Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

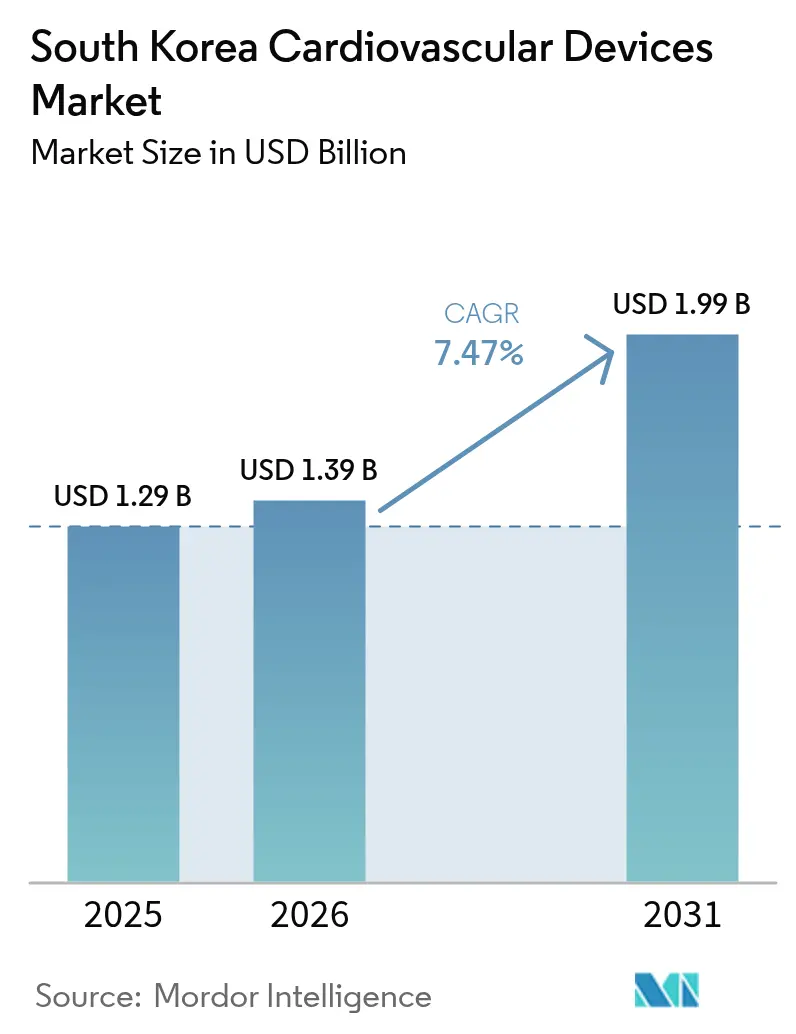

| Base Year Market Size (2025) | USD 1.29 Billion |

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

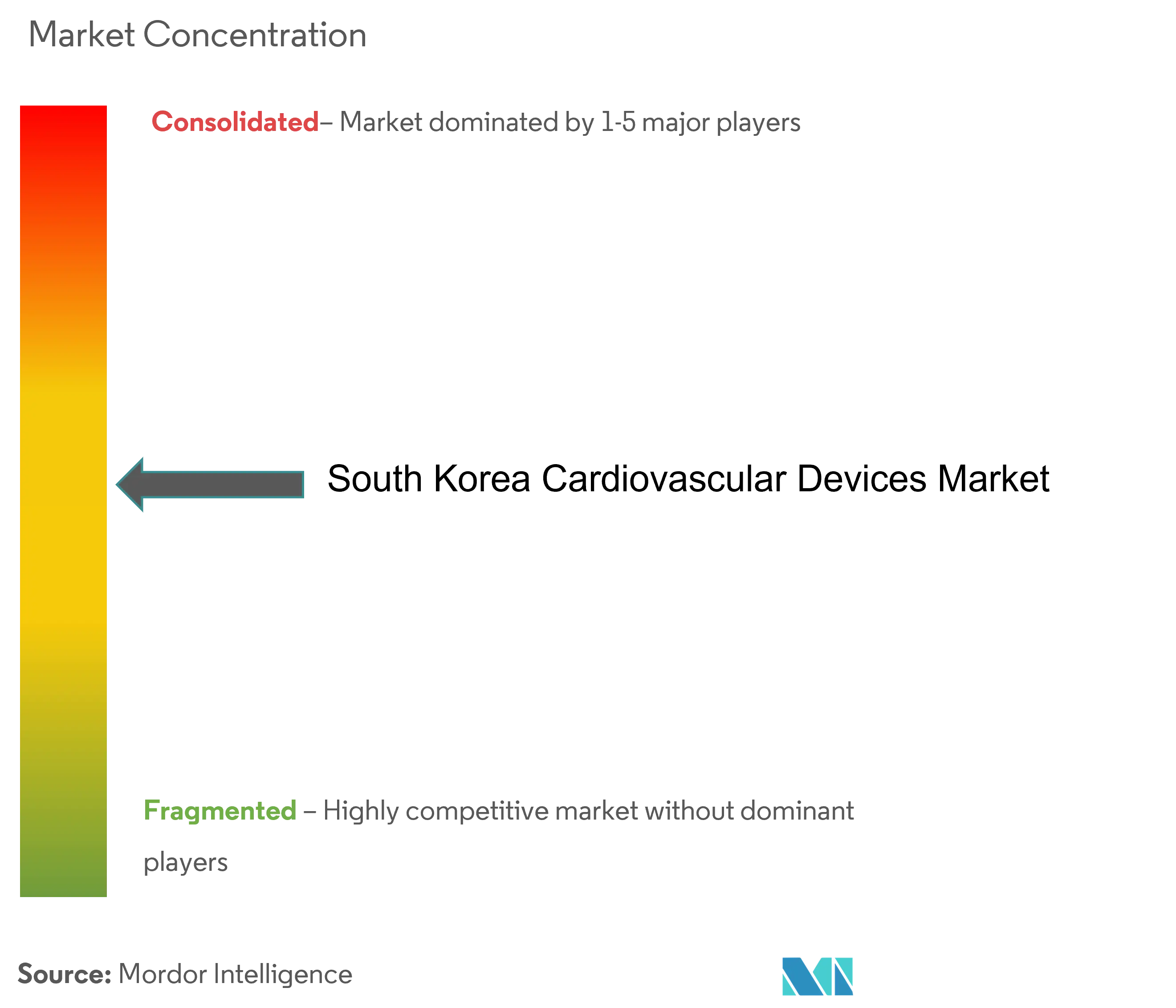

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Cardiovascular Devices Market Analysis by Mordor Intelligence

The South Korea Cardiovascular Devices Market size was valued at USD 1.29 billion in 2025 and estimated to grow from USD 1.39 billion in 2026 to reach USD 1.99 billion by 2031, at a CAGR of 7.47% during the forecast period (2026-2031).

Rising procedure volumes in an aging population, broadening National Health Insurance (NHI) reimbursement for transcatheter therapies, and rapid adoption of high-end imaging and AI software are accelerating demand. Therapeutic and surgical devices currently command 54.20% revenue share, but diagnostic and monitoring systems are expanding briskly on the back of remote-monitoring reimbursement and AI-enabled detection tools. Competitive intensity remains high, with multinationals focusing on premium technologies while domestic firms leverage cost advantages and government innovation grants to capture value in niche sub-segments. Stringent Ministry of Food and Drug Safety (MFDS) pathways for Class-III heart valves, combined with a shortage of provincial interventional cardiologists, temper market growth but open avenues for telemedicine and training solutions.

Key Report Takeaways

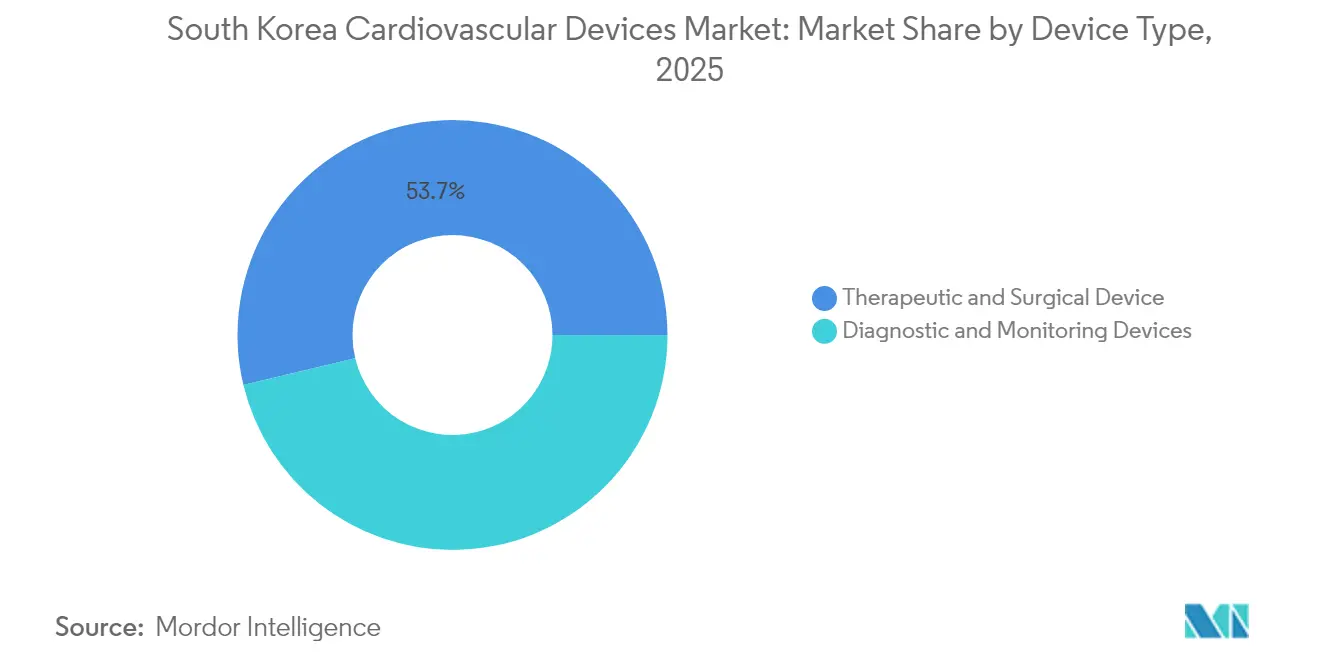

- By device type, therapeutic and surgical devices led with 53.74% revenue share in 2025; diagnostic and monitoring devices are projected to expand at an 7.72% CAGR through 2031.

- By application, coronary artery disease accounted for 54.55% of the South Korea cardiovascular devices market share in 2025, while structural heart disease applications are forecast to grow at a 8.76% CAGR by 2031.

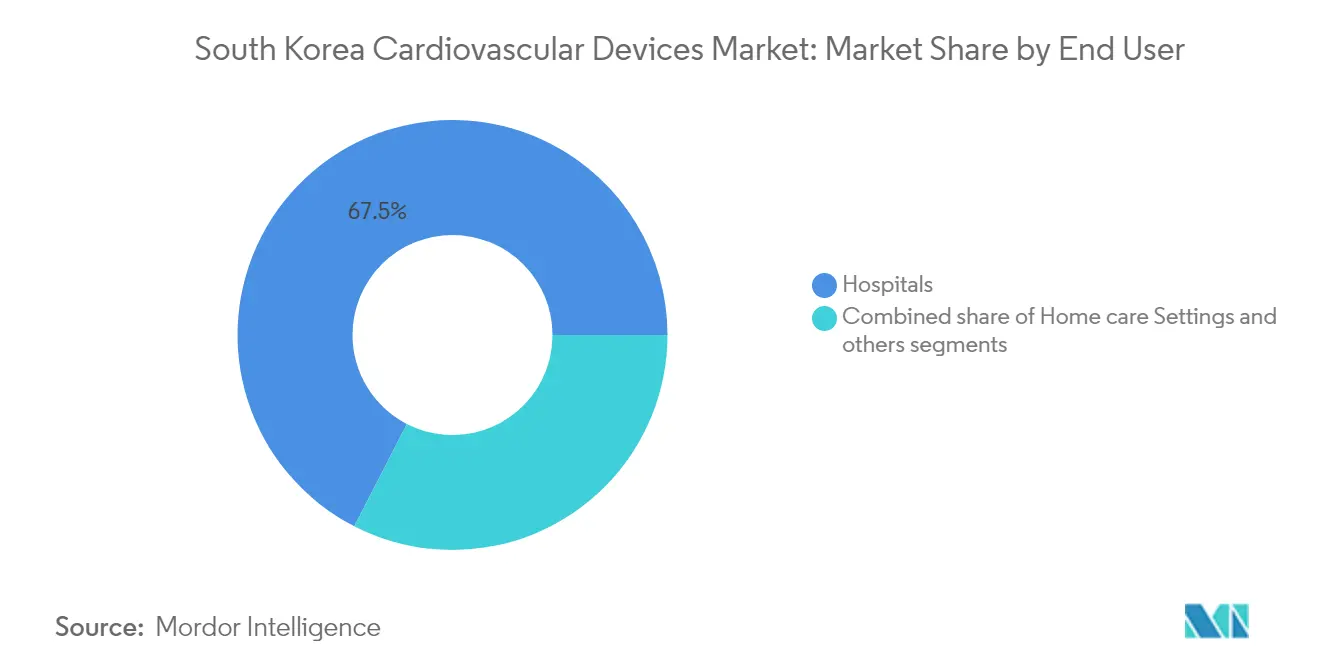

- By end user, hospitals held 67.45% share of the South Korea cardiovascular devices market size in 2025; home-care settings are poised to advance at an 8.41% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic Shift to Super-Aged Society Boosting Cardio Procedure Volumes | +2.10% | National, with early gains in Seoul, Busan, Daegu | Long term (≥5 yrs) |

| NHI Reimbursement Expansion for Transcatheter Therapies | +1.80% | National | Medium term (3-4 yrs) |

| Rapid Uptake of High-End Imaging Modalities in Tertiary Hospitals | +1.20% | Urban centers, tertiary hospitals | Short term (≤2 yrs) |

| Cardiovascular AI Software Adoption Driven by Government "Digital Health" Grants | +1.00% | National, with concentration in teaching hospitals | Medium term (3-4 yrs) |

| Domestic Innovation in Drug-Eluting Stent Coatings | +0.80% | National, with manufacturing concentration in Gyeonggi Province | Medium term (3-4 yrs) |

| Rise of Same-Day PCI Programs in Metropolitan Clinics | +0.50% | Seoul Capital Area, Busan metropolitan region | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Demographic Shift to a Super-Aged Society

South Korea already counts 17.5% of its citizens at least 65 years old in 2024, and official projections place seniors at nearly 35% by 2045. Cardiovascular procedure volumes are rising 12% each year, with octogenarians representing 22% of all percutaneous coronary interventions in 2024. Device makers have responded with geriatric-oriented designs that offer enhanced durability, simplified user interfaces, and embedded remote-monitoring chips. Hospitals are seeing longer lengths of stay and growing demand for low-profile catheters and smaller valve sizes that fit frail anatomies. These trends reinforce multiyear visibility for device replacement demand and recurring consumables.

NHI Reimbursement Expansion for Transcatheter Therapies

In April 2024 the National Health Insurance scheme extended coverage to transcatheter aortic valve replacement for intermediate-risk patients, opening treatment to an additional 4,200 cases annually. TAVR volumes jumped 37% quarter-over-quarter in Q2 2024, with Edwards Lifesciences and Medtronic jointly serving 78% of the expanded pool. The reimbursement upgrade also included drug-coated balloons for peripheral artery disease and next-generation left-atrial-appendage closure systems, giving suppliers multiple avenues for growth. Analysts at the Health Insurance Review & Assessment Service estimate a 22% increase in overall cardiovascular procedure volumes and an 8% reduction in total care costs tied to fewer surgical complications and shorter hospital stays.

Rapid Uptake of High-End Imaging Modalities

The share of tertiary hospitals equipped with cardiac CT integrated with fractional-flow-reserve analysis climbed 43% in 2024, primarily in Seoul, Busan, and Daegu. FFR-CT workflows have cut invasive coronary angiography by 28% and improved diagnostic accuracy, according to Seoul National University Hospital’s outcomes audit. Hospitals are simultaneously upgrading echocardiography systems with 3D strain imaging and adopting cardiac MRI protocols with tissue characterization, fuelling a 32% rise in capital expenditure on cardiovascular imaging in 2024. Domestic supplier Samsung Medison is winning tenders through cost-competitive packages that include AI post-processing modules.

Cardiovascular AI Software Adoption

Government “Digital Health Innovation” grants worth USD 87 million in 2024 earmarked 42% of funds for tertiary centers and 38% for regional hospitals, accelerating adoption of AI algorithms for ECG, echo, and CT analysis. ECG AI software now reads 68% of inpatient tracings and cuts interpretation time 22%. AI-assisted echo improves ejection-fraction accuracy 18% while AI-enabled coronary CT reduces false positives 24%. Remote-monitoring platforms report a 33% fall in readmissions among heart-failure users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent MFDS Approval Pathway for Class-III Heart Valves | -1.40% | National | Medium term (3-4 yrs) |

| Workforce Shortage of Interventional Cardiologists in Provincial Areas | -0.90% | Provincial areas | Long term (≥5 yrs) |

| Declining Unit Prices Under KNHIS Price-Cut Cycles | -0.70% | National | Medium term (3-4 yrs) |

| High Reliance on Imported Heart-Valve Components Amid Weak Won | -0.40% | National, with higher impact on premium segment | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Stringent MFDS Approval Pathway for Class-III Heart Valves

Enhanced MFDS regulations implemented in January 2024 require durability testing of 600 million cycles and thorough thrombogenicity profiling, extending approval timelines to 22 months compared with 11 months in the United States. Compliance expenses rose 35%, prompting three domestic valve developers to prioritize Southeast-Asian launches where requirements are lighter. Smaller firms face liquidity strain, while established players adjust by front-loading bench testing and investing in local clinical trials to shorten review cycles. Hospitals experience longer technology refresh lags, delaying patient access to latest-generation valves.

Workforce Shortage of Interventional Cardiologists in Provincial Areas

Seoul boasts 4.7 interventional cardiologists per 100,000 residents versus 1.8 in provincial regions, below the OECD benchmark of 2.5. Patients outside metropolitan hubs wait 37% longer for elective interventions and undergo 22% fewer advanced device therapies despite comparable disease prevalence. Eighty-six percent of 2024 fellowship graduates accepted Seoul posts, widening the gap. The Ministry of Health and Welfare is rolling out rural practice incentives and tele-consult networks, yet provincial cath-lab utilization remains constrained.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Leadership amid Diagnostic Upswing

Therapeutic and surgical devices held a 53.74% revenue slice of the South Korea cardiovascular devices market in 2025, buoyed by high drug-eluting-stent penetration where DES comprised 87% of placements. The cardiac-rhythm-management niche is gaining renewed momentum after NHI endorsed leadless pacemakers and subcutaneous ICDs, sparking double-digit unit growth. Structural-heart interventions now absorb an expanding capital budget as TAVR case counts jumped 37% year-over-year following intermediate-risk coverage.

Diagnostic and monitoring devices, though smaller, are projected to show an 7.72% CAGR, outpacing the broader South Korea cardiovascular devices market. Remote cardiac monitors dominate momentum thanks to reimbursement for post-discharge surveillance paired with AI arrhythmia detection, a combination that cut heart-failure readmissions 42% in a 2024 multi-center trial. Echo systems sit atop diagnostic spending, with 3D strain imaging triggering accelerated replacement cycles, while optical fractional-flow-reserve systems gain share by slashing procedural time in cath labs.

By Application: Structural Heart Upsets Coronary Dominance

Coronary-artery-disease solutions captured 54.55% of the South Korea cardiovascular devices market in 2025, reflecting entrenched percutaneous infrastructure and consistent stent demand. Nevertheless, structural-heart-disease therapies are charting a 8.76% CAGR through 2031, the highest among applications, boosted by intermediate-risk TAVR coverage and the rollout of transcatheter edge-to-edge mitral repair. Mitral-valve procedure volumes are already rising after Asan Medical Center set up the first dedicated repair center in 2024.

Arrhythmia management sits as the second-largest application, with atrial-fibrillation ablation growing 28% in 2024 on the strength of high-power short-duration protocols and contact-force-sensing catheters. Heart-failure device use is expanding via implantable hemodynamic sensors and percutaneous ventricular-assist systems, while peripheral-artery interventions benefit from drug-coated-balloon reimbursement.

By End User: Hospitals Rule yet Home-Care Ascends

Hospitals controlled 67.45% of revenue in 2025, cementing their status as anchor customers for the South Korea cardiovascular devices market. University-affiliated centers alone account for 63% of hospital sales, with the top 20 institutions conducting 72% of complex interventions. Capital outlays jumped 28% as facilities built hybrid suites and adopted photon-counting CT scanners.

Home care represents the fastest-growing setting at an 8.41% CAGR, propelled by insurance-funded remote monitoring, mobile telemetry, and smartphone ECG devices. Reimbursed home-based cardiac rehab launched in April 2024 and is opening fresh device demand beyond the hospital walls. Ambulatory surgical centers and specialized heart clinics, although smaller, are proliferating in Seoul and Busan to meet demand for focused day procedures.

Geography Analysis

The Seoul Capital Area amassed roughly 49.30% of the South Korea cardiovascular devices market in 2025, enabled by its dense network of tertiary hospitals and 4.7 interventional cardiologists per 100,000 residents, far above the national mean. TAVR penetration runs 2.3 times the national level, and leadless-pacemaker implants sit 1.8 times higher, testifying to the region’s tech-forward orientation. Concentrated purchasing clout, coupled with early AI adoption, clarifies why suppliers prioritize Seoul for product launches and clinical studies.

The southeastern corridor of Busan, Ulsan, and Gyeongsang provinces accounts for 22.60% of 2025 sales and is expanding rapidly following USD 42 million in Ministry of Health and Welfare grants dedicated to cardiovascular service-line upgrades. Busan University Hospital opened a Cardiovascular Center of Excellence that repatriated referrals formerly bound for Seoul, a trend expected to swell local device consumption. Regional insurers are piloting bundled-payment models that reward prompt discharge and remote follow-up, favoring minimally invasive and home-monitoring solutions.

Provincial regions beyond major metros confront under-utilization, purchasing just 63% of national average device volumes after adjusting for population, mainly because interventional-physician density lags and many facilities lack hybrid ORs.

Competitive Landscape

The top five suppliers held a combined more than 50% of share of the South Korea cardiovascular devices market in 2024, indicating moderate concentration. Abbott, Boston Scientific, and Terumo dominate premium stents and structural-heart portfolios, while domestic entrants such as Genoss, Osstem Cardiotech, and HDX are carving out value-tier spaces through price-performance plays backed by state R&D subsidies. Cost-controlled local production is allowing Korean brands to bid aggressively in public tenders, squeezing margins for global incumbents.

Technology-driven differentiation is shaping competition. Edwards Lifesciences filed Korean Patent KR20240035721 covering AI-enhanced hemodynamic optimization for transcatheter valves, signaling a move toward data-rich procedural ecosystems. JLK Inspection seized early mover advantage in AI cardiac imaging analytics, securing MFDS clearance for its UNIST platform that dovetails with photon-counting CT systems. Meanwhile, Samsung Biologics unveiled a Digital Health Solutions unit to blend semiconductor-level miniaturization with remote-patient-monitoring applications, leveraging its manufacturing heft in biologics to enter cardiology adjacency.

Strategic acquisitions are altering the playing field. Boston Scientific bought Genoss for USD 270 million in March 2025, inheriting local manufacturing talent and a CE-marked sirolimus stent platform, accelerating its Korea sourcing footprint. Abbott secured MFDS clearance for its next-generation Navitor TAVR in April 2025, broadening its structural-heart suite and setting the stage for price-protective multi-product contracts. Philips and Siemens lock horns in imaging, each landing landmark photon-counting CT orders at flagship hospitals that include bundled AI analytics and managed-service terms.

South Korea Cardiovascular Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic PLC

Cardinal Health Inc.

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: South Korea’s Digital Medical Products Act took full effect, creating a streamlined approval track for AI-enabled cardiovascular devices and digital therapeutics.

- August 2024: The Ministry of Health and Welfare announced program to upgrade cardiovascular services in underserved provinces, funding imaging, cath labs, and telehealth infrastructure.

South Korea Cardiovascular Devices Market Report Scope

As per the scope of the report, cardiovascular devices are used for the diagnosis of heart diseases and treatment of related health problems. The South Korean cardiovascular devices market is segmented by the cardiovascular device (type (cardiac rhythm management devices, interventional cardiac devices, automated external defibrillators (AED), cardiac ablation catheters, cardiac pacemakers, cardiac angioplasty devices, implantable cardioverter defibrillators (ICD), Prosthetics (artificial) heart valves, stents, ventricular assist devices), and technology (cardiopulmonary bypass products, minimally invasive cardiac surgery, valve prosthesis and repair, and cardiac assist devices). The report offers the value (in USD million) for all the above segments.

By Device

| Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | ||

| Cardiac MRI | ||

| Cardiac CT | ||

| Echocardiography / Ultrasound | ||

| Fractional Flow Reserve (FFR) Systems | ||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents |

| Bare-Metal Stents | ||

| Bioresorbable Stents | ||

| Catheters | PTCA Balloon Catheters | |

| IVUS/OCT Catheters | ||

| Cardiac Rhythm Management | Pacemakers | |

| Implantable Cardioverter Defibrillators | ||

| Cardiac Resynchronization Therapy Devices | ||

| Heart Valves | TAVR/TAVI | |

| Mechanical Valves | ||

| Tissue/Bioprosthetic Valves | ||

| Ventricular Assist Devices | ||

| Artificial Hearts | ||

| Grafts & Patches | ||

| Other Cardiovascular Surgical Devices | ||

By Indication

| Coronary Artery Disease |

| Arrhythmia |

| Heart Failure |

| Valvular Heart Disease |

By End User

| Hospitals |

| Home care Settings |

| Others |

| By Device | Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | |||

| Cardiac MRI | |||

| Cardiac CT | |||

| Echocardiography / Ultrasound | |||

| Fractional Flow Reserve (FFR) Systems | |||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents | |

| Bare-Metal Stents | |||

| Bioresorbable Stents | |||

| Catheters | PTCA Balloon Catheters | ||

| IVUS/OCT Catheters | |||

| Cardiac Rhythm Management | Pacemakers | ||

| Implantable Cardioverter Defibrillators | |||

| Cardiac Resynchronization Therapy Devices | |||

| Heart Valves | TAVR/TAVI | ||

| Mechanical Valves | |||

| Tissue/Bioprosthetic Valves | |||

| Ventricular Assist Devices | |||

| Artificial Hearts | |||

| Grafts & Patches | |||

| Other Cardiovascular Surgical Devices | |||

| By Indication | Coronary Artery Disease | ||

| Arrhythmia | |||

| Heart Failure | |||

| Valvular Heart Disease | |||

| By End User | Hospitals | ||

| Home care Settings | |||

| Others | |||

Key Questions Answered in the Report

What is the current size of the South Korea cardiovascular devices market?

Market size stands at USD 1.39 billion in 2026 and is projected to hit USD 1.99 billion by 2031.

Which device type leads revenue in South Korea?

Therapeutic and surgical devices command 53.74% of 2025 revenue, led by drug-eluting stents.

Why are structural-heart devices growing faster than other segments?

Expanded NHI reimbursement for intermediate-risk TAVR and aging demographics drive a 8.76% CAGR in structural-heart applications.

How is AI impacting cardiovascular care in the country?

AI tools reduce ECG interpretation time 22%, improve echo accuracy 18%, and lower readmissions 33%, fueling adoption across hospitals.

Page last updated on: