Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

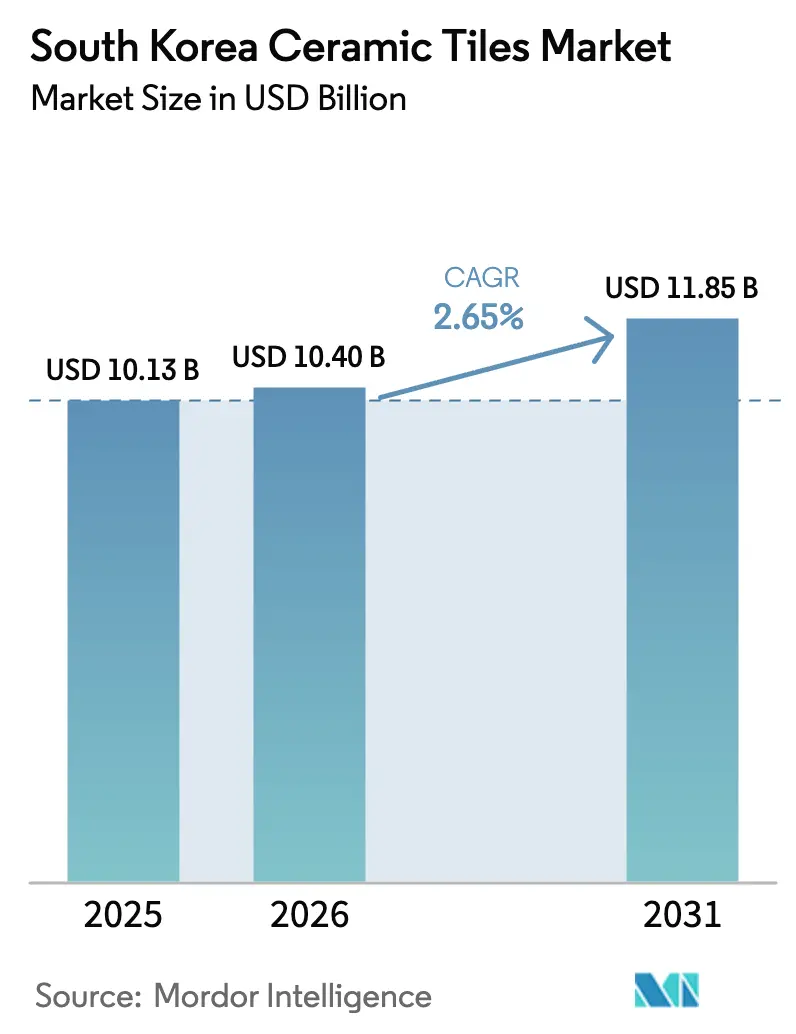

| Base Year Market Size (2025) | USD 10.13 Billion |

| Market Size (2026) | USD 10.40 Billion |

| Market Size (2031) | USD 11.85 Billion |

| Growth Rate (2026 - 2031) | 2.65% CAGR |

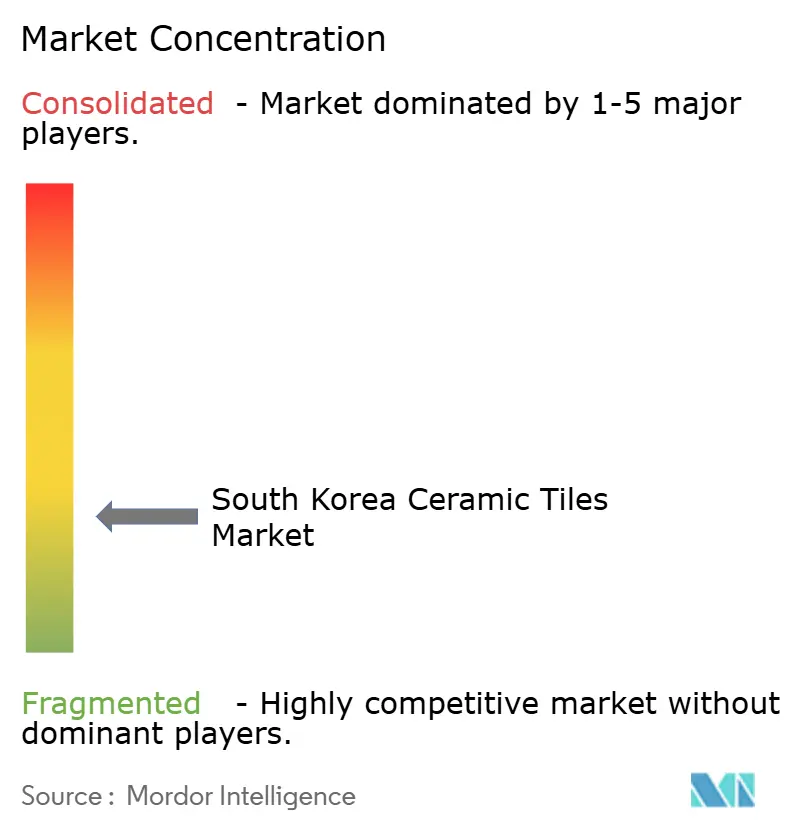

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Ceramic Tiles Market Analysis by Mordor Intelligence

The South Korea Ceramic Tiles Market size is expected to grow from USD 10.13 billion in 2025 to USD 10.40 billion in 2026 and is forecast to reach USD 11.85 billion by 2031 at 2.65% CAGR over 2026-2031.

The growth trajectory is steady because renovation and redevelopment demand balances a softer new-build cycle. Awarded urban-renewal contracts worth USD 19.5 billion (KRW 27 trillion) in the first half of 2025 point to strong procurement cycles for floor, wall, and façade tile systems in multi-phase complexes[1]Ministry of Land, Infrastructure and Transport Coverage, “ZEB Mandate and Building-Energy Performance,” Chosun Biz, biz.chosun.com. New-apartment supply planned for 2025 stands at 146,130 units, the lowest since 2000, which channels household spending into upgrades of existing homes where porcelain formats often see premium specification[2]LX Hausys, “Product Standards and Certifications,” LX Hausys, lxhausys.com. Policy-driven building-efficiency requirements are lifting specification intensity in roofing through cool-roof ceramic tiles that improved modelled cooling loads for Seoul buildings in controlled studies, reinforcing an emerging application niche. Trade frictions and tighter anti-dumping enforcement in nearby markets have reduced the most aggressive price undercutting from Chinese exporters, easing price pressure on domestic plants in the market. Modular bathroom pods are compressing site labour, while elevated LNG feedstock and tighter emissions thresholds raise the premium on energy-efficient kilns and stable supply plans in the South Korea ceramic tiles market.

Key Report Takeaways

- By product type, porcelain led with a 46.23% revenue share of the South Korea ceramic tiles market in 2025, while Decorative / Patterned Tiles are projected to expand at a 2.98% CAGR through 2031.

- By application, floor accounted for a 58.15% share of the South Korea ceramic tiles market in 2025, while roofing is projected to expand at a 2.86% CAGR through 2031.

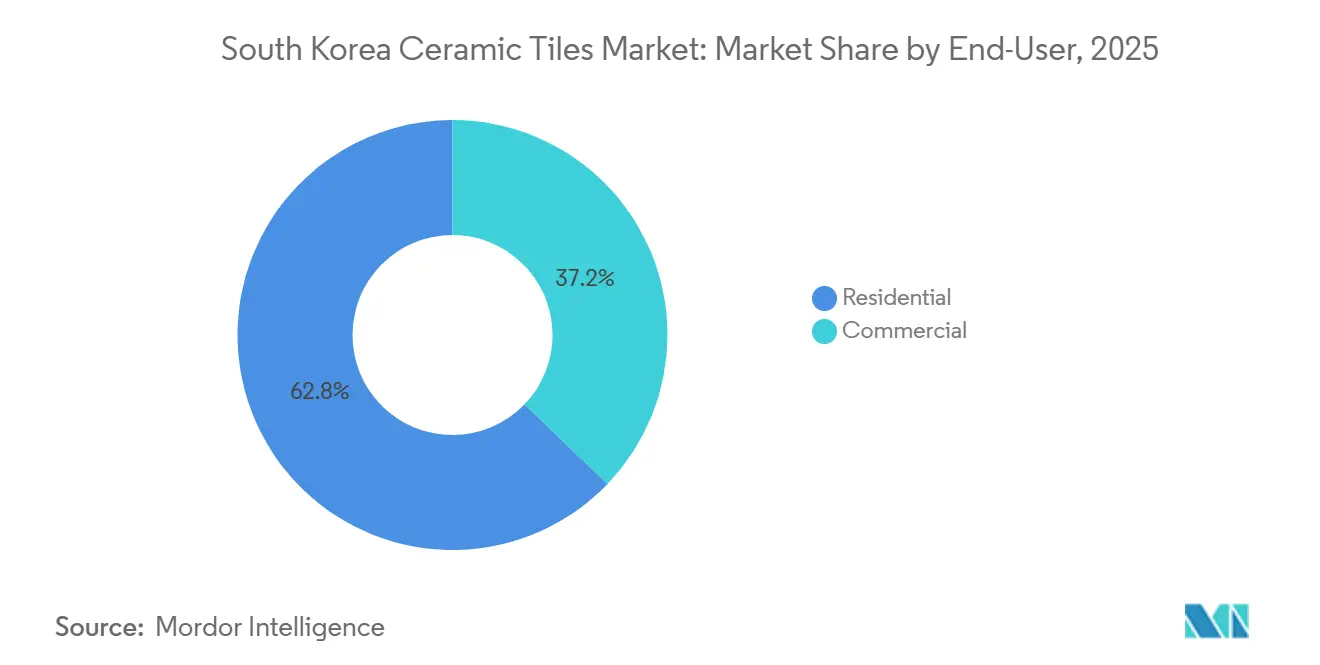

- By end-user, residential represented 62.81% of the South Korea ceramic tiles market share in 2025 and holds the highest projected growth at a 3.19% CAGR through 2031.

- By construction type, renovation held 61.42% of the South Korea ceramic tiles market in 2025, and new construction records the fastest 2.92% CAGR to 2031.

- By distribution channel, specialty stores captured 41.73% of the South Korea ceramic tiles market in 2025, while online retail posts the fastest 3.64% CAGR through 2031.

- By geography, the Seoul Capital Region accounted for 39.21% of the South Korea ceramic tiles market in 2025, and Busan-Ulsan-Gyeongsang is the fastest at 3.15% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing-redevelopment pipeline boosts tile demand | + 0.8% | National, with early gains in Seoul, Gyeonggi, and Busan metro areas | Medium term (2-4 years) |

| Large-format porcelain adoption in renovation | + 0.6% | Seoul Capital Region, Busan-Ulsan-Gyeongsang | Short term (≤ 2 years) |

| Commercial construction revival | + 0.5% | Seoul, Incheon GTX-B corridor, Busan Gadeok Airport zone | Long term (≥ 4 years) |

| Anti-dumping duties stabilize prices | + 0.3% | Global, spill-over to domestic pricing in South Korea | Medium term (2-4 years) |

| ZEB rules lift cool-roof tiles | + 0.3% | National, priority enforcement in Seoul, Sejong, Daejeon | Long term (≥ 4 years) |

| Modular pods adopt thin-tile systems | + 0.2% | National, concentrated in Gyeonggi prefab hubs, expanding to Jeonnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Housing-Redevelopment Pipeline Boosts Tile Demand

Fast-track approvals for demolition and reconstruction of apartment complexes older than 30 years open a large pipeline that spans 950,000 households through 2027, with direct implications for tile consumption across kitchens, baths, and shared corridors in the market. The policy shift addresses permit bottlenecks from the previous credit squeeze, when issuance in 2023 fell short of planned levels and delayed procurement for finishing materials like porcelain. Contract wins for urban renewal exceeded USD 19.5 billion (KRW 27 trillion) in the first half of 2025, signalling a sustained sequence of bidding rounds and material awards for high-spec installations. Landmark redevelopments now underway include large sites such as Hannam District 4 and Guri Sutaek-dong, each with multi-hundred-thousand-square-meter finish scopes where tile selection sets durability and maintenance baselines. The current emissions-allocation design under the Korea Emissions Trading Scheme offsets part of the carbon cost burden for energy-intensive materials producers, which helps keep redevelopment economics viable for kiln-fired products. This combination of permit acceleration, backlogged projects, and partial emissions-cost relief underpins stable multi-year orders for the South Korea ceramic tiles market.

Preference for Large-Format Porcelain Tiles in Home-Renovation Boom

Renovation now anchors a majority of installations as households prioritize upgrades to existing properties while new-build supply sits at a multi-decade low, which steers budgets toward high-visual-impact surfaces that elevate valuations. Large-format porcelain with fewer grout lines provides a clean look, faster placement, and lower maintenance, attributes that align with premium apartment remodelling in the capital region. The market benefits from digital printing advances that deliver natural-stone and wood visuals with consistent quality suited for repeat-fit-out programs. Factory-finished rectified edges and calibrated thickness improve installation productivity in occupied units, which reduces disruption and labour time for contractors. Renovation’s installed-base advantage sustains demand for floor, wall, and bath tile sets even as developers schedule staggered completions for major rebuilds.

Revival of Commercial Construction (Offices, Transit Hubs)

Public works spending in 2025 provides a base layer of tiling demand in transit hubs, municipal buildings, and institutional projects, which anchors commercial volumes during residential volatility in the South Korea ceramic tiles market. Long-horizon mega projects such as the GTX-B express rail and the Gadeok Airport program carry large concourse and terminal finish scopes where slip resistance and antimicrobial performance favour high-grade glazed and porcelain formats. Korean-specific standards for flexural strength and flame spread shape sourcing choices in these projects and often lead to domestic supply because compliance and documentation are streamlined with local certifications[3]M. H. Lee, “South Korea’s New Apartment Supply Set to Hit 24-Year Low in 2025, Industry Data Shows,” Korea Bizwire, koreabizwire.com.. The 2026 enforcement of advanced energy-performance thresholds increases the value of reflective roofing and high-thermal-mass interior materials that contribute to building-level efficiency targets. As retrofit cycles continue in offices and public venues, the South Korea ceramic tiles market gains from a steady cadence of capital projects with defined finish packages.

Anti-Dumping Duties on Low-Priced Chinese Imports Stabilize Prices

Regional trade actions have reduced the sharpest price undercutting from Chinese tiles, which narrows the imported price gap and helps local producers defend list prices. Broader tariff pressure on Chinese ceramics in large end markets also tightens price dispersion and reduces arbitrage risk in South Korea. Liquefied-natural-gas prices are expected to hold in a moderate range through 2026, which helps stabilize kiln-fuel inputs while producers focus on steady throughput and mix optimization. Australia’s seasonal biosecurity rule that mandates heat treatment for certain ceramic consignments adds friction to re-export routes, which further reduces indirect import-price pressure at home. This environment creates a more predictable price floor for domestic porcelain and glazed lines in the South Korea ceramic tiles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural-gas price volatility inflates kiln costs | - 0.7% | National, acute in Gyeonggi and South Chungcheong kiln clusters | Short term (≤ 2 years) |

| Competition from engineered stone and luxury vinyl tiles | - 0.5% | Seoul Capital Region, Busan metro, upscale segments | Medium term (2-4 years) |

| An aging installer workforce raises placement costs | - 0.4% | National, more severe outside the capital with outmigration | Long term (≥ 4 years) |

| Tighter PM-emission limits raise capex for SME kilns | - 0.3% | National, disproportionate impact outside the Seoul-Gyeonggi corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Engineered Stone and Luxury-Vinyl Tiles

Engineered stone and resilient vinyl alternatives continue to gain placement in kitchens, baths, and corridors because they address speed, weight, and maintenance concerns for select projects. The product portfolios of large local suppliers reflect this shift, with new engineered-stone and vinyl introductions showcased in 2025 to broaden options for designers and builders. Elevated energy inputs for ceramics tilt some specifications toward less energy-intensive materials, especially in cost-sensitive renovations where lifecycle criteria are secondary. Workforce constraints further support click-lock vinyl formats for tight schedules and limited skilled labour availability. Sustainability remains a counterweight because porcelain’s inert composition and long service life align with procurement policies in public and healthcare projects, but price and speed pressures still shape outcomes in mixed-use developments. The result is healthy competition that requires ceramic producers to position themselves on performance, ESG, and design rather than cost alone in the South Korea ceramic tiles market.

Aging Installer Workforce Drives Up Placement Costs

The average age of construction engineers in early 2025 reached 52.2 years, and skilled tilers are in shorter supply as older crews retire faster than new entrants train up. Adjustments in foreign-worker quotas for 2026 reduce the pool available for site work, which can raise labour costs and lead times for projects dependent on traditional wet-set tile installation. Installers with experience are gravitating toward factory assembly roles in modular programs that use thin tiles with mechanical locking systems, a shift that shrinks availability for conventional on-site work. Construction firms report that talent gaps are more acute outside the capital, compounding timelines for redevelopment in secondary cities. Persistent shortages push design teams to specify larger formats and pre-mounted mosaics to reduce unit counts per square meter, although such choices can add to material premiums. The cumulative effect is higher installed cost pressure, which projects must manage through scheduling and channel planning in the South Korea ceramic tiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Commands, Decorative Innovates

Porcelain tiles held 46.23% of 2025 revenue in the South Korea ceramic tiles market, supported by low water absorption and durability credentials that suit high-traffic zones and exterior use. The segment sustains a premium position in large urban remodels where pattern consistency and stain resistance inform long-term maintenance plans. Glazed ceramic products serve high-volume kitchen and bath applications in residential towers and small retail, while unglazed formats find use in projects that prioritize abrasion performance. Mosaic formats align with pools, spas, and accent zones because mesh-mounted assemblies reduce site complexity and speed installation in tight spaces. Thin-format and special-shape tiles in the “others” category build on emerging façade-retrofit and feature-wall demand, especially where weight and anchoring considerations are material to design approval. Decorative and patterned tiles are projected to grow fastest at 2.98% CAGR to 2031, supported by maturing digital print capabilities and stable price points in mainstream channels. The segment composition benefits from predictable procurement in urban renewal, where premium wet-area surfaces in bathrooms and kitchens often default to porcelain systems that deliver stain resistance and longevity.

Across product types, digital printing delivers wood, marble, and terrazzo visuals with batch stability, which expands design choice without sacrificing mechanical properties. Tile makers adjust press tonnage and firing curves to balance strength, flatness, and visual definition, which is essential for rectified edges and narrow grout joints. Local standards for flexural strength and flame spread guide specification and factor into procurement preferences for public tenders in the South Korea ceramic tiles market. Energy and emissions rules encourage upgrades in kiln insulation and heat recovery regardless of format, so producers optimize the mix to keep throughput high and fuel per square meter low. As modular pods scale and dry-stack methods mature, demand for thin porcelain panels is positioned to rise across several product categories in the South Korea ceramic tiles market.

By Application: Floor Dominates, Roofing Surges on ZEB Tailwind

Floor applications accounted for a 58.15% share of the South Korea ceramic tiles market size in 2025 and remain the anchor for both residential remodelling and commercial retrofits. Surface finish, slip resistance, and cleaning cycles drive specification in transit, healthcare, and education settings where lifecycle performance outweighs upfront savings. Walls remain a large companion category for bathrooms, kitchens, and lobbies, with large formats used to reduce grout lines and improve maintenance routines. Attention to acoustic and impact criteria grows in multi-family and office environments, which makes heavier porcelain and underlayment details attractive in project specs. As building codes emphasize energy and indoor-environment quality, better-performing tile assemblies are selected to support compliance in the South Korea ceramic tiles market.

Roofing is the fastest-growing application at a 2.86% CAGR to 2031 as building-efficiency mandates shift attention to envelope reflectivity and thermal performance. High-albedo ceramic tiles have demonstrated lower cooling loads in modelled cases, a finding that enables owners to capture operating savings while meeting design targets. Retrofit constraints on aging structures reward lighter panels that reduce dead load while maintaining durability that asphalt shingles cannot match. The South Korea ceramic tiles market benefits from roofing specifications that become more standardized as rules tighten and as local certification programs recognize verifiable performance data.

By End-User: Residential Leads Growth, Commercial Chases Infrastructure Pulse

Residential end-users represented 62.81% of total volume in 2025 and hold the highest growth outlook at 3.19%, driven by approvals for demolition and reconstruction of older apartment stock. Renovation of bathrooms and kitchens in mid- to high-rise apartments concentrates spend on porcelain floors and walls where homeowners want premium visuals and longer service life. Floor replacements that fix acoustic and levelling issues in older buildings are also common, supporting steady floor-tile throughput. As lenders and policy settings shift, owners continue to direct budgets toward visible upgrades that support valuations and comfort. The South Korea ceramic tiles market reflects this pivot, translating household balance-sheet stability into material orders for repeatable residential fit-outs.

Commercial demand tracks public infrastructure and service-sector upgrades, which provide a durable baseline for tiles used in concourses, lobbies, restrooms, and food-service areas. Antimicrobial glazes and slip-resistant surfaces are frequently specified in heavy footfall spaces, and local standards support consistent quality across procurement cycles. Office retrofits and institutional refreshes often combine floor and wall packages that favour larger formats to reduce grout maintenance and deliver a seamless look. Transit projects funded under the public works umbrella maintain a rolling schedule of tiling work that helps smooth cycles for commercial installers. As these schemes progress, the South Korea ceramic tiles market keeps a balanced footprint across private and public end-use programs.

By Construction Type: Renovation Reigns, New-Build Waits for Policy Clarity

Renovation and replacement projects accounted for 61.42% of 2025 installations, reflecting near-term strength in upgrades amid softer new starts in the South Korea ceramic tiles market. Urban renewal wins by large contractors, stacking up to a multi-year wave of bathroom, kitchen, and corridor tile orders. Streamlined approvals for older complexes shorten timelines and reduce uncertainty in scheduling for finishing trades. Renovation remains the volume anchor because it addresses more units quickly, with standardized fit-out kits across buildings in programmatic rollouts.

New construction carries a smaller base but a faster projected 2.92% CAGR through 2031, as supply constraints and policy responses set up a gradual recovery in starts. Recent lows in planned apartment supply have induced more focus on redevelopment but also highlight the need for new product, which will eventually lift base volumes for floors and walls. Project economics face pressure from labour, energy, and compliance costs, so tile specifications may skew toward formats and finishes that reduce total installed cost over time. Modular integration can add to predictability for new-build schedules when deployed in high-rise settings.

By Distribution Channel: Specialty Stores Defend, Online Scales with AR Tools

Specialty stores accounted for 41.73% of the 2025 channel mix and continue to play a key role for homeowners and contractors who value tactile sampling and expert consultancy. These stores provide essential services such as guidance on layout design, trim coordination, and installer selection, which helps maintain their relevance in densely populated urban areas. Their ability to offer personalized advice and hands-on support makes them a preferred choice for many customers. DIY outlets and home-improvement chains also hold a significant share of the market. These formats attract weekend renovation budgets by offering a wide range of products, including adhesives, grouts, trims, and tools.

Online sales represent the fastest-growing channel, with a compound annual growth rate of 3.64%. This growth is supported by the availability of visualizer tools and improved logistics, which reduce the need for multiple showroom visits. The convenience of online platforms is driving more consumers to explore and purchase products digitally. In the market, direct sales to contractors remain a critical channel. These sales are particularly important for large redevelopment projects, where factory gate pricing and volume agreements align orders with project timelines.

Geography Analysis

The Seoul Capital Region accounted for 39.21% of demand in 2025, reflecting a concentration of remodelling and redevelopment spend and a deep base of multi-family housing. Forecast growth in the region trails the national average because of saturation and tighter loan-to-value policies in regulated zones that cool speculative turnover while favouring planned redevelopment. Major redevelopment programs, such as Hannam District 4 and other multi-phase sites, sustain tile orders across floors, walls, and amenities in the South Korea ceramic tiles market. Infrastructure work in and around the capital, including the GTX-B program, keeps commercial and transport concourses on a steady improvement path where ceramic performance requirements are stringent. As energy rules tighten, cool-roof adoption and high-thermal-mass interiors complement upgrades in HVAC to meet compliance, pulling ceramic specifications into roofing and interior envelopes more often.

The Busan-Ulsan-Gyeongsang corridor holds a large share of provincial demand and leads growth at a 3.15% CAGR to 2031, anchored by the Gadeok Airport program and port expansions that commit large finish packages. Industrial and logistics upgrades in the region reinforce commercial tile placements where abrasion resistance and slip ratings are decisive. Residential projects in coastal cities add to volumes as developers target buyers who prefer new mid-market stock outside the capital, which supports flows of floor and wall sets. Expanded public spaces and tourism assets foster organized refresh cycles for corridors and restrooms that favour antimicrobial glazes. As environmental performance becomes a stronger procurement factor, the region’s specifications lean toward high-reflectance roofing and compliant interior surfaces in the South Korea ceramic tiles market.

Jeolla and Jeju together contribute a significant share of provincial demand with steady growth as tourism infrastructure and public facilities continue to modernize. Hotel and airport improvements, along with upgrades in public buildings, generate predictable tile packages that prioritize easy-clean surfaces and lifecycle value. The “Rest of South Korea” bucket, including Gangwon and the Chungcheong provinces, maintains a stable base with tiling activity tied to municipal refreshes and selected housing programs. Some secondary cities saw planned-unit delivery shortfalls in 2024, which delayed floor and wall programs and shifted timing into later phases. Export-focused producers face seasonal heat-treatment requirements for shipments to Australia, which introduces friction to outward logistics but does not materially affect local distribution in the South Korea ceramic tiles market.

Competitive Landscape

The South Korea ceramic tiles market exhibits moderate concentration because large groups deploy scale in sourcing, production, and distribution, while dozens of smaller kilns compete in regional niches. Design leadership, digital printing, and ESG credentials differentiate portfolios in premium segments where owners and architects expect long-wear surfaces and consistent visual quality. Companies with strong sustainability disclosure and certifications influence procurement outcomes in public programs where environmental scoring carries weight. Local standards and certification regimes favour suppliers with proven compliance records and deepen ties to public tenders, while international suppliers face higher entry costs for documentation and testing. Energy and emissions trends push producers toward kiln upgrades and heat-recovery investments that absorb fuel-price volatility and carbon constraints, which reinforces the advantage of scale.

Modular construction is a rising channel that changes procurement timing and routes more volume through factory programs that pre-assemble bathrooms and service cores. This shift rewards producers capable of delivering thin porcelain panels and lock-in trims that match off-site takt times and quality gates. Public and institutional projects that adopt modular methods will increase direct factory-to-project flows and reduce reliance on traditional distributors in select segments of the South Korea ceramic tiles market. Compliance costs around particulate capture and monitoring are accelerating exits among smaller kilns, and acquisitions of distressed assets can expand capacity for well-capitalized players. Seasonal biosecurity measures in key destination markets create timing challenges for exports but also limit arbitrage back into South Korea, stabilizing domestic pricing for broader portfolios.

Product roadmaps now emphasize cool-roof formulations, antimicrobial glazes, and high-definition natural looks to meet project needs across residential towers and public infrastructure. Suppliers expand design libraries quickly to capture trending aesthetics while relying on standards-based performance to secure repeat specifications. Partnerships with builders and modular integrators tighten forecasting and lower logistics risk, which is essential when kiln scheduling is sensitive to energy costs. The mix of scale economics, design capability, and compliance execution defines competitive outcomes through the forecast in the South Korea ceramic tiles market.

South Korea Ceramic Tiles Industry Leaders

KCC Corporation

IS Dongseo Co. Ltd.

Kukdong Ceramics Co. Ltd.

Woongjin Ceramics

Korea Fine Ceramics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: South Korea’s Financial Services Commission launched a KRW 10 trillion support program for small businesses with targeted tranches for startup loans, value-growth initiatives, and restructuring, providing indirect relief for SMEs facing energy-cost and compliance hurdles in building materials.

- April 2025: The Korea Land and Housing Corporation and NRB Inc. showcased South Korea’s first high-rise precast-concrete modular apartment complex at NRB’s Gunsan factory, integrating POSCO’s fully prefabricated bathroom units with thin porcelain tiles and click-lock systems that compress finishing to about 90 minutes per module. The project demonstrated multi-grade acoustic performance and aligned with the LH OSC Housing Roadmap.

- March 2025: LX Hausys was named an Industry Mover in the S&P Global 2024 Corporate Sustainability Assessment, achieving one of the largest year-over-year ESG score increases among building products firms and earning inclusion in the 2025 Sustainability Yearbook.

- February 2025: LX Hausys exhibited advanced surface materials, including floor tiles and resilient flooring, at the Kitchen & Bath Industry Show in Las Vegas, announcing new designs for Western markets and distribution partnerships aligned with expanded capacity.

South Korea Ceramic Tiles Market Report Scope

Ceramic tiles are widely used in construction and renovation projects due to their durability, water resistance, aesthetic versatility, and ease of maintenance. The South Korea ceramic tiles market is segmented by product type, application, end-user, construction type, distribution channel, and geography. By product type, the market is segmented into porcelain tiles, glazed ceramic tiles, unglazed ceramic tiles, mosaic tiles, and others. By application, the market is segmented into floor, wall, and roofing. By end-user, the market is segmented into residential and commercial. By construction type, the market is segmented into new construction and renovation and replacement. By distribution channel, the market is segmented into specialty tile and stone stores, home improvement and DIY stores, online retail, and direct sales to contractors. By geography, the market is segmented into the Seoul Capital Region, Busan-Ulsan-Gyeongsang Region, Jeolla and Jeju, and the rest of South Korea. The report provides market size and forecast estimates for all the above-mentioned segments in value terms (USD).

Segmentation by Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Hand-made) |

Segmentation by Application

| Floor |

| Wall |

| Roofing |

Segmentation by End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airport/Metro/Bus) | |

| Others |

Segmentation by Construction Type

| New Construction |

| Renovation & Replacement |

Segmentation by Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

Segmentation by Geography

| Seoul Capital Region (Seoul + Gyeonggi) |

| Busan-Ulsan-Gyeongsang Region |

| Jeolla & Jeju |

| Rest of South Korea |

| Segmentation by Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Hand-made) | ||

| Segmentation by Application | Floor | |

| Wall | ||

| Roofing | ||

| Segmentation by End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airport/Metro/Bus) | ||

| Others | ||

| Segmentation by Construction Type | New Construction | |

| Renovation & Replacement | ||

| Segmentation by Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| Segmentation by Geography | Seoul Capital Region (Seoul + Gyeonggi) | |

| Busan-Ulsan-Gyeongsang Region | ||

| Jeolla & Jeju | ||

| Rest of South Korea | ||

Key Questions Answered in the Report

What is the size and growth outlook for the South Korea ceramic tiles market by 2031?

The South Korea ceramic tiles market size is USD 10.40 billion in 2026 and is projected to reach USD 11.85 billion by 2031 at a 2.65% CAGR.

Which applications lead demand in South Korea’s ceramic tiles space?

Floor installations lead with a 58.15% share in 2025, and roofing has the fastest projected growth at 2.86% due to energy-performance mandates.

Which end-user group is expanding fastest in South Korea's ceramic tiles?

Residential holds the largest share at 62.81% and the highest projected growth at 3.19%, supported by accelerated redevelopment approvals.

What policies are shaping tile specifications in commercial projects?

Zero-Energy-Building requirements and related performance standards favour high-albedo roofing and high-thermal-mass finishes, lifting specifications for cool-roof ceramic tiles.

How is modular construction changing tile procurement in South Korea?

Factory-built bathroom pods using thin porcelain and click-lock systems shift orders to off-site schedules and reduce site labour, expanding new channels for tile suppliers.

How do energy prices affect tile producers in South Korea?

Reliance on imported LNG keeps kiln costs sensitive to global prices, making hedging and kiln-efficiency upgrades critical for margins.

Page last updated on: