South America Polyether Ether Ketone (PEEK) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

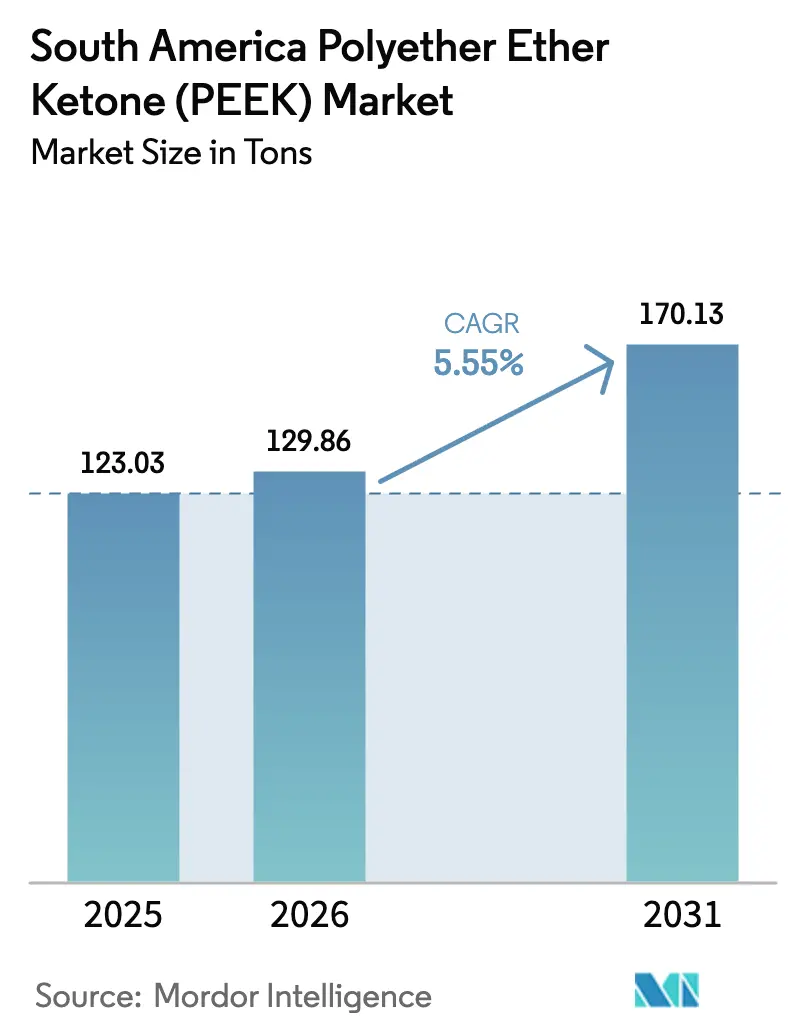

| Base Year Market Size (2025) | 123.03 tons |

| Market Volume (2026) | 129.86 tons |

| Market Volume (2031) | 170.13 tons |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Polyether Ether Ketone (PEEK) Market Analysis by Mordor Intelligence

The South America Polyether Ether Ketone (PEEK) market size is expected to grow from 123.03 tons in 2025 to 129.86 tons in 2026 and is forecast to reach 170.13 tons by 2031 at 5.55% CAGR over 2026-2031. The combination of rising lightweighting mandates in the mobility sector, stricter safety regulations in aerospace cabins, and rapid advancements in medical-device engineering is driving the transition from metals and standard engineering plastics toward high-performance PEEK across the region. Demand has been steadily re-shaped by local content rules in Brazil’s automotive and offshore oil sectors, which encourage substitution of imported metal parts with polymer equivalents that meet endurance and corrosion targets. Currency fluctuations and a 20% import duty on selected polymers, introduced in July 2025, have marginally increased landed costs, but they have also stimulated interest in domestic compounding and additive-manufacturing pathways that shorten lead times. Competitive dynamics remain globally concentrated; however, local distributors leverage exclusive agreements to secure supply, ensure technical support, and mitigate currency-driven price fluctuations for their customers.

Key Report Takeaways

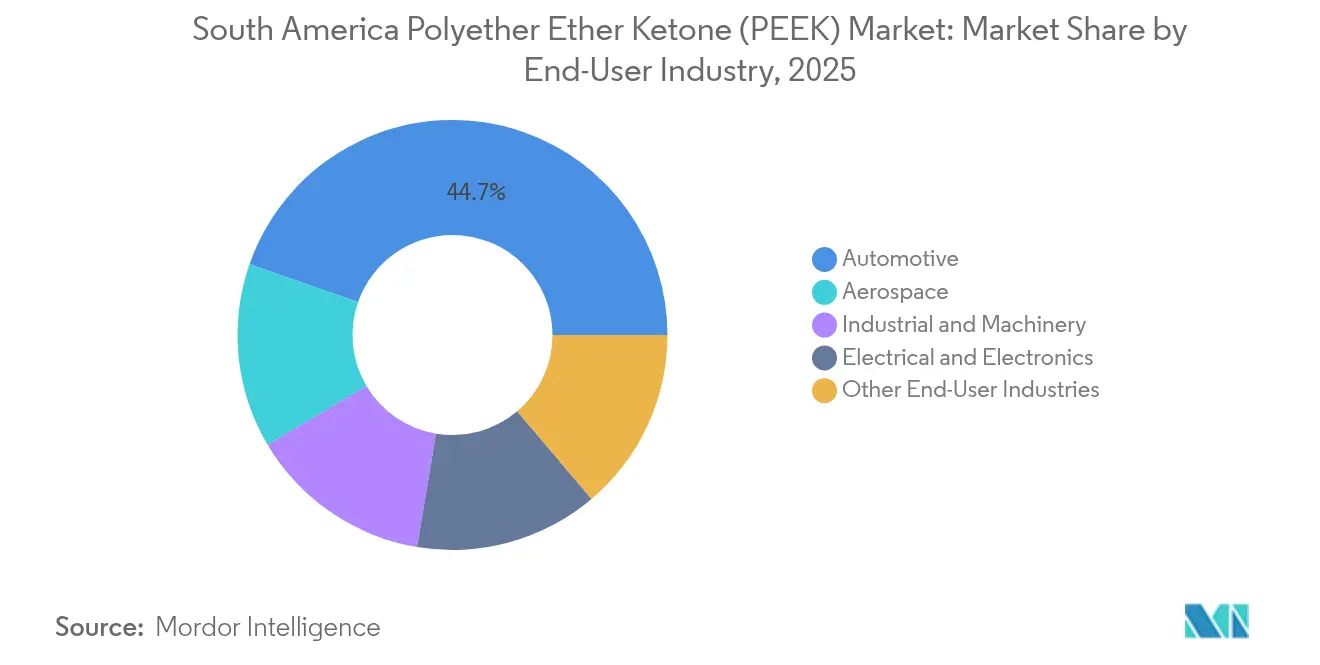

- By end-user industry, automotive led with 44.66% revenue share in 2025; other end-user industries are projected to expand at a 6.23% CAGR through 2031.

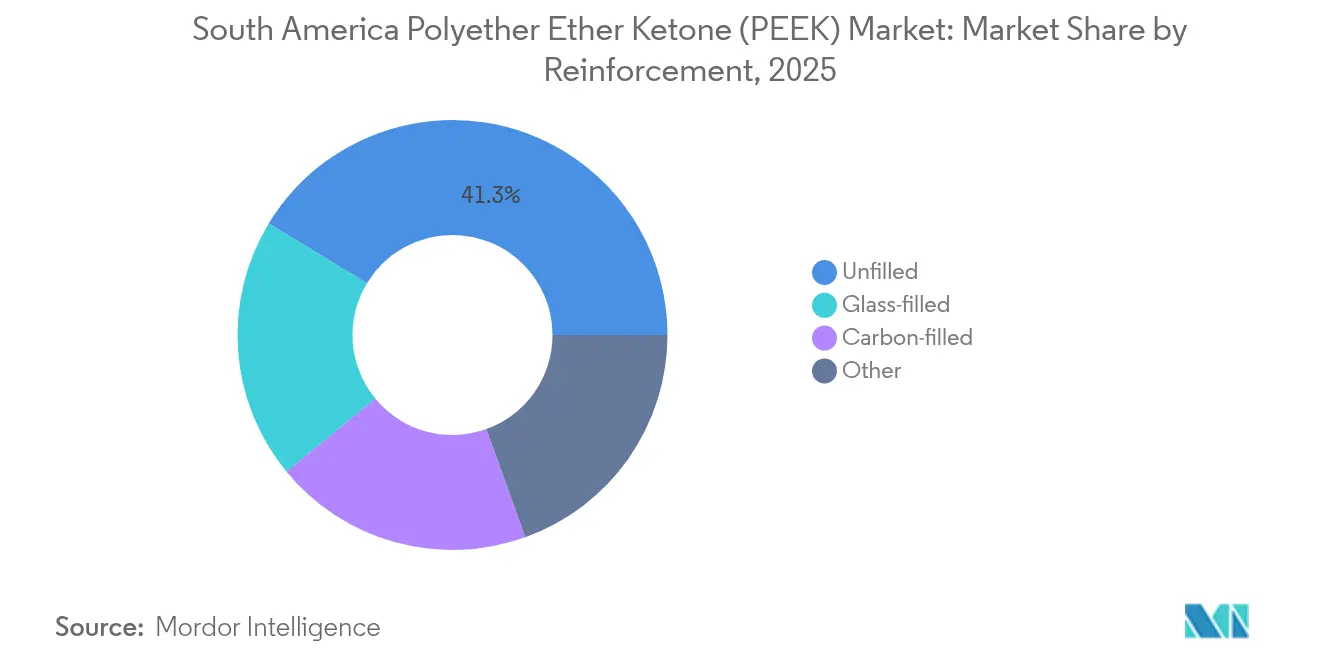

- By reinforcement type, unfilled grades accounted for a 41.32% share of the South America PEEK market size in 2025, while carbon-filled variants are advancing at a 6.78% CAGR to 2031.

- By geography, Brazil held 65.55% of the South America PEEK market share in 2025, whereas Argentina is forecast to record an 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Polyether Ether Ketone (PEEK) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting push in aerospace and automotive | +1.8% | Brazil core, Argentina emerging | Medium term (2-4 years) |

| Rising demand for biocompatible implants | +1.2% | Brazil and Colombia primary markets | Long term (≥ 4 years) |

| Electric-vehicle component localization in Brazil | +1.5% | Brazil concentrated, spillover to Argentina | Short term (≤ 2 years) |

| Rapid medical-device manufacturing growth | +1.0% | Brazil and Colombia focused | Medium term (2-4 years) |

| 3D-printing of PEEK spare parts for offshore oil and gas | +0.9% | Brazil offshore, potential Venezuela | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Push in Aerospace and Automotive

Automakers and aircraft-tier suppliers in Brazil and Argentina pursue aggressive mass-reduction targets, and PEEK components typically offer up to 60% weight savings compared with aluminum while retaining mechanical integrity. Local OEM qualification of transmission gears, battery spacers, and thermofused structural brackets is accelerating because these parts reduce fuel burn or extend electric-vehicle range. Adopters also cite lower interior noise and vibration metrics—an outcome already demonstrated by PEEK gears in global powertrains. Aerospace suppliers serving Embraer and Airbus programs in Brazil increasingly integrate PEEK for cable clamps, seat components, and bleed-air system parts because the polymer meets FAR 25.853 flame requirements without flame-retardant additives. Although supply remains largely import-dependent, regional distributors negotiate volume-based pricing and technical assurance packages that offset cost premiums and smooth logistics.

Rising Demand for Biocompatible Implants

Hospitals in Brazil and Colombia are moving beyond titanium for trauma plates, cranial meshes, and spinal cages because PEEK’s elastic modulus is closer to cortical bone, reducing stress shielding and improving patient outcomes[1]MDPI, “Polyether Ether Ketone for Biomedical Applications,” mdpi.com. The polymer’s radiolucency eases post-surgical imaging, allowing clinicians to monitor bone fusion without artifact distortion. Universities such as UFRJ spearhead surface-modification research that enhances osseointegration through plasma treatments and hydroxyapatite coatings, signaling maturing domestic know-how. Implant manufacturers also value PEEK’s ability to survive up to 3,000 autoclave cycles without mechanical loss, facilitating reusable instrument design that lowers lifecycle costs for cash-strained public health systems. FDA clearance of 3D-printed PEEK cranial implants in 2025 is expected to accelerate ANVISA approvals, broadening reimbursement pathways in the medium term.

Electric-Vehicle Component Localization in Brazil

Brazil’s national reindustrialization plan prioritizes local sourcing for high-voltage EV systems, pushing tier-ones to specify PEEK in e-motor slot liners, busbar insulation, and battery-pack bushings. Victrex APTIV film already enables compact rotor design by combining dielectric strength with thermal conductivity, cutting motor mass and cooling loads. Component suppliers gain tariff exemptions when using Brazilian-made parts, and domestic converters explore thin-film extrusion and injection over-molding lines tailored to PEEK’s 350-400 °C melt profile. The transition to 800 V architectures in premium EVs further heightens material-performance needs, positioning the South America PEEK market as a strategic enabler of next-generation drivetrains.

3D-Printing of PEEK Spare Parts for Offshore Oil and Gas

Petrobras’ LABi3D in Rio hosts Ultra-class printers that fabricate PEEK valves, impeller housings, and sensor clamps on demand, avoiding weeks-long import cycles for niche spares[2]Fabbaloo, “Petrobras Launches Latin America’s Leading 3D Printing Lab,” fabbaloo.com. Early field trials revealed 35% total-cost savings when printed parts replaced corrosion-prone stainless steel in high-CO₂ wells. PEEK’s thermal limit above 250 °C and resistance to supercritical CO₂ align with Brazil’s pre-salt reservoir conditions, while carbon-fiber variants improve creep resistance in dynamic loading. As Venezuela’s upstream rigs restart, operators signal interest in similar distributed-manufacturing hubs, expanding regional appetite for PEEK filament and pellet supplies.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High resin and processing costs vs PPS/PEI | −1.4% | Region-wide, cost-sensitive applications | Short term (≤ 2 years) |

| Scarce local compounding/conversion capacity | −0.8% | Brazil concentrated, Argentina limited | Medium term (2-4 years) |

| Currency-volatility risk on imported monomers | −0.6% | Argentina primary, Brazil secondary | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Resin and Processing Costs vs PPS/PEI

PEEK’s price premium—often 3-5 times that of PPS or PEI—forces value-engineering reviews in cost-sensitive programs. Processing requires molds heated to 170-200 °C and machines capable of 400 °C melt temperatures, inflating capital budgets for converters. Victrex’s 20% volume growth without proportional revenue gains during FY 2024 reveals pricing pressure as buyers benchmark against lower-cost alternatives that meet minimum performance thresholds. Small and mid-sized South American processors report higher reject rates due to PEEK’s tight crystallization window, adding hidden costs that accelerate payback challenges.

Scarce Local Compounding/Conversion Capacity

With no regional monomer plants, PEEK resin imports traverse complex tax filters—ICMS, IPI, PIS/COFINS—before reaching converters. Only a handful of Brazilian firms possess cleanrooms and moisture-controlled storage to produce medical-grade or aerospace-qualified parts. Argentina’s macroeconomic volatility curbs equipment-finance options, limiting adoption to experimental or pilot-scale programs. Consequently, many OEMs still import finished parts, dampening near-term volume potential for the South America PEEK market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Automotive Leads Amid Diversification

The automotive sector captured 44.66% of the South America PEEK market share in 2025, reflecting entrenched demand for lightweight gears, e-motor insulation films, and thermal-management components. Tier-one suppliers in São Paulo integrate PEEK rotor insulators that cut motor mass by 8 kg and boost efficiency, supporting local automakers’ compliance with fleet-average CO₂ rules. The South America PEEK market size for automotive parts is projected to advance at a healthy pace as EV output ramps up, and local content targets encourage substitution of imported magnets and metal housings.

Aerospace uptake remains steadier but commands premium margins, with flame-retardant interior fittings and bleed-air ducts offsetting volume limitations. Electrical and electronics users deploy PEEK in wafer-transport carriers and high-frequency connectors, leveraging the polymer’s 180 °C continuous-use temperature. The “Other End-User Industries” cluster—oil and gas, additive-manufacturing bureaus, and industrial pumps—exhibits the highest volume growth at 6.23% CAGR, driven by Petrobras’ spare-part localization programs and the rising adoption of carbon-fiber reinforced PEEK in subsea equipment. Medical-device demand, although currently small, is expanding at double-digit rates because of implant approvals and the spread of high-temperature FFF printers in clinical engineering labs.

By Reinforcement: Carbon-Filled Drives Innovation

Unfilled grades retained a 41.32% share of the South America PEEK market size in 2025, favored for pumps, bushings, and brackets where pure polymer properties satisfy load criteria at the lowest cost. Glass-filled products address mid-range stiffness needs in electrical enclosures and compressor components, balancing price and performance. Carbon-filled PEEK, however, is propelling innovation; its 6.78% CAGR through 2031 stems from higher tensile modulus and fatigue resistance that suit dynamic aerospace brackets, high-torque gears, and composite pipe shields. Research documenting 82.3% interfacial-strength gains via novel fiber-sizing chemistries underscores the continuing potential for property enhancement.

Marketability of carbon-filled variants also rises with the adoption of large-format additive-manufacturing systems that print 20% CF-PEEK filament into load-bearing implants. These reinforced grades demand precise melt-impregnation control, pushing converters to invest in two-stage screw systems and advanced vacuum-drying protocols. Specialty blends containing PTFE for tribology and conductive fillers for EMI shielding cater to smaller but lucrative niches such as semiconductor etch chambers and radar housings, sustaining higher price points.

Geography Analysis

Brazil anchored 65.55% of PEEK volumes in 2025, leveraging an automotive cluster that consumes motor insulation films, timing-belt teeth, and turbo-charger brackets. Federal offshore exploration concessions further amplify demand for extruded PEEK tubing and 3D-printed spares able to withstand 10,000 psi service pressures. The government’s 20% import duty imposed in July 2025 raised resin costs but simultaneously improved the business case for domestic compounding lines, with at least two investment proposals under fiscal-incentive review.

Argentina’s 7.61% CAGR through 2031 reflects industrial-modernization credits that stimulate aerospace machining and medical-device prototyping clusters in Córdoba and Buenos Aires. Exchange-rate risk remains a hurdle; nevertheless, the South America PEEK market finds growth as Argentine tier-twos adopt PEEK bushings and radar-sensor brackets in satellite and drone platforms destined for export contracts. Collaboration between ANMAT and Brazil’s ANVISA to harmonize implant-approval dossiers is expected to streamline cross-border licensing by 2027.

Rest-of-South-America markets remain niche but strategic. Colombia’s Medellín medical-device corridor manufactures external fixation systems and dental-surgical guides from sterilizable PEEK, capitalizing on proximity to Florida logistics hubs for rapid export. Venezuela’s stepwise oil-sector recovery revives polymer-lined pump barrel projects that had stalled during the downturn, while Chilean mining firms trial PEEK wear plates in copper-concentrate pipelines to cut downtime. Collectively these pockets reinforce the distributed nature of demand addressed by regional distributors who aggregate smaller orders to achieve container-load efficiencies.

Competitive Landscape

Global resin producers retain technological and capacity leadership. Emerging competition arises from additive-manufacturing enablers. 3D Systems, miniFactory, and Roboze partner with oil-field and orthopedic firms to validate design-to-print workflows that bypass conventional injection tooling, lowering minimum-order sizes and accelerating design iterations. Brazilian converters such as Compraco install twin-screw lines capable of carbon-fiber PEEK compounding, promoting regional autonomy. Intellectual-property filings focus on fiber-sizing chemistry and pore-free extrusion die design, indicating process differentiation as a key battleground. Regulatory frameworks exert a moderate influence. Aerospace suppliers must navigate AS9100 audits and material-specification compliance, such as Boeing BMS 8-256 for PEEK sheet. Medical-device producers maintain ISO 10993 biocompatibility test libraries and cleanroom molds to process implant-grade PEEK, giving incumbents with established QMS systems a defensible edge. Market entry for new resin brands from Asia hinges on documented equivalence data and the ability to place technical service personnel in Brazil’s key industrial centers.

South America Polyether Ether Ketone (PEEK) Industry Leaders

Victrex plc

Syensqo

Evonik Industries AG

Ensinger

Pan Jin Zhongrun High Performance Polymer Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Avient Corporation has launched Colorant Chromatics Transcend Biocompatible PEEK pre-colored compounds and colorants at MEDICA 2024, designed specifically for the healthcare industry. These formulations meet the ISO 10993 biocompatibility standards and are ideal for use in injection molding and extrusion processes.

- April 2024: Evonik’s VESTAKEEP i4 3DF PEEK filament was utilized in the first surgeries involving 3D printed spinal implants developed by Curiteva, marking a significant advancement in medical additive manufacturing. This milestone highlights the potential of implant-grade 3D printing materials in personalized spinal treatments.

South America Polyether Ether Ketone (PEEK) Market Report Scope

Aerospace, Automotive, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. Argentina, Brazil are covered as segments by Country.| Aerospace |

| Automotive |

| Electrical and Electronics |

| Industrial and Machinery |

| Other End-User Industries |

| Unfilled |

| Glass-filled |

| Carbon-filled |

| Other |

| Brazil |

| Argentina |

| Rest of South America |

| By End-User Industry | Aerospace |

| Automotive | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Other End-User Industries | |

| By Reinforcement | Unfilled |

| Glass-filled | |

| Carbon-filled | |

| Other | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

Market Definition

- End-user Industry - Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyether ether ketone market.

- Resin - Under the scope of the study, virgin polyether ether ketone resin in primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms