Europe Polyether Ether Ketone (PEEK) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

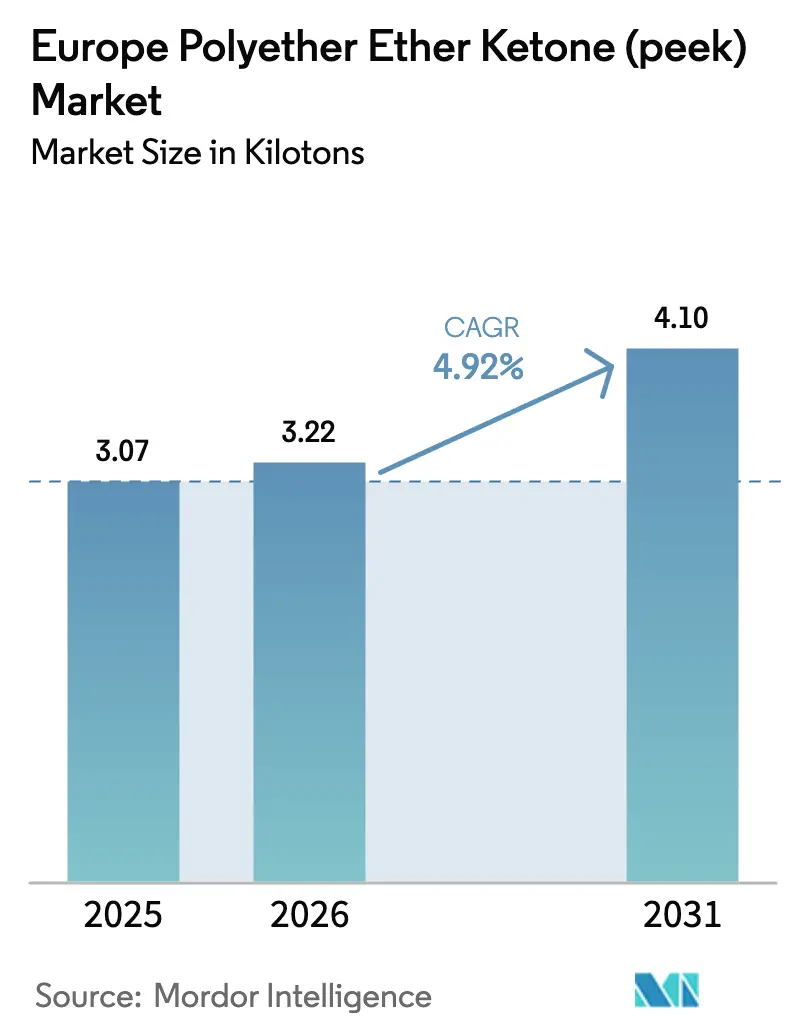

| Base Year Market Size (2025) | 3.07 kilotons |

| Market Volume (2026) | 3.22 kilotons |

| Market Volume (2031) | 4.1 kilotons |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Polyether Ether Ketone (PEEK) Market Analysis by Mordor Intelligence

Europe Polyether Ether Ketone market size in 2026 is estimated at 3.22 kilotons, growing from 2025 value of 3.07 kilotons with 2031 projections showing 4.1 kilotons, growing at 4.92% CAGR over 2026-2031. This steady trajectory underscores how a recovering aerospace sector and aggressive electric-vehicle lightweighting priorities are reshaping the region’s high-performance polymers landscape. European manufacturers are turning to polyether ether ketone for its chemical resistance, thermal stability, and processing versatility, gradually displacing traditional metal and lower-grade polymer solutions. Capacity tightness among a handful of integrated producers keeps supply–demand fundamentals balanced, yet surging imports from Asia are compressing margins and compelling incumbents to double down on application-specific innovation. Regulatory trends are equally influential: EU REACH drives compliance costs but also rewards PEEK’s non-toxic profile, while decarbonization policies encourage substitution of heavier metals with lighter engineering thermoplastics.

Key Report Takeaways

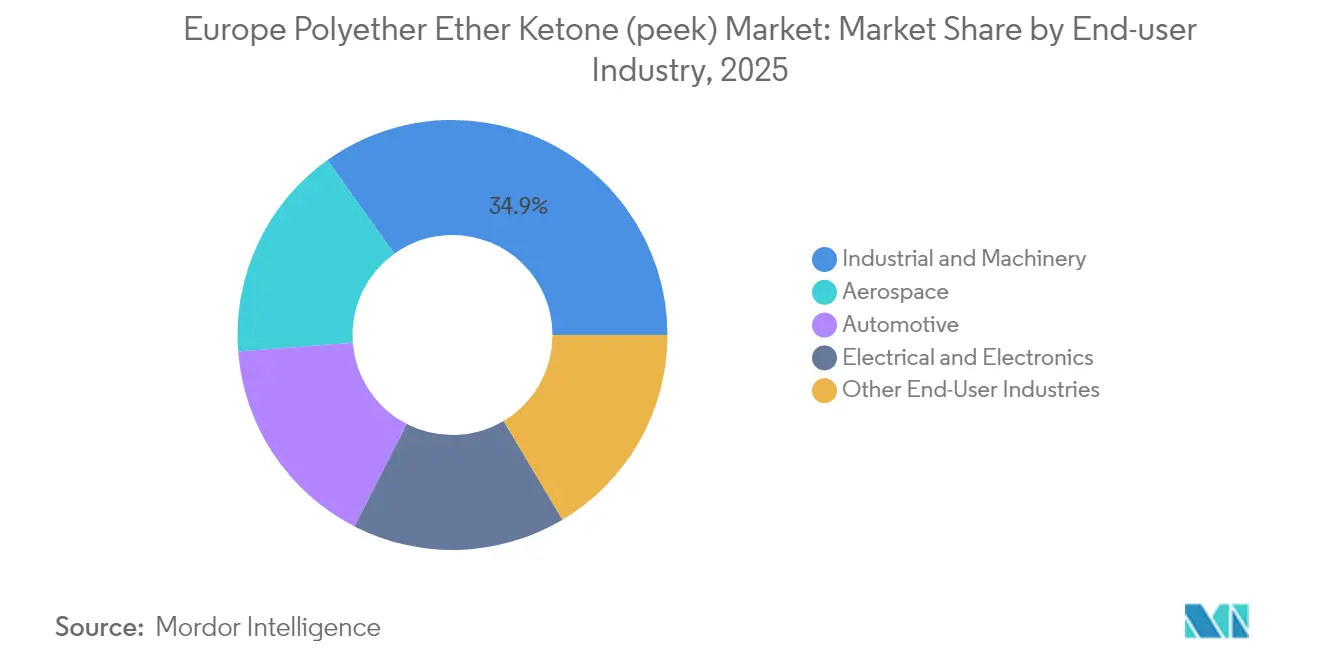

- By end-user industry, industrial machinery held 34.88% of the Europe Polyether Ether Ketone (PEEK) market share in 2025, whereas aerospace is expanding at a 5.67% CAGR through 2031.

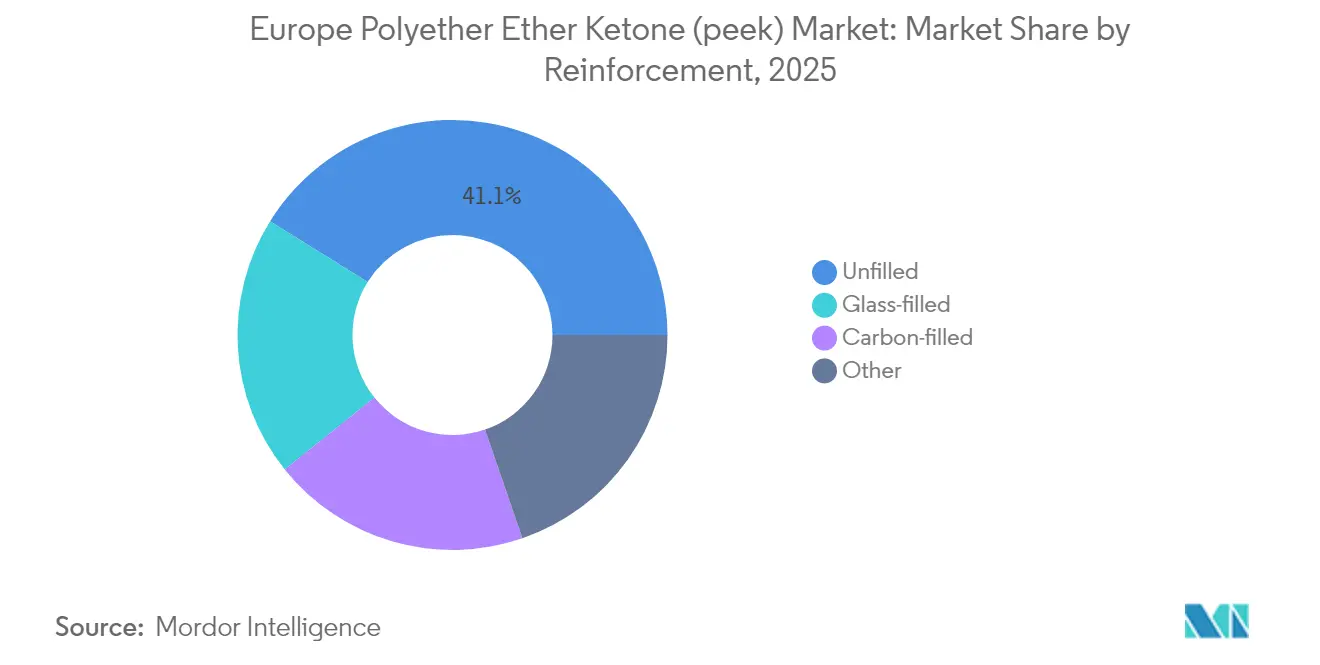

- By reinforcement, unfilled grades accounted for 41.12% of the Europe Polyether Ether Ketone (PEEK) market size in 2025, while carbon-filled grades are advancing at a 5.55% CAGR to 2031.

- By geography, Rest of Europe led with 33.02% volume in 2025; the United Kingdom is registering the fastest growth at a 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Polyether Ether Ketone (PEEK) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust EU aerospace production resurgence | +1.2% | Germany, France, UK, Italy | Medium term (2-4 years) |

| Accelerated EV component lightweighting push | +0.8% | Germany, France, Rest of Europe | Short term (≤ 2 years) |

| Miniaturization in high-frequency 5G electronics | +1.1% | Germany, UK, France | Long term (≥ 4 years) |

| Shift toward metal-free surgical implants | +0.7% | Germany, France, UK, Italy | Medium term (2-4 years) |

| OEM demand for chemical-resistant process line parts | +0.9% | Germany, Rest of Europe, France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust EU Aerospace Production Resurgence

European OEMs restarted wide-body and narrow-body programs in 2024, fueling record orders for thermoplastic composites. Airbus raised monthly A320neo output targets, while Boeing qualified Syensqo’s KetaSpire PEEK for secondary structures. Airframe suppliers now specify PEEK brackets, clamps, and electrical insulation systems because each kilogram trimmed translates to lower fuel burn. Defense contractors follow suit, adopting PEEK in helicopter rotor components and satellite subsystems. This trend revives demand across Germany and France, the region’s twin aerospace hubs.

Accelerated EV Component Lightweighting Push

Europe’s 2035 internal-combustion phase-out accelerates the use of lightweight parts. Evonik developed high-torque PEEK gears that cut drivetrain mass by 60% versus steel. Syensqo’s Ajedium PEEK film boosts e-motor efficiency by enabling higher slot fill factors in magnet wire insulation. Battery housings, busbars, and coolant manifolds also migrate to PEEK to withstand electrolytes and repeated charge cycles. German automakers account for the bulk of this incremental volume, but French and Spanish plants are rapidly certifying similar designs.

Miniaturization in High-Frequency 5G Electronics

Semiconductor fabs in Dresden, Imec, and South Wales have adopted PEEK wafer-handling parts that last 50% longer than PPS analogs and minimize ionic contamination. EU Chips Act incentives channel capital toward fan-out packaging lines, where PEEK test sockets maintain dimensional stability at 180 °C reflow profiles[1]European Commission, “European Chips Act,” digital-strategy.ec.europa.eu. Telecom infrastructure builders value PEEK’s low dielectric loss for mmWave antenna spacers and connector housings.

Shift Toward Metal-free Surgical Implants

Surgeons report lower stress-shielding with PEEK spinal cages and cranial plates. Evonik’s VESTAKEEP Fusion launched in 2024, integrating osteoconductive additives that promote bone on-growth. 3D Systems received FDA clearance for additively manufactured PEEK cranial implants, with 40 European cases completed by 2025. Imaging compatibility and allergy avoidance drive hospital procurement away from titanium, lifting volumes in Germany, Italy, and the UK.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU REACH red-tape for high-temperature polymers | -0.4% | EU-wide; notably Germany and France | Short term (≤ 2 years) |

| Volatile fluoro-aromatic precursor prices | -0.3% | EU-wide supply chain | Short term (≤ 2 years) |

| Emerging bio-based PPS substitutes | -0.2% | Germany, France, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU REACH Red-tape for High-temperature Polymers

Polymer microparticle rules add reporting layers that lift compliance budgets 15-20% for PEEK producers[2]European Chemicals Agency, “REACH Regulation Overview,” echa.europa.eu. Smaller firms struggle to finance toxicological dossiers, cementing incumbent advantages. OEM design cycles also lengthen as suppliers compile safety data across aerospace, medical, and electronics contexts. Nonetheless, PEEK’s halogen-free profile helps end-users meet substance restrictions more readily than fluorinated alternatives.

Volatile Fluoro-aromatic Precursor Prices

Difluorobenzophenone (DFBP) prices fluctuated in 2024, driven by Chinese plant turnarounds and freight surcharges. Each kilogram of PEEK contains roughly 0.8 kg of DFBP, so raw-material shocks squeeze margins. Industrial-grade pellets saw an 8% price drop, but medical-grade lots still command more than USD 500 per kg. European producers are discussing backward integration and off-take agreements to curb exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Industrial Machinery Drives Volume While Aerospace Accelerates Growth

Industrial machinery represented 34.88% of the European PEEK market in 2025, reflecting widespread use in pumps, valves, and chemical-processing components that face 250 °C fluids. This segment’s installed base creates repeat-purchase demand for replacement parts, anchoring overall tonnage. The aerospace category, although smaller, achieves the highest 5.67% CAGR as OEMs convert metallic clips and brackets to PEEK composites for fuel-efficiency gains. Automotive applications gain momentum from battery-electric models, with PEEK gears and e-axle bearings extending drivetrain life under high torque.

Electrical and electronics consumption scales gradually alongside 5G rollout. Medical devices contribute to a fast-growing niche, exemplified by 3D-printed patient-specific implants scheduled for wider EU adoption by 2026. The European PEEK market size for medical devices is poised to expand as hospital purchasing committees emphasize biocompatibility and MRI clarity.

By Reinforcement: Carbon-filled Variants Accelerate Despite Unfilled Dominance

Unfilled resin retained 41.12% of the European PEEK market share in 2025, favored for injection-molded parts with tight tolerances. Carbon-filled grades deliver the fastest 5.55% CAGR, meeting aerospace and EV stiffness requirements. Glass-filled blends cater to cost-sensitive industrial uses. Mineral-filled options support electronics where thermal conductivity is vital. Research shows that an optimal carbon-fiber loading lifts tensile strength 6.8% and elongation 14.85% over neat resin. European compounders fine-tune fiber length and surface treatment, achieving consistent modulus across large part geometries. The Europe Polyether Ether Ketone (PEEK) market size for carbon-filled grades is forecast to double in structural aircraft brackets and battery enclosures by 2030.

Carbon fiber reinforcement also unlocks the substitution of aluminum in robotics joints and semiconductor carrier plates. Process innovations, such as optimized twin-screw extruders with side feeders, prevent fiber attrition and ensure reproducible mechanical performance. OEMs lean on supplier application centers to co-engineer parts, embedding differentiation and customer lock-in.

Geography Analysis

The rest of Europe captured 33.02% of the 2025 volume, spanning the Netherlands, Belgium, Switzerland, and the Nordic countries. These nations favor PEEK in offshore energy equipment, pharma reactors, and precision machining. Ensinger’s new prepreg facility in Bavaria underpins the supply of thermoplastic composite tapes to these mid-sized markets.

The United Kingdom leads growth with a 6.08% CAGR through 2031. Victrex’s upstream integration and research and development campus in Lancashire anchors local supply, while aerospace clusters in Bristol and Glasgow qualify new thermoplastic composite wingskins. The National Health Service fosters adoption of PEEK spinal cages and cranial plates, making the UK a bellwether for medical applications. Post-Brexit customs align with EU technical standards but allow domestic fast-track regulatory decisions, accelerating commercialization.

Germany and France remain volume stalwarts. German automakers integrate PEEK e-motor insulation and battery module hardware, whereas French airframe plants demand flame-retardant grades for cabin interiors. Italy’s Lombardy region hosts orthopedic implant makers leveraging osteoconductive PEEK pellets. Eastern European uptake is modest but rising as contract manufacturers win EV component work. The Europe Polyether Ether Ketone (PEEK) market share gains in each locale depend on sector specializations, with no single geography replicating the UK’s growth momentum.

Competitive Landscape

The European PEEK market is consolidated in nature. Intellectual-property portfolios cover everything from biphenyl monomer synthesis to high-flow grades for thin-wall molding. Vertical integration reduces feedstock risk, though DFBP volatility remains a key variable. Strategic moves mirror this focus on downstream value. Victrex co-developed continuous-fiber reinforced tapes with Airbus, locking in multi-program supply. Syensqo partnered with a Tier-1 automotive supplier to qualify PEEK field coils for 800-V e-motors. Evonik invested in medical-grade filament lines to serve contract printers manufacturing orthopedic scaffolds.

Europe Polyether Ether Ketone (PEEK) Industry Leaders

Arkema

Ensinger GmbH

Evonik Industries AG

Syensqo

Victrex plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Essentra Components launched PEEK fasteners for fuel-system and ultra-high vacuum assemblies, citing superior chemical and thermal stability.

- May 2023: Evonik entered a non-exclusive deal with ProductionToGo to distribute INFINAM PEEK filaments and photopolymers across the EU, Switzerland, Norway, and the UK.

Europe Polyether Ether Ketone (PEEK) Market Report Scope

Aerospace, Automotive, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. France, Germany, Italy, Russia, United Kingdom are covered as segments by Country.| Aerospace |

| Automotive |

| Electrical and Electronics |

| Industrial and Machinery |

| Other End-User Industries |

| Unfilled |

| Glass-filled |

| Carbon-filled |

| Other |

| Germany |

| France |

| United Kingdom |

| Italy |

| Russia |

| Rest of Europe |

| By End-User Industry | Aerospace |

| Automotive | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Other End-User Industries | |

| By Reinforcement | Unfilled |

| Glass-filled | |

| Carbon-filled | |

| Other | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe |

Market Definition

- End-user Industry - Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyether ether ketone market.

- Resin - Under the scope of the study, virgin polyether ether ketone resin in primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms