7.28% CAGR |

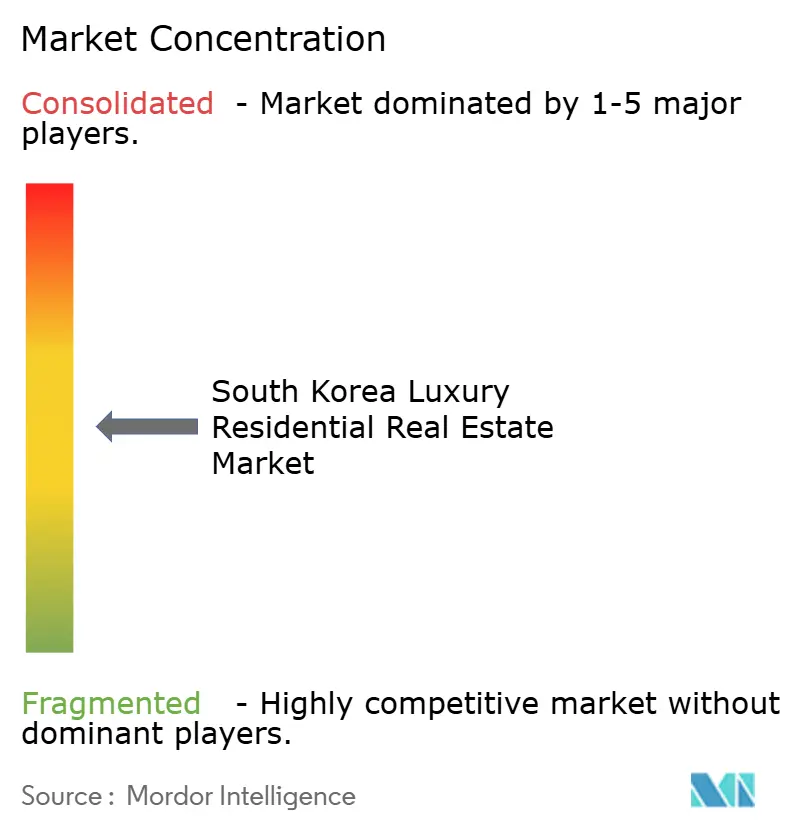

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The South Korea luxury residential real estate market size stood at USD 46.71 billion in 2024 and is forecast to rise to USD 71.21 billion by 2030, reflecting a robust 7.28% CAGR for the period. Demand has stayed resilient even as regulators tighten credit standards and impose transaction permits, confirming the depth of genuine end-user appetite for high-end homes. A growing pool of domestic high-net-worth individuals (HNWIs), a steady inflow of foreign capital, and the enduring scarcity of prime land in Seoul together reinforce price strength despite macroeconomic headwinds. Developers are responding with technology-rich, sustainability-certified projects that align with both the Zero Energy Building mandate and rising ESG preferences among younger affluent buyers. Celebrity endorsements, landmark transactions, and the network effect created by clusters of high-profile residents continue to keep Seoul at the epicenter of luxury price discovery, while the rental model and secondary cities such as Incheon show stronger percentage growth.

Key Report Takeaways

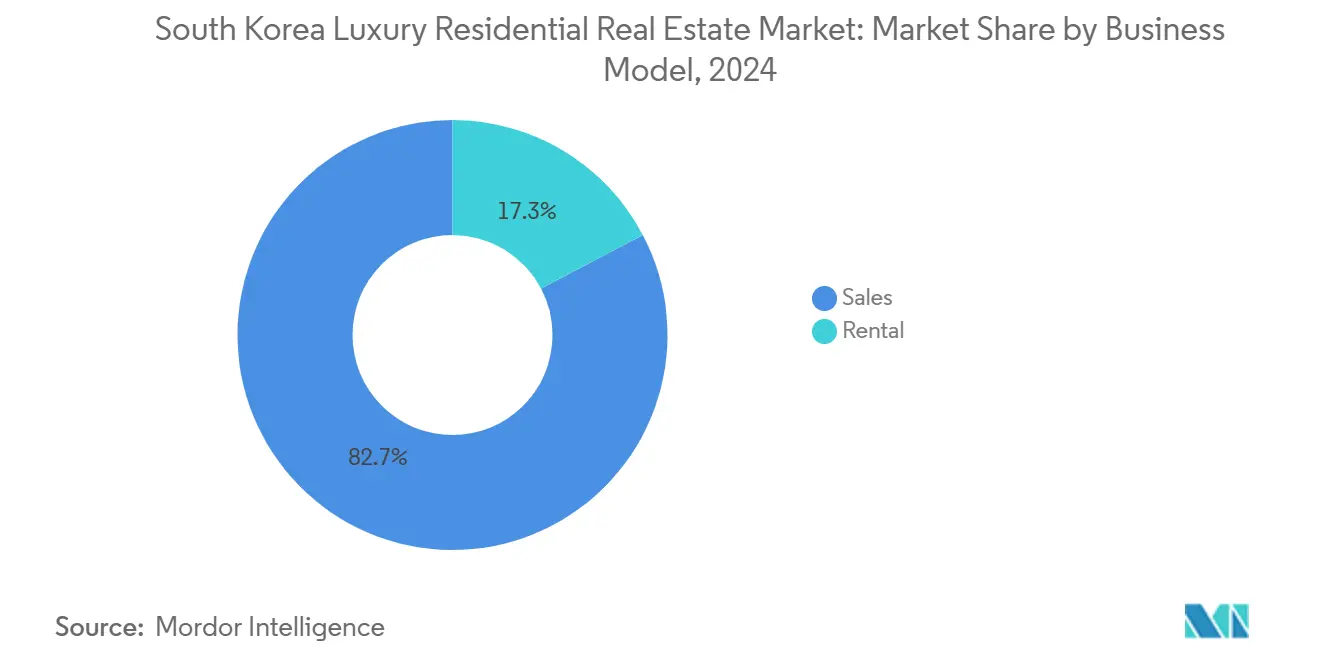

- By business model, sales captured 82.7% of 2024 revenue, while the rental segment is forecast to expand at a 7.97% CAGR through 2030, indicating a rental renaissance among younger affluent demographics.

- By property type, apartments and condominiums commanded 66.2% of the 2024 South Korea luxury residential real estate market size, yet villas and landed houses are set to grow at the quickest 8.16% pace through 2030 as buyers seek privacy and outdoor space.

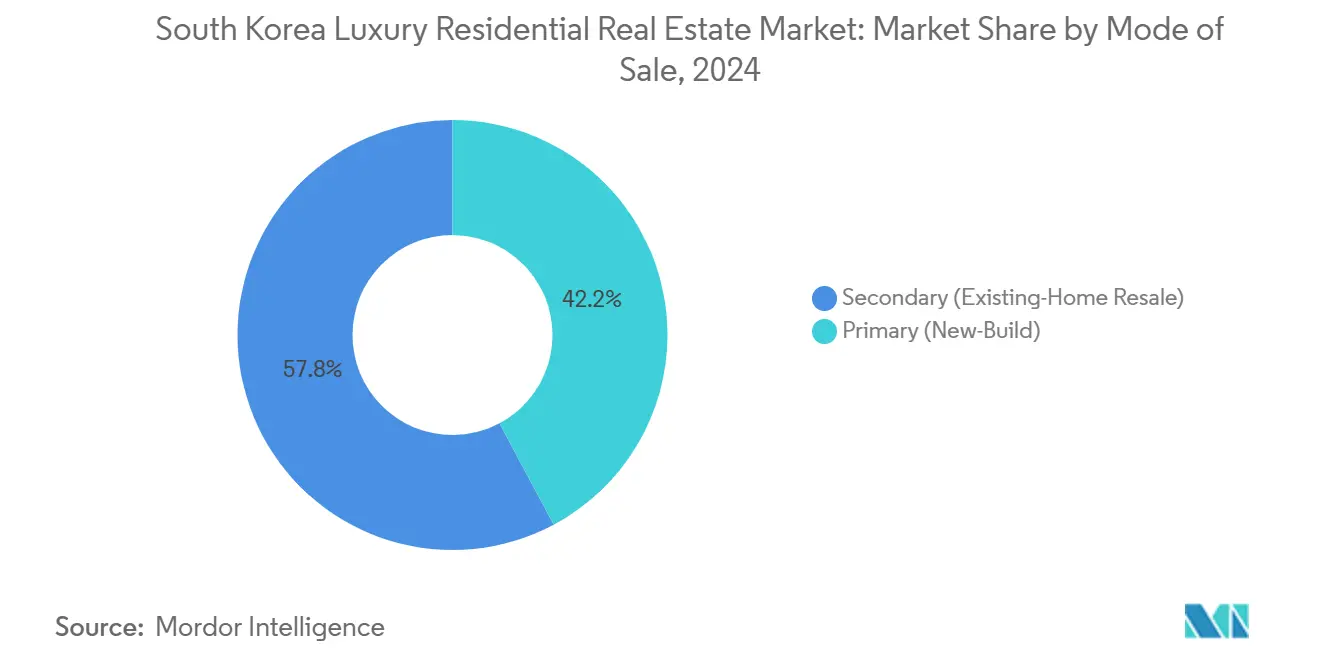

- By mode of sale, secondary transactions represented 57.8% of 2024 activity, whereas primary developments are advancing at an 8.31% CAGR, propelled by smart-home integration and sustainability features.

- By city, Seoul accounted for 72.8% of the South Korea luxury residential real estate market share in 2024, whereas Incheon is projected to record the fastest 9.07% CAGR to 2030.

South Korea Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand in Seoul and Busan for premium apartments and branded residences | +1.8% | Seoul metropolitan area, Busan core districts | Medium term (2-4 years) |

| Rising wealth among domestic high-net-worth individuals is fueling luxury housing purchases | +1.5% | National, concentrated in Seoul, Busan, Incheon | Long term (≥ 4 years) |

| Limited land supply in major cities is creating scarcity-driven price appreciation | +1.2% | Seoul, Busan, Daegu urban cores | Long term (≥ 4 years) |

| Strong preference for smart, high-tech, and sustainability-integrated luxury residences | +0.9% | National, early adoption in Seoul, Incheon | Medium term (2-4 years) |

| Foreign buyer interest is supported by Korea’s global city positioning and cultural appeal | +0.7% | Seoul, Busan, with spillover to secondary cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Demand in Seoul and Busan for Premium Apartments and Branded Residences

Seoul has reached an inflection point where branded residences command clear premiums rooted in architecture, curation, and concierge-level services. Complexes such as The Penthouse Cheongdam have led Korea’s price charts for four consecutive years, with 407.71 m² units recording USD 12.2 million in public disclosures, a USD 120,000 uptick over the prior year. Busan mirrors that momentum; official assessments showed 1.47% price growth for 2025, led by Gijang-gun’s 2.15% rise on the back of new infrastructure. Celebrity residents in Nine One Hannam and Eterno Cheongdam create aspirational spillovers that cement premium price points, and this endorsement effect is spreading to Busan’s coastal towers. Developers now bundle private dining, spa, and club facilities into the branded offer, raising benchmarks across both cities[1]Hyun-Jin Kim, “2025 Standard Housing Price Trend,” Busan Metropolitan Government, busan.go.kr.

Rising Wealth Among Domestic High-Net-Worth Individuals Fueling Luxury Housing Purchases

Korea’s millionaire cohort is forecast to climb from 1.3 million in 2023 to 1.64 million in 2028, a 27% jump that materially widens the luxury buyer base. Millennials and Gen X millionaires, growing twice as fast as older cohorts, allocate 20.4% of investable assets to property and exhibit above-average risk tolerance. Cryptocurrency and technology entrepreneurs increasingly prize smart-home automation and green credentials over traditional luxury cues, steering demand toward Zero Energy-certified towers. In Seoul’s Gangnam district, prices rose 7.2% in 2024, evidence of wealth concentration combining with redevelopment pipelines to keep high-end stock scarce. The demographic shift, therefore, embeds structural depth into demand instead of a purely cyclical bounce.

Limited Land Supply in Major Cities Creating Scarcity-Driven Price Appreciation

Seoul and Busan possess tight zoning and heritage overlays that keep luxury development sites rare, insulating values even when mid-market prices soften. Planned maintenance projects in Seongnam-si will add 50,000 apartments, yet most fall outside luxury price bands and do little to ease shortages for premium buyers. Median Seoul apartment values breached USD 689,085 in 2024, but luxury addresses trade at multiples of that baseline owing to location, views, and amenity blends. Environmental rules further restrict high-rise approvals in heritage corridors, creating a structural floor under existing prime assets. The resulting imbalance ensures price stability and defensive investment characteristics that appeal to wealth-preservation strategies.

Strong Preference for Smart, High-Tech and Sustainability-Integrated Luxury Residences

Since the Zero Energy Building (ZEB) standard took effect in 2017, energy-positive design has moved from optional to mandatory in the upper tier. The Smart City Act reinforces this shift by funding integrated digital infrastructure, helping new projects differentiate through technology rather than postcode alone. A revival of modernized hanok villas reveals how tradition and technology converge; residents cite natural ventilation and timber aesthetics enhanced by IoT-based climate control. Buyers now scrutinize energy dashboards, carbon metrics, and connectivity scores before price per square foot, pushing developers to bundle advanced automation, EV charging, and grey-water recycling as standard inclusions. These expectations extend from Seoul to Incheon as the MZ generation brings ESG priorities to real-estate decisions.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict government regulations on property purchases and speculation curbing demand | -1.4% | Seoul metropolitan area, Busan, Daegu | Short term (≤ 2 years) |

| High taxation and ownership costs reducing attractiveness for some luxury investors | -0.8% | National, concentrated in high-value districts | Medium term (2-4 years) |

| Economic headwinds and demographic challenges impacting long-term luxury demand growth | -0.6% | National, with regional variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Government Regulations on Property Purchases and Speculation Curbing Demand

Apartment trading permits enacted in Gangnam, Seocho, Songpa, and Yongsan until September 2025 oblige buyers to prove primary-residence intent, disqualifying purely speculative deals. Capital-gains rules for newly married couples extended the exemption horizon from five to 10 years, lengthening required holding periods and discouraging quick flips. Foreign buyers face heightened scrutiny, with transaction audits aimed at deterring market distortion even as legal frameworks struggle to police beneficial-ownership structures. Stress-interest ratios introduced in February 2024 reduce loan capacity by 2–4 percentage points, adding friction to leverage-driven purchases. Collectively, these moves thin buyer pools in the short term yet raise the quality of demand over time[2]Joon-Ho Park, “2024 Housing Transaction Permit Expansion Notice,” Ministry of Land, Infrastructure and Transport, molit.go.kr.

High Taxation and Ownership Costs Reduce Attractiveness for Some Luxury Investors

Acquisition taxes start at 4% and climb for premium assets, while annual property levies range up to 0.4% with surcharges in overconcentration zones. 2025 tax reforms clarified global minimum-tax rules for multinationals and trimmed reliefs, adding complexity for foreign executives seeking pied-à-terres. Transfer taxes on exit compound the carrying costs, spurring certain investors to diversify toward lower-tax jurisdictions or liquid assets. Despite the fiscal load, lifestyle-driven buyers continue to transact given the intangible value of location, school catchments, and prestige. Consequently, taxation tempers speculative froth without derailing core demand[3]Sang-Min Lee, “2025 National Tax Revision Highlights,” Ministry of Economy and Finance, moef.go.kr.

Segment Analysis

By Business Model: Rental Demand Accelerates While Sales Remain Dominant

Rental products generated the highest growth momentum, advancing at a 7.97% CAGR to 2030, while sales retained 82.7% of 2024 revenue. That divergence signals evolving consumption patterns in the South Korea luxury residential real estate market as mobility-minded professionals and global expats seek flexibility. Institutional landlords such as IGIS Asset Management are scaling portfolios, unlocking annuity cash flows for investors and premium amenities for tenants. In contrast, legacy family wealth still favors title deeds, preserving volume dominance for outright sales. Looking ahead, the rental option offers a risk-adjusted avenue for developers to monetize land holdings without immediate sell-down pressure.

The acceleration of the rental model corresponds with regulatory biases; trading-permit rules aimed at speculation leave leasing untouched, letting landlords service demand that formerly funneled into quick resales. Maturing capital markets structures further normalize build-to-rent as a strategic asset class, mirroring global gateway-city trends. Consequently, the South Korea luxury residential real estate market size attributable to rental inflows is poised to compound even if sales values set pricing benchmarks.

By Property Type: Villas and Landed Houses Outpace High-Rise Stock

Apartments and condominiums still comprise 66.2% of 2024 spending, reflecting supply depth and cultural familiarity with tower living. Yet villas and landed houses are on course for an 8.16% growth trajectory into 2030, outstripping vertical formats. The privacy, yard space, and customization available in landed products resonate with post-pandemic wellness priorities. Moreover, zoning restrictions mean each villa built removes disproportionate land from future supply, magnifying scarcity. Where villas emerge—often on Seoul’s city-fringe hillsides—the South Korea luxury residential real estate market share for that micro-segment quickly reaches double-digit absorption because ultra-HNWIs prize exclusivity over density.

Modernized hanok compounds capture an additional lifestyle layer by weaving heritage aesthetics with geothermal heating, triple-glazed paper windows, and discreet IoT sensors. While development costs are higher, per-square-foot premiums offset capital outlays, enabling favorable margins. Accordingly, villas form the experimental edge of luxury design, with lessons cascading into next-generation apartment towers.

By Mode of Sale: Primary Projects Gain Ground on Secondary Inventory

Secondary stock generated 57.8% of 2024 turnover due to the simple fact that many prized addresses were completed years ago and rarely replicated. However, primary projects are set to clock an 8.31% CAGR, led by technology-heavy launches such as Lotte E&C’s 805-unit Kaya Station Lotte Castle SkyL in Busan. Buyers appreciate clean warranties, optimum floor-plate utilization, and embedded sustainability features not always feasible in retrofits. For developers, presales finance construction and lock-in revenues despite subdued broader credit conditions.

In prime Seoul, constraints on fresh land supply cap absolute primary volume, but every newly zoned plot attracts intense HNWI interest, validating higher starting prices. Where suburban or secondary-city plots exist, contemporary master plans fuse residential towers with mixed-use retail, schools, and transit nodes, lifting livability benchmarks. Over the medium term, primary launches will continue to nibble share from secondary listings on the back of experience-centric design and regulatory compliance advantages.

Geography Analysis

Seoul generated 72.8% of the 2024 South Korea luxury residential real estate market revenue, underscoring its unrivaled mix of finance, entertainment, and designer retail precincts. Tight trade-permit controls in Gangnam, Seocho, Songpa, and Yongsan have thinned speculative churn yet inadvertently reinforced scarcity, sustaining pricing power for legacy towers and newer smart-home developments. International schools, Michelin-star dining, and global brand boutiques further anchor aspirational value for both domestic and expatriate residents, ensuring turnover even during macro lulls.

Incheon is the fastest-growing luxury node, projected at a 9.07% CAGR, aided by Songdo International Business District’s tech infrastructure and proximity to the international airport. Projects designed under the Smart City Act embed energy-efficiency and 5G connectivity from day one, attracting millennial millionaires priced out of central Seoul but unwilling to compromise on amenities. Government incentives for foreign headquarters also encourage executive relocations, widening the luxury tenant base.

Busan maintains second-tier primacy through its coastal lifestyle and cultural festivals. Assessed prices advanced 1.47% for 2025 despite nationwide cooldowns, helped by waterfront reclamations and hospitality-linked branded residences. Lotte E&C’s new launches capitalize on metro extensions and department-store adjacencies, reinforcing Busan’s tourist-friendly luxury narrative.

Daegu, plus the rest of South Korea, collectively hold a modest share today yet represent optionality for buyers seeking larger plots and lower entry points. Developments like Kolon Global’s Byeongyoungro Skychae Lac View in Ulsan illustrate how regional urban centers position luxury stock near scenic rivers and green belts. Sustained high-speed rail investments and local government tax sweeteners could catalyze incremental redistribution of high-end demand, albeit Seoul is expected to stay the anchor.

Competitive Landscape

The market displays moderate concentration, with the top five chaebol-linked contractors controlling the majority of signature projects yet facing fresh competition from asset-management arms and boutique specialists. Samsung C&T, Daewoo E&C, and POSCO E&C leverage integrated land-banking, EPC, and financing capabilities to win redevelopment tenders in constrained districts. Their premium sub-brands, Raemian, Prugio Supex, and The Sharp, signal quality and assist in presale velocity. Mid-tier developers differentiate through design partnerships with global architects and early adoption of biophilic features.

Institutional investors are deepening involvement. Hana Financial Group’s KRW 50 trillion (USD 34 billion) asset-management merger underscores shifting capital toward rent-yielding luxury holdings. Private equity firms increasingly back build-to-rent platforms in Songdo and Yongin, incentivized by tax-deductible depreciation and stable tenant rolls. Regulatory hurdles in foreign land acquisition favor domestic incumbents, yet joint ventures with Japanese and Singaporean developers appear when local know-how pairs with offshore capital.

Technology and ESG form the new competitive frontier. Developers race to integrate AI-driven climate control, facial-recognition entry, and digital concierge platforms. Meanwhile, ZEB compliance and green-bond financing tilt buyer sentiment toward schemes with transparent sustainability reporting. Overall, rivalry is pivoting from the domain of mere address prestige to holistic lifestyle ecosystems.

South Korea Luxury Residential Real Estate Industry Leaders

Samsung C&T Corporation

Daewoo Engineering & Construction

KyeRyong Construction Industrial

Hoban Construction

DL Construction

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hana Financial Group finalized the merger of Hana Asset Management and Hana Alternative Asset Management, creating a USD 34 billion real-estate platform positioned to expand build-to-rent luxury portfolios nationwide.

- March 2025: Apartment-trading permits began in Gangnam, Seocho, Songpa, and Yongsan, granting councils power to reject deals lacking primary-residence intent, a measure aimed at curbing speculation while preserving genuine luxury demand.

- August 2024: Kolon Global launched Byeongyoungro Skychae Lac View in Ulsan, an 803-unit luxury complex offering interest-free interim payments to capture younger affluent buyers in regional markets.

- March 2024: Lotte Engineering & Construction unveiled Kaya Station Lotte Castle SkyL in Busan with 805 households and integrated retail, confirming continued developer confidence outside the capital.

South Korea Luxury Residential Real Estate Market Report Scope

Real estate is deemed "luxury" when it includes a desirable location, a high asking price, a substantial size, priceless materials, professional design, upscale facilities, and a distinguished past. Luxury real estate often includes a valuation that falls among the top 10% of houses on the local market. The report covers a complete background analysis of the South Korean luxury residential real estate market. It includes the economic assessment and sector contribution to the economy, market overview, market size estimation for key segments, emerging market segments, market dynamics, geographical trends, and the impact of geopolitics and pandemic on the market.

The South Korean luxury residential real estate market is segmented by type (apartments and condominiums, villas, and landed houses) and cities (Seoul, Busan, and other cities).

The report offers the South Korean luxury residential real estate market size and forecasts in value (USD) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

How large is the South Korea luxury residential real estate market in 2025?

It is valued at USD 46.71 billion and is projected to compound at 7.28% annually to 2030.

Which city commands the highest share of Korean luxury home sales?

Seoul leads with 72.8% of 2024 value, thanks to deep HNWI pools and unmatched lifestyle infrastructure.

What is driving growth in Korea’s luxury rental segment?

Younger millionaires and expatriate executives favor flexibility, pushing luxury rentals toward a 7.97% CAGR through 2030.

Why are villas growing faster than apartments in Korea’s high-end market?

Post-pandemic lifestyle shifts toward privacy and outdoor space are propelling villas at an 8.16% growth rate.

Page last updated on: