North America Polyether Ether Ketone (PEEK) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

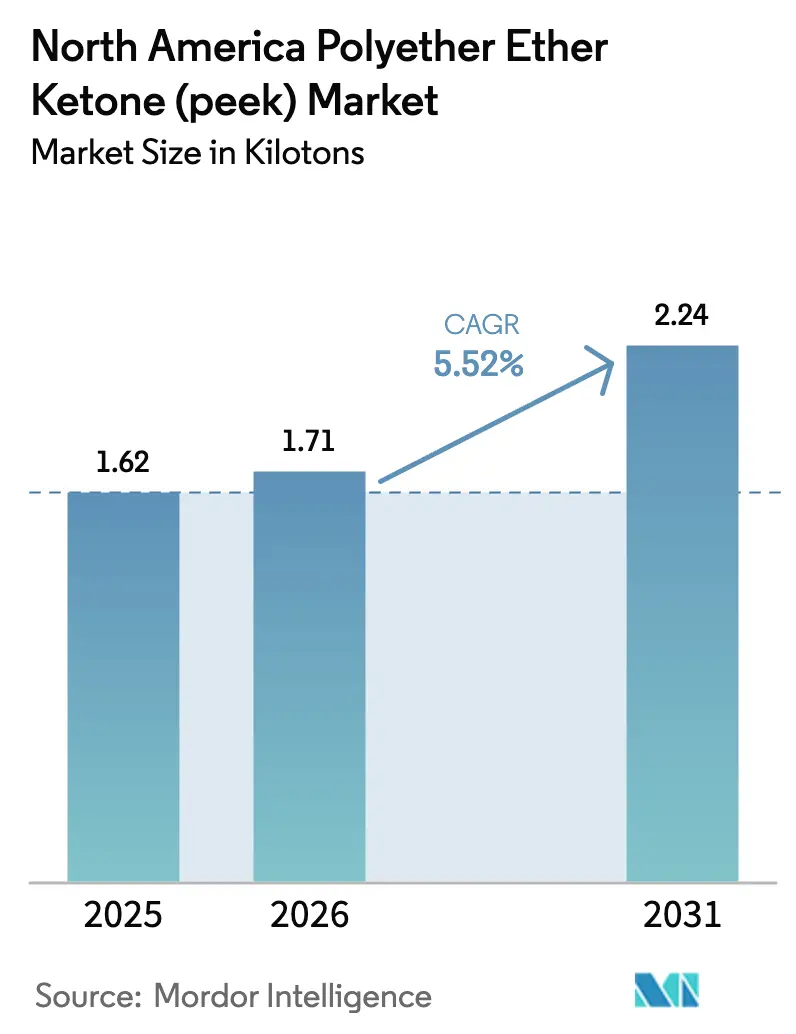

| Base Year Market Size (2025) | 1.62 kilotons |

| Market Volume (2026) | 1.71 kilotons |

| Market Volume (2031) | 2.24 kilotons |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Polyether Ether Ketone (PEEK) Market Analysis by Mordor Intelligence

The North America Polyether Ether Ketone Market size in 2026 is estimated at 1.71 kilotons, growing from 2025 value of 1.62 kilotons with 2031 projections showing 2.24 kilotons, growing at 5.52% CAGR over 2026-2031. This steady expansion mirrors sustained demand for high-performance thermoplastics able to tolerate temperatures above 250 °C, resist aggressive chemicals, and satisfy stringent biocompatibility and flame-retardant requirements. Aerospace lightweighting mandates, FDA-backed implant adoption, and electric-vehicle (EV) thermal challenges collectively support premium pricing while restraining volume growth. Regional supply-chain reshoring incentives under USMCA encourage domestic capacity investments, yet the PEEK market continues to rely on European resin producers for roughly four-fifths of global output. Additive-manufacturing innovations further shift value from tonnage to precision applications, widening the opportunity set for specialty compounders and contract manufacturers.

Key Report Takeaways

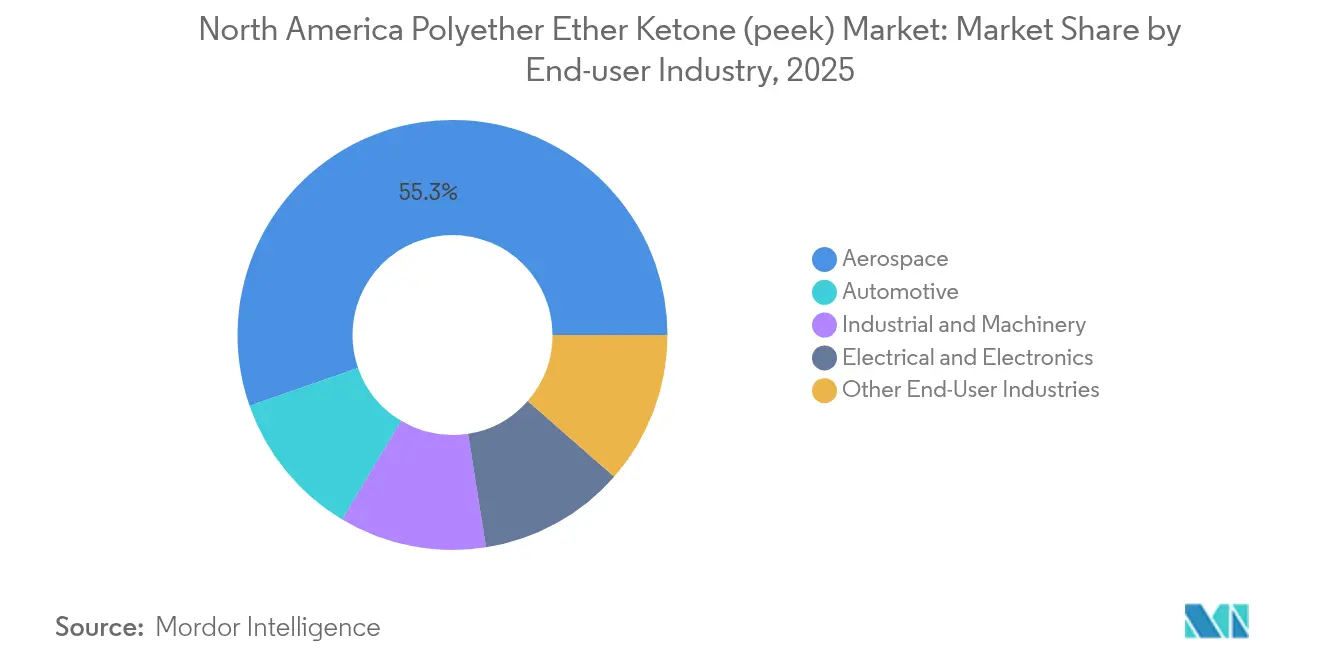

- By end-user industry, aerospace led with 55.34% of PEEK market share in 2025, while “other industries are forecast to expand at a 5.90% CAGR through 2031.

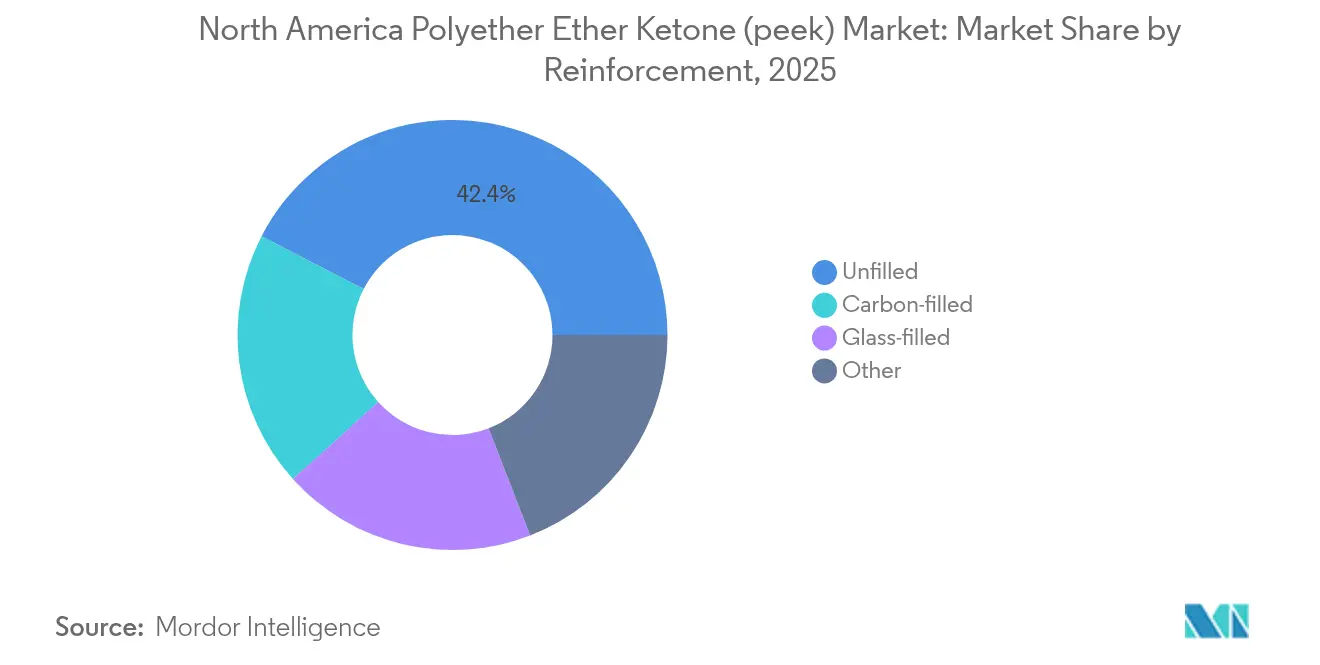

- By reinforcement type, unfilled grades accounted for 42.40% of the PEEK market size in 2025; carbon-filled variants hold the highest growth outlook at a 6.33% CAGR to 2031.

- By geography, the United States controlled 83.55% of PEEK market share in 2025, whereas Mexico is projected to advance at a 7.70% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Polyether Ether Ketone (PEEK) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace lightweighting and FST compliance | +1.8% | United States aerospace hubs | Medium term (2-4 years) |

| Medical-implant biocompatibility demand | +1.2% | United States and Canada | Long term (≥ 4 years) |

| EV high-temperature component adoption | +1.0% | United States and Mexico auto corridors | Medium term (2-4 years) |

| Additive-manufacturing of on-demand spares | +0.9% | Early adoption in North America | Short term (≤ 2 years) |

| USMCA-led regional PEEK supply-chain reshoring | +0.6% | Trilateral trade region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aerospace Lightweighting and FST Compliance

Federal Aviation Administration flame, smoke, and toxicity thresholds align with weight-reduction targets, positioning PEEK as a metal substitute for interior panels, fuel-system components, and wiring harnesses. The resin’s 1.3 g/cm³ density yields 40% weight savings over aluminum without halogenated additives, simplifying certification workflows[1]Federal Aviation Administration, “Advisory Circular 25.853-1B Cabin Interior Flame Resistance,” faa.gov . On-demand printing of spare parts shortens maintenance cycles and minimizes inventory overhead, and sustainable aviation-fuel adoption further elevates demand for chemically resistant tubing and valves. These factors collectively reinforce North American aerospace as the anchor customer for the PEEK market.

Medical-Implant Biocompatibility Demand

A bone-like elastic modulus, inherent radiolucency, and ISO 10993 cytotoxicity compliance support growing use of PEEK in spinal cages, cranial plates, and trauma fixation devices. The 2024 FDA clearance of 3D Systems’ additively manufactured cranial implant demonstrated up to 85% material savings versus machined blanks while enabling patient-specific geometries[2]U.S. Food & Drug Administration, “Recognized Consensus Standards: ASTM F2820-12(2021)e1,” fda.gov. As hospital-based printing centers proliferate, demand for sterilizable, MRI-compatible materials rises, reinforcing long-term consumption growth in the PEEK market.

EV High-Temperature Component Adoption

Next-generation 800-V drivetrains require insulation capable of continuous service above 200 °C. PEEK delivers high dielectric strength and chemical resistance, allowing thinner wall sections that reduce mass and extend battery range. Mexico’s cost-competitive assembly plants integrate PEEK-based stator end-caps, coolant manifolds, and charging connectors, amplifying regional volume growth under USMCA origin rules.

Additive-Manufacturing of On-Demand Spares

Advances in laser-sintered powders and high-temperature FFF filaments shorten lead times for legacy components with complex geometries. Aerospace and semiconductor fabs report double-digit reductions in total cost of ownership when switching to localized printing of PEEK parts, despite higher per-kilogram resin pricing. Recent grades with 25% higher impact strength expand suitability for dynamic load cases, accelerating adoption across industrial maintenance operations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High raw-material and processing cost | -1.4% | Globally, amplified in North America | Medium term (2-4 years) |

| Limited processor base and tooling complexity | -0.8% | North America | Long term (≥ 4 years) |

| Volatile difluoro-benzophenone precursor supply | -0.6% | China-centric supply chain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Processor Base and Tooling Complexity

Injection-molding and extrusion of PEEK demand nickel-based alloys, hot-runner gates, and mold temperatures above 180 °C, limiting participation to a handful of experienced North American processors. Capacity constraints inflate lead times during demand spikes, while aerospace and medical quality-management certification erects additional entry barriers.

Volatile Difluoro-Benzophenone Precursor Supply

Chinese producers dominate global output of this niche intermediate, and sporadic environmental shutdowns have triggered spot price swings of ±30% since 2024. Processors lock multi-year contracts to mitigate risk, but volatility tempers aggressive capacity expansions and suppresses the overall PEEK market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Aerospace Dominance Drives Premium Applications

Aerospace accounted for 55.34% of PEEK market share in 2025, underpinned by high regulatory compliance hurdles and weight-reduction economics that offset material premiums. Commercial airframe builders specify PEEK brackets, seals, and wire insulation to eliminate corrosion and meet flame-retardant thresholds. Medical devices, oil and gas tooling, and semiconductor wafer-handling systems comprise the fastest-growing “other” category, advancing at a 5.90% CAGR. Demand diversification helps shield the PEEK market from aerospace order-cycle volatility.

Continued engine electrification, fuel-cell development, and novel drone architectures extend aerospace pull through 2031. In parallel, rising spinal fusion procedure volumes and broader insurance reimbursement in the United States propel medical implant consumption. Across these applications, the PEEK market size expands as value shifts from high-throughput molding to low-volume precision machining, reinforcing the material’s position as an enabler of mission-critical components.

By Reinforcement: Carbon-Filled Innovation Accelerates Growth

Unfilled formulations retained 42.40% of the PEEK market size in 2025, driven by medical and semiconductor uses where particulate shedding must be minimized. Emerging aerospace and EV designs, however, demand higher modulus and conductivity, lifting carbon-filled grades to a 6.33% CAGR over the forecast horizon. The optimized fiber orientation achievable by laser-sintering enables lightweight brackets with 50% greater stiffness at identical mass relative to unfilled counterparts.

Glass-filled PEEK satisfies cost-sensitive auto under-hood parts, although higher density moderates weight-saving potential. Proprietary mineral-reinforced variants target compressor vane inserts and downhole pump components. Collectively, these tailored offerings demonstrate the PEEK market’s pivot toward application-specific compound development, leveraging the polymer’s inherent thermal envelope while fine-tuning mechanical and electrical properties.

Geography Analysis

The United States maintained 83.55% of regional PEEK market share in 2025 on the strength of its aerospace production footprint, FDA-aligned medical-device ecosystem, and sophisticated contract-manufacturing base. Civil aircraft output in Washington, South Carolina, and Texas anchors resin demand, while Silicon Valley fabs procure ultra-pure grades for 300-mm wafer transfer mechanisms. Oil-patch operators in the Permian Basin deploy PEEK seals in sour-gas service, reinforcing consumption diversity across industrial verticals.

Mexico represents the fastest-growing sub-market, charting a 7.70% CAGR as automotive electrification and aerospace tier-2 assembly migrate south to leverage labor-cost advantages under USMCA. Local molders in Nuevo León and Guanajuato install high-temperature presses to produce battery-cooling manifolds and connector housings. Government incentives for near-shoring critical supply chains further accelerate domestic capability buildup.

Canada’s demand centers on commercial aviation structures in Québec and additive-manufactured orthopedic implants clustered around Toronto. Energy operators in Alberta integrate PEEK thrust washers in bitumen upgraders, capitalizing on the polymer’s wear resistance and hydrocarbon compatibility. Across North America, logistics savings, regulatory alignment, and customer proximity consolidate the region’s position as the single largest consumer within the global PEEK market.

Competitive Landscape

The North American Polyether Ether Ketone (PEEK) market is consolidated in nature. Their backward integration into monomer production and expansive patent portfolios reinforce pricing power. North American compounders focus on downstream value-added services such as carbon-fiber masterbatch creation, close-tolerance machining, and sterilization-ready packaging. Strategic moves include 3D Systems’ launch of an end-to-end cranial-implant platform combining VSP design software, ProX SLS printers, and cleared VESTAKEEP-based powder. Evonik introduced a carbon-fiber reinforced filament enabling fused-filament fabrication of load-bearing implants, broadening application reach into sports-medicine fixation devices.

North America Polyether Ether Ketone (PEEK) Industry Leaders

Evonik Industries AG

Pan Jin Zhongrun High Performance Polymer Co., Ltd.

RTP Company

Syensqo

Victrex PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Journal of Medical and Biological Engineering published a finite-element validation of lattice-structured PEEK cervical discs, confirming superior load distribution versus ball-and-socket implants.

- October 2023: Evonik Industries, Inc. launched a carbon-fiber reinforced PEEK filament for 3D-printed medical implants. This biomaterial works with common extrusion-based 3D printing methods like fused filament fabrication (FFF).

North America Polyether Ether Ketone (PEEK) Market Report Scope

Aerospace, Automotive, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. Canada, Mexico, United States are covered as segments by Country.| Aerospace |

| Automotive |

| Electrical and Electronics |

| Industrial and Machinery |

| Other End-User Industries |

| Unfilled |

| Glass-filled |

| Carbon-filled |

| Other |

| United States |

| Canada |

| Mexico |

| By End-User Industry | Aerospace |

| Automotive | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Other End-User Industries | |

| By Reinforcement | Unfilled |

| Glass-filled | |

| Carbon-filled | |

| Other | |

| By Geography | United States |

| Canada | |

| Mexico |

Market Definition

- End-user Industry - Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyether ether ketone market.

- Resin - Under the scope of the study, virgin polyether ether ketone resin in primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms