Middle East Polyether Ether Ketone (PEEK) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

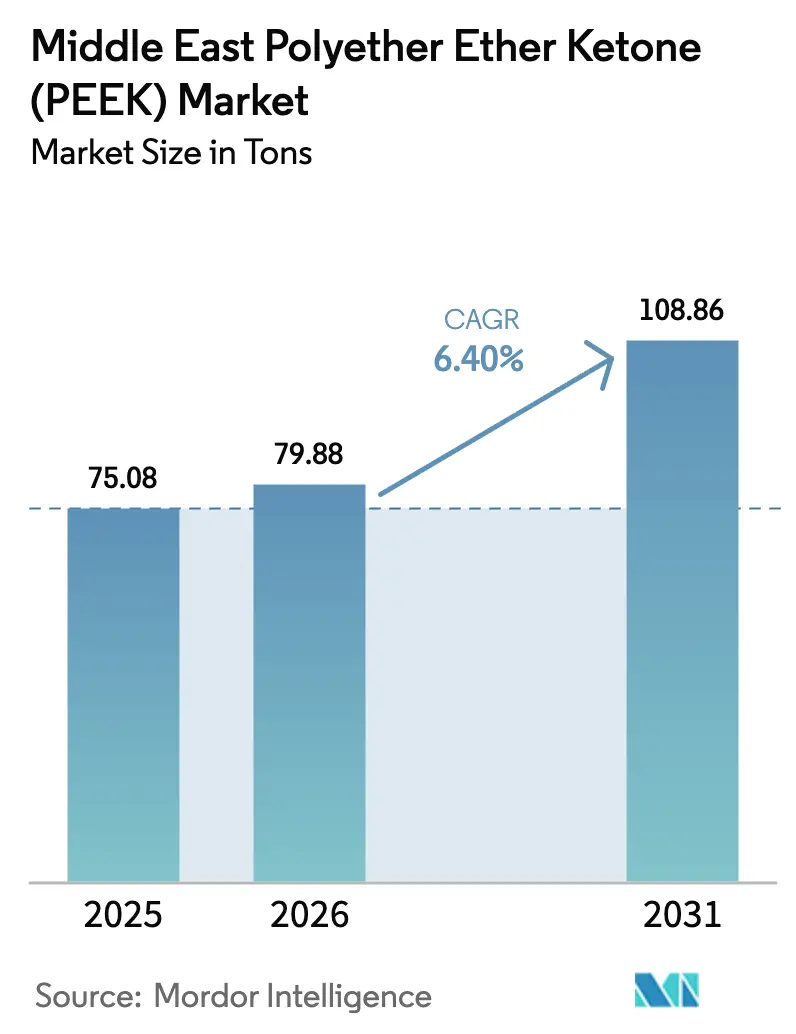

| Base Year Market Size (2025) | 75.08 tons |

| Market Volume (2026) | 79.88 tons |

| Market Volume (2031) | 108.86 tons |

| Growth Rate (2026 - 2031) | 6.40% CAGR |

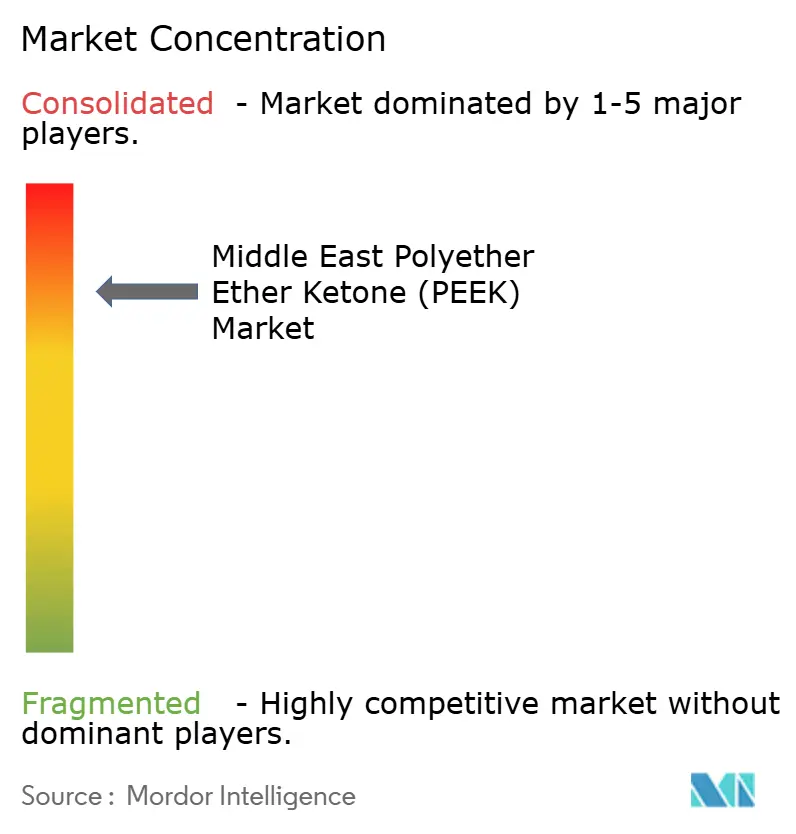

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Polyether Ether Ketone (PEEK) Market Analysis by Mordor Intelligence

The Middle East Polyether Ether Ketone market size is expected to grow from 75.08 tons in 2025 to 79.88 tons in 2026 and is forecast to reach 108.86 tons by 2031 at 6.40% CAGR over 2026-2031. Robust aerospace programs, medical-device manufacturing, and oil-and-gas infrastructure upgrades underpin demand, while national industrial‐diversification agendas in Saudi Arabia and the United Arab Emirates (UAE) amplify the pull for high-performance polymers. Regional suppliers are also starting to add polymerization and compounding lines, reducing lead times and freight exposure for customers who previously relied exclusively on imports. The UAE’s concerted push into additive manufacturing is spurring incremental volumes of specialty grades, whereas Saudi Arabia’s petrochemical majors are leveraging feedstock integration to improve cost competitiveness. Chinese capacity additions are nudging standard-grade prices downward, but localized value-added processing keeps margins resilient.

Key Report Takeaways

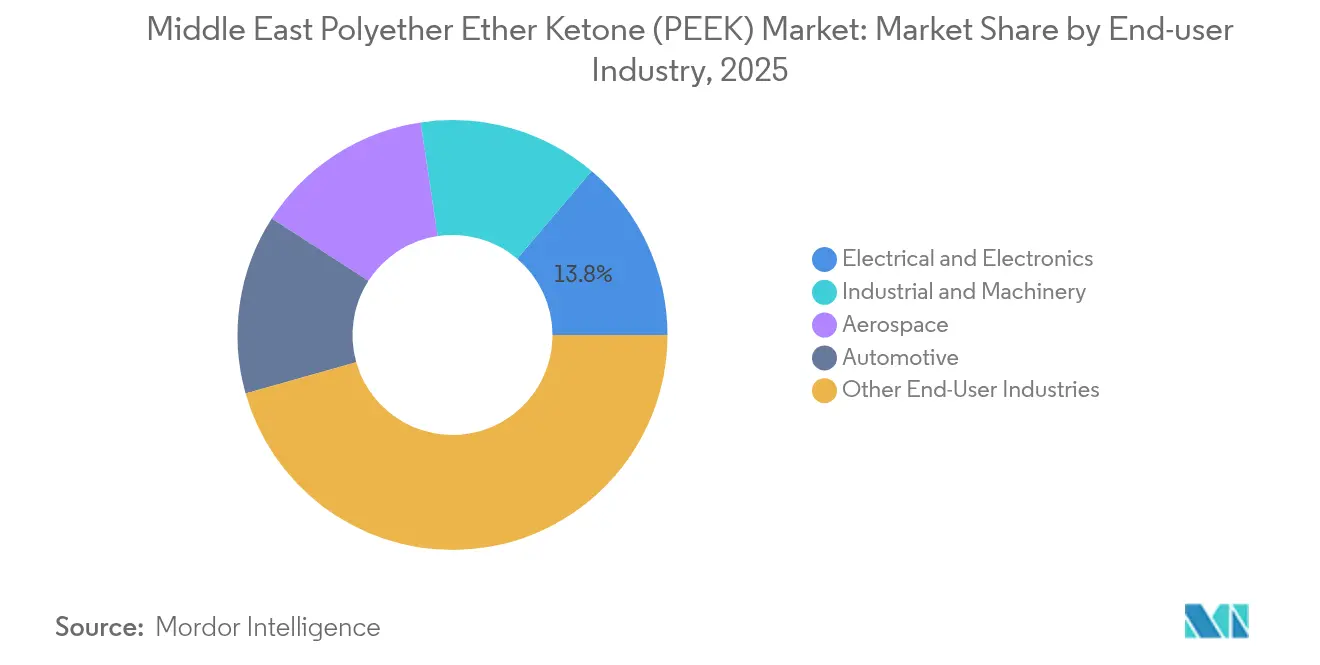

- By end-user, Other End-user Industries commanded 45.62% revenue share in 2025, whereas Electrical and Electronics is advancing at a 7.18% CAGR to 2031.

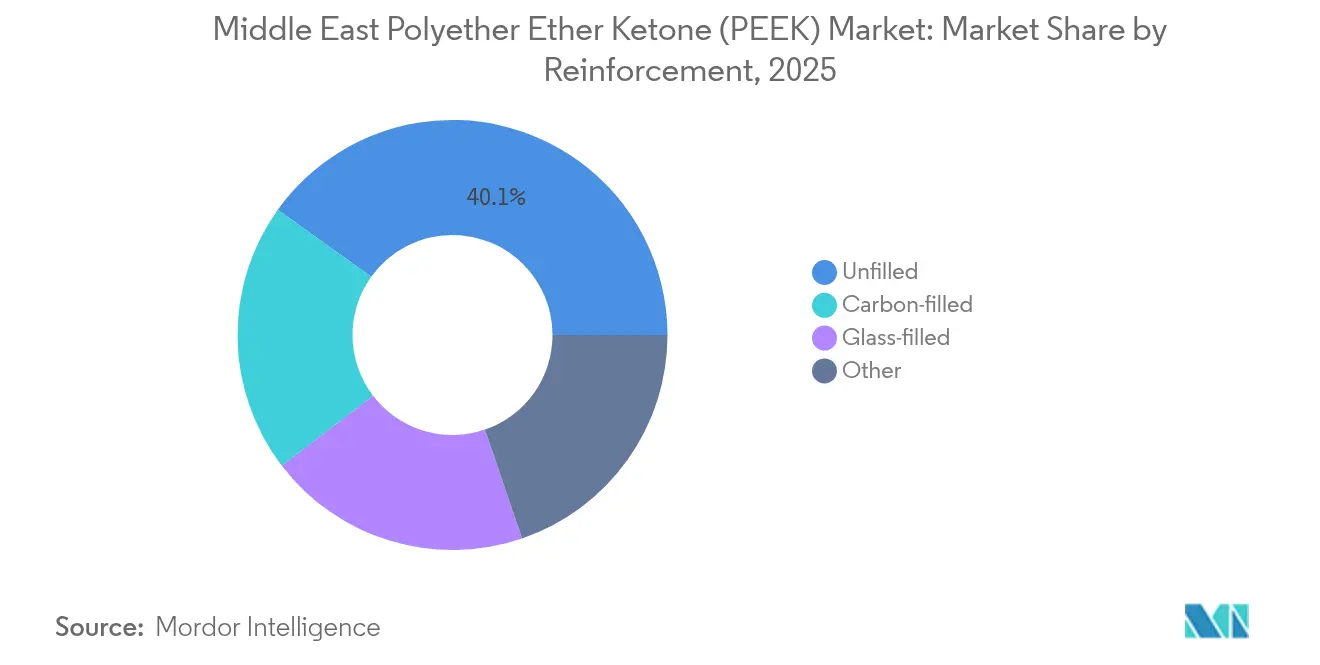

- By reinforcement, unfilled grades captured 40.10 % of the Middle East polyether ether ketone market size in 2025, while carbon-filled variants are set to expand at a 7.21% CAGR through 2031.

- By geography, the Rest of the Middle East held 46.30% of the Middle East polyether ether ketone market share in 2025; the United Arab Emirates is projected to post the fastest 7.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Polyether Ether Ketone (PEEK) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace lightweighting and fuel-efficiency push | +1.8% | UAE core, spillover to Saudi Arabia | Medium term (2-4 years) |

| Rapid adoption of PEEK in spinal and orthopedic implants | +1.2% | GCC countries, with UAE leading | Long term (≥ 4 years) |

| Oil and gas demand for high-temp, chemically-resistant parts | +1.5% | Saudi Arabia dominant | Short term (≤ 2 years) |

| GCC additive-manufacturing programs for specialty polymers | +0.9% | UAE and Saudi Arabia focused | Medium term (2-4 years) |

| Saudi research and development subsidies for high-performance polymer start-ups | +0.7% | Saudi Arabia national | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aerospace Lightweighting and Fuel-Efficiency Push

Dubai’s aerospace cluster has attracted tier-1 suppliers that now machine and print aircraft interior and structural parts from PEEK, shortening lead times for carriers that hub in the region. Local availability of flame-retardant carbon-fiber-reinforced grades enables cabin components that meet FAR 25.853 without post-treatments, trimming assembly cost. Partnerships such as the Roboze-SLB venture in Dammam deliver powder and filament within days rather than weeks, mitigating supply-chain risk for maintenance, repair, and overhaul (MRO) shops[1]Roboze, “Roboze and SLB Partner for Local PEEK Manufacturing in Saudi Arabia,” roboze.com. These efficiencies dovetail with Emirates Airlines’ fleet-expansion roadmap, amplifying pull for advanced thermoplastics. As Airbus and Boeing ramp A321neo and 787 output, regional offset agreements are expected to channel additional work packages to Gulf manufacturing zones, locking in medium-term demand visibility.

Rapid Adoption of PEEK in Spinal and Orthopedic Implants

GCC healthcare spending now tops USD 100 billion annually, and regulators have fast-tracked pathways for Class III implants produced in free-zone factories that meet U.S. Food and Drug Administration (FDA) Quality System Regulation. Patient-matched PEEK interbody cages produced via fused-filament fabrication show bone-like modulus (3-5 GPa) and radiolucency that simplifies post-operative imaging. Local contract manufacturers report order books dominated by degenerative spine and cranio-maxillofacial products, reducing hospital reliance on flown-in implants. Government tenders increasingly stipulate locally produced devices, extending the addressable volume. Over the long term, academic–industry consortia plan to integrate antimicrobial nano-fillers to elevate infection resistance, cementing the material’s foothold in value-based care models.

GCC Additive-Manufacturing Programs for Specialty Polymers

Dubai’s mandate that 25% of new-build components be 3D-printed by 2030 has spurred investment in high-temperature fused-filament systems capable of maintaining 400 °C chamber environments. Research at Khalifa University optimized PEEK extrusion parameters, achieving 0.8 mm feature resolution while lowering porosity by 30%, a milestone that unlocked new tooling applications. Energy savings from microwave sintering—down 25% per tonne—improve the cost profile for low-to-medium volume parts. Pilot projects include on-site printing of desalination-plant impellers and JIG fixtures for aerospace composites, expanding the customer base beyond prototyping to functional production.

Saudi Research and Development Subsidies for High-Performance Polymer Start-Ups

A USD 100 million Aramco-KAUST fund anchors polymer innovation centers that explore catalyst pathways to bring monomer intermediates in-house, potentially shaving 8-10% from PEEK resin cost[2]King Abdulaziz City for Science and Technology, “Advanced Materials Research Program,” kacst.edu.sa . SABIC’s new Riyadh lab targets copolymer recipes that boost impact resistance without compromising crystallinity, eyeing medical-device opportunities. The Saudi Standards, Metrology and Quality Organization’s USD 2.66 billion Standard Incentives Program reimburses up to 50% of pilot-scale equipment purchases, lifting capital barriers for spin-outs. These subsidies deepen the local talent pool and create a pipeline of intellectual property that could displace imports over the long horizon.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High resin cost versus incumbent engineering plastics | –1.4% | Region-wide | Short term (≤ 2 years) |

| Processing complexity (more than or equal to 340 °C melt, specialized tooling) | –0.8% | UAE and Saudi manufacturing centers | Medium term (2-4 years) |

| Competition from PI, PEI and PPS in moderate-temperature uses | –0.6% | GCC, especially diversification projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Processing Complexity (More than or Equal to 340 °C Melt, Specialized Tooling)

Injection-molding PEEK demands barrel temperatures above 340 °C, mold temperatures to 190 °C, and residence-time control to avoid degradation. Capital expenditure for such presses and hot-runner systems can exceed USD 600,000 per line, deterring new entrants. Moisture sensitivity requires 150 °C desiccant drying for 3 hours before molding, stretching production cycles. Skill shortages in crystallinity control and post-annealing further constrain localized supply.

Competition from PI, PEI, and PPS in Moderate-Temperature Uses

In applications below 220 °C, designers often swap to polyimide (PI), polyetherimide (PEI), or polyphenylene sulfide (PPS) at 30-60% lower part cost. Tier-2 automotive suppliers in Turkey thus hesitate to qualify PEEK for under-hood clips or housings where peak temperatures rarely breach 200 °C. Unless PEEK producers unlock tangible weight or durability gains, substitution risk persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Diversification Beyond Traditional Applications

Other End-user Industries held 45.62% of the total market and are projected to edge higher as infrastructure projects specify corrosion-resistant polymers for pumps, valves, and semiconductor-fabrication jigs. Electrical and Electronics demand, though smaller, is on track for a 7.18% CAGR, driven by UAE wafer-foundry projects and hyperscale data-center build-outs that require low-smoke, high-heat plastics for chip handlers and server connectors. Aerospace programs continue to draw volumes for brackets and ducts because metal substitution yields 50-60% weight savings. Automotive deployment lags due to entrenched supply chains, yet luxury-SUV makers in the region started pilot runs for PEEK fuel-system components that withstand 10% ethanol blends.

Industrial buyers increasingly factor lifecycle cost rather than up-front price, valuing PEEK’s chemical inertness and dimensional stability. Petrochemical complexes in Kuwait switched compressor ring carriers to unfilled grades, extending mean-time-between-failures from six to 18 months. Semiconductor cleanrooms adopt PEEK wafer grippers to cut ionic contamination. Compliance with ISO 23153 and USP Class VI widens the accessible medical-device space, and volume tie-ups with local compounders are under negotiation to secure supply for sterilizable surgical tools. Collectively, these developments re-weight the Middle East polyether ether ketone market toward high-value technology verticals.

By Reinforcement: Carbon-Filled Variants Drive Performance Enhancement

Unfilled grades maintained a 40.10% share in 2025, buoyed by biocompatible and purity-critical applications. Carbon-filled PEEK is the fastest-moving sub-segment and is on course to notch a 7.21% CAGR through 2031 thanks to aerospace interiors and structural panels that benefit from a 3-5× increase in modulus over neat polymer. Glass-fiber grades remain a workhorse for compressor seals and machine-tool bearings but face gradual cannibalization where carbon formulations yield longer service life.

Material scientists at Abu Dhabi’s Technology Innovation Institute fine-tuned fiber-orientation during extrusion to boost tensile strength, while continuous-fiber laminates now qualify for cabin-floor assemblies after flame-smoke-toxicity tests. Expansion of filament-winding lines in Saudi industrial cities signals a pivot to composite pipe for sour-gas service. Specialty reinforcements, such as PTFE-filled blends that lower coefficient of friction, gain traction for dynamic seals in regional desalination plants. The evolving reinforcement mix underlines how the Middle East polyether ether ketone market increasingly prizes engineered performance over simple commodity substitution.

Geography Analysis

Rest of Middle East (excluding Saudi Arabia and the UAE) commands 46.30% market share, anchored by Qatar’s gas-processing modules and Oman’s refinery upgrades that consume PEEK for valve seats, compressor vanes, and chemical-resistant gaskets. Cross-border engineering, procurement, and construction (EPC) contracts bundle PEEK components sourced from UAE free zones, demonstrating intra-regional integration. Kuwait’s Integrated Petrochemicals Complex procures rod stock for pump wear rings, sustaining baseline demand, while Bahrain’s aluminum smelter integrates PEEK insulation in pot-line sensors to boost uptime.

The UAE is the fastest-growing geography at a 7.22% CAGR and is central to additive-manufacturing breakthroughs. Dubai South’s aviation ecosystem hosts service bureaus that print flight-certified brackets within 48 hours of CAD release, reducing costly aircraft-on-ground events. Abu Dhabi’s sovereign wealth funds back semiconductor fabs and battery gigafactories that specify PEEK for chemical-process tooling. The country’s “Operation 300bn” industrial strategy earmarks zero-interest loans for high-temperature polymer processors, catalyzing downstream investments.

Saudi Arabia positions itself as an innovation node, leveraging Vision 2030 and its USD 2.66 billion standard-incentive scheme to incubate local polymer intellectual property. The Novel Non-metallics joint venture between Saudi Aramco and Baker Hughes opened a composite-pipe plant that embeds carbon-fiber PEEK liners for downhole service. NEOM’s building code includes high-performance polymers for utility conduits, locking in long-cycle material demand. Over time, localized synthesis aims to trim import reliance and anchor the Middle East polyether ether ketone market within domestic value chains.

Competitive Landscape

The market is consolidated in nature. Global incumbents such as Evonik, Solvay, and Victrex retain process know-how in monomer synthesis and ultra-clean production, giving them a materials-science edge. Their Middle East sales rose on the back of aerospace and medical contracts, but face price tension from Chinese entrants that shipped a record 8,500 tons worldwide in 2025. Regional petrochemical giants, led by SABIC, explore backward integration into diphenyl ether to reduce resin cost and capture margin. Strategic collaborations shape competitive contours. Roboze and SLB’s Saudi facility produces filament and powder catering to localized aerospace and oil-field customers, slashing freight costs and import duties.

Middle East Polyether Ether Ketone (PEEK) Industry Leaders

Evonik Industries AG

Pan Jin Zhongrun High-Performance Polymer Co. Ltd.

SABIC

Syensqo

Victrex plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Roboze partnered with SLB to establish Saudi Arabia’s first PEEK manufacturing plant, supplying aerospace and oil-field customers.

- March 2024: Khalifa University demonstrated sub-millimeter-resolution polyether ether ketone (PEEK) filament printing for industrial tooling.

Middle East Polyether Ether Ketone (PEEK) Market Report Scope

Aerospace, Automotive, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. Saudi Arabia, United Arab Emirates are covered as segments by Country.| Aerospace |

| Automotive |

| Electrical and Electronics |

| Industrial and Machinery |

| Other End-User Industries |

| Unfilled |

| Glass-filled |

| Carbon-filled |

| Other |

| Saudi Arabia |

| United Arab Emirates |

| Rest of Middle East |

| By End-User Industry | Aerospace |

| Automotive | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Other End-User Industries | |

| By Reinforcement | Unfilled |

| Glass-filled | |

| Carbon-filled | |

| Other | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East |

Market Definition

- End-user Industry - Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyether ether ketone market.

- Resin - Under the scope of the study, virgin polyether ether ketone resin in primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms