Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

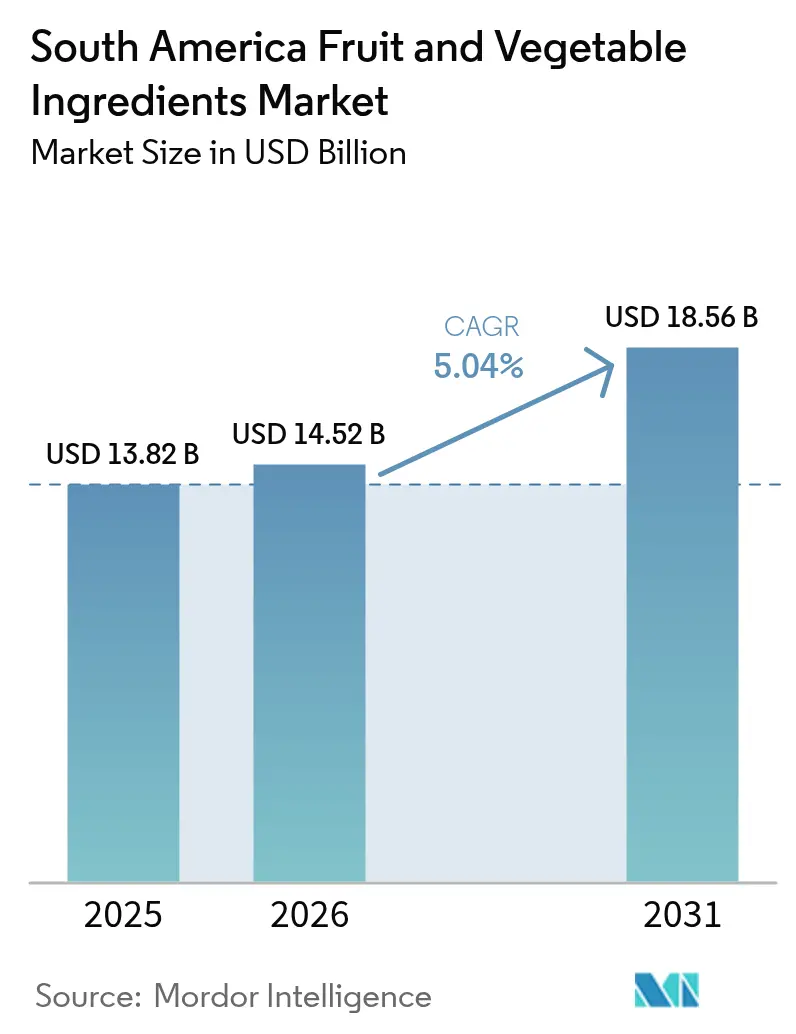

| Base Year Market Size (2025) | USD 13.82 Billion |

| Market Size (2026) | USD 14.52 Billion |

| Market Size (2031) | USD 18.56 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Fruit And Vegetable Ingredients Market Analysis by Mordor Intelligence

The South America fruit and vegetable ingredients market size in 2026 is estimated at USD 14.52 billion, growing from 2025 value of USD 13.82 billion with 2031 projections showing USD 18.56 billion, growing at 5.04% CAGR over 2026-2031. Food processors are increasingly turning to concentrates, purees, and powders, moving away from synthetic additives. This shift not only aligns with retailer demands for shorter ingredient lists but also taps into the premium pricing associated with clean-label formulations. Ingredient buyers are now favoring shelf-stable formats, which help in reducing cold-chain costs. Meanwhile, in a bid to expedite commercialization, governments in Brazil, Argentina, and Chile have streamlined the approval process for natural colorants and flavors, slashing the time by over 50%. Currency fluctuations are playing a pivotal role in export dynamics: as the Real weakens, Brazil's citrus shipments gain momentum, and a dip in the peso boosts exports of Argentine apple and pumpkin concentrates. In the dairy sector, manufacturers are diversifying flavors, particularly in Greek-style yogurt and premium ice cream, where exotic fruit purees can command a retail premium exceeding 40%. The competitive landscape is moderately intense, with multinationals entering toll-processing agreements with cooperatives to secure harvest-season volumes, while regional specialists hone in on organic and non-GMO markets.

Key Report Takeaways

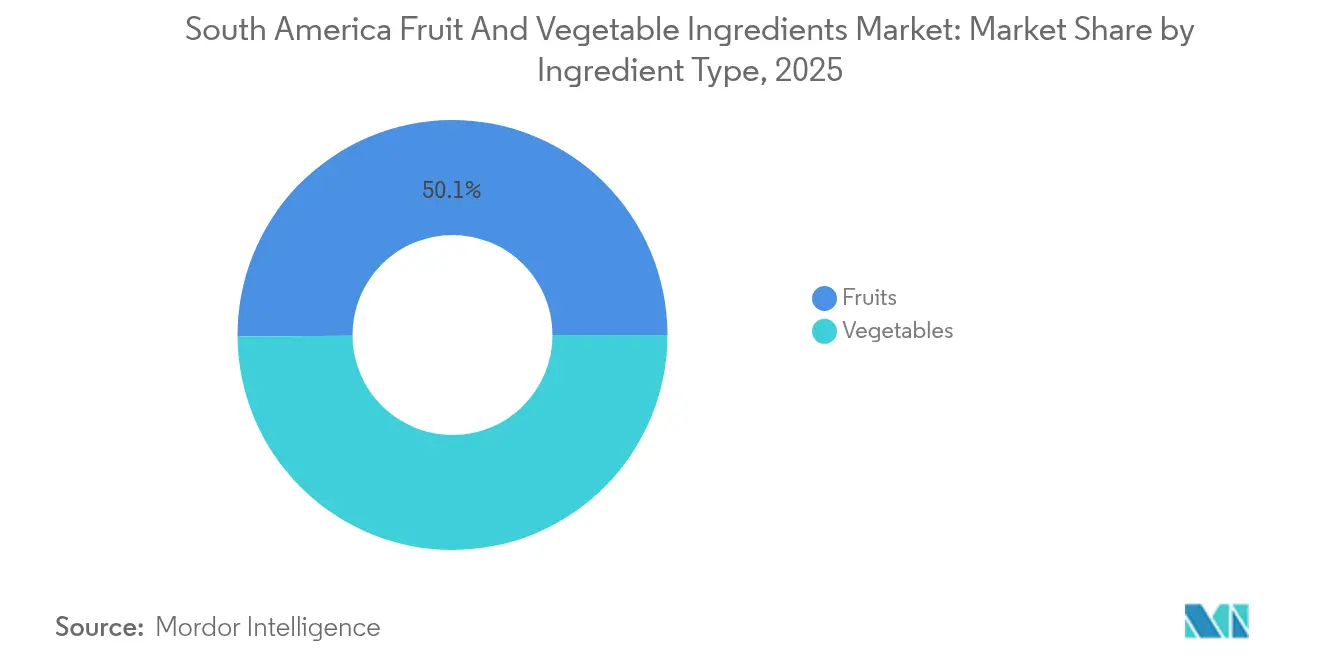

- By ingredient type, fruits led with 50.12% of the South America fruit and vegetable ingredients market share in 2025, while vegetables are forecast to expand at a 6.62% CAGR through 2031.

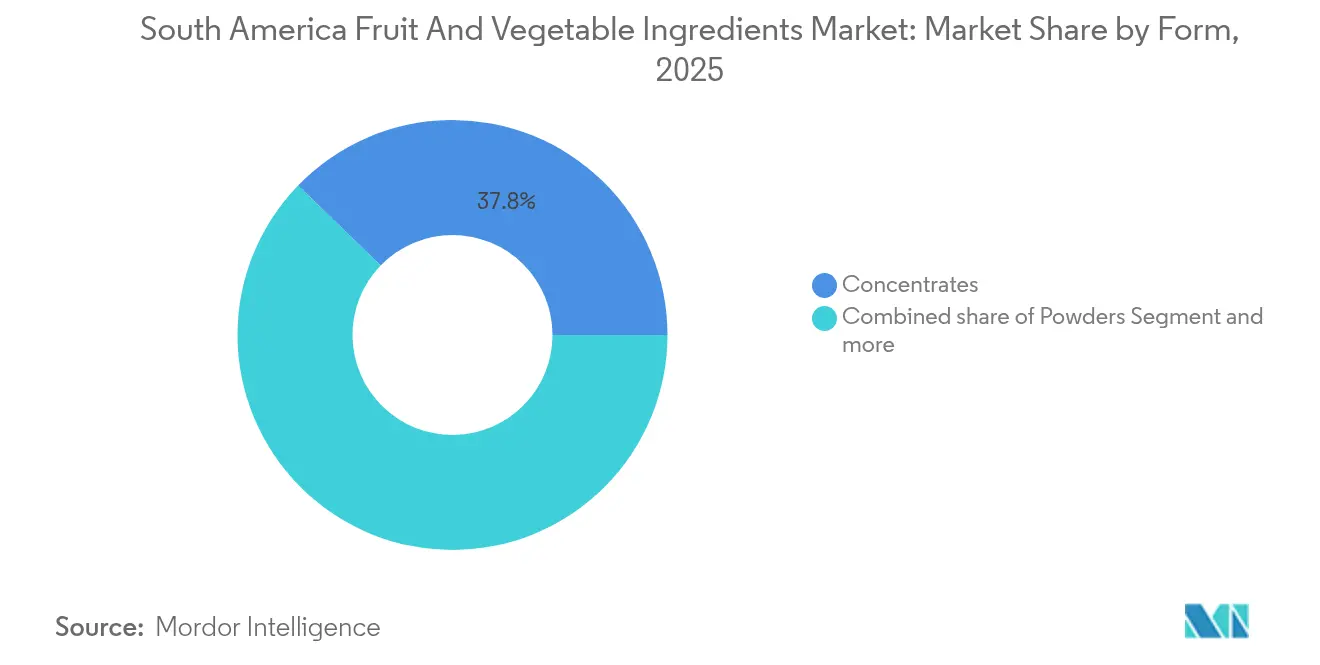

- By form, concentrates accounted for 37.75% of the South America fruit and vegetable ingredients market size in 2025; powders are projected to post the fastest 7.45% CAGR to 2031.

- By application, beverages held 38.55% of demand in 2025, whereas dairy products are expected to advance at a 6.72% CAGR between 2026-2031.

- By geography, Brazil captured 41.20% revenue in 2025; Argentina is set to record the highest 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Fruit And Vegetable Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and clean-label ingredients | +1.2% | Brazil, Argentina, Chile; spillover to Colombia and Peru | Medium term (2-4 years) |

| Expansion of the food processing industry | +1.0% | Brazil (São Paulo, Paraná), Argentina (Buenos Aires, Mendoza), Chile (Maule, O'Higgins) | Long term (≥ 4 years) |

| Shift towards plant-based diets | +0.9% | Brazil, Chile, Argentina urban centers; early adoption in Colombia | Medium term (2-4 years) |

| Product innovation and diversification | +0.8% | Global, with research and development hubs in Brazil and Chile | Short term (≤ 2 years) |

| Chile and Peru bio-economy incentives for ingredient research and development | +0.4% | Chile (Santiago, Valparaíso, Concepción), Perú (Lima, Arequipa) | Long term (≥ 4 years) |

| Supporting government initiatives and regulations | +0.6% | Brazil (ANVISA clean-label guidance), Argentina (agroindustrial zones), Chile (CORFO grants) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and clean-label ingredients

In South America, consumer scrutiny of ingredient lists has intensified. A 2024 survey by the Brazilian Association of Food Industries (ABIA) revealed that 68% of Brazilian shoppers actively avoid artificial colors and preservatives[1]Source: Brazilian Association of Food Industries, “Consumer Preferences Survey 2024,” abia.org.br. This behavioral shift is compelling multinational food manufacturers to reformulate legacy SKUs. They're now turning to fruit and vegetable concentrates, purees, and powders, which provide color, flavor, and nutritional value without synthetic additives. The clean-label trend is especially evident in the dairy and confectionery segments. Here, brands are substituting artificial strawberry and orange flavors with real fruit purees, aligning with retailer demands for simpler ingredient lists. In 2024, Chile's Ministry of Health broadened its front-of-pack warning label system to encompass artificial additives. This move amplifies regulatory pressure, hastening the shift towards natural ingredients. Ingredient suppliers, in response, are channeling investments into cold-press and enzyme-assisted extraction technologies. These methods safeguard volatile flavor compounds and anthocyanins, allowing formulators to match the sensory qualities of synthetic alternatives, albeit at a 10-15% cost premium.

Expansion of the food processing industry

In 2024, Brazil's food processing sector raked in USD 233 billion, buoyed by agribusiness exports hitting record highs. As the Real weakened against the dollar, Brazilian concentrates and purees gained a competitive edge in global markets, as highlighted by the USDA Foreign Agricultural Service[2]Source: USDA Foreign Agricultural Service, “Brazil Food Processing Annual 2024,” fas.usda.gov. The sector is now expanding into Paraná and Santa Catarina states, establishing new processing parks alongside citrus and tropical fruit orchards. This strategic move aims to cut logistics costs and capitalize on harvest-season volumes. Meanwhile, in Argentina, the government unveiled the "Plan Agroindustrial 2030" in 2024. This initiative provides tax holidays and subsidized credit lines to processors in underutilized agricultural zones, especially those adopting spray-drying or freeze-drying technologies to tackle the post-harvest losses of over 25% historically seen in perishable fruits and vegetables. Additionally, the Mercosur-EU trade agreement's removal of tariffs on processed ingredients has spurred a flurry of greenfield investments. Multinational corporations and regional cooperatives are in a race, eager to secure duty-free access to European beverage and dairy manufacturers. These manufacturers, sourcing over EUR 2 billion worth of fruit and vegetable ingredients annually, stand to benefit significantly from the agreement.

Shift towards plant-based diets

In 2024, Brazil's plant-based food sales hit USD 1.13 billion, marking a robust 38.1% year-over-year growth, driven by the rising popularity of flexitarian diets among urban millennials and Gen Z, as reported by the Good Food Institute Brazil[3]Source: Good Food Institute, “Plant-Based Foods in Brazil 2024,” gfi.org. This dietary shift is fueling a demand for vegetable-based ingredients that offer functional benefits beyond mere nutrition. For instance, beetroot powder is being sought after for its natural nitrate content in sports nutrition, while carrot concentrate is prized for beta-carotene fortification in plant-based dairy alternatives. In Chile, 2024 consumer profiling data showed a notable rise in flexitarian identification among Santiago residents, jumping to 42% from 28% in 2022. This demographic evolution is prompting shifts in ingredient procurement strategies for both local and multinational food manufacturers. Vegetable ingredients are increasingly infiltrating domains once reserved for animal-derived components. For example, pumpkin puree is now a go-to for replacing egg yolks in vegan mayonnaise, and tomato paste is being utilized as a foundational element in plant-based cheese analogs. Such transitions are propelling a forecasted 6.90% CAGR for vegetable ingredients, as formulators increasingly pursue clean-label, allergen-free solutions that resonate with health and sustainability narratives.

Product innovation and diversification

Ingredient manufacturers are moving beyond traditional commodity concentrates, venturing into value-added formats. These include encapsulated powders, freeze-dried pieces, and enzyme-modified purees, all designed to enhance functionality for targeted applications. A prime example of this trend is Cargill's 2024 debut of a microencapsulated acai powder line in Brazil. This innovation offers beverage formulators a shelf-stable ingredient, boasting anthocyanin retention levels exceeding 85% after 18 months at room temperature. In contrast, conventional spray-dried powders only manage a 40-50% retention. In 2024, Kerry Group rolled out a selection of organic mango and passion-fruit purees in Chile. These purees cater to premium yogurt and ice cream producers, who are ready to shell out a 20-25% premium for ingredients that are non-GMO and fair-trade certified. The innovation pipeline is also tackling texture and mouthfeel issues in plant-based products. Suppliers are crafting vegetable-fiber blends that replicate the viscosity and suspension qualities of dairy proteins, making them ideal for smoothies and meal-replacement drinks. Furthermore, patent filings for processing technologies related to fruit and vegetable ingredients surged by 34% in South America from 2023 to 2024. This uptick underscores a growing competitive landscape in research and development, as suppliers vie for a foothold in the lucrative specialty segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from synthetic and artificial alternatives | -0.5% | Brazil, Argentina, Colombia; price-sensitive segments | Short term (≤ 2 years) |

| Raw-material price volatility | -0.4% | Brazil (citrus, tropical fruits), Argentina (apples, pumpkins), Chile (berries) | Short term (≤ 2 years) |

| Stringent multi-country food-safety and labeling rules | -0.3% | Cross-border trade within Mercosur and exports to the EU, North America | Medium term (2-4 years) |

| Limited processing technology and expertise | -0.3% | Peru, Colombia, and smaller processors in Argentina and Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from synthetic and artificial alternatives

On a per-unit basis, synthetic flavors and colors are consistently cheaper than their natural fruit and vegetable counterparts. This price advantage exerts ongoing pressure in cost-sensitive sectors, notably carbonated soft drinks and hard candies. Major multinational flavor companies are channeling investments into nature-identical compounds. These compounds mimic the sensory profiles of genuine fruits, thanks to recent breakthroughs in fermentation-derived vanillin and enzymatically produced esters, achieving this at a significantly reduced cost. In Argentina and Colombia, the economic volatility and currency depreciation are so pronounced that mid-tier food manufacturers are compelled to prioritize ingredient costs, often at the expense of clean-label aspirations. South America's regulatory framework still endorses a broad spectrum of synthetic additives, many of which have been banned in Europe and North America. This leniency diminishes the urgency for reformulation, enabling legacy products to retain their market presence. In response to these dynamics, ingredient suppliers are innovating hybrid solutions. By merging minimal quantities of natural fruit or vegetable extracts with sanctioned synthetic components, they can market their products as "natural flavor with other natural flavors," commanding a premium over entirely synthetic options.

Raw-material price volatility

In 2024, weather disruptions driven by El Niño led to a 22% drop in Brazilian orange yields and an 18% decline in Argentine apple harvests. These reductions spurred price spikes in concentrates, squeezing margins for beverage and dairy producers, as reported by the USDA Foreign Agricultural Service. Climate models indicate that South America's primary fruit and vegetable regions will face more frequent extreme precipitation and drought events, suggesting this volatility is structural, not cyclical. In response, ingredient buyers are diversifying their sourcing across various geographies and committing to long-term contracts with cooperatives. However, these strategies come with heightened working capital demands and diminished procurement flexibility. Smaller processors, lacking the scale to hedge against commodity fluctuations via futures or multi-year agreements, find themselves at the mercy of spot-market price fluctuations, jeopardizing their operating margins during tight supply scenarios. Moreover, the limited development of crop insurance markets in Peru and Colombia intensifies this vulnerability. Growers, shouldering the full brunt of weather-induced financial losses, risk exiting production entirely after a series of poor harvests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Vegetables Gain Ground in Fortification Plays

Forecasts indicate that from 2026 to 2031, the vegetable market will grow at a CAGR of 6.62%. This growth is set to outpace the 50.12% market share fruits held in 2025. Formulators are increasingly prioritizing functional ingredients, seeking nutritional benefits that extend beyond mere sweetness and flavor. Carrots and beetroots are carving out a niche in sports nutrition and plant-based dairy. Their inherent nitrate and beta-carotene content allows for clean-label fortification claims, eliminating the need for synthetic vitamins. Tomato-based components are making inroads into the savory snack and ready-to-eat meal markets. Formats like paste and powder are now preferred over MSG and hydrolyzed vegetable protein, catering to a consumer demand for familiar ingredient names. Meanwhile, pumpkin puree is gaining traction as a foundational ingredient in plant-based sauces and bakery fillings. Its ability to retain moisture and provide natural sweetness diminishes the necessity for added sugars and emulsifiers.

Fruits continue to dominate the ingredient landscape, firmly establishing their presence in beverages and confections. Oranges, apples, and pineapples lead the charge, making up the bulk of concentrate and puree volumes. Berries, on the other hand, are fetching premium prices in yogurt and ice cream. Their anthocyanin content not only imparts vibrant colors but also bolsters antioxidant marketing claims, appealing to health-conscious consumers. Ingredients derived from mangoes and bananas are becoming increasingly popular in smoothies and meal-replacement products. Their creamy texture and tropical flavor adeptly mask the off-notes often associated with plant-based proteins. This industry's pivot towards vegetables underscores a growing acknowledgment: functional benefits and nutritional fortification are now on par with sensory attributes in ingredient selection. This shift is particularly pronounced as regulators in Brazil and Chile impose stricter limits on added sugars in packaged foods.

By Form: Powders Surge on Logistics and Shelf-Life Advantages

Spray-dried and freeze-dried powders are set to grow at a 7.45% CAGR through 2031, challenging the 37.75% share that concentrates commanded in 2025. Ingredient buyers are increasingly prioritizing formats that cut cold-chain costs and extend shelf life beyond 24 months. Powders offer modular formulation strategies, enabling beverage and dairy manufacturers to tweak flavor intensity and color depth by adjusting dosage rates, all without the need to reformulate entire production batches. Freeze-dried fruit pieces are making inroads into breakfast cereal and snack bar segments. Their crunchy texture and intense flavor deliver a premium sensory experience, justifying a 25-30% higher retail price compared to products with conventional dried fruit. Encapsulated powders are becoming popular in functional beverages, as microencapsulation shields volatile flavor compounds and bioactive nutrients from degradation during thermal processing and storage.

Concentrates dominate the form-segment share, thanks to their deep-rooted role in juice and nectar production. Their liquid format integrates effortlessly into existing processing lines, eliminating the need for extra rehydration or dispersion equipment. Pastes and purees maintain their foothold in bakery and confectionery, where their viscosity and water-binding traits enhance texture and moisture retention. Pieces and slices are gaining traction in premium yogurt and ready-to-eat meals, with visible fruit and vegetable inclusions signaling quality and authenticity to consumers. The powder segment's rapid growth highlights a shift in supply-chain economics. Ingredient buyers are keen to reduce refrigerated transport and warehousing costs, which can make up 15-20% of the total landed cost for liquid concentrates traversing South America's vast distances. Döhler's 2024 investment in a spray-drying facility in Brazil's Minas Gerais state underscores this trend. The plant is set to transform fresh fruit purees into shelf-stable powders, ready for export to North American and European markets, all without the need for cold-chain logistics.

By Application: Dairy Products Accelerate on Premiumization and Flavor Innovation

From 2026 to 2031, dairy products are projected to grow at a 6.72% CAGR, closing the gap with beverages. In 2025, beverages commanded a 38.55% share of the market, as yogurt and cheese producers increasingly turn to fruit and vegetable ingredients to set their products apart in crowded retail spaces. In Brazil, Greek yogurt makers are blending in exotic fruit purees like açaí, passion fruit, and guava. This strategy not only justifies a premium price that's 40-50% higher than standard varieties but also taps into consumers' readiness to invest in unique flavors and the associated health benefits. The rising popularity of plant-based dairy alternatives is fueling a demand for vegetable ingredients. These ingredients not only enhance color but also boost nutritional value. For instance, carrot and beetroot powders are now being used in almond and oat milk formulations, replacing synthetic beta-carotene and iron supplements. In Argentina, ice cream producers are unveiling limited-edition flavors, spotlighting regional fruits like calafate and murta. By emphasizing local sourcing and sustainability, they're vying for market share against global brands.

Beverages dominate the application landscape, heavily relying on fruit concentrates and purees for both flavor and color, especially in juice, nectar, and carbonated soft drink categories. As urbanization rises and more households enjoy dual incomes, there's a growing appetite for ready-to-eat products. Vegetable ingredients are stepping up, forming the backbone of soups, sauces, and meal kits, all designed to deliver that cherished home-cooked taste with minimal prep. While the confectionery and bakery sectors remain steady, utilizing fruit pastes and purees for moisture, sweetness, and natural coloring in items like gummies, jellies, cakes, and pastries, soups and sauces are carving out a niche. Here, tomato paste and vegetable concentrates are taking center stage, replacing artificial enhancers and thickeners in a move towards cleaner labels. The dairy segment's rapid ascent highlights a key trend: ingredient suppliers offering tailored flavor systems and application support are reaping the rewards in high-margin categories. In contrast, vendors of commodity concentrates are feeling the pinch, facing tighter margins in established beverage markets.

Geography Analysis

In 2025, Brazil secured a dominant 41.20% share of the global citrus processing market. Notably, São Paulo state contributed over 70% of the world's orange juice concentrate exports, serving as a vital supply hub for local beverage and dairy producers. Brazil's food processing sector, boasting revenues of USD 233 billion in 2024, thrived on vertically integrated supply chains. These chains seamlessly connected fruit and vegetable growers to ingredient processors, facilitated by cooperative structures and contract farming. In 2024, Brazil's ANVISA expedited approvals for clean-label ingredients, shortening regulatory timelines. This move allowed manufacturers to swiftly launch products reformulated with natural fruit and vegetable extracts. Throughout 2024, the Real's decline against the dollar bolstered Brazil's export appeal. Consequently, Brazilian mango and pineapple concentrates made significant inroads into North American and European markets, outpacing Asian competitors.

Argentina is projected to lead major South American markets with a robust 7.52% CAGR through 2031. This growth is fueled by a devalued peso, making its apple, pumpkin, and tomato ingredients highly sought after in export markets. Additionally, government incentives for agroindustrial processing zones in Mendoza and Río Negro provinces play a pivotal role. Under the "Plan Agroindustrial 2030", processors installing spray-drying or freeze-drying capacities benefit from tax holidays and subsidized credit. This initiative aims to curtail post-harvest losses, historically exceeding 25% for perishables. In 2024, Argentina's apple concentrate exports surged 34% in volume, overtaking Chinese suppliers in European beverage formulations. Buyers, aiming to diversify sourcing and mitigate geopolitical risks, turned to Argentina. Furthermore, the Mercosur-EU trade agreement's tariff eliminations have been a boon for Argentine exporters. They now tap into the EUR 400 billion European food market without facing the previous 8-12% duties that hampered price competitiveness.

While Chile held a modest market share in 2024, it's strategically positioning itself in premium segments through counter-seasonal berry production and bio-economy initiatives. With a USD 45 million boost from CORFO, Chilean processors are valorizing agroindustrial residues. This investment allows them to derive high-value compounds from fruit and vegetable by-products, leading to sustainability-certified ingredients. These premium ingredients fetch a 15-20% price advantage in North America's natural-foods market. Meanwhile, Peru's freeze-dried tropical fruits are making waves in export markets. This momentum is bolstered by CONCYTEC's USD 12 million grant program, which supports pilot-scale production facilities. These facilities are eyeing North American and Asian markets, where buyers are willing to pay a premium for enhanced flavor profiles. Colombia, alongside the rest of South America, may represent a smaller market, but it's on the rise. Urbanization and increasing disposable incomes are fueling a demand for processed foods enriched with fruit and vegetable ingredients, enhancing flavor, color, and nutritional value.

Competitive Landscape

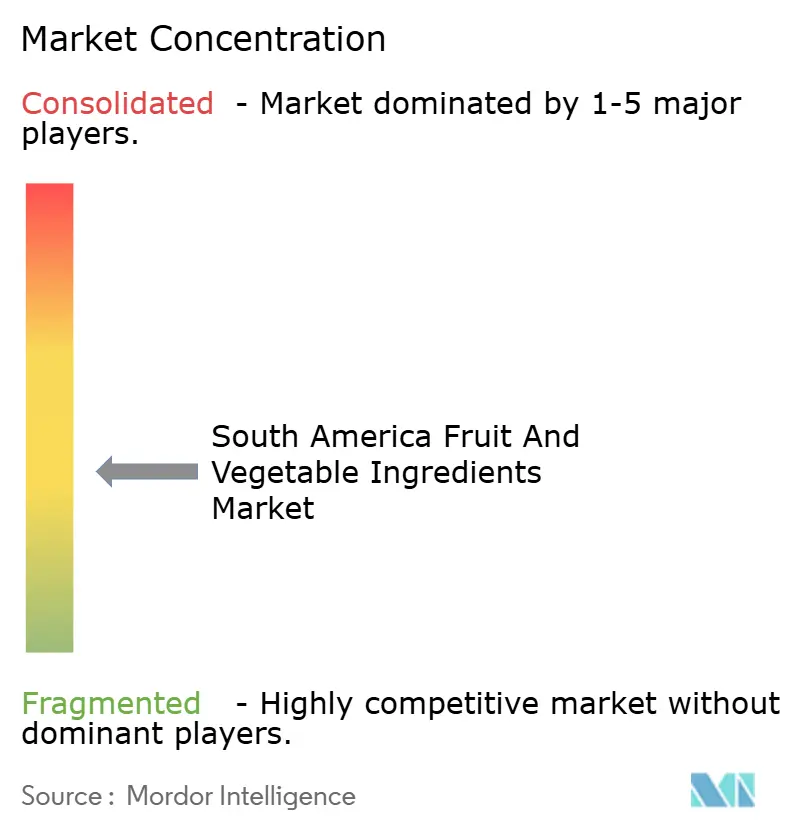

In South America, multinational ingredient houses like Archer Daniels Midland, Cargill, and Kerry Group dominate the fruit and vegetable ingredients market. They achieve this through vertically integrated supply chains and toll-processing agreements with local cooperatives. These global giants leverage their scale advantages in procurement, processing technology, and distribution to ensure consistent quality and year-round availability, which are critical for multinational food manufacturers operating across the region. Meanwhile, regional specialists such as SVZ Industrial Fruit and Vegetable Ingredients, Paradise Fruits, and Taura Natural Ingredients are carving out niches by offering organic-certified, non-GMO, and fair-trade ingredient lines. These products command premium prices in North American and European natural-foods channels. Additionally, functional vegetable ingredients for plant-based dairy and meat alternatives present emerging opportunities, where established fruit-concentrate suppliers lack application expertise and formulation support capabilities.

Technology is becoming a pivotal competitive edge in the market. Leading players are investing in enzyme-assisted extraction, microencapsulation, and freeze-drying technologies, which preserve bioactive compounds and volatile flavor molecules at higher retention rates compared to traditional spray-drying. For instance, Cargill's 2024 patent filing for a cold-press extraction method ensures anthocyanin levels in berry concentrates remain above 90%. This innovation positions Cargill to target premium yogurt and ice cream markets, where color stability commands higher margins. However, smaller processors face challenges in adopting these advanced technologies due to capital constraints and limited technical expertise. This has resulted in a bifurcated market, where larger players dominate high-margin specialty segments, while regional suppliers compete on price in the commodity concentrate categories.

The Mercosur-EU trade agreement is further intensifying competitive dynamics in the market. Tariff eliminations now allow European ingredient manufacturers to export duty-free into South America, while local producers gain preferential access to European markets. This dual advantage is compressing margins for mid-tier players, who are caught between low-cost commodity suppliers and technology-leading multinationals. As a result, the market landscape is becoming increasingly challenging for mid-sized companies, forcing them to adapt to the evolving competitive pressures or risk losing market share.

South America Fruit And Vegetable Ingredients Industry Leaders

Cargill Incorporated

Sensient Technologies

Dohler Group

Archer Daniels Midland

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Cargill announced a USD 85 million expansion of its citrus processing facility in Araraquara, Brazil, adding spray-drying capacity to convert fresh orange juice into shelf-stable powder for export to North American beverage manufacturers. The investment includes enzyme-assisted extraction technology designed to preserve vitamin C and volatile flavor compounds at retention rates exceeding 85% after 18 months of ambient storage, positioning Cargill to capture premium pricing in functional beverage applications.

- August 2024: Kerry Group partnered with Chilean fruit cooperative Copefrut to develop organic-certified mango and passion-fruit purees for premium yogurt and ice cream manufacturers in North America and Europe. The partnership includes a USD 12 million investment in cold-press extraction equipment at Copefrut's Maule region facility, enabling production of non-GMO, fair-trade ingredients that meet EU organic standards and command 20-25% price premiums over conventional purees.

- July 2024: Archer Daniels Midland acquired a 60% stake in Argentine vegetable processor Agroindustrias del Sur for an undisclosed sum, gaining access to pumpkin and carrot concentrate production capacity in Mendoza province. The acquisition strengthens ADM's position in plant-based dairy and meat alternative applications, where vegetable ingredients provide color, nutritional fortification, and functional properties that align with clean-label positioning.

South America Fruit And Vegetable Ingredients Market Report Scope

The fruit and vegetable ingredient market in South America is segmented by ingredient type, product, application, and geography. Based on ingredients the market is segmented into fruit and vegetables. Based on product the market is segmented into concentrates, pastes and purees, pieces and powders, and NFC Juices. Based on application the market is segmented into beverages, confectionery products, bakery products, soups and sauces, dairy products, and RTE products. Based on geography the study provides an analysis of the fruit & vegetable ingredients market in Brazil, Argentina, Colombia, and the Rest of South America.

Ingredient Type

| Fruits | Apple |

| Orange | |

| Pineapple | |

| Mango | |

| Banana | |

| Berries | |

| Other Fruits | |

| Vegetables | Carrots |

| Beetroots | |

| Tomato | |

| Pumpkins | |

| Other Vegetables |

Form

| Concentrates |

| Pastes and Purees |

| Pieces and Slices |

| Powders |

| Others |

Application

| Beverages |

| Confectionery Products |

| Bakery Products |

| Soups and Sauces |

| Dairy Products |

| RTE Products |

| Others |

Geography

| Brazil |

| Argentina |

| Colombia |

| Peru |

| Chile |

| Rest of South America |

| Ingredient Type | Fruits | Apple |

| Orange | ||

| Pineapple | ||

| Mango | ||

| Banana | ||

| Berries | ||

| Other Fruits | ||

| Vegetables | Carrots | |

| Beetroots | ||

| Tomato | ||

| Pumpkins | ||

| Other Vegetables | ||

| Form | Concentrates | |

| Pastes and Purees | ||

| Pieces and Slices | ||

| Powders | ||

| Others | ||

| Application | Beverages | |

| Confectionery Products | ||

| Bakery Products | ||

| Soups and Sauces | ||

| Dairy Products | ||

| RTE Products | ||

| Others | ||

| Geography | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which country leads the regional demand for fruit and vegetable ingredients?

Brazil leads with 41.20% revenue share owing to its scale in citrus processing and vertically integrated supply chains.

Which ingredient form is expanding fastest in South America?

Powders are projected to post a 7.45% CAGR through 2031 because they reduce cold-chain costs and offer extended shelf life.

Why are vegetable ingredients gaining popularity?

Vegetable powders and purees offer natural fortification with nitrates, beta-carotene, and fiber, aligning with plant-based diet trends and clean-label requirements.

How will the Mercosur-EU trade deal affect regional suppliers?

The agreement eliminates tariffs, enabling South American processors to access a EUR 400 billion European food market duty-free while facing tougher competition at home.

What are the key challenges facing ingredient manufacturers?

Weather-driven raw-material volatility, competing synthetic flavors that are 30-40% cheaper, and fragmented food-safety rules across Brazil, Argentina, and Chile remain top hurdles.

Page last updated on: