Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

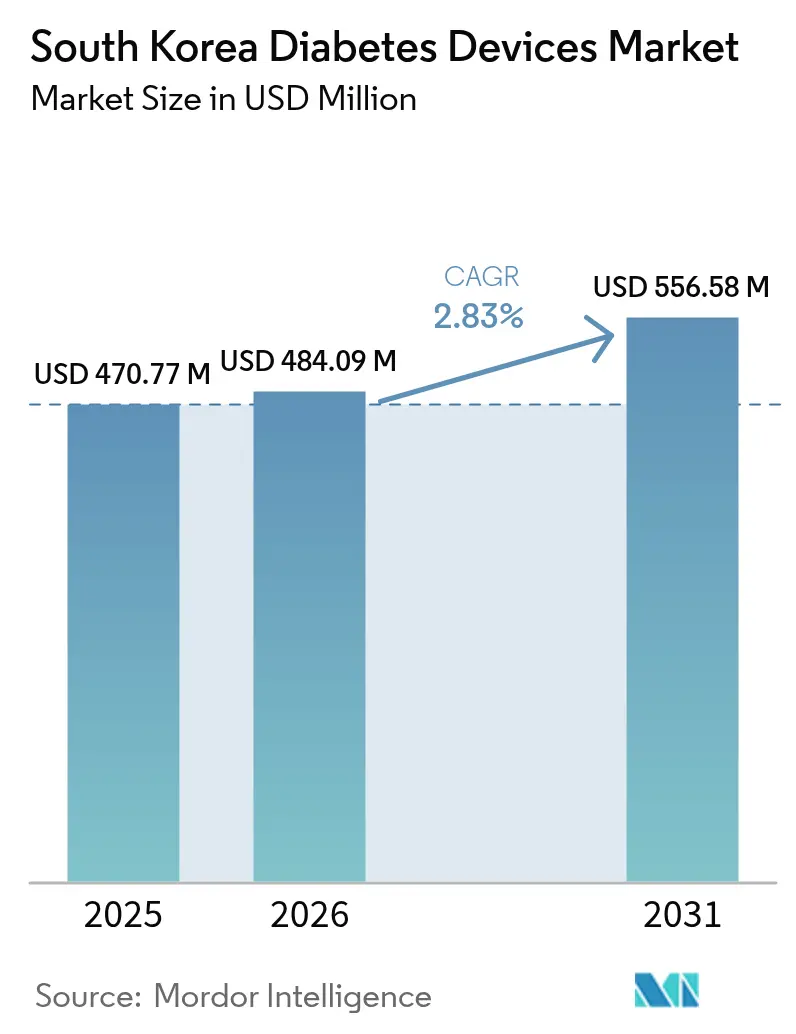

| Base Year Market Size (2025) | USD 470.77 Million |

| Market Size (2026) | USD 484.09 Million |

| Market Size (2031) | USD 556.58 Million |

| Growth Rate (2026 - 2031) | 2.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Diabetes Devices Market Analysis by Mordor Intelligence

The South Korea diabetes devices market size is expected to grow from USD 470.77 million in 2025 to USD 484.09 million in 2026 and is forecast to reach USD 556.58 million by 2031 at 2.83% CAGR over 2026-2031. Demand remains resilient because 29.3% of adults aged 65 and older live with diabetes, a share that continues to rise as the population ages. Competitive intensity is sharpening as domestic manufacturers scale up, the National Health Insurance Service (NHIS) extends coverage for continuous glucose monitoring (CGM) and insulin pumps, and 5G-enabled telemedicine broadens access to specialist care. Simultaneously, strict reference pricing from the Health Insurance Review and Assessment Service (HIRA) is pressuring margins, compelling firms to localize production and recalibrate product portfolios. Market leadership is gravitating toward companies that pair hardware with artificial-intelligence software capable of predicting glycemic excursions, because outcomes-based reimbursement is gaining traction.

Key Report Takeaways

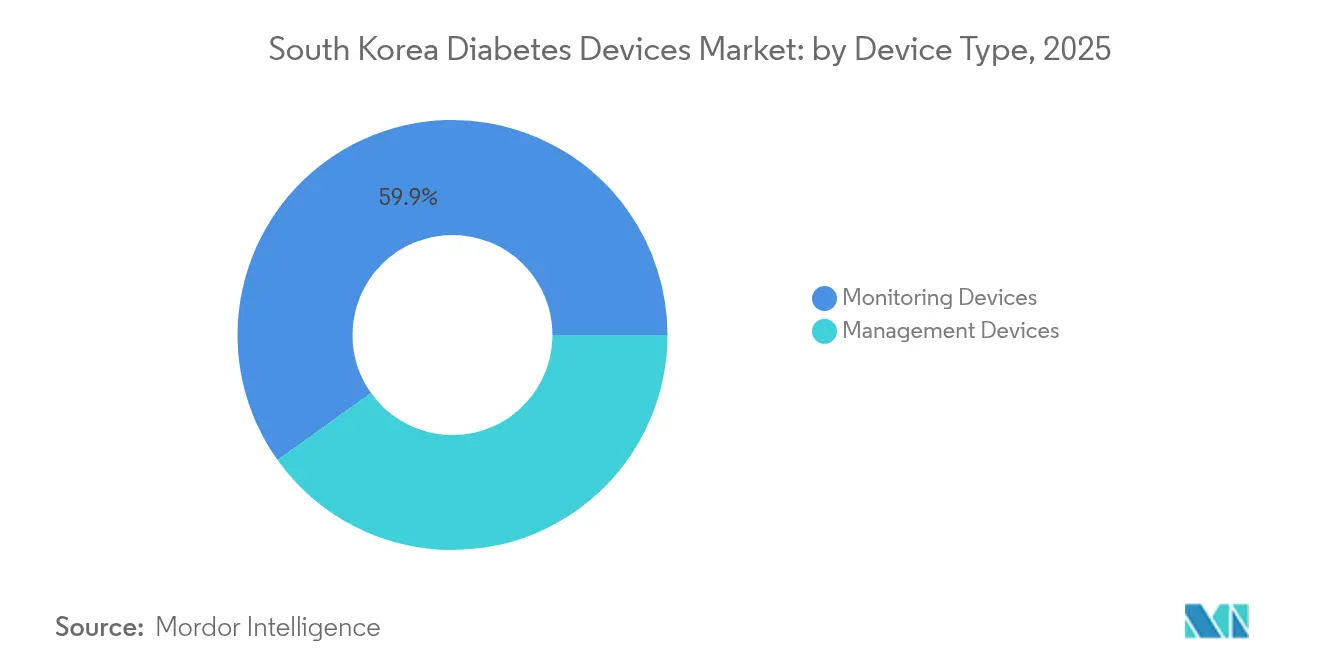

- By device type, Monitoring Devices led with 59.87% of the South Korea diabetes devices market share in 2025, while Management Devices are projected to expand at a 4.02% CAGR through 2031.

- By end user, Hospitals & Specialty Clinics controlled 54.62% of the South Korea diabetes devices market size in 2025, whereas Home-Care Settings are advancing at a 4.28% CAGR.

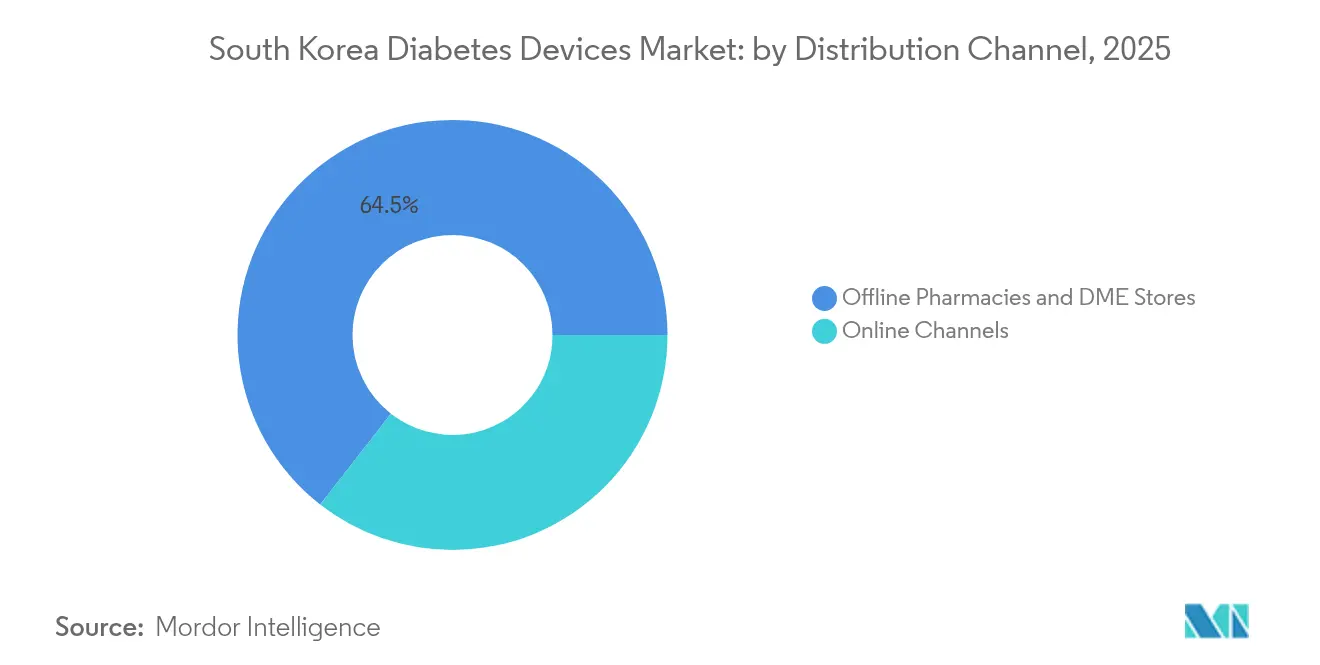

- By distribution channel, Offline Pharmacies & DME Stores accounted for 64.45% of the South Korea diabetes devices market size in 2025; Online Channels are growing at a 3.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence and earlier age of onset | +0.6% | National; stronger in urban centers | Long term (≥ 4 years) |

| Government reimbursement expansion for advanced glucose monitoring and insulin delivery | +1.0% | National; earliest uptake in Seoul, Busan, Incheon | Medium term (2-4 years) |

| Growth of digital health ecosystem and 5G connectivity enabling remote diabetes management | +0.8% | National; metro concentration | Medium term (2-4 years) |

| Government-led K-Bio strategy and tax incentives attracting local production of sensors, pumps, and smart pens | +0.4% | Songdo and other biotech hubs | Medium term (2-4 years) |

| Increasing adoption of home-based self-care practices among aging population | +0.5% | National; higher impact in regions with aging demographics | Short term (≤ 2 years) |

| Domestic med-tech manufacturing investments supported by K-Bio and export incentives | +0.4% | National; export-oriented clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence and Earlier Age of Onset in South Korea

South Korea’s diabetes prevalence has climbed to 15.5% among adults aged 30 and older, and 2.2% among adults aged 19-39, creating unprecedented lifetime demand for monitoring and delivery devices [1]Se Eun Park et al., “Diabetes Fact Sheets in Korea 2024,” Diabetes & Metabolism Journal, e-dmj.org. Earlier onset means patients now spend more years using technology-enabled interventions, a pattern that lengthens device replacement cycles and raises cumulative revenue per patient. Roughly 87.1% of young adults with diabetes are obese, further increasing the need for continuous metabolic insight and prompting manufacturers to design low-profile, lifestyle-compatible CGM sensors. Awareness remains lower among young adults (43.3%) than seniors (78.8%), signaling untapped potential for targeted education and early screening programs that can lift device penetration. This demographic-driven demand is expected to keep the South Korea diabetes devices market on a stable upward trajectory even as price controls intensify.

Government Reimbursement Expansion for Advanced Glucose Monitoring and Insulin Delivery

NHIS began reimbursing CGM sensors and transmitters in 2019 and has since broadened eligibility for insulin pumps, reducing out-of-pocket costs and triggering a sharp rise in prescriptions across all age groups [2]National Health Insurance Service, “Health Keeper e-Brochure,” nhis.or.kr. Reimbursement now focuses on outcomes metrics such as time-in-range and hypoglycemia events, strengthening the business case for devices with proven clinical effectiveness. Earlier access to advanced tools is improving long-term glycemic control, which supports payer objectives to curb costly complications. The South Korea diabetes devices market is therefore seeing a pivot from single-function glucometers toward integrated monitoring-and-delivery ecosystems that align with payer priorities.

Growth of Digital Health Ecosystem and 5G Connectivity Enabling Remote Diabetes Management

South Korea’s nationwide 5G rollout delivers real-time, low-latency data flow that links CGM sensors to cloud analytics and telehealth portals, unlocking predictive insights and automated insulin titration. Rural patients now receive specialist input via high-definition video consults, and a cost-minimization study showed telemedicine cut per-consultation societal costs by USD 7.92, primarily from avoided travel [3]Sei-Jong Baek et al., “Cost-Minimization Analysis of Teleconsultation Versus In-Person Care,” mdpi.com. Device vendors are embedding 5G modules and open APIs to ensure seamless interoperability with hospital information systems, helping clinicians integrate continuous data into electronic medical records. The capability leap is steering the South Korea diabetes devices market toward always-on, algorithm-supported care models.

Increasing Adoption of Home-Based Self-Care Practices Among Aging Population

With 29.3% of adults aged 65 and older diagnosed, seniors are embracing home-based monitoring that minimizes hospital visits and supports independent living. Manufacturers are releasing age-friendly interfaces featuring large fonts, haptic alerts, and voice commands to overcome vision and dexterity barriers. Urban seniors often pair CGM with smartphone dashboards, while rural users rely on simplified readers integrated with telemedicine hubs. This behavioral shift is expanding the South Korea diabetes devices market into non-traditional retail avenues, including direct-to-consumer subscription models that bundle sensors and coaching.

Domestic Med-Tech Manufacturing Investments Supported by K-Bio and Export Incentives

The K-Bio initiative, tax credits, and expedited review pathways are fueling heavy capital spending by local firms such as i-SENS, which invested KRW 500 billion (USD 50 million) to scale CGM production at its Songdo plant. Localized assembly defrays tariff exposure, lowers logistics costs, and allows faster iteration for Korean-specific clinical needs, while export grants position domestic brands for Southeast-Asian expansion. These factors underpin a maturing value chain that adds capacity and price flexibility to the South Korea diabetes devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent pricing controls and reference pricing limiting device margins | −0.5% | National | Long term (≥ 4 years) |

| High out-of-pocket costs for advanced insulin pumps despite partial reimbursement | −0.3% | Rural and lower-income areas | Medium term (2-4 years) |

| Regulatory delays for novel wearable and implantable sensors | −0.2% | National | Short term (≤ 2 years) |

| Physician preference for established therapies slowing uptake of alternative delivery technologies | −0.1% | Outside major metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Pricing Controls and Reference Pricing Limiting Device Margins

HIRA benchmarks diabetes devices against reference countries, often granting reimbursement 30-40% below US and EU levels, squeezing returns on high-R&D products [4]Kwon Soonman, “Price Setting and Price Regulation in Health Care: Republic of Korea,” World Health Organization, who.int. CGM and pump makers confront a conundrum: South Korea’s tech-forward market is ideal for showcasing innovation, yet margin realization lags. Firms respond by redesigning products with fewer bundled accessories, moving production to local plants, or adopting software-subscription models that shift revenue to post-sale services. Without structural change, low pricing will continually shadow the South Korea diabetes devices market.

High Out-of-Pocket Costs for Advanced Insulin Pumps Despite Partial Reimbursement

Patients still pay more than KRW 2 million (USD 1,500) upfront for premium pumps, plus ongoing consumable fees, generating tiered adoption aligned with income levels. Low-income patients with diabetes show nearly triple the all-cause mortality of higher-income peers, evidencing inequity in access to optimal technologies. Unless reimbursement is extended to disposables, pump uptake will stay concentrated in affluent urban segments, tempering overall South Korea diabetes devices market growth.

Regulatory Delays for Novel Wearable and Implantable Sensors

The Korean Food and Drug Administration’s rigorous clinical-evidence demands can extend time-to-market, particularly for implantable CGM or optical sensors that lack long-term safety data. While the Digital Medical Products Act (2025) promises streamlined pathways for AI-embedded devices, short-term backlog persists, slowing the commercial rollout of next-generation solutions and muting near-term gains in the South Korea diabetes devices market.

Physician Preference for Established Therapies Slowing Uptake of Alternative Delivery Technologies

Endocrinologists and diabetes educators lean toward familiar regimens, delaying adoption of needle-free injectors or closed-loop AID systems in favor of proven pens and pumps. Consensus-guideline updates take years, so clinical inertia keeps innovators in lengthy pilot programs before broad uptake, trimming the speed at which advanced modalities penetrate the South Korea diabetes devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Monitoring Devices Lead While Management Innovations Accelerate

Monitoring Devices account for 59.87% of 2025 revenue, underscoring their central role in real-time decision support across both Type 1 and insulin-treated Type 2 populations. Continuous glucose monitoring is the fastest-rising sub-segment as Korean Diabetes Association guidelines now recommend real-time CGM for all adults with Type 1 and for selected Type 2 cases. The South Korea diabetes devices market size for CGM is propelled by superior HbA1c reductions, with real-time users dropping from 8.9% to 7.1% versus intermittently-scanned users who fell from 8.6% to 7.5%. Local production by i-SENS lowers costs, potentially widening uptake.

Management Devices, while smaller today, are increasing at 4.02% CAGR and include patch pumps, traditional pumps, and connected pens that feed data to cloud dashboards. Domestic wearable-pump specialist EOFlow and multinationals Medtronic and Tandem are iterating closed-loop algorithms that adjust basal flow every five minutes, positioning the South Korea diabetes devices market for a coming wave of automated insulin delivery (AID) systems. Integration of CGM and pump data into unified apps is narrowing the functional gap between monitoring and management solutions, blurring category lines and encouraging ecosystem competition.

By End User: Home-Care Settings Gaining Ground Through Digital Integration

Hospitals & Specialty Clinics hold 54.62% revenue as they remain the gatekeepers for device initiation, insurance paperwork, and complications management. Endocrinology centers in Seoul National University Hospital and Samsung Medical Center often run specialized diabetes technology clinics where certified educators train new CGM and pump users. Institutional demand nevertheless faces modest growth because reimbursement reforms encourage outpatient follow-up and because connected devices reduce the need for in-office titration.

Home-Care Settings are expanding at 4.28% CAGR as remote monitoring platforms mature. Real-time dashboards relay sensor data to cloud portals that allow clinicians to adjust therapy without physical visits, crucial for seniors with mobility constraints. Subscription bundles that mail fresh sensors every fortnight mirror consumer electronics models, keeping patients adherent and boosting consumables revenue. Growing adoption of voice-activated smart speakers that deliver glucose alerts further integrates diabetes care into daily living, deepening the South Korea diabetes devices market presence inside homes.

By Distribution Channel: Digital Transformation Reshaping Access Pathways

Offline Pharmacies & DME Stores captured 64.45% share in 2025 because they blend walk-in convenience with personalized counseling. Community pharmacists provide point-of-care HbA1c testing, cost checks, and device demonstrations, thereby reinforcing trust for older patients wary of online purchases. Automated inventory systems ensure timely stocking of CGM sensors and pump consumables, which mitigates supply disruptions and supports adherence.

Online Channels grow at 3.74% CAGR as post-pandemic consumers value doorstep delivery, bundled discounts, and subscription replenishment for sensors and infusion sets. Major e-commerce platforms integrate prescription verification modules that satisfy regulatory controls while simplifying ordering. Some hospitals partner with online pharmacies to auto-populate shopping carts based on electronic prescriptions, reducing errors and creating a frictionless path from teleconsultation to product fulfillment. The resulting data stream yields cross-sell insights, helping the South Korea diabetes devices market shift toward predictive logistics.

Geography Analysis

Metropolitan hubs—Seoul, Busan, and Incheon—anchor 82% of the urban population and act as early adopters of premium devices owing to higher disposable incomes and dense specialist networks. CGM penetration is highest in Seoul clinics where real-time trend arrows facilitate tight glycemic control for professionals with erratic schedules. NHIS coverage ensures baseline access nationwide, but advanced technology uptake still varies by region. Rural provinces such as North Gyeongsang report lower CGM use, primarily because older residents face digital literacy gaps and longer device-training travel times.

Government initiatives under the Digital New Deal are narrowing these divides by subsidizing 5G base-station rollouts and telehealth kiosks in community centers. A cost-minimization study confirmed telemedicine saved USD 7.92 per visit in underserved areas, validating the economic logic for continued infrastructure funding. Mobile health vans outfitted with point-of-care HbA1c analyzers and CGM starter kits tour remote villages, onboarding patients who later transition to app-based follow-up. As these efforts mature, the South Korea diabetes devices market gains incremental volume outside traditional metropolitan strongholds.

Demographic differences also drive geographic strategies. Rural counties exhibit faster population aging, making them prime targets for devices with simplified user interfaces and caregiver notification features. Urban marketing, by contrast, highlights analytics dashboards and fitness-wearable integrations that resonate with tech-savvy workers managing type 2 diabetes alongside active lifestyles. The Community-Based Hypertension and Diabetes Control Program integrates local clinics, pharmacies, and civic groups, offering a new distribution node for CGM sensors and smart insulin pens.

Regulatory Landscape

South Korea regulates diabetes devices under the Ministry of Food and Drug Safety (MFDS) using a four-tier, risk-based classification system (Class I to IV). Class II to IV products generally require technical documentation review, and for higher-risk devices, clinical evidence. For drug-device and connected device combinations, early MFDS classification consultation matters because combination products are routed based on primary mode of action.

Manufacturers must also meet Korean Good Manufacturing Practice (KGMP) requirements for Class II to IV devices as part of the market authorization process. After MFDS clearance, broad commercial access depends on reimbursement and price positioning via the National Health Insurance Service (NHIS) and Health Insurance Review and Assessment Service (HIRA), with the National Evidence-based Healthcare Collaborating Agency (NECA) health technology assessment acting as an additional gate for new technologies. HIRA reference pricing pressure remains a defining constraint for premium CGM and pump portfolios.

Value Chain Analysis

The value chain begins with component sourcing (sensors, microelectronics, adhesives, and infusion-set consumables), moves into device manufacturing and assembly (increasingly localized for select players), and then proceeds through MFDS authorization and KGMP quality compliance. Payer access follows a separate sequence, including NECA health technology assessment and HIRA reimbursement listing, before NHIS coverage drives volume. For imported products, international manufacturers commonly operate through a Korea License Holder (KLH) for registration and post-market obligations, which adds an in-country compliance and distribution layer.

Downstream, hospitals and specialty clinics remain central to initiation and training, while offline pharmacies and DME stores handle most recurring consumables fulfillment, supported by growing online subscription replenishment. Integration with domestic digital health platforms is becoming an operational step in the chain, evidenced by hospital-facing data aggregation (for example, iKooB LabConnect) and partnerships that embed CGM data into clinical workflows. Distribution structures also matter for control and support, such as Dexcom's domestic supply arrangement with Kakao Healthcare (December 2025), which couples device supply with local operation and user support.

Competitive Landscape

The South Korea diabetes devices market features moderate concentration with multinationals Abbott, Dexcom, and Medtronic holding strong portfolios, while domestic innovators such as i-SENS and EOFlow rapidly capture share. Abbott’s FreeStyle Libre enjoys brand recognition, but price-sensitive consumers increasingly evaluate the locally developed CareSens Air, approved in 2024, which offers comparable accuracy at lower cost. Dexcom is leveraging a June 2023 partnership with Kakao Healthcare to couple G7 sensors with Korea’s dominant messaging platform, simplifying data sharing between patients and providers.

Medtronic signed a global pact with Abbott in August 2024 to align sensors and pumps, ensuring cross-compatibility and easing regulatory filings for integrated systems. EOFlow differentiates via tubeless patch pumps that pair with its Narsha iOS app, offering discrete insulin delivery favored by younger adults. Local manufacturing, supported by K-Bio tax incentives, allows i-SENS and EOFlow to price aggressively yet maintain margins, intensifying competition for hospital tenders.

Strategic focus is shifting from hardware specifications to ecosystem depth. Vendors now bundle cloud analytics, coaching chatbots, and physician dashboards under subscription plans, locking in recurring revenue and elevating switching costs. Opportunities remain in geriatric-oriented solutions: products combining large-text displays, fall detection, and caregiver alerts are underrepresented. As the Digital Medical Products Act formalizes AI safety standards, software differentiation will gain regulatory clarity, and companies with established data-science talent will hold an edge. Overall, rivalry is firm but not monopolistic, leaving space for specialized entrants targeting niche needs within the South Korea diabetes devices market.

South Korea Diabetes Devices Industry Leaders

Abbott Diabetes Care

Eli Lilly and Comapny

Dexcom

Medtronic

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity is reducing import dependence in core monitoring categories. In 2024, import reliance for CGM and test strips was reported at 92.5% and 93.8%, respectively, despite category expansion in glucose monitoring over 2020-2024. This creates room for domestic manufacturing scale-up and localization of sensor and strip supply, consistent with local investment momentum (for example, i-SENS scaling CGM production capacity at Songdo) and payer-driven pressure to lower unit costs under HIRA reference pricing.

A second opportunity is ecosystem-level differentiation through AI and clinical integration. The Digital Medical Products Act (effective January 24, 2025) and government programs supporting AI-enabled chronic disease management provide a regulatory and policy anchor for this direction. Partnerships already visible in the market, including Dexcom with Kakao Healthcare and hospital-platform integrations such as FreeStyle Libre 2 with iKooB LabConnect, indicate a procurement shift toward devices that can feed EMRs and clinician dashboards. That, in turn, creates space for vendors to package CGM, decision-support software, and workflow integrations into reimbursable pathways for hospitals, specialty clinics, and home-care monitoring programs.

Recent Industry Developments

- March 2026: Dexcom and Kakao Healthcare held the inaugural DynamiK Symposium events in Seoul and Busan focused on CGM-based diabetes management. The program reinforced clinical adoption by centering on real-world CGM use and data sharing, supporting broader uptake of connected monitoring through a local platform partner.

- December 2025: Dexcom and Kakao Healthcare signed an exclusive domestic supply agreement covering Dexcom CGM devices, including the G7, in South Korea. The arrangement strengthens control over distribution and patient support in a reimbursement-led market, and it positions a single local operator to scale onboarding, education, and app-based data services.

- April 2024: Medtronic Korea began direct distribution and sales of its diabetes management devices in South Korea. Moving closer to end users and providers can shorten response times for training, servicing, and consumables logistics, which are critical for pump therapy persistence in hospital-initiated care pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers diabetes devices sold and used in South Korea that help people measure blood glucose or deliver insulin, including the related consumables and the linked device software used for monitoring or dosing.

Scope exclusions: We exclude oral anti-diabetic drugs, hospital lab analyzers used for biochemical testing, and general wellness wearables that do not measure glucose or support insulin delivery.

Segmentation Overview

- By Device Type

- Monitoring Devices

- Self-Monitoring Blood Glucose Devices

- Continuous Glucose Monitoring Devices

- Management Devices

- Insulin Pumps

- Insulin Syringes

- Cartridges in Reusable Pens

- Insulin Disposable Pens

- Jet Injectors

- Monitoring Devices

- By End User

- Hospitals & Specialty Clinics

- Home-Care Settings

- By Distribution Channel

- Offline Pharmacies & DME Stores

- Online Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public health and utilization signals that explain how large the diabetes device demand pool can be, and where the next growth wave is coming from. We used Korea Disease Control and Prevention Agency materials for diabetes prevalence signals, the National Health Insurance Service and HIRA for reimbursement and pricing context, and Statistics Korea for population aging trends that influence the treated patient base.

To connect demand to shipments and spending, we also reviewed import and export statistics from the Korea Customs Service, relevant Ministry of Food and Drug Safety publications on device approvals and rules, and peer-reviewed clinical literature on CGM and pump adoption in Korea. These inputs were then cross-checked against company filings, investor presentations, association updates, and a paid subscription for company financials, news, and patent intelligence to confirm product focus and launch timing. The desk sources listed here are illustrative only, and we used other public references to validate and clarify assumptions during the work.

Primary Interviews and Surveys

Primary work focused on validating what is actually being used and paid for in South Korea across monitoring and insulin delivery, and how quickly newer technologies are replacing older ones. We spoke with a mix of device manufacturers and distributors, hospital and clinic stakeholders, and pharmacy or channel-side respondents to confirm reimbursement coverage, typical replacement cycles, and pricing ranges for key consumables.

To avoid over-counting, feedback was also taken on what should be treated as a diabetes device sale versus adjacent digital health services, and on how tendering, formulary access, and patient out-of-pocket behavior can shift volumes year to year.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | |

| Mid tier: 49% | Functional/Unit leaders: 31% | |

| Smaller Players: 22% | Managers: 56% |

Market-Sizing & Forecasting

Sizing was built using a mix of top-down and bottom-up checks, so the final number stays tied to real demand signals without assuming every company sale can be fully rolled up. On the top-down side, we reconstructed device spending by linking the treated diabetes population in South Korea to monitoring frequency and insulin usage patterns, then mapping those to device penetration and annual consumable needs.

A few of the practical inputs that shaped the model include diabetes prevalence by age band, CGM and SMBG adoption mix, test strip and sensor replacement intervals, insulin delivery split across pens and pumps, and the pricing and reimbursement logic that influences realized selling prices. These assumptions were stress-tested with selective bottom-up approximations, such as sample channel checks for unit volumes and ASPs by device type, followed by gap-filling where coverage is limited by using proxy uptake rates from similar care settings.

For forecasting, scenario analysis was used, since reimbursement expansion, guideline changes, and upgrade cycles can move adoption faster than a simple trend line. The scenarios were anchored on expected shifts in CGM penetration, pump coverage, and the pace of aging, and then adjusted after primary feedback on how hospitals and pharmacies expect ordering patterns to change.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including patient pool math, reimbursement and pricing context, and trade flow direction checks for relevant device categories. When a value looked out of range, we re-opened the assumptions, re-ran the calculations, and re-contacted respondents if the mismatch could not be explained through timing or policy changes.

Before sign-off, the model and supporting logic go through multi-step analyst review so definitions, additions, and currency handling stay consistent across years. Reports are refreshed annually, and interim updates are made when there are material events such as coverage changes, large pricing resets, or major product approvals, followed by a final pre-delivery review to keep the numbers current.

Mordor Intelligence's South Korea Diabetes Devices Market Size Compared With Other Published Estimates

Published market sizes for South Korea diabetes devices can look far apart, even when the topic name sounds the same. The differences usually come from what each estimate counts as a device, whether consumables are fully included, and how pricing is treated when reimbursement rules change.

Reimbursement coverage signals and replacement-cycle checks for sensors, test strips, and pump consumables are the evidence used to keep Mordor Intelligence aligned to what is actually consumed in the country, instead of blending in broader diabetes care spend. When another estimate expands the boundary to include wider diabetes care categories or applies aggressive long-range adoption assumptions, the near-term market value can move up quickly even if unit usage does not.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 484.09 M (2026) | |

| Industry Publisher A | USD 395.70 M (2025) | Uses a different base year and a longer forecast window, and the scope description leans toward a narrower device-and-channel view that can understate consumables tied to monitoring frequency. |

| Industry Publisher B | USD 1.48 B (2024) | Appears to use a broader diabetes care devices boundary and may bundle adjacent device-related categories, which can inflate totals compared with a patient-facing monitoring and insulin delivery device-only definition. |

Taken together, the spread in values is mainly explained by scope boundaries and how utilization and pricing are translated into spending. By keeping the inputs tied to observable demand drivers like penetration, replacement cadence, and reimbursed pricing behavior, the estimate stays repeatable and easier to audit when assumptions are updated.

Key Questions Answered in the Report

How big is the South Korea Diabetes Devices Market?

The South Korea Diabetes Care Devices Market size is expected to reach USD 484.09 million in 2026 and grow at a CAGR of 2.83% to reach USD 556.58 million by 2031.

Which device category leads sales in South Korea?

Monitoring Devices, particularly CGM systems, command 59.87% of 2025 revenue.

Who are the key players in South Korea Diabetes Devices Market?

Abbott Diabetes Care, Eli Lilly and Comapny, Dexcom, Medtronic and Novo Nordisk A/S are the major companies operating in the South Korea Diabetes Devices Market.

Are pricing controls a major challenge?

Yes. HIRA reference pricing can be 30-40% below US/EU levels, squeezing margins and potentially delaying next-generation launches.

Page last updated on: