Hong Kong Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

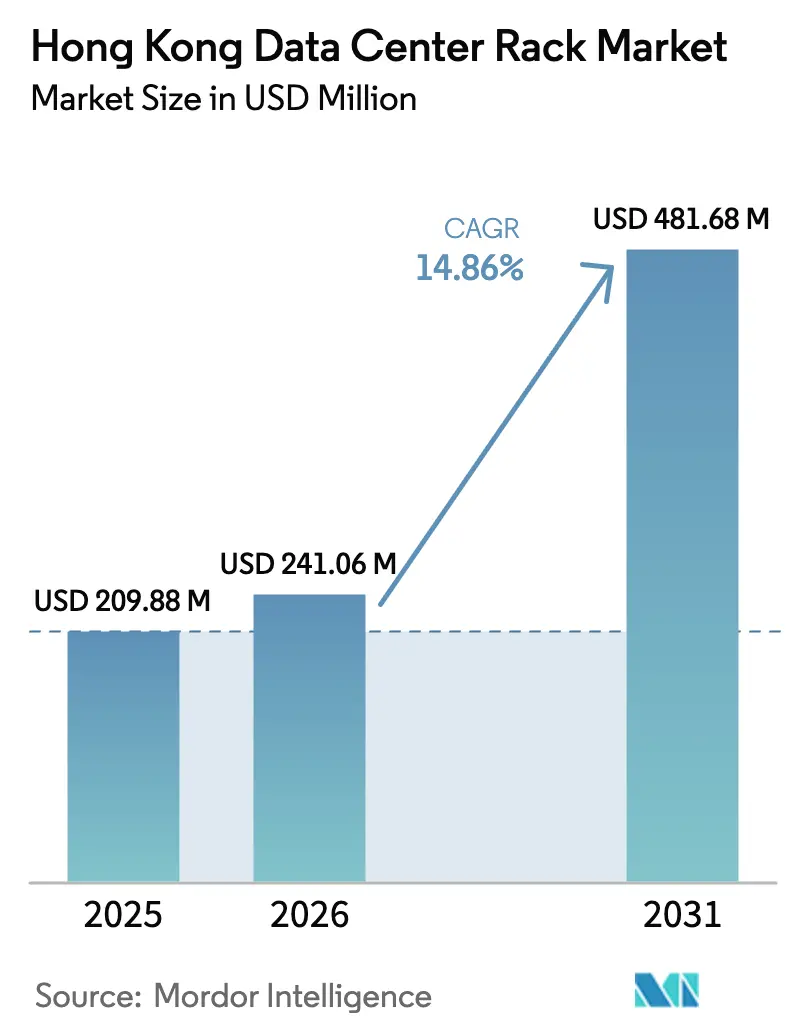

| Base Year Market Size (2025) | USD 209.88 Million |

| Market Size (2026) | USD 241.06 Million |

| Market Size (2031) | USD 481.68 Million |

| Growth Rate (2026 - 2031) | 14.86% CAGR |

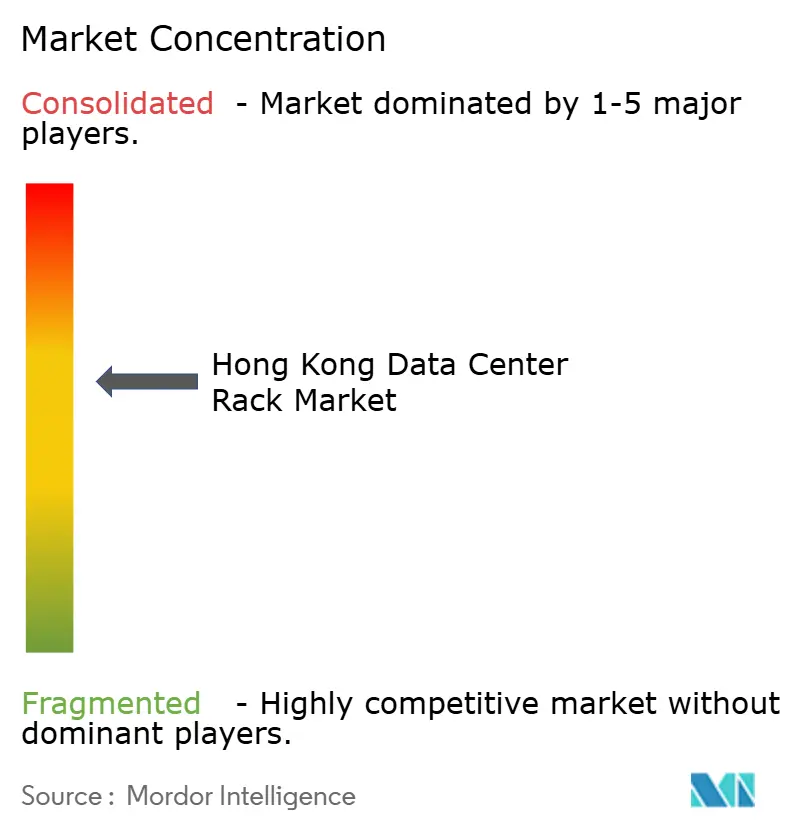

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Data Center Rack Market Analysis by Mordor Intelligence

The Hong Kong data center rack market size was valued at USD 209.88 million in 2025 and estimated to grow from USD 241.06 million in 2026 to reach USD 481.68 million by 2031, at a CAGR of 14.86% during the forecast period (2026-2031). Surging hyperscale investment, accelerated 5G deployment, and policy incentives under Smart City 2.0 are converging to raise rack densities, promote taller form factors, and favor liquid-ready designs that support AI workloads. Demand is further boosted by the territory’s 2.6-minute average annual power-outage record, which reassures operators that high-density deployments can run with limited interruption. A sizeable share of capital is flowing toward cabinet systems that deliver both environmental control and tamper resistance, critical in Hong Kong’s humid subtropical climate and tightly regulated financial sector. Meanwhile, the Hong Kong data center rack market is seeing a steady shift from steel to aluminum as ESG-oriented buyers prioritize recyclability and embodied-carbon reductions.

Key Report Takeaways

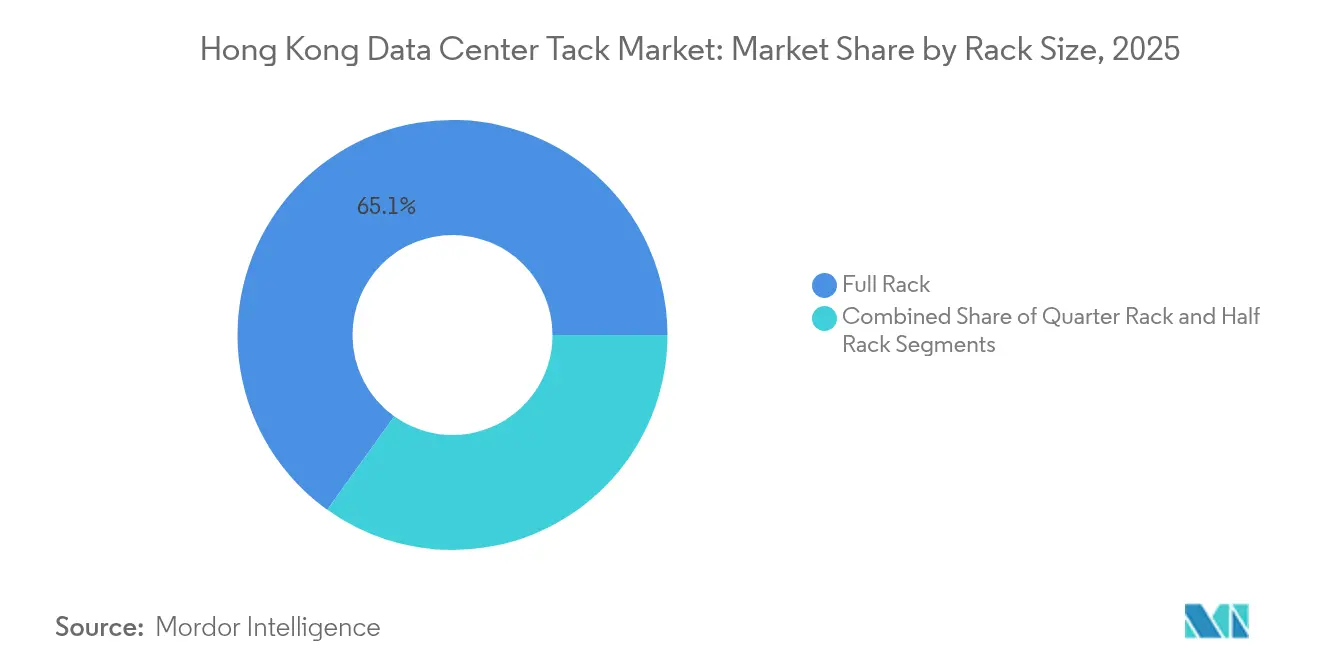

- By rack size, full racks led with 65.10% of the Hong Kong data center rack market share in 2025 while growing at 16.85% CAGR through 2031.

- By rack height, 42U held 50.45% of the Hong Kong data center rack market size in 2025, whereas 48U is poised for the fastest 15.72% CAGR to 2031.

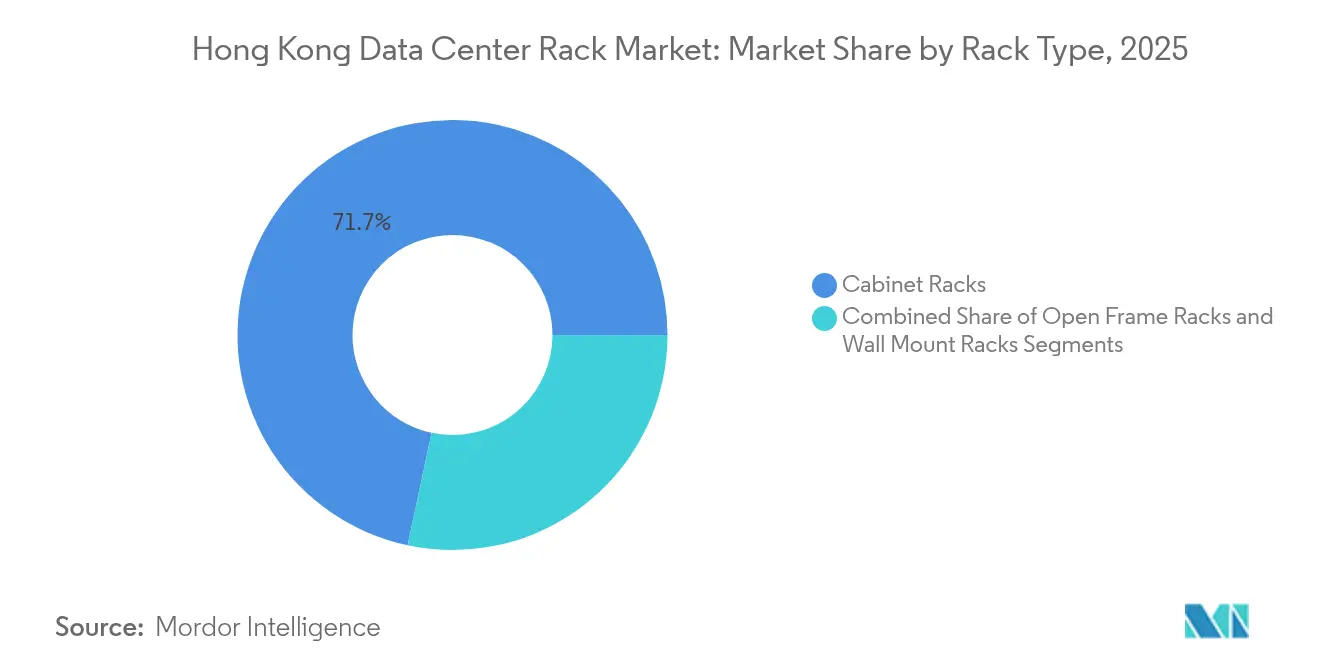

- By rack type, cabinets accounted for 71.65% revenue share and are advancing at 14.98% CAGR on stronger security and airflow management needs.

- By data-center type, colocation facilities commanded 55.10% share in 2025, but hyperscale sites will outpace the overall Hong Kong data center rack market with a 15.18% CAGR to 2031.

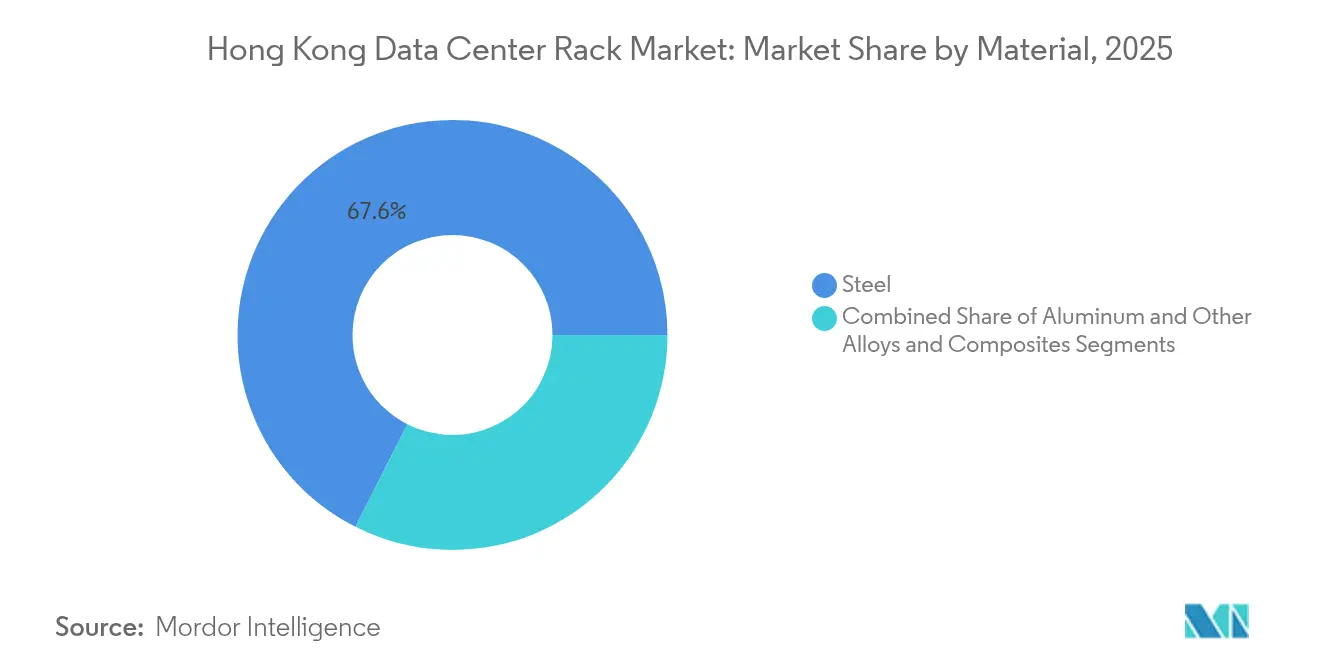

- By material, steel retained 67.55% share in 2025; aluminum will expand the Hong Kong data center rack market size for sustainable racks at a 16.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in Hong kong includes both locally based firms and those operating across multiple regions. The market landscape in the global data center rack industry research shows how these players are arranged internationally.

Hong Kong Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G rollout and explosive IoT traffic | +3.2% | Hong Kong territory-wide, spillover to Greater Bay Area | Medium term (2-4 years) |

| Fiber backhaul densification across the territory | +2.8% | Hong Kong core districts, extending to New Territories | Short term (≤ 2 years) |

| Surge in hyperscale and cloud colocation build-outs | +4.1% | Tseung Kwan O, Sha Tin industrial zones | Medium term (2-4 years) |

| Smart-City 2.0 digital-infrastructure incentives | +2.3% | Hong Kong government-designated areas | Long term (≥ 4 years) |

| Adoption of liquid/immersion-ready high-density racks | +1.9% | Hyperscale facilities, enterprise edge deployments | Medium term (2-4 years) |

| ESG push for recyclable modular aluminium racks | +1.2% | Global multinational enterprises, local government facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Rollout and Explosive IoT Traffic

Territory-wide 5G coverage has surpassed 90%, forcing operators to shift compute resources from centralized halls to distributed edge nodes that demand hybrid racks capable of housing both IT and radio equipment.[1]HKT, “5G Coverage Reaches 90% of the Population,” hkt.com HKBN’s adoption of 25 Gbit/s PON fiber accentuates the need for racks that can deliver high-density power, optimized cable management, and field-swappable optics within a single enclosure. As Smart City 2.0 pilots add thousands of lamppost sensors, micro stations, and AI cameras, rack suppliers must support short-depth devices and outdoor IP-rated cabinets on rooftops and street furniture. High bandwidth, low latency, and small-footprint demands together pull the Hong Kong data center rack market toward multifunctional, compact designs.

Fiber Backhaul Densification Across the Territory

Hong Kong’s nine international cable systems funnel traffic through carrier-neutral sites like MEGA-i, where each suite may terminate 900–1,200 fiber pairs.[2]iAdvantage, “MEGA-i Carrier-Neutral Connectivity Factsheet,” iadvantage.netSuch densities require racks that integrate structured fiber trays, rollable-ribbon managers, and front-access MPO modules that speed Moves-Adds-Changes. The USD 500 million E-MEA cable further cements the territory’s role as Asia’s gateway and drives additional landing-station expansions that lift specialized rack demand. As these cross-connect hubs proliferate in Kowloon and Sha Tin, the Hong Kong data center rack market pursues corrosion-resistant alloys and quick-release panels that simplify optical maintenance within tight spaces.

Surge in Hyperscale and Cloud-Colocation Build-outs

Hyperscale tenants now design for 40 kW-plus per rack loads, accelerating the shift to liquid-capable enclosures and 48U heights that optimize cubic utilization. Global Switch’s adoption of direct liquid cooling highlights the need for structural rigidity that can handle coolant manifolds and high-mass cold plates while still meeting Hong Kong’s seismic code. BDx’s financing round confirms investors’ willingness to back new hall expansions even as land scarcity intensifies. These specifications compel vendors to ship pre-verified rack-power-cooling bundles, driving the Hong Kong data center rack market toward integrated, scalable platforms.

Smart City 2.0 Digital-Infrastructure Incentives

The HKD700 million (USD 89.17 million) state budget for Smart City 2.0 earmarks funds for “smart lamppost” nodes, mobile edge pods, and cyber-secure data hubs, all needing hardened, compact racks . Back-end processing for the iAM Smart digital-ID platform further elevates requirements for trusted-platform modules, tamper logs, and dual-factor rack locks. Suppliers that align with these public-sector standards benefit from predictable procurement cycles and city-wide visibility, deepening the Hong Kong data center rack market penetration over the long term.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating ransomware & cyber-extortion incidents | -2.1% | Global impact with Hong Kong financial sector concentration | Short term (≤ 2 years) |

| Land-and-power scarcity for new data-centre halls | -3.4% | Hong Kong territory-wide, acute in core districts | Medium term (2-4 years) |

| Export-control delays for advanced metal alloys | -1.8% | China-Hong Kong trade corridor, global supply chains | Medium term (2-4 years) |

| Skilled precision-fabrication labour deficit | -1.3% | Hong Kong manufacturing sector, regional spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Ransomware and Cyber-Extortion Incidents

Fifty-nine percent of local enterprises reported a ransomware event in 2024, prompting CFOs to reallocate budgets from expansion to resilience upgrades. The USD 75 million DarkAngels payout underscored the financial stakes facing regulated banks that anchor many Hong Kong colocation room.[3]ISACA, “Ransomware Trends and Record Payouts,” isaca.orgAs boards demand real-time physical-cyber convergence, rack manufacturers must embed intrusion sensors, smart locks, and logging firmware, raising bill-of-materials costs and slowing order volumes for conventional SKUs in the Hong Kong data center rack market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full Racks Drive Standardization

Full racks seized 65.10% of the Hong Kong data center rack market share in 2025 and will grow at 16.85% CAGR as hyperscale entrants impose uniform 42U and 48U blocks that streamline automation and spares logistics. This preference accelerates the adoption of cartridge-ready power shelves and top-of-rack coolant manifolds that can be factory-tested before roll-in. Quarter racks still support Smart City sensor hubs and pop-up 5G micro sites, but their unit economics limit uptake beyond edge niches. Half racks remain a middle-ground choice for SMEs needing colocation presence without over-allocating capital.

Liquid cooling is an additional catalyst for full-rack dominance. Supermicro’s rack-scale immersion kit reaches 100 kW per rack and depends on consistent width, depth, and height to optimize manifold routing. Standardized footprints simplify hot-aisle containment, door-based heat exchangers, and front-serviceable PDUs. Consequently, full racks will continue to influence how builders provision floor tiles, cable trenches, and raised-floor airflow across the Hong Kong data center rack market.

By Rack Height: 48U Gains Ground Despite 42U Dominance

The 42U format controlled 50.45% of the Hong Kong data center rack market size in 2025, reflecting its historical ubiquity among enterprise applications. Yet 48U will expand at 15.72% CAGR as hyperscale firms chase vertical density, reducing white-space leasing costs per kilowatt. Taller frames allow additional bus-bar segments, side-car manifolds, and blanking-panel arrangements that improve airflow modeling.

LiquidStack’s DataTank 48U immersion chassis exemplifies how the extra elevation accommodates coolant expansion tanks and service cranes within a single bay. Operators gain more compute per tile while maintaining ergonomic service reach using lift-assist tools. As AI GPU clusters push rack weights past 1,500 kg, manufacturers reinforce 48U frames with higher-gauge steels or double-folded aluminum rails, which enhances competitiveness in the Hong Kong data center rack market.

By Rack Type: Cabinets Dominate Security-Conscious Market

Cabinet-style enclosures captured 71.65% share in 2025 as Hong Kong’s finance-driven customer base demands side-panel locking, gasketed doors, and real-time access logs. Sealed cabinets also mitigate salt-air corrosion in waterfront facilities and control humidity swings during typhoon seasons. Open-frame racks persist inside hot-aisle containment pods where airflow efficiency outranks physical security, while wall-mount skews fulfill retail-branch or smart-building edge closets with shallow depth and limited load ratings.

Security anxiety following the 2024 ransomware surge pushes procurement toward intelligent cabinets with BLE badges and biometric handles. Vendors that supply these secure enclosures are expanding the Hong Kong data center rack market size through value-added software modules that integrate with SIEM dashboards. This convergence between physical and cyber monitoring has become a buying criterion in nearly every RFP issued by financial tenants during 2025.

By Data Center Type: Colocation Leads While Hyperscale Accelerates

Colocation halls retained 55.10% revenue share in 2025 because international carriers, OTTs, and fintech firms prize Hong Kong’s carrier neutrality and dense cross-connect ecosystem. Yet hyperscale growth will outpace the overall Hong Kong data center rack market at 15.18% CAGR as cloud majors replicate mainland availability zones on local soil to meet data-residency demands. Hybrid enterprises leverage the same halls for cloud on-ramps that sit meters away from private cages, a pattern that sustains cabinet sales even in hyperscale shells.

SUNeVision’s MEA Plus campus in Tseung Kwan O uses prefabricated steel frames that can swing between retail colo layouts and single-tenant mega-pods, enabling rapid mix-and-match leasing. Hyperscale appetite for taller racks and liquid loops forces colo landlords to retrofit chilled-water capacity and floor loading. As a result, rack vendors that can supply delivered-in-place systems ready for 45 kW racks secure larger contracts in the Hong Kong data center rack market.

By Material: Steel Dominates Despite Aluminum’s Sustainability Push

Steel held a 67.55% share in 2025 due to its lower cost and mature fabrication ecosystem in Guangdong factories that ship overnight into Hong Kong. Aluminum, however, will log 16.05% CAGR as ESG scorecards incorporate recycled content and embodied-carbon metrics into tender scoring. Lighter alloys reduce transportation CO₂ and ease manual handling in constrained goods lifts serving upper-floor server rooms.

Tate’s Grid LEC aisle, assembled with renewable-energy aluminum, cuts embodied carbon 55% without sacrificing stiffness. Clients pursuing LEED Platinum or BREAM Outstanding goals assign bonus weight to such innovations, lifting aluminum’s share of the Hong Kong data center rack market. Trade frictions on aerospace-grade alloys and export licensing, however, slow advanced alloy imports, compelling buyers to dual-source between domestic steel and international aluminum over the medium term.

Geography Analysis

Hong Kong’s compact geography concentrates more than 40 facilities within a 30 km radius, enabling cross-facility latency of under 1 ms and fostering a unique ecosystem where hyperscalers colocate with liquidity venues and FX gateways. Tseung Kwan O, the designated data-center corridor, clusters mega-campuses beside the territory’s first dedicated power substation, supporting multi-hundred-megawatt footprints that amplify demand in the Hong Kong data center rack market. Sha Tin hosts second-tier halls targeting mainland enterprise overflow, while Kowloon and Hong Kong Island maintain premium edge rooms serving banking, trading, and copyright-sensitive media.

Integration with the Greater Bay Area magnifies growth prospects. Cross-border fiber spines allow Shenzhen and Guangzhou manufacturers to back up mission-critical workloads in Hong Kong under dual-jurisdiction compliance.. Nevertheless, geopolitical concerns around data inspection temper inbound investments from some Western cloud studios, prompting sovereign-edge deployments in Hong Kong for customer PII while pushing less-sensitive archives to Singapore.

Mordor Intelligence tracks the data center rack market across other major regions such as Africa, Middle East, and South America, with additional country-level coverage spanning Singapore, Thailand, South Africa, Saudi Arabia, Brazil, and Chile, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Moderate fragmentation defines the Hong Kong data center rack market. Global OEMs such as Vertiv, APC, and Rittal compete with regional specialists like Chatsworth Products and local sheet-metal fabricators that customize for typhoon-proof logistics constraints. Market leaders differentiate through holistic bundles that merge rack, busway, containment, and cooling distribution under a single warranty, reducing integration risk for hyperscalers. Start-ups meanwhile court edge deployments with IP-65-rated micro cabinets that can bolt to smart lampposts or shopping-mall rooftops.

Strategic partnerships have become the route to securing specification lock-in. Vertiv’s joint reference designs with NVIDIA incorporate rear-door heat exchangers certified for HGX H100 clusters, creating pull-through demand for its D-Series cabinets among AI tenants. Rittal collaborates with Stulz for ChillerTFM pods that couple rack shells with precision free-cooling coils, accelerating time-to-production in land-scarce plots where building heights are restricted. These alliances illustrate how rack vendors evolve into solution orchestrators rather than commodity sheet-metal suppliers, a trend shaping purchasing in the Hong Kong data center rack market.

Hong Kong Data Center Rack Industry Leaders

Eaton Corporation

Vertiv Group Corp.

Schneider Electric SE

Rittal GmbH & Co. KG

Delta Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BDx secured financing for further expansion in Hong Kong, signalling sustained hyperscale appetite despite land shortages.

- April 2025: China Mobile explored a USD 835 million acquisition of HKBN to strengthen cross-border connectivity.

- April 2025: Vertiv reported USD 2,036 million Q1 2025 sales, up 24% year-over-year, underscoring demand for AI-optimized racks.

- February 2025: CapitaLand Investment committed more than USD 700 million to its first Japanese data center, echoing regional expansion that may redirect traffic through Hong Kong.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Hong Kong data-center rack market as all new, factory-built cabinet, open-frame, and wall-mount racks (19-inch standard or custom heights) installed inside colocation, hyperscale, cloud, enterprise, and edge facilities across the territory. Units shipped are converted to value using average selling prices that reflect material mix and height distribution.

Refurbished or second-hand racks, outdoor telecom cabinets, and purely network distribution frames fall outside our count.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Interviews with facility engineers, procurement heads, regional integrators, and alloy suppliers across Central, Tseung Kwan O, and Kwai Chung helped validate utilization rates, price band shifts, and adoption appetite for aluminum racks. Guided surveys with hyperscale cloud operators clarified expansion phasing and allowed us to stress-test forecast drivers unearthed during desk work.

Desk Research

Our analysts first mapped supply and demand signals through freely available tier-1 sources such as Hong Kong's Census and Statistics Department server import codes, the Office of the Communications Authority's 5G base-station roll-outs, Building Department permits for data halls, OpenInfra power-capacity trackers, and scholarly work on high-density cooling thresholds. Company 10-Ks, carrier presentations, listed colocation prospectuses, and news harvested from Dow Jones Factiva enriched the baseline. Paid assets like D&B Hoovers provided revenue splits that helped anchor vendor shipments. This list is indicative; many additional web archives, trade portals, and patent libraries informed cross-checks.

Market-Sizing and Forecasting

A top-down reconstruction began with installed IT load (MW) and white-floor expansion plans; those megawatts were converted to rack counts via density norms (kW per rack) and then multiplied by ASP curves tied to global steel and aluminum indices. Select bottom-up checks, supplier shipment audits and sampled colocation rack tallies, tempered over-projection risk. Key variables include hyperscale capacity additions, average rack density, steel price trend, 5G traffic growth, and rack-height mix shift toward 48U. Multivariate regression, supplemented by scenario analysis for land-power constraints, projects values from the 2024 base through 2030. Gaps in shipment data were bridged using weighted moving averages from customs codes plus expert judgment.

Data Validation and Update Cycle

Outputs pass a three-layer analyst review where variance versus historical series, external benchmarks, and peer models triggers re-work. Our tables refresh every twelve months, with interim adjustments when large colocation projects or policy shifts materially alter demand. A final pre-publication sweep ensures clients receive the latest vetted view.

Why Mordor's Hong Kong Data Center Rack Baseline stands out for reliability

Published estimates often differ; definitions, inclusion of retrofit demand, ASP assumptions, and refresh cadence rarely align.

Key gap drivers here include whether hyperscale self-builds are counted, how aluminum cabinet premiums are treated, currency year bases, and the frequency with which models are revisited after major land-policy announcements.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 209.88 million (2025) | Mordor Intelligence | - |

| USD 200 million (2024) | Regional Consultancy A | Limits scope to enterprise halls; overlooks hyperscale ramp-up and ASP escalation tied to liquid-cooling ready cabinets |

| USD 150 million (2023) | Trade Journal B | Relies solely on shipment surveys, excludes retrofit demand and aluminum racks |

These contrasts show that Mordor's disciplined variable selection, annual refresh, and dual validation provide a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current size of the Hong Kong data center rack market?

The Hong Kong data center rack market stands at USD 241.06 million in 2026 and is projected to reach USD 481.68 million by 2031.

Which rack size segment leads the Hong Kong data center rack market?

Full racks lead with 65.10% share in 2025 due to hyperscale standardization and are growing at 16.85% CAGR.

How does land scarcity affect rack deployment in Hong Kong?

Limited greenfield plots delay new halls, pushing operators to deploy higher-density racks within existing sites and slightly dampening near-term growth.

Why are aluminum racks gaining traction?

Aluminum offers recyclability and lower embodied carbon, aligning with ESG mandates and expanding at a 16.05% CAGR through 2031 despite steel’s current dominance.

Page last updated on: