Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

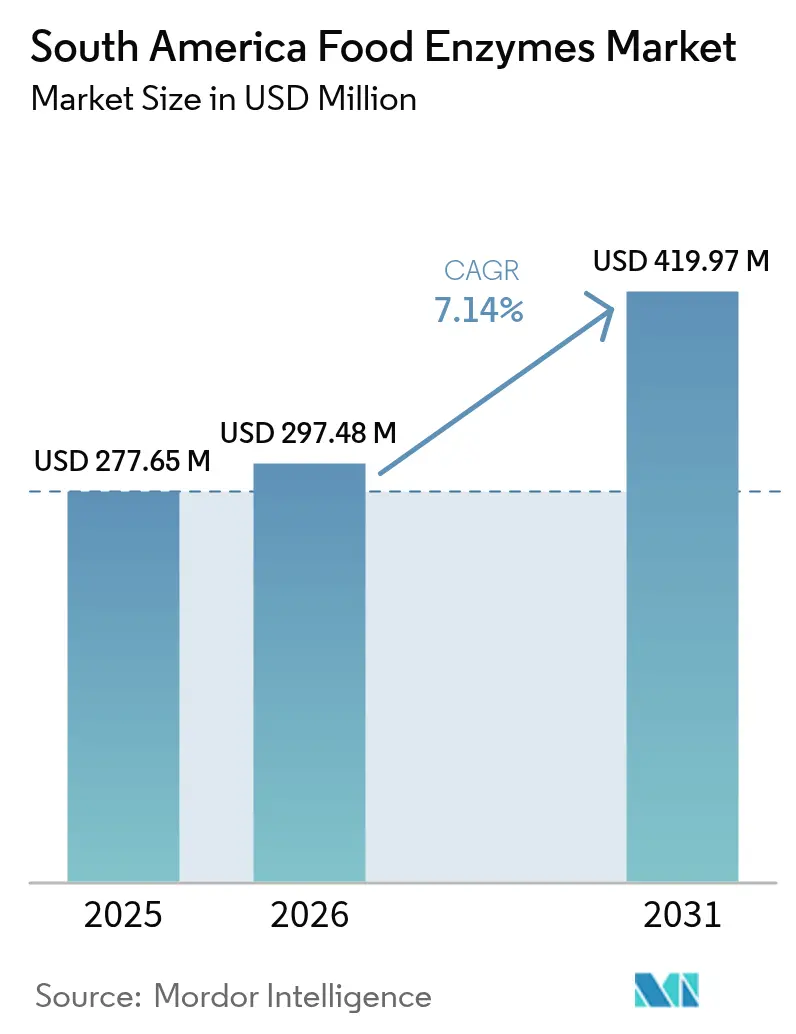

| Base Year Market Size (2025) | USD 277.65 Million |

| Market Size (2026) | USD 297.48 Million |

| Market Size (2031) | USD 419.97 Million |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

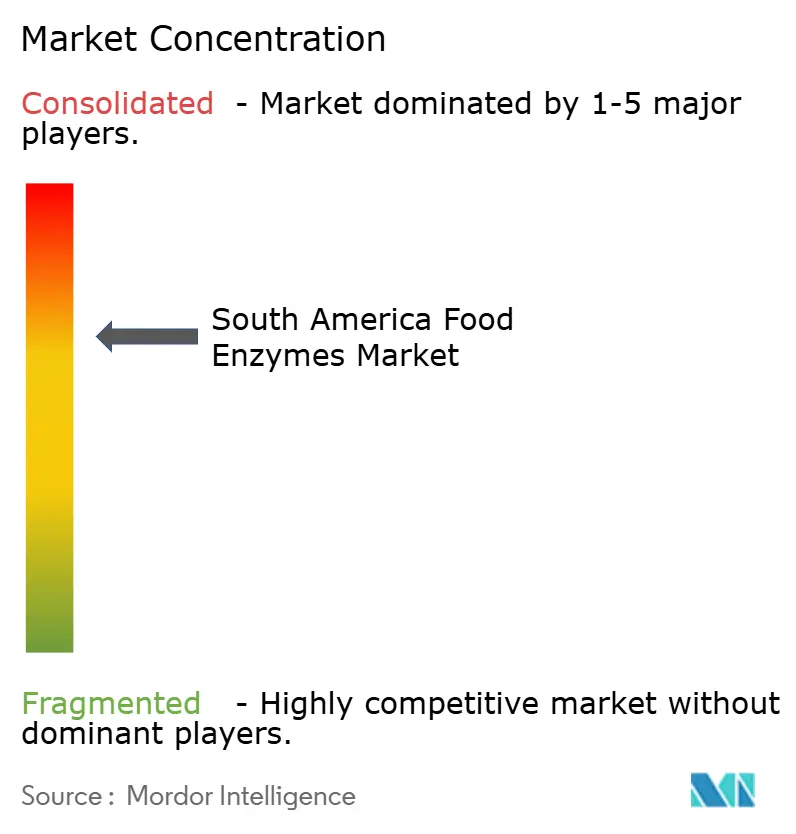

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Food Enzymes Market Analysis by Mordor Intelligence

The South American food enzymes market size is expected to grow from USD 277.65 million in 2025 to USD 297.48 million in 2026 and is forecast to reach USD 419.97 million by 2031 at 7.14% CAGR over 2026-2031. Manufacturers in the region are moving from bulk commodities toward value-added processed foods, and enzymes enable that shift because they lengthen shelf life, lower waste, and help processors claim clean labels without overhauling entire recipes. Currency swings, especially the 2024-2025 real depreciation, magnify the cost of imported concentrates, yet local demand keeps rising as bakery, dairy, and beverage plants upgrade lines for higher throughput. Multinational suppliers dominate technically complex applications, but regional distributors win share by repacking enzymes into smaller formats and extending flexible credit to mid-sized processors. Regulatory hurdles under (Agência Nacional de Vigilância Sanitária) ANVISA’s RDC 728 lengthen product-launch timelines to roughly two years, so firms that already hold dossiers enjoy a first-mover edge

Key Report Takeaways

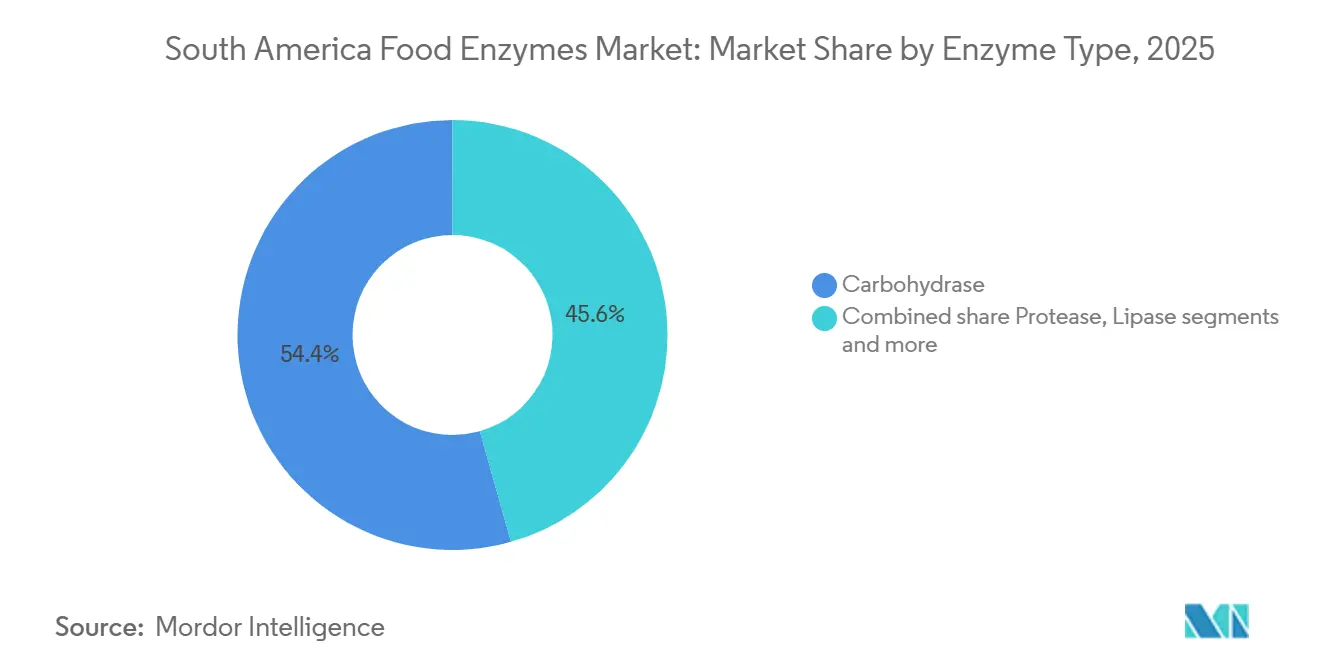

- By enzyme type, carbohydrases led with 54.39% of the food enzymes market share in 2025, while lipase is the fastest-growing enzyme type at a 7.76% CAGR through 2031.

- By form, powder forms accounted for 67.38% of the food enzymes market size in 2025 and are projected to grow at a CAGR at 7.46% through 2031.

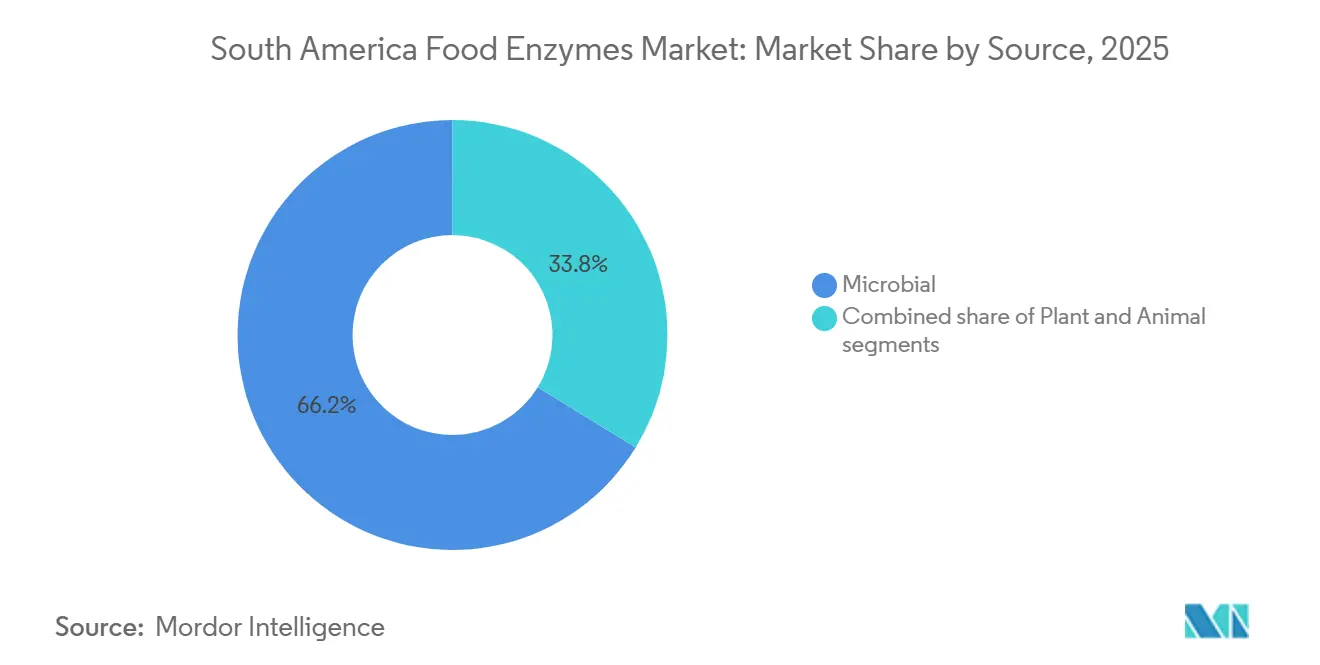

- By source, microbial sources captured 66.24% food enzymes market share during 2025, whereas plant-derived variants expand at a 7.61% CAGR.

- By application, bakery and confectionery held 24.73% revenue share in 2025; dairy and desserts represent the quickest-growing application at an 8.07% CAGR.

- By geography, Brazil commanded 42.93% of regional revenue during 2025, but Argentina posts the strongest growth with an 8.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Food Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumption of bakery and confectionery products | +1.3% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Rising demand for clean-label and natural ingredients | +1.5% | Brazil, Chile, Argentina | Long term (≥ 4 years) |

| Expansion of dairy and beverage processing industries | +1.4% | Brazil, Argentina, Peru | Medium term (2-4 years) |

| Demand for lactose-free and specialty food products | +1.2% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Technological advancements in enzyme development | +0.9% | Regional, led by Brazil | Long term (≥ 4 years) |

| Rising adoption of enzymes for process efficiency | +1.0% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumption of bakery and confectionery products

Urbanization and the rise of dual-income households are boosting per-capita consumption of packaged breads, cakes, and biscuits across South America. Manufacturers are using bakery enzymes to cut dough mixing time, enhance crumb softness, and extend shelf life without synthetic emulsifiers. Amylases break down damaged starch into fermentable sugars, speeding up yeast activity and producing higher loaf volumes. Xylanases modify pentosan structure to improve dough machinability on high-speed production lines. In 2024, Brazil's bakery sector produced 7.2 million tonnes of bread, increasing by 4.1% compared to 2023, as supermarket chains expanded in-store bakeries to capture impulse purchases[1]Source: Associação Brasileira da Indústria de Panificação e Confeitaria, “Theme: Healthiness”, abip.org.br. Argentina's alfajor and facturas manufacturers are adopting enzyme blends to maintain texture during the country's high-humidity summer months, reducing product returns and waste. The shift toward artisanal-style breads with visible grains and seeds is prompting formulators to use cellulases and hemicellulases, which soften bran particles and prevent the "sandpaper" mouthfeel consumers reject.

Rising demand for clean-label and natural ingredients

Urban consumers are increasingly scrutinizing ingredient lists, linking chemical-sounding additives to health risks and demanding transparency from food brands. Enzymes provide a regulatory edge: as processing aids, they often escape declaration on finished-product labels under Codex and Mercosur guidelines. This loophole enables manufacturers to tout "no artificial preservatives" claims while still achieving desired functional outcomes. A 2024 survey by the Brazilian Food Industry Association revealed that 68% of consumers would pay a 15-20% premium for products labeled as natural or organic[2]Source: Associação Brasileira da Indústria de Alimentos, “The numbers that drive the industry”, abia.org.br. This presents margin opportunities for brands reformulating with enzymes, steering clear of synthetic dough conditioners or flavor enhancers. Chile's updated food-labeling law, which enforces black warning octagons for high sodium, sugar, and saturated fat, is inadvertently amplifying enzyme use. Manufacturers are now using lipases to trim fat content in baked goods, ensuring mouthfeel remains intact. The clean-label movement isn't confined to retail; foodservice operators catering to schools and hospitals are also adapting. Facing procurement specs that limit E-numbers, they're increasingly turning to enzyme-assisted production.

Expansion of dairy and beverage processing industries

The expansion of dairy and beverage processing industries is a key driver of the South America food enzymes market. Growing consumer demand for processed dairy products such as cheese, yogurt, flavored milk, and lactose-free beverages is encouraging manufacturers to adopt enzymes to improve product texture, flavor, and shelf stability. Food enzymes play a crucial role in enhancing production efficiency, optimizing fermentation processes, and reducing processing time, making them increasingly valuable for large-scale dairy operations. In the beverage sector, enzymes are widely used to improve juice clarification, extraction yields, and product consistency, supporting rising demand for fruit-based and functional drinks. Increasing investments in modern food processing facilities across countries such as Brazil and Argentina are further accelerating enzyme adoption. Additionally, the rising popularity of health-oriented and lactose-free products is driving the use of specialized enzymes in formulation.

Demand for lactose-free and specialty food products

Rising demand for lactose-free and specialty food products is a significant driver of the South America food enzymes market. Increasing awareness of lactose intolerance and digestive health issues is encouraging consumers to shift toward lactose-free dairy products and functional food alternatives. Food enzymes, particularly lactase, play a crucial role in breaking down lactose, enabling manufacturers to produce dairy products that are easier to digest without compromising taste or nutritional value. The growing popularity of specialty foods, including high-protein, reduced-sugar, and clean-label products, is further supporting enzyme adoption in food processing. Manufacturers are increasingly using enzymes to improve product texture, enhance flavor development, and extend shelf life while maintaining natural formulations. Expanding urban populations and rising disposable incomes are also contributing to higher consumption of value-added and health-oriented food products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of enzyme production and formulation | -0.8% | Regional, acute in smaller markets | Short term (≤ 2 years) |

| Strict regulatory approvals and compliance requirements | -0.6% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Limited awareness among small-scale manufacturers | -0.5% | Peru, Colombia, Rest of South America | Long term (≥ 4 years) |

| High dependency on imports for enzyme supply | -0.7% | Regional, except Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of enzyme production and formulation

Enzyme manufacturing relies on capital-intensive fermentation infrastructure, sterile production environments, and downstream purification processes, including chromatography and ultrafiltration. These requirements increase unit costs, making it difficult for small and mid-sized food processors to manage. Additionally, maintaining enzyme activity during transport from production sites to end-users requires cold-chain logistics. In regions with inconsistent refrigerated transport, such as northern Brazil and the Andean highlands, this requirement raises landed costs by 12-18%. Currency depreciation further worsens these challenges. In 2024, Brazil's real depreciated by 8.3% against the US dollar, which increased the costs of imported enzyme concentrates[3]Source: Bando Central do Brasil, “BCB's Annual Conference”, bcb.gov.br. This situation forces processors to either reduce margins or raise prices for retailers. Many small bakeries and dairy plants fail to optimize enzyme dosing due to a lack of expertise. This failure often leads to over-application, which reduces cost savings and can introduce off-flavors.

Strict regulatory approvals and compliance requirements

Strict regulatory approvals and compliance requirements represent a significant restraint for the South America food enzymes market. Food enzymes must meet stringent safety, labeling, and quality standards set by national food regulatory authorities before being approved for commercial use. The approval process can be time-consuming and costly, requiring extensive documentation, testing, and validation to demonstrate product safety and efficacy. These regulatory complexities may delay product launches and increase operational costs for enzyme manufacturers and food processors. Smaller companies, in particular, may face challenges in meeting compliance requirements due to limited financial and technical resources. Variations in regulatory frameworks across different South American countries further add complexity to market entry and expansion strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enzyme Type: Lipase Gains as Dairy Pivots to Specialty Fats

Carbohydrases dominated the South America food enzymes market in 2025, capturing the largest share of 54.39%. This segment maintained its leading position due to its widespread use in bakery, dairy, and beverage applications, where it helps improve texture, sweetness, and overall product quality. The versatility of carbohydrases in breaking down complex carbohydrates into simpler sugars makes them highly valuable across multiple food processing industries. Their ability to enhance yield and reduce processing time further strengthens their adoption among manufacturers. Additionally, growing consumer demand for functional and nutritionally enhanced foods has reinforced the preference for carbohydrase-based solutions.

Lipase, on the other hand, emerged as the fastest-growing enzyme segment, projected to expand at a CAGR of 7.76% through 2031. This rapid growth is driven by increasing demand in dairy, bakery, and fat modification applications, where lipases help improve flavor, texture, and shelf life. The rising popularity of specialty and high-value dairy products, such as cheese and flavored spreads, has fueled lipase consumption. Technological advancements in enzyme formulation have also enhanced the efficiency and stability of lipase, encouraging wider adoption. Moreover, the growing focus on clean-label and natural processing solutions has further boosted its demand.

By Form: Powder Dominates but Liquid Gains in Automated Dairies

Powder enzymes commanded 67.38% of market share in 2025 and will grow at 7.46% CAGR through 2031, favored for their ambient-temperature stability, ease of transport, and compatibility with manual dosing systems prevalent in small bakeries and regional dairy plants. Liquid enzyme formulations are gaining share in large-scale operations where automated dosing pumps ensure precise addition rates, reducing over-application waste and improving batch-to-batch consistency. Powder enzymes offer logistical advantages in tropical climates where cold-chain infrastructure is unreliable; they can be stored at room temperature for 12-18 months without significant activity loss, whereas liquid enzymes require refrigeration at 2-8°C to prevent microbial contamination and activity degradation.

Liquid enzymes are preferred in continuous dairy processing lines where inline dosing systems inject enzymes directly into milk streams ahead of pasteurizers or cheese vats, eliminating the dust generation and dissolution time associated with powders. Large Brazilian dairy cooperatives operating ultrafiltration plants report 8-12% reductions in enzyme usage when switching from powder to liquid formats, as the latter offer higher specific activity and eliminate losses from incomplete dissolution. The liquid segment is also benefiting from enzyme producers' development of stabilized formulations that extend shelf life to 24 months under refrigeration, narrowing the convenience gap with powders.

By Source: Microbial Enzymes Lead but Plant-Derived Variants Capture Clean-Label Premium

Microbial sources dominated the South America food enzymes market in 2025, accounting for the largest share of 66.24%. Their leading position is driven by high yield, consistent quality, and ease of production compared to animal- or plant-derived enzymes. Microbial enzymes are highly versatile, making them suitable for applications across bakery, dairy, beverages, and other processed foods. They offer stability under diverse processing conditions, which ensures reliable performance during industrial-scale operations. Additionally, microbial sources are considered more sustainable and cost-effective, supporting their widespread adoption in the region. The scalability of microbial enzyme production further reinforces their dominance, making them a cornerstone of the South America food enzymes market.

Plant-derived enzymes, on the other hand, are the fastest-growing segment, projected to expand at a CAGR of 7.61% through 2031. This rapid growth is driven by increasing consumer preference for natural and plant-based ingredients, especially in clean-label and specialty food products. Plant-derived enzymes are widely used in fruit and vegetable processing, bakery, and dietary applications, where they improve flavor, texture, and nutritional quality. Technological advancements have enhanced their stability and functional efficiency, boosting adoption among manufacturers. Rising awareness of vegan and vegetarian diets is also contributing to higher demand for plant-based enzyme solutions.

By Application: Dairy Outpaces Bakery as Premiumization Accelerates

The bakery and confectionery segment dominated the South America food enzymes market in 2025, accounting for the largest revenue share of 24.73%. This strong position is driven by the widespread use of enzymes such as amylases, proteases, and lipases to improve dough quality, texture, and shelf life. Enzymes help enhance volume, softness, and flavor, which are critical factors for bakery and confectionery products. The high consumption of bread, cakes, and pastries across the region supports consistent demand for enzyme solutions. Additionally, manufacturers prefer enzymatic solutions for clean-label formulations, reducing the need for chemical additives. The combination of technological efficiency and consumer demand has solidified bakery and confectionery as the leading application segment.

In contrast, the dairy and desserts segment is the fastest-growing application, projected to expand at a CAGR of 8.07% through 2031. This rapid growth is fueled by increasing demand for cheese, yogurt, flavored desserts, and other value-added dairy products. Enzymes such as lipases and proteases play a key role in improving flavor, texture, and yield in these applications. Rising consumer preference for functional and specialty dairy products, including lactose-free and protein-enriched options, is boosting enzyme adoption. Technological advancements in enzyme formulations have enhanced efficiency and stability, further supporting growth in this segment. As the region’s dairy industry continues to expand and innovate, the demand for enzymatic solutions in dairy and desserts is expected to grow steadily in the coming years.

Geography Analysis

Brazil dominated the South America food enzymes market in 2025, commanding the largest revenue share of 42.93%. The country’s leading position is supported by its well-established food processing industry, including strong bakery, dairy, and beverage sectors. Brazil benefits from a large consumer base and growing demand for processed and convenience foods, which drives enzyme adoption across multiple applications. Technological advancements and investments in modern food manufacturing facilities have further strengthened the market presence of food enzymes in the country. Additionally, the availability of raw materials and supportive regulatory framework have contributed to Brazil’s dominance. With its combination of production capacity, consumer demand, and industrial infrastructure, Brazil remains the key revenue contributor in the region.

Argentina, on the other hand, is the fastest-growing market, projected to expand at a CAGR of 8.01% through 2031. This growth is driven by increasing investments in the food and beverage industry, particularly in dairy, bakery, and confectionery production. Rising consumer awareness of functional foods and clean-label ingredients is boosting enzyme adoption across various applications. Technological advancements and improved production processes are enabling local manufacturers to incorporate enzymes more efficiently. The expanding export-oriented food sector is also contributing to the increasing demand for high-quality enzymatic solutions. As Argentina continues to modernize its food processing infrastructure, it is expected to witness significant market expansion over the coming years.

Chile, Colombia and Peru represent emerging markets within the South America food enzymes industry, showing steady growth potential. Both countries are investing in the modernization of their food processing sectors, particularly in dairy, fruit processing, and bakery applications. Consumer demand for processed and value-added foods, along with increasing awareness of functional ingredients, is gradually driving enzyme adoption. While the market size in these countries is smaller compared to Brazil and Argentina, opportunities exist for new product launches and technological innovations. Supportive trade policies and growing export-oriented production are likely to enhance the market landscape in Chile and Peru.

Competitive Landscape

The South America food enzymes market exhibits moderate consolidation, with a few key global and regional players holding a significant share of the market. Leading companies such as Creative Enzymes, International Flavors & Fragrances, Inc., Ajinomoto Group, Kerry Group plc, and Associated British Foods plc dominate the landscape, leveraging their strong technological capabilities, wide product portfolios, and extensive distribution networks. These players focus on strategic partnerships, mergers, and acquisitions to expand their market reach and strengthen their foothold in high-demand segments such as dairy, bakery, and beverages. Their established brand reputation and technical expertise give them a competitive edge over smaller local manufacturers, allowing them to secure long-term contracts with food processing companies across the region.

Mid-sized and local enzyme manufacturers in South America also play a key role in the market, although they face intense competition from global leaders. These companies often specialize in niche applications or specific enzyme types, such as plant-derived or liquid enzymes, to differentiate themselves in the market. By focusing on customized solutions, cost-effective products, and local distribution channels, they can capture demand from small and medium-sized food processors. Some local players also engage in collaborations with global companies to access advanced technology and expand their product offerings.

The competitive landscape is further shaped by factors such as regulatory compliance, technological advancements, and the growing demand for sustainable and natural enzyme solutions. Companies that can efficiently navigate the complex regulatory environment in South American countries gain an advantage in market penetration. Innovation in enzyme formulation, stability, and application versatility allows players to meet the increasing requirements of modern food processing, including clean-label and functional products. Market participants are also focusing on sustainability by developing enzymes that reduce energy consumption and minimize waste during food production.

South America Food Enzymes Industry Leaders

Creative Enzymes

International Flavors & Fragrances, Inc.

Kerry Group plc

Associated British Foods plc

Ajinomoto Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: IFF introduced TEXSTAR, an enzymatic solution specifically designed for dairy and plant-based fresh-fermented products. This innovative system actively converts sucrose into poly- and oligosaccharides during the fermentation process. By doing so, it creates creamy textures with improved smoothness, eliminating the need for added stabilizers and enhancing product quality.

- June 2024: AAB Enzymes, a subsidiary of ABF Ingredients, launched Veron HPP and Veron S50 protease enzymes to enhance biscuit and cracker production. These enzymes actively improve dough extensibility, significantly reduce resting time, and effectively prevent issues such as cracking and uneven browning. Veron HPP delivers smoother dough with fewer defects, while Veron S50 provides a cleaner-label alternative to sodium metabisulfite. Additionally, Veron S50 enables manufacturers to use lower-cost flours, helping to reduce overall production expenses without compromising quality.

- May 2024: Biocatalysts Ltd introduced two protease enzymes, Promod 327L and Promod 295L, to enhance the efficiency of collagen hydrolysis. These enzymes actively break down extracted collagen into low molecular weight, neutral-tasting collagen peptides, offering improved functionality and versatility for various applications.

South America Food Enzymes Market Report Scope

Food enzymes are naturally occurring or manufactured proteins that act as biological catalysts to accelerate chemical reactions in food processing. Food enzymes are widely used in industries such as bakery, dairy, beverages, and meat processing to improve efficiency, enhance taste and texture, extend shelf life, and support clean-label or functional food development. The South America food enzymes market is segmented by enyzme type, form, source, application and geography. Based on enyzme type, the market is segmented into carbohydrase, protease, lipase, and others. Based on form, the market is segmented into powder and liquid. Based on source, the market is segmented by plant, microbial and animal-based. Based on the application, the market is divided into the bakery, confectionery, dairy, and desserts, meat, beverages, meat and meat products, soups, sauces, and dressings and other applications. The study also covers the regional level analysis of the major countries, which includes Brazil, Columbia, and rest of South America. The market sizing has been done in value terms in USD for all the above mentioned segments.

By Enzyme Type

| Carbohydrase | Amylases |

| Pectinases | |

| Cellulases | |

| Other | |

| Protease | |

| Lipase | |

| Other Enzymes |

By Form

| Powder |

| Liquid |

By Source

| Plant |

| Microbial |

| Animal |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

By Geography

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Enzyme Type | Carbohydrase | Amylases |

| Pectinases | ||

| Cellulases | ||

| Other | ||

| Protease | ||

| Lipase | ||

| Other Enzymes | ||

| By Form | Powder | |

| Liquid | ||

| By Source | Plant | |

| Microbial | ||

| Animal | ||

| By Application | Bakery and Confectionery | |

| Dairy and Desserts | ||

| Beverages | ||

| Meat and Meat Products | ||

| Soups, Sauces, and Dressings | ||

| Other Applications | ||

| By Geography | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America |

Key Questions Answered in the Report

What CAGR is forecast for the South America food enzymes market between 2026 and 2031?

The market is projected to register a 7.14% CAGR during 2026-2031.

Which enzyme type is expanding the fastest in South America?

Lipase shows the quickest growth at a 7.76% CAGR as dairy processors target trans-fat-free products.

Why do processors favor powder formulations?

Powders tolerate ambient storage, skip cold-chain fees, and fit manual dosing in small plants, which kept them at 67.38% share in 2025.

Which country leads regional demand?

Brazil accounted for 42.93% of revenue in 2025 due to its large bakery, dairy, and beverage industries.

How do immobilized enzyme systems benefit dairy plants?

They allow lactase reuse across many batches, cutting enzyme costs by as much as 60%.

Page last updated on: