Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

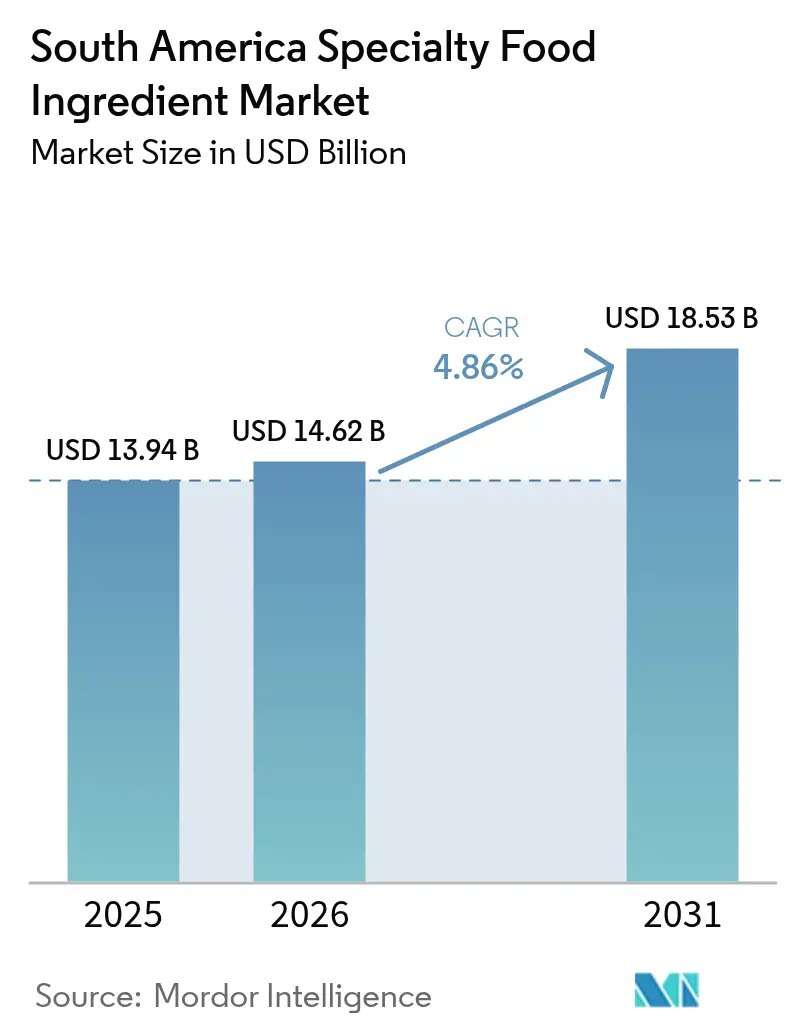

| Base Year Market Size (2025) | USD 13.94 Billion |

| Market Size (2026) | USD 14.62 Billion |

| Market Size (2031) | USD 18.53 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

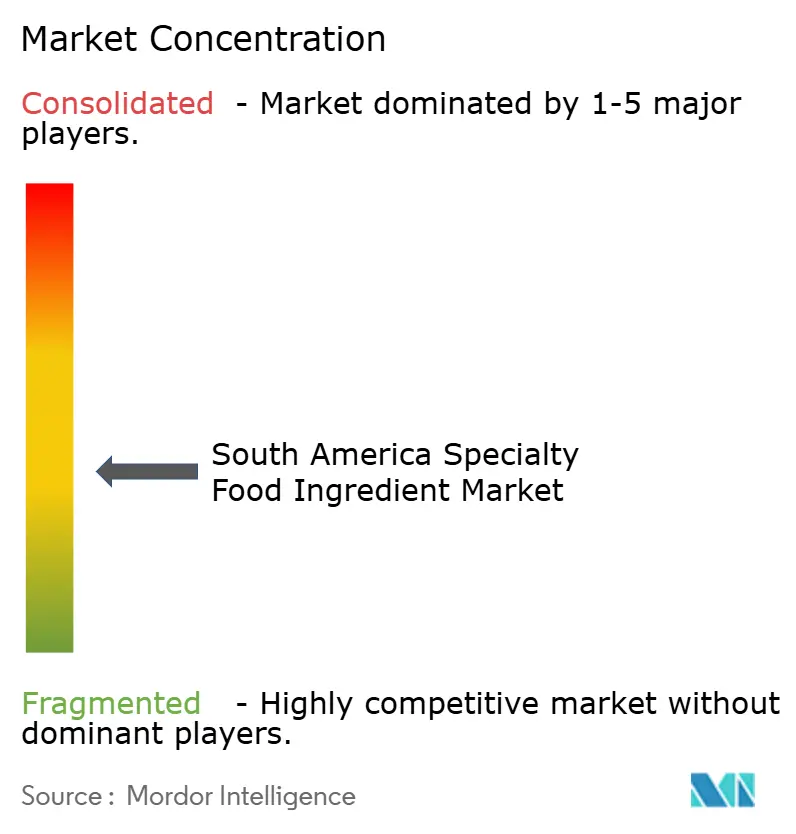

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Specialty Food Ingredient Market Analysis by Mordor Intelligence

The specialty food ingredients market size in South America is expected to grow from USD 13.94 billion in 2025 to USD 14.62 billion in 2026 and is forecast to reach USD 18.53 billion by 2031 at 4.86% CAGR over 2026-2031. The market growth is driven by the expansion of the food and beverage processing sector across Brazil, Argentina, and Chile, where urbanization and higher disposable incomes are influencing consumer preferences toward processed and ready-to-eat food products. Health-conscious consumers in South America are increasing the demand for functional food options, including natural sweeteners, plant-based proteins, probiotics, and dietary fibers. Consumer preference for clean-label products has prompted manufacturers to develop products with minimally processed ingredients and transparent ingredient lists. The market is further strengthened by government policies supporting food innovation and increased investments from multinational food companies and ingredient suppliers, which enhance technological capabilities and product development in the region.

Key Report Takeaway

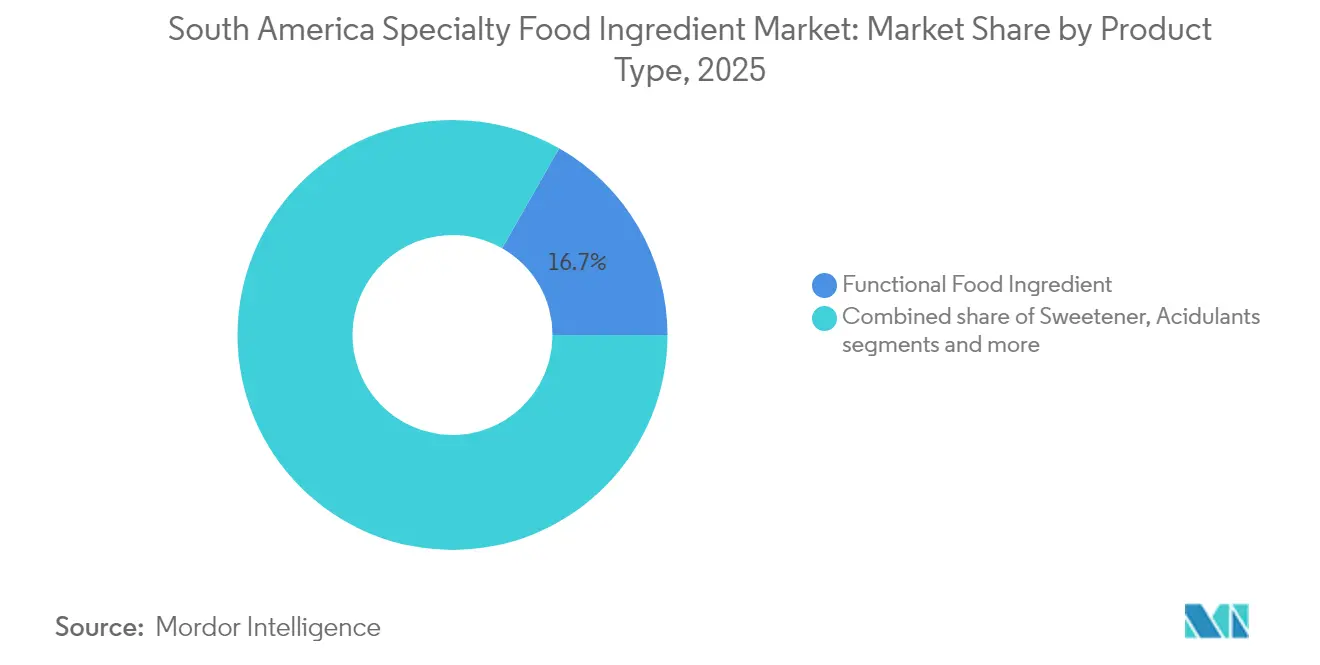

- By product type, functional food ingredients led with 16.74% revenue share in 2025; the enzymes segment is forecast to expand at a 5.71% CAGR to 2031.

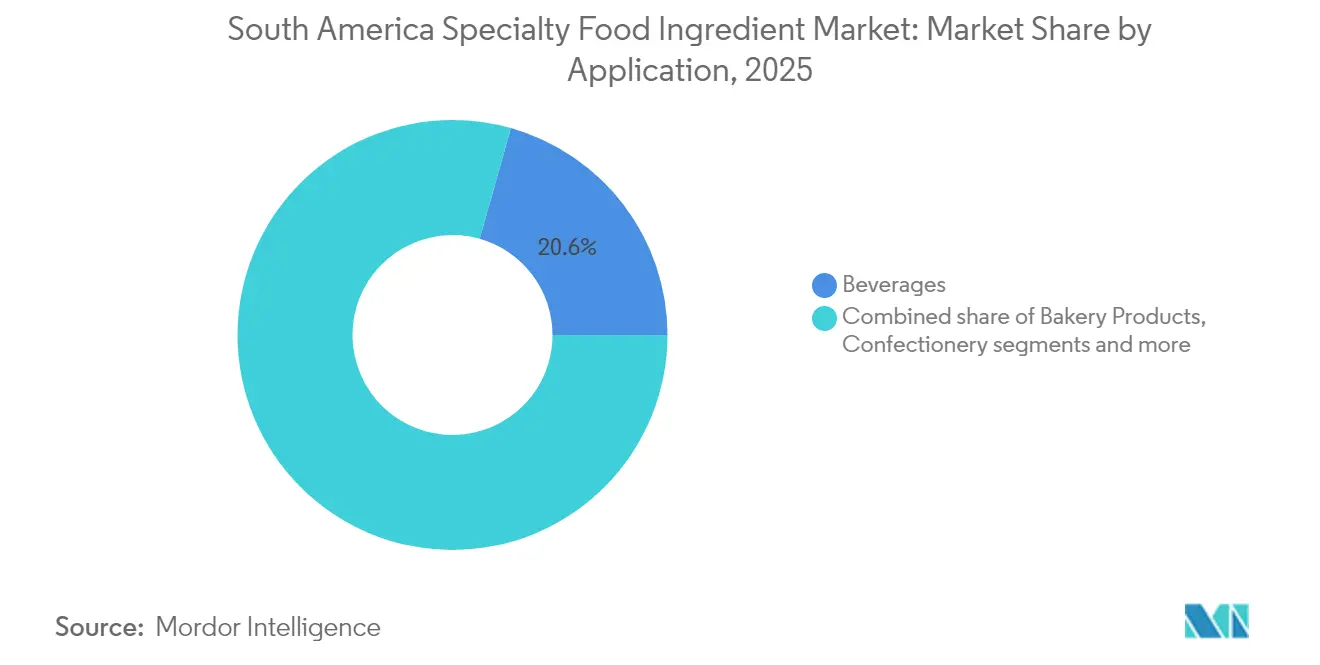

- By application, beverages accounted for 20.62% of the specialty food ingredients market share in 2025, whereas plant-based food and beverage applications are projected to post the fastest CAGR of 6.12% through 2031.

- By geography, Brazil held 54.82% of the specialty food ingredients market size in 2025, while Argentina is poised to grow at a 6.02% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Specialty Food Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of food processing sector | +1.2% | Brazil, Argentina, Chile | Medium term (3-4 years) |

| Rise of plant-based and vegan diets | +0.9% | Brazil, Argentina, Rest of South America | Long term (≥ 5 years) |

| Consumer demand for fortified food and beverage products | +0.7% | Brazil, Chile, Argentina | Medium term (3-4 years) |

| Technological advancements in ingredient processing | +0.6% | Brazil, Argentina | Long term (≥ 5 years) |

| Rising consumer demand for natural and clean-label food products | +0.4% | Brazil, Argentina, Chile | Medium term (3-4 years) |

| Urbanization and changing dietary patterns | +0.3% | Brazil, Argentina, Rest of South America | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Expansion of Food Processing Sector

The specialty food ingredients market in South America demonstrates robust growth, primarily driven by Brazil's food processing industry, which generated revenues of USD 233 billion in 2024, representing a 9.9% increase from the previous year, according to the USDA Foreign Agricultural Service. The market expansion stems from increasing requirements for functional ingredients that enhance product quality, extend shelf life, and deliver specific nutritional benefits. According to the Brazilian Institute of Geography and Statistics (IBGE), the country's 2025 harvest increased by 5.8% compared to 2024, reaching 311 million tonnes [1]Source: Brazilian Institute of Geography and Statistics (IBGE), "First forecast for 2025 harvest expects growth of 5.8% against 2024", www.agenciadenoticias.ibge.gov.br. Soybean production is projected to rise by 10.9%, adding up to 160.2 million tonnes in 2025, while corn (1st crop) production is expected to increase by 9.1% to 24.9 million tonnes in relation to the 2024 harvest, according to the first forecast of the Systematic Survey of Agricultural Production (LSPA). This substantial agricultural output strengthens the specialty food ingredients market by ensuring a consistent supply of raw materials for ingredient manufacturing.

Rise of Plant-Based and Vegan Diets

The South American specialty food ingredients market is experiencing significant growth due to increasing consumer adoption of plant-based and vegan diets. Health consciousness, animal welfare considerations, and environmental concerns are driving consumers, particularly urban residents and younger demographics, to reduce their consumption of animal-based products. This shift has increased demand for plant-based alternatives, including meat substitutes, dairy-free beverages, egg alternatives, and vegan snacks. Brazilian retail sales of plant-based meat and seafood alternatives reached USD 223.5 million in 2023, representing a 38% increase from 2022, according to the Good Food Institute. Government support is also strengthening the market, with several South American authorities implementing supportive policies and initiatives. The Brazilian Ministry of Health's dietary guidelines promote whole, minimally processed plant-based foods while recommending reduced consumption of meat and ultra-processed products. Additionally, São Paulo has implemented "Meatless Monday" programs in public schools and institutions, expanding the demand for plant-based ingredients in institutional food service.

Consumer Demand for Fortified Food and Beverage Products

In South America, increasing consumer demand for fortified food and beverage products serves as a primary driver for the specialty food ingredients market. The combination of heightened health consciousness, accelerated urbanization, and expansion of the middle-class demographic has resulted in a substantial shift in consumer preferences toward nutritionally enhanced food products. Fortified products, incorporating essential components such as vitamins, minerals, fibers, probiotics, and bioactive compounds, address prevalent nutritional deficiencies, including iron-deficiency anemia and vitamin D insufficiency. Within key markets such as Brazil and Argentina, fortified beverages, breakfast cereals, and dairy products have demonstrated significant market penetration, particularly among working-class families and health-conscious millennials. For instance, according to the International Labour Organization (ILO), Argentina recorded a workforce of over 3.4 million employed individuals aged between 35 and 44 in 2023 [2]Source: International Labour Organization (ILO), "Number of employed persons in Argentina", www.ilo.org.

Technological Advancements in Ingredient Processing

Advanced ingredient processing technologies are driving growth in the South American specialty food ingredients market. Consumer preferences for clean-label, fortified, and functional foods have increased the adoption of modern processing methods to develop ingredients with improved stability, bioavailability, and nutritional properties. Key technologies include microencapsulation, enzyme-assisted extraction, fermentation, and nanotechnology, which enable manufacturers to create ingredients that meet consumer and industrial requirements. Microencapsulation technology helps mask the unpleasant tastes of vitamins and minerals while improving shelf life and enabling controlled release in fortified products. These processing methods also facilitate the incorporation of sensitive compounds, such as omega-3 fatty acids and probiotics, into various food formats. In Brazil and Chile, developments in biotechnology and food engineering have enabled local manufacturers to expand into global markets by producing specialized ingredients, including natural colorants, clean-label emulsifiers, and plant-based protein concentrates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expensive certification and testing requirements | -0.8% | Brazil, Argentina, Chile | Medium term (3-4 years) |

| Lack of ingredients traceability system | -0.6% | Brazil, Argentina, Rest of South America | Short term (≤ 2 years) |

| Limited research and development capabilities compared to other markets | -0.6% | Brazil, Argentina, Chile | Long term (≥ 5 years) |

| Logistical challenges from poor transportation networks | -0.1% | Brazil, Argentina, Rest of South America | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Expensive Certification and Testing Requirements

Stringent certification and testing requirements across South America create significant cost barriers for specialty ingredient manufacturers, particularly affecting smaller companies with limited resources. Brazil's National Health Surveillance Agency (Anvisa) regulates food additives and technological aids through RDC 778/2023 and IN 211/2023, which specify permitted additives and their usage limits. The regulatory framework operates on risk analysis principles to ensure safety and technological necessity, requiring substantial investment in testing and documentation. Regulatory updates based on scientific advancements and international standards create ongoing compliance challenges. While RDC 843/2024 exempts certain additives from registration requirements for industrial food production, the complex regulatory landscape increases costs and potentially restricts innovation and market entry for new ingredients.

Lack of Ingredients Traceability System

The specialty food ingredients market in South America faces significant growth constraints due to inadequate ingredients traceability systems. The region's fragmented supply chains, limited digital infrastructure, manual documentation processes, and inconsistent cross-border regulations make it challenging to track ingredients from source to final product. This poses difficulties for manufacturers in verifying the origin, quality, and handling of raw materials, particularly for specialty ingredients like botanical extracts, organic acids, and natural preservatives. As global food companies implement stringent traceability requirements for ESG compliance, South American suppliers without proper traceability systems risk market access limitations, product recalls, and potential reputational damage from contamination or adulteration issues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Product Type: Functional Ingredients Lead Innovation Wave

The product type segmentation shows that Functional Food Ingredients held a 16.74% market share in 2025, driven by increasing consumer awareness of health benefits and demand for foods with specific functional properties. This segment's growth is supported by scientific advancements in ingredient efficacy and bioavailability, as manufacturers invest in clinical validation to substantiate health claims. The Food Ingredients South America (FiSA) 2024 event report by Sebrae highlighted sustainability, health, and technology trends in food production. The event, held from August 6-8, 2024, in São Paulo, showcased innovations in plant-based products, upcycled ingredients, and food waste reduction solutions.

From 2026 to 2031, the enzymes category is projected to witness a CAGR of 5.71%. The rising adoption of enzymes across diverse sectors such as food, agriculture, and pharmaceuticals drives this growth. These industries favor enzymes for their advantages, including heightened efficiency, shortened processing times, and environmentally friendly attributes. Specifically, in the food sector, enzymes play a pivotal role in enhancing product quality, substituting synthetic chemicals, and bolstering the eco-friendliness of production processes. Ingredion's 2024 Annual Report indicated double-digit organic sales growth in its Texture & Healthful Solutions segment, attributed to higher-value specialty starches and clean-label texturizers. The company maintains manufacturing facilities in South America, focusing on local sourcing and efficient supply chains. The report noted successful debottlenecking initiatives in Colombia and Mexico, which increased production capacity for specialty ingredients.

Application: Beverages Drive Volume, Plant-Based Accelerates

In the application segmentation, Beverages held the largest market share at 20.62% in 2025, driven by the region's warm climate and increasing consumer interest in functional and fortified drink options. According to PepsiCo's 2024 Annual Report, Latin America contributed 13% to the company's total revenue of USD 91.854 billion, with the company focusing on portfolio evolution to meet consumer needs. Plant-based Food and Beverage applications are expected to grow at a CAGR of 6.12% from 2026-2031, indicating the expansion of plant-based alternatives across the region.

The plant-based specialty food ingredients market is growing due to health and environmental concerns, particularly in plant-based milk and meat alternatives. Bakery products constitute a significant application segment, with manufacturers using specialty ingredients to improve texture, shelf life, and nutritional content. The segment is characterized by increased demand for healthy and functional foods, sustainable production practices, and food technology innovations.

Geography Analysis

Brazil holds a 54.82% share of the South American Specialty Food Ingredients Market in 2025, supported by its established food processing infrastructure and agricultural capabilities. The country's food processing sector generated revenues of USD 233 billion in 2024, according to the U.S. Department of Agriculture . The market shows significant dependence on imported food ingredients, creating opportunities for suppliers. Brazilian consumers demonstrate increasing preference for plant-based products and transparent ingredient sourcing.

Argentina's specialty food ingredients market is expected to grow at a CAGR of 6.02% from 2026-2031. Following a 1.7% economic contraction in 2023 due to macroeconomic challenges and drought conditions, the country's economy showed a 5.5% growth in 2025, according to the World Bank. This recovery is attributed to improved weather conditions and agricultural investments. World Bank-supported food programs and the country's emphasis on sustainable agriculture and climate resilience contribute to market development.

Chile and other South American countries represent an important segment of the market, with Chile notable for its regulatory standards and health-focused food initiatives. The World Bank's Global Economic Prospects report indicates Latin America and the Caribbean's growth will increase from 2.3% in 2024 to 2.4% in 2025. This growth outlook reflects enhanced external demand and improved agricultural production, particularly in Brazil. While regional inflation is decreasing, allowing for interest rate reductions that may increase investment, the market faces potential challenges from geopolitical issues and climate change impacts on agricultural production and food security.

Competitive Landscape

The specialty food ingredients market in South America demonstrates a moderately fragmented competitive structure, wherein multinational corporations, including Cargill Incorporated, The Archer-Daniels-Midland Company, Ingredion Incorporated, DSM-Firmenich AG, and Kerry Group plc, maintain dominant market positions through their established distribution networks and strategically located production facilities. These organizations implement comprehensive sustainability initiatives and develop clean-label solutions to address evolving consumer preferences and comply with regulatory frameworks.

The market's competitive dynamics continue to transform through strategic mergers, acquisitions, and collaborative ventures, as organizations strengthen their specialty ingredient portfolios and expand their geographical presence. Regional manufacturers establish market differentiation through technological advancement, allocating resources to sophisticated processing methodologies and digital infrastructure to optimize ingredient functionality and enhance supply chain visibility.

Mid-tier regional players are carving out niches in the market through their agility and specialization. Oterra is utilizing annatto and paprika lines, sourced through regenerative-agriculture protocols, and has successfully secured contracts with meat processors aiming for natural color transitions. Furthermore, digital platforms that track farm-level sourcing and carbon intensity are playing a pivotal role in determining contract awards, underscoring the growing significance of traceability credentials in the specialty food ingredients market.

South America Specialty Food Ingredient Industry Leaders

-

Cargill, Incorporated

-

The Archer-Daniels-Midland Company

-

Ingredion Incorporated

-

Kerry Group plc

-

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Arla Food Ingredients introduced a toolbox to assist South American manufacturers in developing high-protein desserts. The toolbox contains 12 recipes and ready-to-mix formulations, including low-fat instant pudding mixes and clear, gelatinous products made with Lacprodan whey protein isolate.

- February 2025: Umami Bioworks introduced hybrid caviar as a B2B ingredient. The product combines plant-based components, including seaweed and natural binders, to replicate the buttery texture and rich flavor profile of premium caviar.

- July 2024: Archer-Daniels-Midland Company established a new premix manufacturing facility in Apucarana, Paraná, which enhanced its production capacity by 40%. The facility specialized in producing combinations of minerals, amino acids, vitamins, and additives.

- July 2023: Tate & Lyle expanded its sweetener portfolio by introducing TASTEVA SOL stevia sweetener. The product demonstrates solubility that is 200 times higher than Reb M and D products. The sweetener readily dissolves in concentrates and maintains its solubility at low pH levels.

South America Specialty Food Ingredient Market Report Scope

Specialty food ingredients are typically utilized in food production for color, texture, blending, and preservation. The South American specialty food ingredient market is segmented by product type, application, and geography. Based on product type, the market is segmented into Functional Food Ingredients, Specialty Starch and Texturants, Sweeteners, Food Flavors and Enhancers, Acidulants, Preservatives, Emulsifiers, Colorants, Enzymes, Proteins, Specialty Fats & Oils, Food Hydrocolloids & Polysaccharides, Anti-Caking Agents, and Others. By application, the market is segmented into Bakery Products, Beverages, Meat, Poultry, and Seafood, Dairy Products, Confectionery, Fats & Oils, Dressings/Condiments/Sauces/Marinade, Pasta, Soup and Noodles, Prepared Food, Plant-based Food and Beverage, and Other Applications. By geography, the market is segmented into Brazil, Chile, Argentina, and the rest of South America. For each segment, market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Functional Food Ingredient |

| Speciality Starch and Texturants |

| Sweetener |

| Food Flavors and Enhancers |

| Acidulants |

| Preservatives |

| Emulsifiers |

| Colorants |

| Enzymes |

| Proteins |

| Speciality Fats & Oils |

| Food Hydrocolloids & Polysaccharides |

| Anti-Caking Agents |

| Others |

By Application

| Bakery Products |

| Beverages |

| Meat, Poultry, and Seafood |

| Dairy Products |

| Confectionery |

| Fats & Oils |

| Dressings/Condiments/Sauces/Marinade |

| Pasta, Soup and Noodles |

| Prepared Food |

| Plant-based Food and Beverage |

| Other Applications |

By Geography

| Brazil |

| Chile |

| Argentina |

| Rest of South America |

| By Product Type | Functional Food Ingredient |

| Speciality Starch and Texturants | |

| Sweetener | |

| Food Flavors and Enhancers | |

| Acidulants | |

| Preservatives | |

| Emulsifiers | |

| Colorants | |

| Enzymes | |

| Proteins | |

| Speciality Fats & Oils | |

| Food Hydrocolloids & Polysaccharides | |

| Anti-Caking Agents | |

| Others | |

| By Application | Bakery Products |

| Beverages | |

| Meat, Poultry, and Seafood | |

| Dairy Products | |

| Confectionery | |

| Fats & Oils | |

| Dressings/Condiments/Sauces/Marinade | |

| Pasta, Soup and Noodles | |

| Prepared Food | |

| Plant-based Food and Beverage | |

| Other Applications | |

| By Geography | Brazil |

| Chile | |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

How large is the specialty food ingredients market in South America today?

The South American Specialty Food Ingredients Market stands at USD 14.62 billion in 2026 and is forecast to reach USD 18.53 billion by 2031.

Which product segment holds the biggest share?

Functional food ingredients lead with a 16.74% share of the specialty food ingredients market in 2025, reflecting robust demand for health-enhancing components.

What is the fastest-growing application area?

Plant-based food and beverage applications are projected to rise at a 6.12% CAGR, outpacing all other categories through 2031.

Why does Brazil dominate regional demand?

Brazil combines a USD 233 billion food-processing industry, extensive crop availability and clear additive regulations, delivering 54.82% of regional revenue in 2025.

Page last updated on: