Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

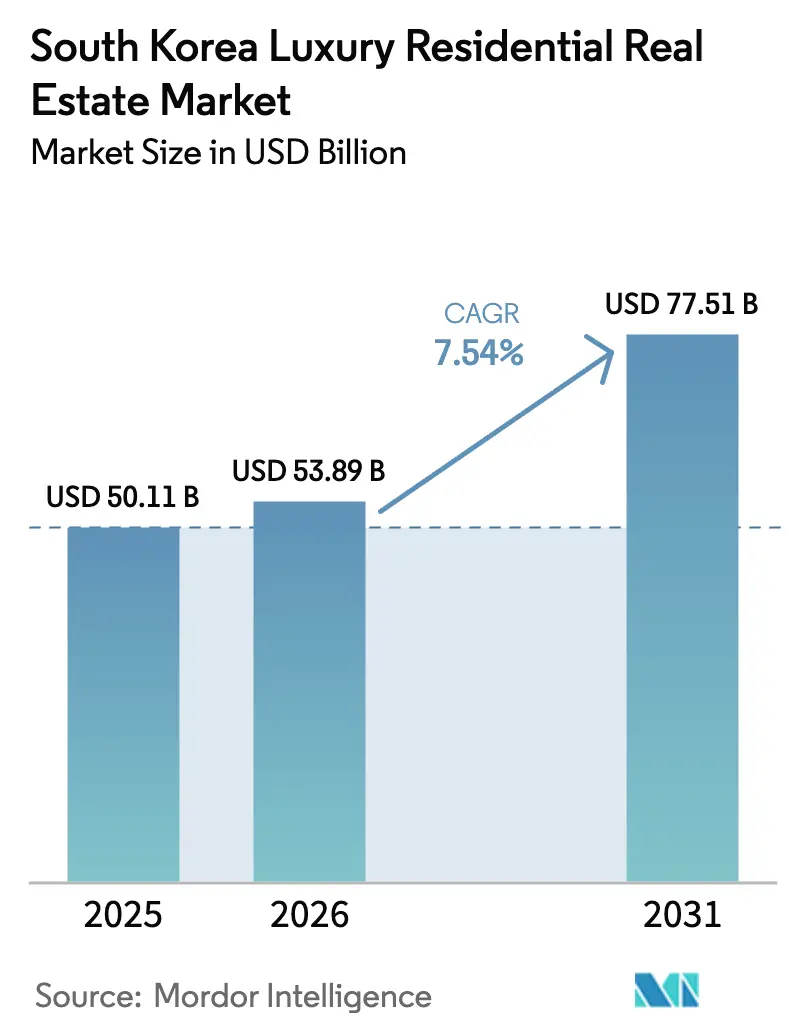

| Base Year Market Size (2025) | USD 50.11 Billion |

| Market Size (2026) | USD 53.89 Billion |

| Market Size (2031) | USD 77.51 Billion |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The South Korea Luxury Residential Real Estate Market size is projected to be USD 50.11 billion in 2025, USD 53.89 billion in 2026, and reach USD 77.51 billion by 2031, growing at a CAGR of 7.54% from 2026 to 2031.

Limited land supply in Seoul’s core, a dense concentration of high-net-worth individuals (HNWIs), and deep‐rooted brand preferences keep demand resilient despite tighter fiscal rules. Foreign buyers, mainly Chinese nationals, continue to view prime Seoul addresses as currency and political hedges, sustaining cross-border capital inflows even after the August 2024 permit-zone expansion. Developers are therefore prioritizing mixed-use megaprojects with artificial-intelligence (AI) security suites and internet-of-things (IoT) energy management, which command 10-15% price premiums over non-branded stock. Meanwhile, villas and landed houses are emerging as a privacy-driven alternative for ultra-HNWIs and are projected to outpace apartments in growth. Finally, the Bank of Korea’s rate cuts have softened mortgage costs, yet stringent loan-to-value (LTV) and debt-service-ratio (DSR) caps continue to favor buyers with ample liquidity.

Key Report Takeaways

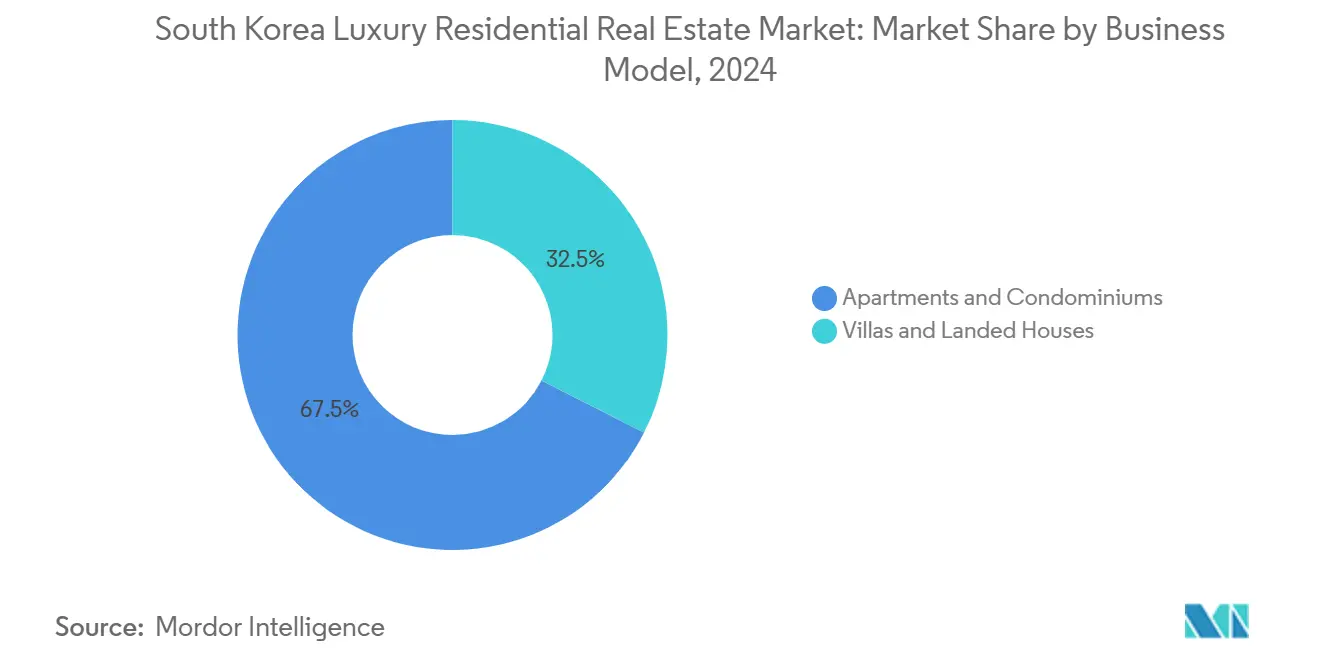

- By property type, apartments and condominiums led with 67.5% of South Korea's luxury residential real estate market share in 2025, while villas and landed houses are set to expand at an 8.27% CAGR through 2031.

- By business model, sales transactions led with 84% of South Korea's luxury residential real estate market share in 2025, while rentals are projected to expand at an 8.07% CAGR through 2031 on the back of expatriate demand in Songdo and Incheon.

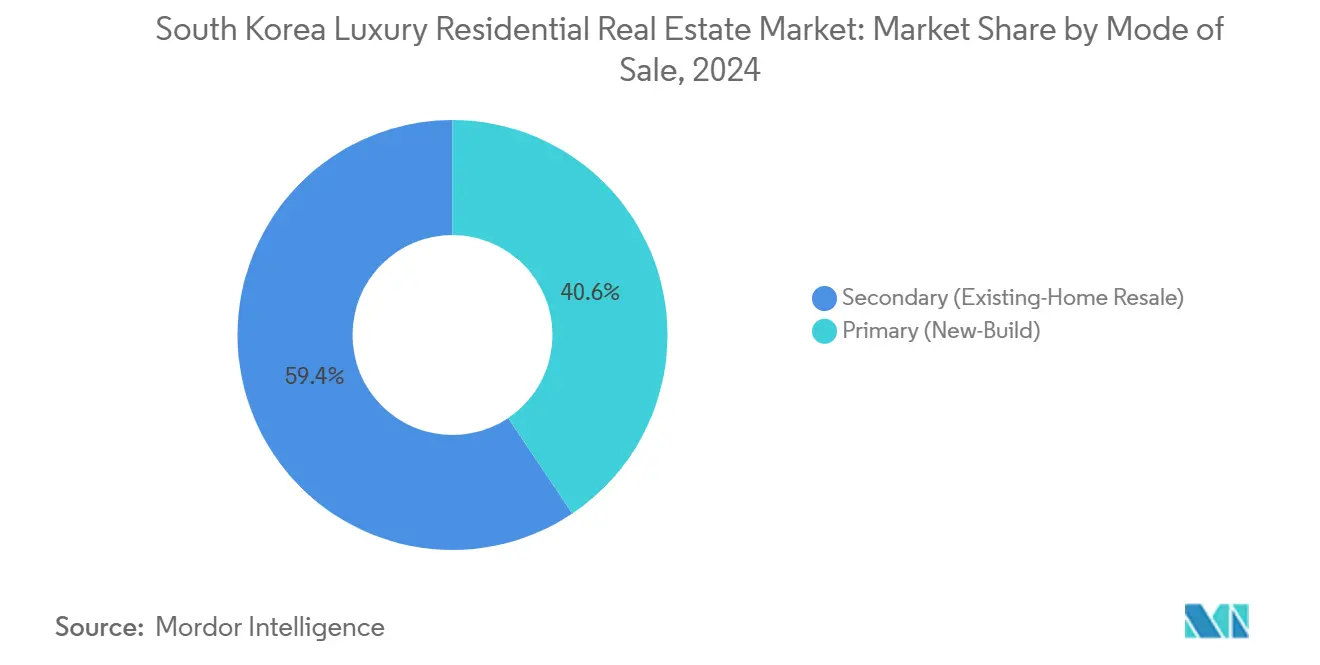

- By mode of sale, secondary (existing-home) deals held a 59.4% share in 2025, yet primary launches are forecast to grow at 8.41% CAGR thanks to tech-integrated branded projects.

- By city, Seoul accounted for 74.6% of the South Korea luxury residential real estate market size in 2025, and Incheon is set to expand at a 9.19% CAGR through 2031, supported by Songdo smart-city development.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising High-Net-Worth Population in Seoul Drives Ultra-Premium Housing Demand | 1.8% | Seoul (Gangnam, Hannam, Cheongdam), spillover to Songdo | Medium term (2-4 years) |

| Limited Land Availability in Prime Seoul Locations Sustains Luxury Price Growth | 1.5% | Seoul core districts, Yongsan IBD | Long term (≥ 4 years) |

| Preference for Branded High-Rise Apartments Boosts Premium Property Sales | 1.3% | Seoul, Incheon (Songdo), Busan (Haeundae) | Short term (≤ 2 years) |

| Rising Foreign Investor Interest Increases Cross-Border Luxury Transactions | 1.2% | Seoul (Gangnam, Hannam), Incheon, Busan | Medium term (2-4 years) |

| Expansion of Luxury Mixed-Use Developments Enhances Buyer Appeal | 1.0% | Seoul (Yongsan IBD), Incheon (Songdo), Busan | Medium term (2-4 years) |

| Limited Supply of Ultra-Luxury Villas and Penthouses Supports Value Growth | 0.9% | Seoul (Hannam, Seongbuk-gu), Busan (Haeundae) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising High-Net-Worth Population in Seoul Drives Ultra-Premium Housing Demand

Gangnam, Hannam, and Cheongdam have become wealth nodes where proximity to finance, luxury retail, and international schools reinforces further HNWI clustering. Record 2025 deals, such as Nine One Hannam at USD 18.5 million, confirm that location prestige outweighs unit size. The social network effect reduces search costs for buyers who value anonymity and peer signaling. As a result, these districts showed limited price elasticity even after acquisition-tax hikes. Chinese buyers also use a Gangnam address as a geopolitical hedge, supporting valuations amid domestic policy tightening.[1]Ministry of Land, Infrastructure and Transport, “Permit Zones Expansion Notice,” molit.go.kr

Limited Land Availability in Prime Seoul Locations Sustains Luxury Price Growth

Green-belt zoning around the capital creates artificial scarcity that developers counter through vertical densification and protracted land assembly. Yongsan International Business District (IBD) illustrates how 15-year planning cycles restrict near-term supply, thereby underpinning price resilience.[2]Seoul Metropolitan Government, “Yongsan IBD Master Plan,” english.seoul.go.krExisting low-rise villa zones such as Seongbuk-gu cap floor-area ratios at 150%, preventing tower conversions and reinforcing exclusivity. Consequently, new luxury inventory emerges only in sporadic waves, cushioning the segment against macro downturns.

Preference for Branded High-Rise Apartments Boosts Premium Property Sales

Brand loyalty is pronounced; Samsung C&T’s Raemian, Lotte E&C’s Castle, and HDC Hyundai’s I’Park are viewed as proxies for build quality and resale liquidity. Seventy-eight percent of 2025 launches embedded Samsung SDS or LG CNS IoT suites that cut energy bills by up to 20% and deploy biometric access. Branded units trade 25% faster than unbranded peers, justifying a 10-15% premium and entrenching market leaders.

Rising Foreign Investor Interest Increases Cross-Border Luxury Transactions

Chinese nationals represented 73% of foreign luxury purchases in 2025, followed by Americans (14%). Flight times under two hours, combined with Hallyu cultural affinity, keep Seoul attractive despite August 2024 permit requirements that now prolong closings by up to two months. Foreign ownership climbed to 12.3% in 2025, signaling that regulatory friction slowed but did not reverse inflows. Developers now staff bilingual sales teams and property-management desks tailored to absentee owners.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Property Tax and Ownership Regulations Dampen Luxury Investments | -1.1% | National, with acute impact in Seoul, Busan | Short term (≤ 2 years) |

| Tight Mortgage Lending and Loan-to-Value Limits Restrict Financing Access | -0.9% | National, particularly Seoul, regulated zones | Medium term (2-4 years) |

| High Acquisition and Capital Gains Taxes Reduce Luxury Transactions | -0.8% | National, concentrated in Seoul, Incheon | Short term (≤ 2 years) |

| Interest Rate Fluctuations and Economic Uncertainty Delay Luxury Purchases | -0.7% | National, with spillover to foreign buyer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Property Tax and Ownership Regulations Dampen Luxury Investments

Comprehensive holding taxes of up to 2.7%, surcharges for owners of three or more homes, and the 2024 permit-zone expansion have cooled speculative buying. Draft 2025 rules would further cap ownership at two units and impose a 3% vacancy levy on idle high-end stock.[3] Ministry of Economy and Finance, “Draft Real Estate Tax Reforms 2025,” moef.go.kr Consequently, luxury trades slid 18% year-on-year in Q1 2025.

Tight Mortgage Lending and Loan-to-Value Limits Restrict Financing Access

The Bank of Korea and Financial Services Commission keep LTVs at 50% and DSRs at 40%. A USD 2.22 million apartment, therefore, demands USD 1.11 million cash, restricting leverage to ultra-liquid investors. Non-resident foreigners remain ineligible for local mortgages, curbing demand from buyers reliant on debt.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartments Maintain Lead while Villas Accelerate

Apartments and condominiums controlled 67.5% of the South Korea luxury residential real estate market in 2025, underpinned by subway connectivity and on-site amenities. Villas, however, are projected to deliver the fastest growth, expanding at an 8.27% CAGR through 2031 as privacy, outdoor space, and customizable architecture gain favor among ultra-HNWIs. Branded towers such as Raemian and I’Park routinely bundle AI energy-management tools that trim utility bills by up to 20%.

The South Korea luxury residential real estate market size associated with villa transactions remains smaller than that of apartments, yet scarcity in Hannam-dong and Seongbuk-gu fuels competitive bidding at 5-10% annual price gains. Developers are piloting hybrid low-rise formats that mimic villa privacy within high-density sites, signaling an evolving product mix that could gradually narrow the share gap.

By Business Model: Sales Still Dominate but Rentals Gain Traction

Sales made up 84.0% of 2025 turnover, reflecting Korea’s home-ownership culture and tax incentives for primary residences. Rentals accounted for the rest but are forecast to grow fastest at an 8.07% CAGR, buoyed by multinational relocations to Songdo and Yongsan.

Institutional landlords such as IGIS Asset Management are scaling build-to-rent portfolios that incorporate bilingual concierge desks and corporate lease packages, aiming to raise the rental slice of South Korea luxury residential real estate market size to roughly 20% by 2031. If LTV caps persist, some would-be buyers may opt to rent, lending further momentum to this segment.

By Mode of Sale: Secondary Stock Commands Liquidity Premium

Secondary (existing-home resale) captured 59.4% of the South Korea luxury residential real estate market in 2025 as buyers prized immediate occupancy and proven building performance. Primary (new-build), although smaller in volume, are slated to expand at an 8.41% CAGR on IoT and biometric-security upgrades.

Primary launches embed AI concierges and green-building certifications that boost South Korea luxury residential real estate market share for branded developers. Yet delivery risk lengthens cash-conversion cycles, so liquidity-focused investors continue to prefer the secondary channel, where average days-on-market remain below 90.

Geography Analysis

Seoul controlled a commanding 74.6% of the 2025 value, thanks to a 65% concentration of national HNWIs, a dense network of international schools, and the USD 30 billion Yongsan IBD redevelopment that keeps future supply in the pipeline. Foreign ownership reached 12.3% despite new permit rules, underscoring the capital’s appeal as a safe haven for regional wealth.

Incheon is the fastest climber, advancing at a 9.19% CAGR through 2031 on Songdo’s 1,500-acre smart-city blueprint, airport expansion to 100 million passengers, and five-year property-tax holidays for new luxury purchases. Developers such as POSCO E&C position Songdo units roughly 40% below equivalent Gangnam prices, drawing both expatriate executives and value-oriented domestic buyers.

Busan thrives on Haeundae’s waterfront penthouses and cultural cachet from the Busan International Film Festival. Daegu and other secondary cities collectively captured 13% as high-speed rail cuts Seoul travel to under two hours, enabling weekend retreats and second-home demand. Still, network effects around Seoul’s finance and luxury retail core ensure it remains the anchor of the South Korean luxury residential real estate market.

Competitive Landscape

Competition is moderately concentrated: the top five chaebol builders, Samsung C&T, HDC Hyundai Development, Lotte E&C, GS E&C, and POSCO E&C, secured the majority share of 2025 luxury launches. Their vertical supply chains shave construction costs by up to 20% versus mid-tier rivals and underpin consistent brand premiums.

Strategic differentiation now hinges on technology. Samsung C&T’s 65-story Raemian Yongsan Tower sold 92% of units within three days thanks to AI energy dashboards and voice-activated controls, while HDC’s I’Park Songdo Marina aligns with yacht-club amenities to lure expatriate executives. GS E&C’s Xi uses building information modeling to cut defect rates by 25%, boosting buyer confidence.

Smaller players pursue niches: Booyoung specializes in bespoke villas with 15-year warranties, and Kolon Global converts heritage sites into signature penthouses. Prop-tech portals such as Zigbang have begun offering virtual-reality tours, reducing search friction, but off-market brokerage remains dominant for ultra-prime listings, insulating margins in the highest tiers.

South Korea Luxury Residential Real Estate Industry Leaders

Samsung C&T Corporation

Daewoo Engineering & Construction

KyeRyong Construction Industrial

Hoban Construction

DL Construction

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Hyundai E&C partnered with HND TS and CMP Construction to build a premium residential complex in Auckland. This marks a strategic push to export South Korea's high-end, tech-enabled "K-Housing" ecosystem to affluent international buyers.

- September 2025: Mandarin Oriental partnered with Hanwha Group to develop an exclusive, hospitality-branded luxury property in Seoul's Central Business District. This introduces a new tier of globally branded, service-integrated luxury living to the South Korean market.

- May 2025: Daewoo E&C officially renewed its ultra-premium "SUMMIT" brand and rolled out its "Prugio Edition 2025" design standard. Focused on a "Healing in Everyday Life" theme, the rollout integrated resort-style private spas, advanced inter-floor noise reduction structures, and upgraded smart home tech into its new builds.

- January 2025: Samsung C&T opened Raemian Yongsan Tower, integrating 850 units with Samsung SDS smart-home platforms; 92% sold within 72 hours.

South Korea Luxury Residential Real Estate Market Report Scope

By Property Type

| Apartments and Condominiums |

| Villas and Landed Houses |

By Business Model

| Sales |

| Rentals |

By Mode of Sale

| Primary (New-Build) |

| Secondary (Existing-Home Resale) |

By City

| Seoul |

| Busan |

| Daegu |

| Incheon |

| Rest of South Korea |

| By Property Type | Apartments and Condominiums |

| Villas and Landed Houses | |

| By Business Model | Sales |

| Rentals | |

| By Mode of Sale | Primary (New-Build) |

| Secondary (Existing-Home Resale) | |

| By City | Seoul |

| Busan | |

| Daegu | |

| Incheon | |

| Rest of South Korea |

Key Questions Answered in the Report

How large is the South Korea luxury residential real estate market in 2026?

The South Korea luxury residential real estate market size is estimated at USD 53.89 billion for 2026.

What CAGR is expected through 2031?

Market value is projected to advance at a 7.54% CAGR between 2026 and 2031.

Which property type dominates premium sales?

Apartments and condominiums captured 67.5% share in 2025 thanks to branded high-rise demand.

Where is the fastest regional growth?

Incheon leads with a 9.19% CAGR as Songdo’s smart-city build-out accelerates.

How are taxes affecting foreign buyers?

Permit-zone expansion and higher acquisition levies have lengthened closing times by up to 60 days, yet foreign ownership still rose to 12.3% in 2025.

Who are the leading developers?

Samsung C&T, HDC Hyundai Development, Lotte E&C, GS E&C and POSCO E&C are the leading developers.

Page last updated on: