Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

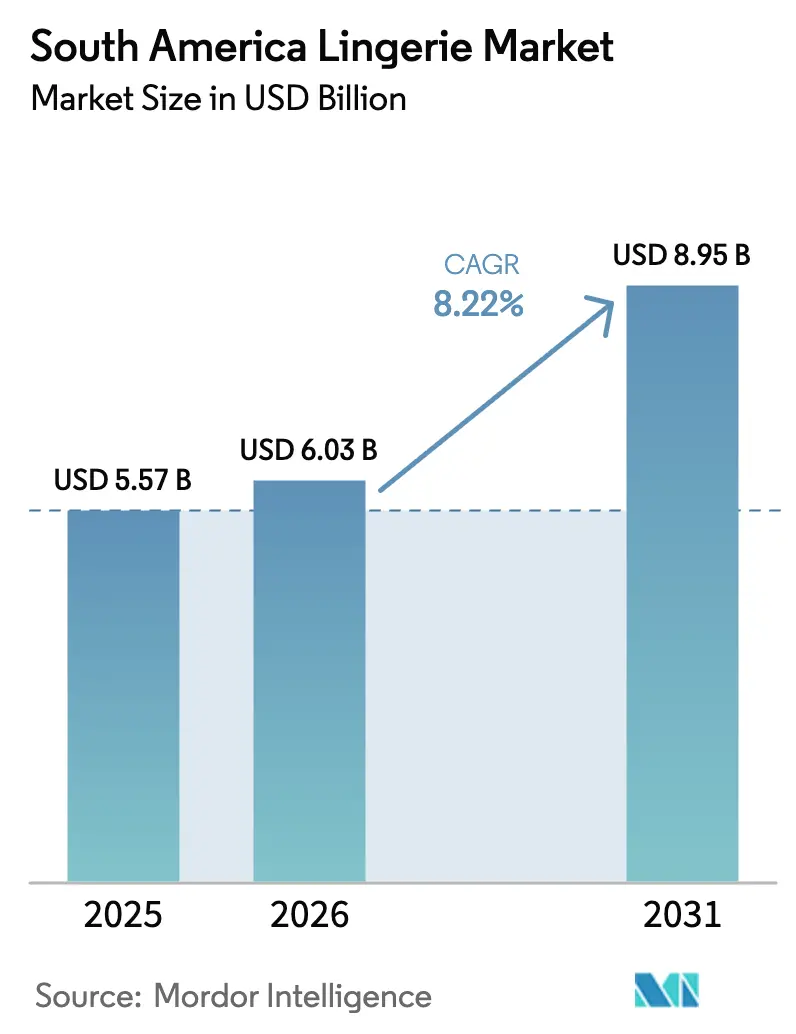

| Base Year Market Size (2025) | USD 5.57 Billion |

| Market Size (2026) | USD 6.03 Billion |

| Market Size (2031) | USD 8.95 Billion |

| Growth Rate (2025 - 2031) | 8.22% CAGR |

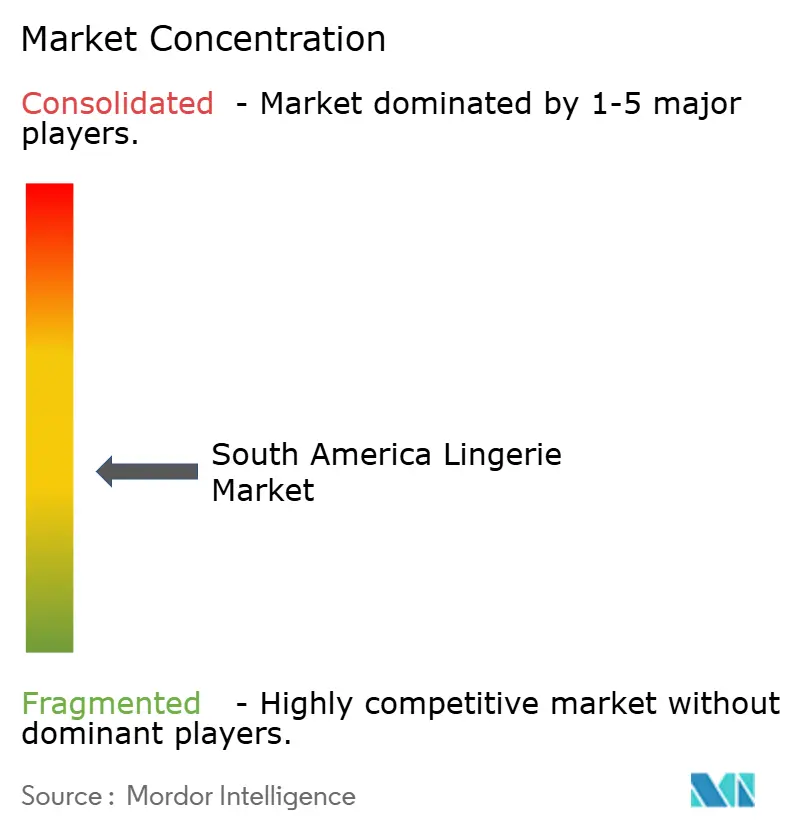

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Lingerie Market Analysis by Mordor Intelligence

The South America lingerie market size was valued at USD 5.57 billion in 2025 and estimated to grow from USD 6.03 billion in 2026 to reach USD 8.95 billion by 2031, at an 8.22% CAGR during the forecast period (2026-2031). A resilient rebound in discretionary spending, smoother cross-border trade, and widespread mobile connectivity are underpinning this trajectory. Online retail is scaling fastest, helped by the Pix instant-payment rail that handled 40% of Brazilian e-commerce transactions in 2025. Sustainability is no longer a niche concern: recycled and bio-based fibers are advancing at a 10.71% CAGR, outstripping cotton’s 42.87% revenue share. Competitive intensity is rising as multinationals open flagships in São Paulo and Buenos Aires while regional champions such as Leonisa double down on vertical integration. Counterfeit enforcement has improved—Brazilian customs seized more than 785,000 illicit pieces in 2025—yet parallel imports continue to weigh on branded margins.

Key Report Takeaways

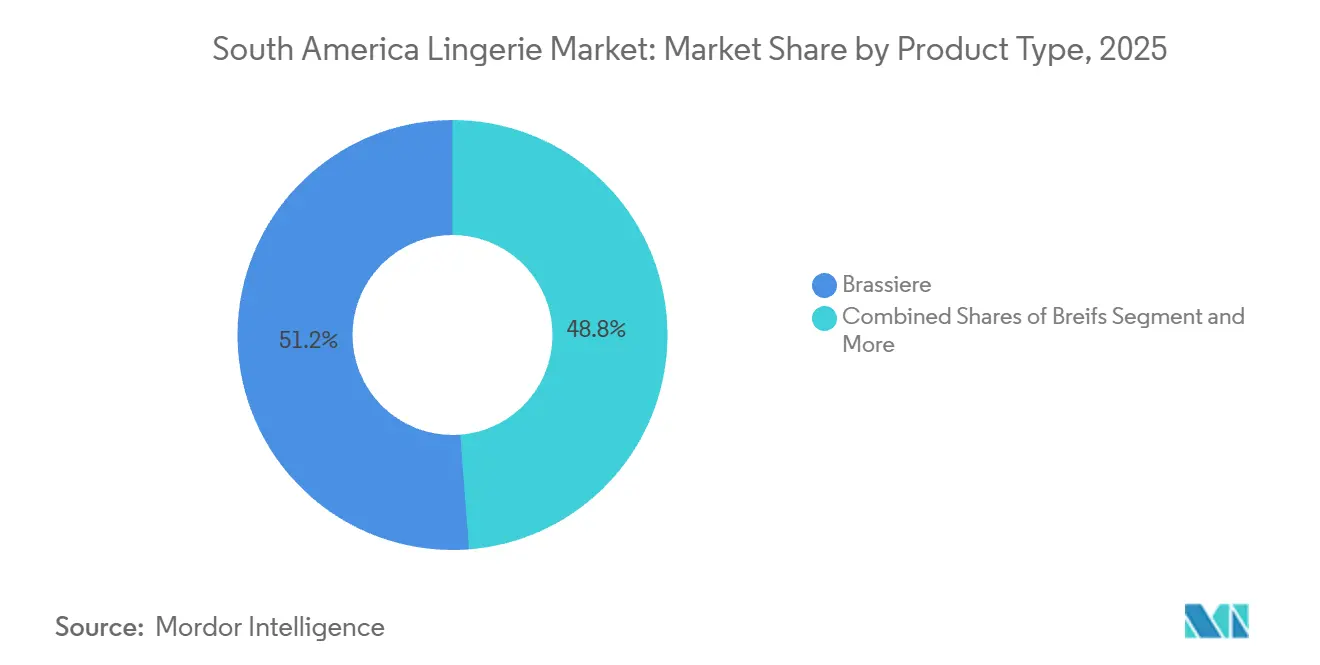

- By product type, brassieres led with a 51.23% revenue share in 2025, while the category is projected to expand at an 8.96% CAGR to 2031.

- By price range, the mass tier accounted for 72.35% of sales in 2025, and the premium tier is forecast to register a 9.21% CAGR through 2031.

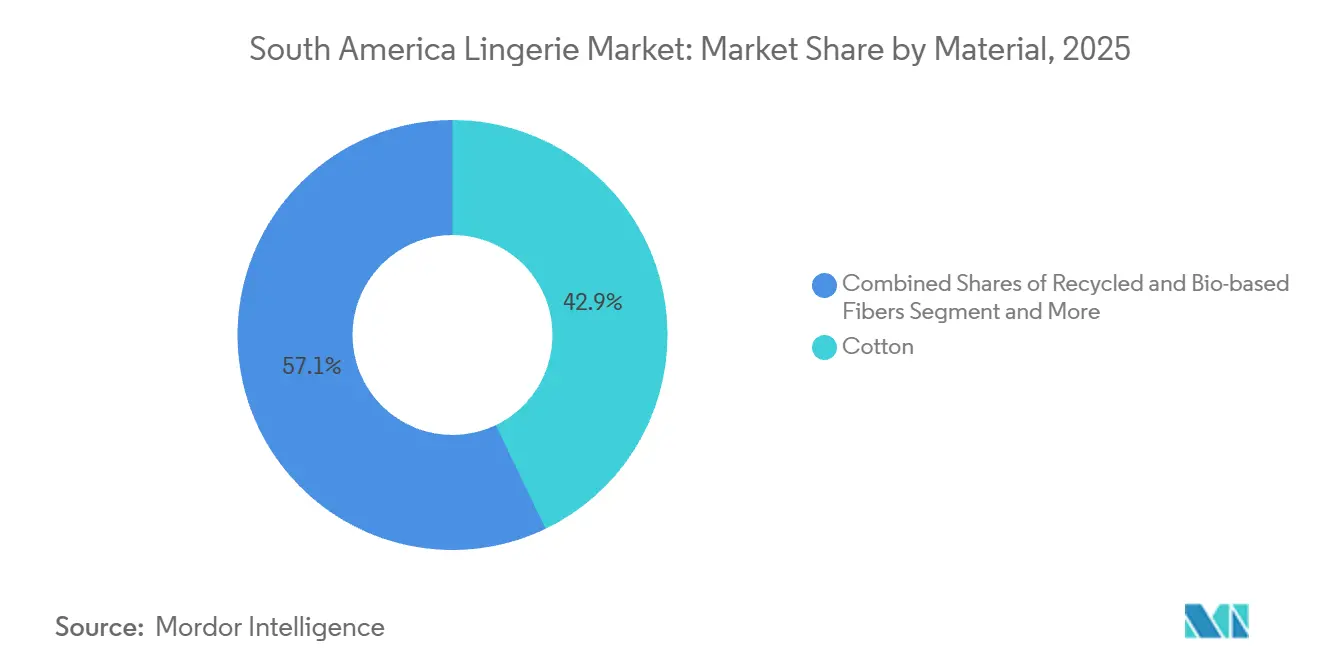

- By material, cotton captured 42.87% of 2025 turnover, whereas recycled and bio-based fibers are poised to advance at a 10.71% CAGR over 2026-2031.

- By distribution channel, specialty stores held 44.77% of receipts in 2025, yet online retail is expected to climb at a 9.42% CAGR to 2031.

- By geography, Brazil contributed 46.76% of regional income in 2025, and Argentina is projected to be the fastest-growing market at an 8.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Lingerie Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing E-Commerce Penetration Offering Wider Product Variety | +2.1% | Brazil, Argentina, Chile; spillover to Colombia and Peru | Short term (≤ 2 years) |

| Influence of Social Media and Influencer Marketing | +1.8% | Brazil (dominant), Argentina, Colombia | Short term (≤ 2 years) |

| Rising Focus on Sustainability and Ethical Fashion | +1.5% | Brazil, Chile, Argentina; urban centers across region | Medium term (2-4 years) |

| Rising Self-Care and Wellness Focus in Personal Grooming | +1.3% | Global; strongest in Brazil and Argentina middle-income cohorts | Medium term (2-4 years) |

| Innovations in Fabric and Design Technology | +1.0% | Brazil (manufacturing hub), Colombia (Leonisa, local producers) | Medium term (2-4 years) |

| Increased Female Workforce Participation Boosting Style Needs | +0.9% | Brazil, Chile, Argentina; urban employment centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing E-Commerce Penetration Offering Wider Product Variety

Digital commerce is addressing distribution gaps in second- and third-tier cities, where specialty stores face economic limitations. In 2025, Brazil's online lingerie sales surged, driven by mobile devices that enabled seamless discovery and purchases. Local payment systems like Pix, capturing 40% of online transactions, reduced checkout friction and cart abandonment, especially for low-cost items like panties and bralettes[1]Banco Central do Brasil. "Pix Payment System Statistics", bcb.gov.br. Marketplaces such as Mercado Libre and Shopee aggregated diverse SKUs from regional brands, allowing consumers to compare fit, fabric, and price in one session—an advantage physical retail cannot match. The rise of TikTok Shop highlights social commerce's growing influence, pulling market share from brick-and-mortar stores. This shift is fueling premium segment growth, as online platforms attract affluent consumers seeking unique fabrics, inclusive sizing, and direct-to-consumer brand stories.

Influence of Social Media and Influencer Marketing

Influencer-led discovery is redefining the path from awareness to purchase, disrupting the traditional marketing funnel. Creator content now drives online engagement, with consumers increasingly making purchases through interactive formats like live streams. The expanding creator ecosystem has opened marketing channels to smaller and regional brands, reducing reliance on large advertising budgets. Collaborations with micro-influencers are proving cost-effective, boosting engagement and follower growth. Social platforms targeting young, trend-driven audiences are fostering emerging labels that emphasize sustainability, inclusivity, and authenticity over legacy branding. Visual-first platforms are becoming discovery engines, where peer-generated content shapes product perception and buying decisions. Specialty retail stores are struggling to compete with the personalized, trust-driven influence creators deliver at scale.

Rising Focus on Sustainability and Ethical Fashion

Circularity is shifting from being a brand messaging tool to becoming a critical operational priority as textile waste and counterfeit enforcement intersect. In 2024, global textile waste reached 120 million metric tons, yet less than 1% was recycled into new fibers. Adding to the challenge, recycled polyester costs more than twice as much as virgin material, creating significant margin pressures for brands striving to implement closed-loop supply chains. Leonisa's production of over 10,000 swimwear pieces from recycled fishing nets over two years highlights the scale required to achieve material substitution while maintaining cost competitiveness. The LYCRA Company's upcoming January 2025 launch of the LIVE! Upfit collection, featuring bio-derived LYCRA EcoMade fiber, represents a pivotal development. This fiber, the first of its kind sampled globally and in Latin America, reflects fiber suppliers' efforts to localize sustainable inputs, reduce carbon footprints, and address regional demand. Brazil's Grupo Boticário, with its network of over 4,000 reverse-logistics collection points and an investment exceeding approximately USD 2.4 million in circularity initiatives, demonstrates how adjacent consumer goods sectors are building infrastructure that lingerie brands can leverage. In Chile, the Atacama Desert accumulates approximately 66,000 tons of clothing waste annually, much of it stemming from fast-fashion imports. With regulatory pressure intensifying for extended producer responsibility schemes, brands lacking take-back programs are at risk of facing penalties.

Rising Self-Care and Wellness Focus in Personal Grooming

Post-pandemic, premium lingerie has shifted from a functional necessity to a form of self-expression, driving increased spending among middle-income groups. Ipsos Flair Brazil 2025 highlights AI-driven personalization, virtual try-ons, and beauty-fit analysis as key innovations, with Gen Z demanding gender-inclusive products for diverse body types and identities. Brazilian brand Ouseuse exemplifies this trend with copper-ion-lined panties that eliminate 99% of fungi and bacteria and biodegradable nylon fitness lines with UV50+ protection, blending wellness with technology to justify premium pricing. Maria Fernanda Lingerie’s focus on empowerment, self-love, and self-care through inclusive, elegant designs aligns with consumers who view lingerie as self-care rather than a basic purchase. In Brazil, where women buy an average of 7.6 lingerie items annually, brands have multiple opportunities to upsell higher-margin products like lace bralettes, silk camisoles, and shapewear. Positioning lingerie within the wellness narrative helps premium brands avoid price competition, as consumers see these purchases as investments in confidence and well-being.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Competition From Unbranded And Low-Cost Imports | -1.4% | Brazil, Argentina, Chile; concentrated in mass segment | Short term (≤ 2 years) |

| Counterfeit Products Affecting Brand Value | -1.1% | Brazil, Peru, Chile, Argentina; online and informal retail channels | Short term (≤ 2 years) |

| Online Shoppers Grapple with Fit-Related Issues | -0.8% | Brazil, Argentina; e-commerce-heavy markets | Medium term (2-4 years) |

| Regulatory Variations and Compliance Hurdles by Country | -0.5% | Regional; cross-border e-commerce and import/export operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Competition From Unbranded And Low-Cost Imports

Unbranded imports from Asia are squeezing margins in the mass segment, where most of the 2025 revenue is concentrated. These imports offer price points 30-50% lower than domestic brands, without matching investments in fit development or fabric quality. In 2025, Argentina reduced tariffs on over 90 product lines, including polyester and fabrics. While this move has cut input costs for local manufacturers, it has also facilitated the entry of finished goods imports that undercut regional production. In January 2025, Brazil's textile capacity utilization in Argentina was a mere 33.9%. This chronic underutilization hampers domestic players' ability to achieve economies of scale and compete on price. Marketplaces like Shopee and Shein, which aggregate Chinese manufacturers and dropship directly to consumers, sidestep traditional import duties and quality inspections, creating an uneven playing field. The World Customs Organization's Operation FRONPIAS, carried out in January 2025, seized 13.8 million pieces across 332 cases in 14 countries across the Americas. Accessories and clothing were the focus of 71 seizures each. However, enforcement of these measures varies significantly across borders. As a result, branded players face a dilemma: compete on price and erode gross margins or invest heavily in brand differentiation. This differentiation comes through sustainability, influencer partnerships, and omnichannel experiences, all aimed at justifying premium pricing.

Online Shoppers Grapple with Fit-Related Issues

Fit inconsistencies drive lingerie returns, averaging 20% industry-wide, with reverse logistics costs in South America often exceeding item margins due to fragmented geography. Brarista's AI fitting solution, with over 20,000 confirmed fit records and 80% accuracy, claims to cut return rates to 3% and boost order values by 61%. However, adoption is limited to digitally native brands like Lemonade Dolls, while mass-market players lag. The lack of standardized sizing across brands worsens the issue, as a size M in Brazil may equal a size L in Colombia or Argentina, prompting consumers to buy multiple sizes and return extras, inflating costs. Virtual try-on technology, requiring costly 3D scans and algorithms, remains inaccessible to smaller players. INTERPOL's Operation Crete II (August–September 2024) seized over 11 million counterfeit products worth USD 225 million, highlighting how fake goods, mimicking branded packaging but offering poor fit and quality, erode online shopping trust. Brazil's ADI No. 03/2025, effective December 2025, allows customs to confiscate counterfeit goods without judicial orders, supporting brand protection. Yet, with over 785,000 products seized in 2025 so far, enforcement struggles to keep up with counterfeit inflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Brassieres Command Innovation Premium

In 2025, brassieres contributed 51.23% of product-type revenue and are projected to grow at 8.96% annually through 2031, driven by innovations like wireless designs, adaptive sizing, and moisture-wicking fabrics suited for humid climates. This category remains a repeat-purchase staple, with Brazilian women buying an average of 7.6 lingerie items annually, 40-50% of which are brassieres. The shift towards comfort, fueled by remote work, has boosted demand for wireless bras, with brands like Leonisa leading the trend through body-positive messaging and large-scale production. Brazilian brand Ouseuse differentiates itself with copper-ion linings that eliminate up to 99% of fungi and bacteria. Additionally, the LYCRA Company's bio-derived LYCRA EcoMade fiber, launched in Brazil's LIVE! Upfit collection in January 2025, combines performance features like compression and UPF50+ sun protection, blending lingerie with activewear and supporting premium pricing.

Briefs and other categories—camisoles, shapewear, and sleepwear—account for 48.77% of revenue but grow slower as consumers focus on core products. Briefs, with lower prices and frequent purchases, act as entry points for new brands but face margin pressure from unbranded imports. Shapewear sees growth with rising female workforce participation in Brazil and Chile, though sizing challenges and in-person fitting needs limit expansion. Camisoles and sleepwear, positioned as self-care indulgences, grow modestly due to premiumization trends but remain niche with limited repeat purchases. The convergence of lingerie and activewear, highlighted by Riachuelo's February 2021 "Mais Sustentável Fitness" collection using biodegradable polyamide, expands the market while complicating segmentation.

By Price Range: Mass Dominance Meets Premium Acceleration

In 2025, the mass segment dominated with 72.35% of revenue, reflecting South America's income distribution and the focus of specialty stores and hypermarkets on volume over margin. Meanwhile, the premium segment is growing at 9.21% annually through 2031, outpacing the market's 8.22% CAGR. Rising disposable incomes, influencer-driven trends, and sustainability messaging are driving demand among urban middle-income groups. In Brazil, premium lingerie is increasingly seen as an accessible indulgence. Victoria's Secret's flagship store launch in Buenos Aires in November 2025 highlights confidence in premium demand, despite economic challenges. The brand's Q3 2025 sales rose 9.21% year-on-year to USD 1.471 billion, reflecting global players' success in the premium tier. E-commerce is fueling premium growth by offering SKU variety and price comparisons unavailable in physical stores. With gross margins 20-30 percentage points higher than the mass market, the premium segment is attracting new entrants.

Mass-market brands are responding with vertical integration, localized production, and competitive pricing, but margin pressures are driving consolidation. Gildan's USD 4.4 billion acquisition of HanesBrands, announced in August 2025 and closing in early 2026, will create a combined entity with over 40 manufacturing sites in Central America, enabling faster lead times and USD 200 million in annual cost savings. Brazilian brand Nayane, which achieved 30% revenue growth in H1 2025 and expanded to 4,000 wholesale clients, is scaling through automation and plans to open a third factory in H2 2025. However, unbranded Asian imports, priced 30-50% lower than domestic brands, are squeezing margins, forcing mass-market players to invest in differentiation or exit. Argentina's tariff cuts on over 90 product lines, including polyester and fabrics, have reduced input costs but also increased competition from finished-goods imports, challenging local producers[2]Argentine Ministry of Economy. "Tariff Reductions and Trade Policy", economia.gob.ar.

By Material: Cotton Leads, Sustainability Fibers Surge

In 2025, cotton accounted for 42.87% of material-based revenue, driven by its breathability, hypoallergenic properties, and consumer trust. Recycled and bio-based fibers, growing at 10.71% annually through 2031, are the fastest-expanding segment, reflecting regulatory pressures, rising demand for circularity, and sustainable inputs from local suppliers. The LYCRA Company's bio-derived LYCRA EcoMade fiber, launched in Brazil's LIVE! Upfit collection in January 2025, matches traditional spandex in performance while reducing environmental impact. Its recognition at ISPO 2024 underscores the growing competitiveness of sustainable fibers.

Silk, satin, and synthetic materials make up the remaining 57.13% of revenue. Synthetics dominate the mass market due to affordability and durability, while silk and satin focus on the premium tier. In South America's humid climates, synthetics like nylon and polyester excel with moisture-wicking and quick-drying properties, extending garment life and reducing wash frequency. Riachuelo's "Mais Sustentável Fitness" collection, launched in February 2021, uses Rhodia's Amni Soul Eco biodegradable polyamide, which decomposes in about three years, addressing environmental concerns tied to synthetics. Silk and satin remain niche due to higher costs and care needs but are growing in the premium segment as self-care indulgences. Hybrid materials, such as recycled polyester blended with organic cotton, balance cost, comfort, and sustainability.

By Distribution Channel: Specialty Stores Hold, Online Disrupts

In 2025, specialty stores contributed 44.77% of distribution-channel revenue, driven by personalized fitting services, tactile product evaluations, and instant gratification. However, online retail is growing rapidly at 9.42% annually through 2031, the fastest in this segment. E-commerce addresses distribution gaps in smaller cities, aggregates niche SKUs, and leverages social commerce to streamline the marketing funnel. In Brazil, online lingerie sales rose from 15-20% in 2024 to 20-25% in 2025, with mobile devices generating 72% of e-commerce traffic, enabling quick purchases. Local payment systems like Pix, which handled 40% of online transactions in 2025, reduced checkout friction and cart abandonment. TikTok Shop is projected to capture 5-9% of Brazil’s e-commerce volume by 2028, equivalent to BRL 25-39 billion, signaling social commerce’s growing impact on channel dynamics.

Supermarkets, hypermarkets, and other channels, including direct-to-consumer stores and department store concessions, held the remaining 55.23% of revenue. Supermarkets and hypermarkets drive mass-segment volume through high foot traffic and impulse buys but struggle to meet premium demand due to limited assortments and fitting services. H&M’s launch of four stores in São Paulo in 2025, with four more planned for 2026 in Rio de Janeiro and Porto Alegre, highlights fast-fashion brands’ focus on physical retail to build brand awareness and attract omnichannel shoppers. Similarly, Victoria’s Secret opened its first Argentina flagship in Buenos Aires in November 2025, emphasizing specialty stores’ role in delivering premium experiences. However, rising rents are pressuring physical retail economics, prompting brands to use stores as marketing tools to boost online traffic and customer lifetime value rather than standalone profit centers.

Geography Analysis

In 2025, Brazil is projected to hold a 46.76% market share, driven by its strong economy and advanced retail infrastructure that supports domestic and international brand growth. Leading in e-commerce in 2024 with fashion penetration at 15-20%, the market favors digital-first lingerie brands, while established retailers enhance omnichannel strategies (Brazilian E-commerce Association). The Pix payment system simplifies online transactions, boosting sales of premium lingerie items. São Paulo and Rio de Janeiro ensure efficient distribution, while secondary cities offer growth opportunities for geographic diversification.

Argentina is expected to grow at a CAGR of 8.37% from 2026 to 2031, despite economic challenges. Government support for hemp-derived and sustainable textiles (Argentine Ministry of Agriculture) drives modernization. The country’s fashion heritage and design expertise give local brands an edge by blending European aesthetics with regional insights. However, currency fluctuations create mixed impacts, improving export competitiveness but increasing costs for imported materials.

Colombia, Chile, and Peru show strong growth potential, supported by economic recovery and a growing middle class with higher spending power. Colombia’s urban concentration and import reliance create opportunities for local and international brands (Colombian National Statistics Department). Chile’s sustainability-focused regulations encourage early adoption of recycled and bio-based fibers, while Peru’s textile manufacturing offers a regional alternative to Asian sourcing. Success in these markets requires localized strategies addressing consumer preferences, regulations, and distribution, while leveraging regional trade agreements for cross-border expansion.

Competitive Landscape

The South America lingerie market is moderately fragmented, allowing global and regional brands to secure strong positions through unique strategies. Global players like Victoria's Secret, Triumph International, and Hanesbrands use their scale for efficient supply chains and marketing. Regional brands such as Leonisa and CLO Intimo focus on local knowledge and cultural alignment to connect with consumers. The market benefits from diverse channels, with specialty stores supporting premium products and mass retailers driving cost-focused strategies.

Technology is a key competitive factor, with brands adopting virtual fitting tools, smart textiles, and data analytics to improve customer experience and operations. In 2024, Redwood Capital Management acquired Hunkemöller, highlighting private equity interest in scaling digital-first lingerie brands. Patents for seamless designs and sustainable fibers protect premium brands, while commodity producers face pressure from standardized products. Opportunities lie in sustainable luxury and personalized services that combine premium materials with data-driven fit optimization.

The market targets both mass and premium segments. Mass-market products focus on affordability through e-commerce and retail partnerships, while premium products emphasize luxury, comfort, and design, often showcased in flagship stores and exclusive collections. Cotton remains popular for its comfort, while synthetic fabrics are growing due to features like moisture-wicking and stretchability. Sustainable materials, such as organic cotton and biodegradable fabrics, are gaining traction as demand for ethical fashion rises. These strategies help brands meet diverse consumer needs across South America.

South America Lingerie Industry Leaders

-

Victoria's Secret & Co.

-

CLO intimo

-

Global Intimates LLC (Leonisa)

-

PVH Corp.

-

Lojas Renner (Valisere)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Authentic Brands Group (ABG) expands its footprint in South America with a strategic alliance for Nautica in Brazil. The company has announced a long-term agreement with Altomax, a leading manufacturer in the underwear and hosiery segment, which will oversee the development, production, and distribution of these categories for men, women, and children in the Brazilian market.

- April 2025: Alto Palermo, one of Buenos Aires' most iconic shopping malls, announced an agreement with global brand Victoria's Secret, which opened its first full-assortment store in Argentina. The store offered a wide selection of products, from classic lingerie to the full Victoria's Secret Beauty line, including fragrances and popular body mists.

- April 2025: Victoria's Secret launched its first full-line store in Argentina at Alto Palermo. According to the brand, the new store will be located on the second floor of the shopping mall and will span more than 400 square meters. It will offer a wide selection of products, from classic lingerie to the full Victoria's Secret Beauty line, including fragrances and popular body mists.

South America Lingerie Market Report Scope

Lingerie is a category of women's clothing, including shapewear, undergarments, and others. This line of garments for women includes bras, panties, and camisoles, among others. The South American lingerie market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into brassiere, briefs, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. It provides an analysis of emerging and established economies across the region, comprising Brazil, Argentina, Columbia, and the rest of South America. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Brassiere |

| Briefs |

| Other Product Types |

By Price Range

| Mass |

| Premium |

By Material

| Cotton |

| Silk and Satin |

| Synthetic |

| Recycled and Bio-based Fibers |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| Oat |

| By Product Type | Brassiere |

| Briefs | |

| Other Product Types | |

| By Price Range | Mass |

| Premium | |

| By Material | Cotton |

| Silk and Satin | |

| Synthetic | |

| Recycled and Bio-based Fibers | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Oat |

Key Questions Answered in the Report

What is the current value of the South America lingerie market?

The market stood at USD 6.03 billion in 2026 based on Mordor Intelligence estimates.

How fast will premium lingerie grow in South America?

Premium lines are projected to register a 9.21% CAGR between 2026 and 2031, the quickest pace among price tiers.

Which country will see the strongest sales growth through 2031?

Argentina is forecast to be the fastest-growing market with an 8.37% CAGR as inflation cools and tariffs drop.

How is e-commerce changing lingerie distribution?

Online retail is expanding at a 9.42% CAGR thanks to payment innovations like Pix and social-commerce discovery engines.

Page last updated on: