South America Fluoropolymer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

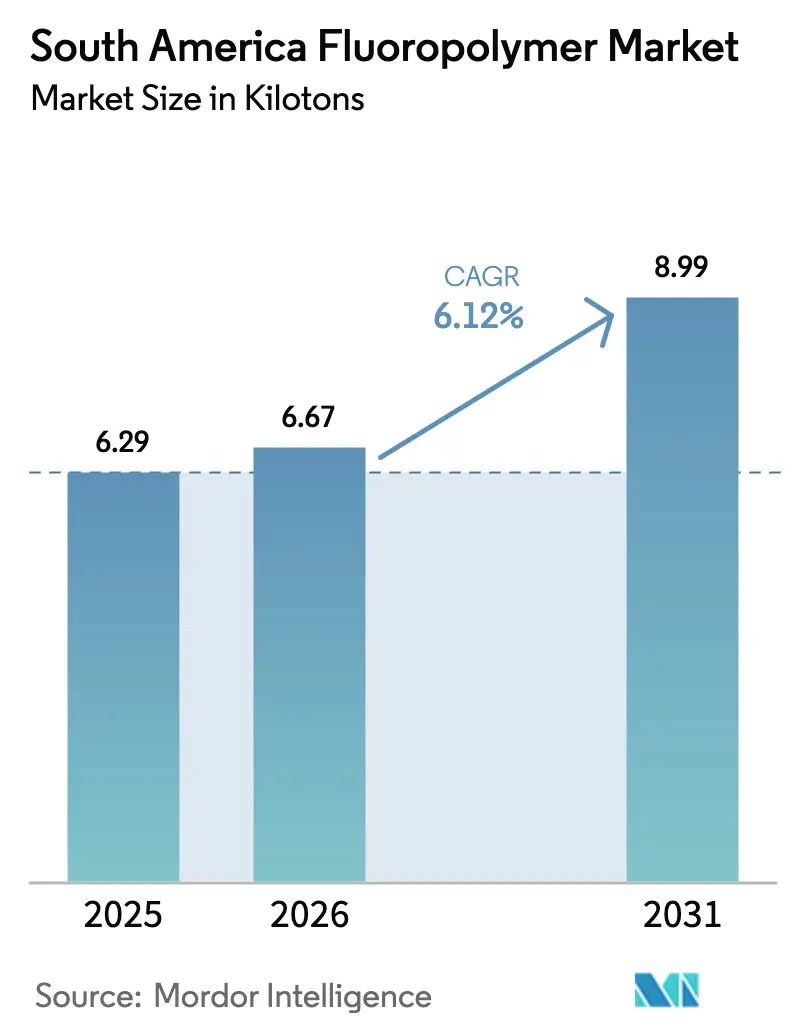

| Base Year Market Size (2025) | 6.29 kilotons |

| Market Volume (2026) | 6.67 kilotons |

| Market Volume (2031) | 8.99 kilotons |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

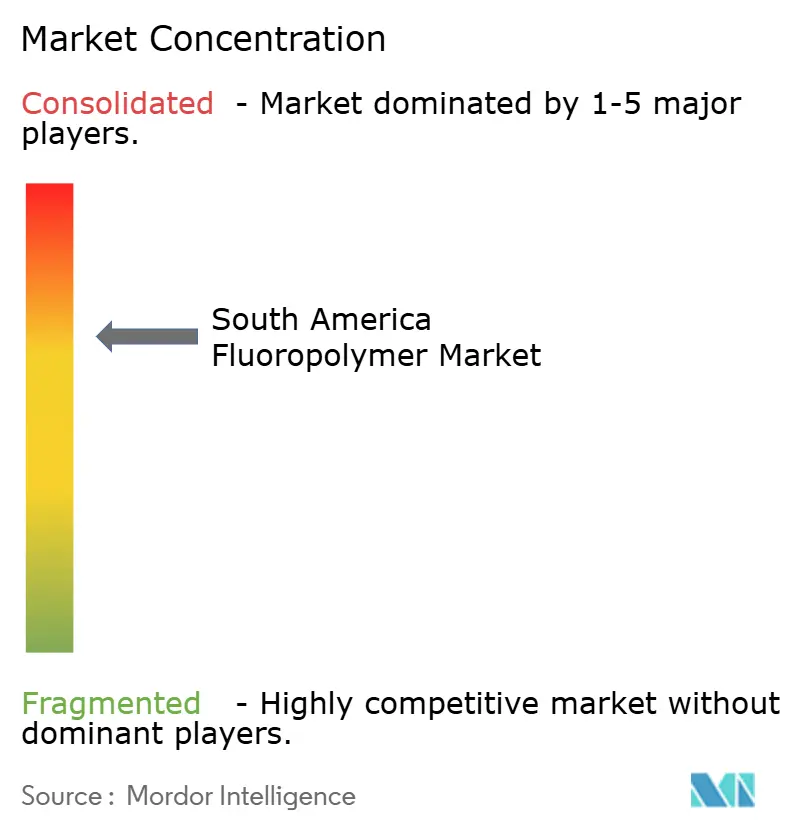

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Fluoropolymer Market Analysis by Mordor Intelligence

South America Fluoropolymer Market size in 2026 is estimated at 6.67 kilotons, growing from 2025 value of 6.29 kilotons with 2031 projections showing 8.99 kilotons, growing at 6.12% CAGR over 2026-2031. Rapid automotive lightweighting programs, accelerating renewable energy projects, and sustained minerals processing activities are reinforcing long-term demand for high-performance resins that withstand extreme heat and corrosive media. Brazil and Argentina are shaping product-mix evolution as electric-vehicle platforms, shale-gas processing, and photovoltaic installations favor polyvinylidene fluoride (PVDF) for battery separators and backsheets, while mining and petrochemicals preserve polytetrafluoroethylene (PTFE) dominance. At the same time, supply-chain localization and vertical integration moves—such as Orbia’s backward integration into fluorspar and Bermo Válvulas’ BRL 60 million plant expansion—are buffering import exposure and reducing lead times. Overall, the South American fluoropolymer market continues to benefit from the irreplaceable material capabilities in chemically aggressive and high-temperature environments, cementing its resilience against raw-material volatility and regulatory headwinds.

Key Report Takeaways

- By sub-resin type, PTFE led with 56.92% of the South America fluoropolymer market share in 2025, whereas PVDF is projected to post the fastest 6.77% CAGR through 2031.

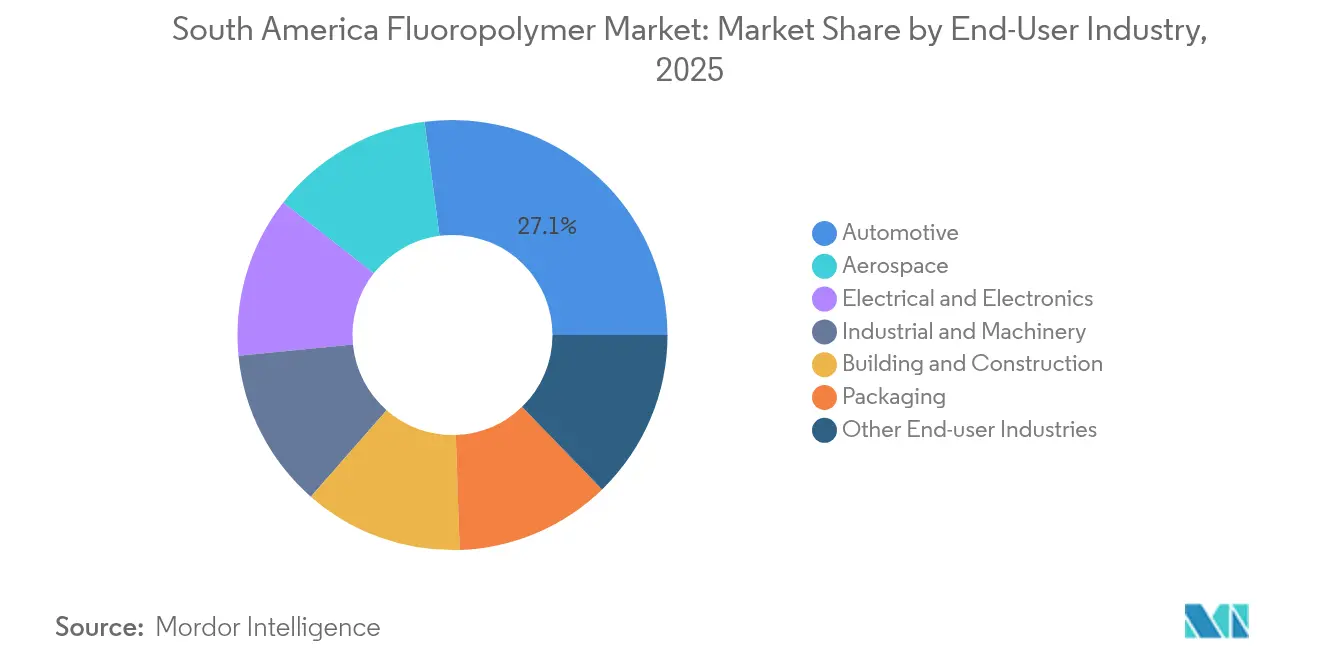

- By end-user industry, automotive captured 27.08% of the South America fluoropolymer market size in 2025, while aerospace applications are expanding at a 6.71% CAGR to 2031.

- By geography, Brazil commanded 63.55% of South America fluoropolymer market share in 2025; Argentina is on track for the quickest 8.29% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Fluoropolymer Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrical and electronics demand for high-temperature cable insulation | +1.8% | Brazil core, Argentina secondary | Medium term (2–4 years) |

| Automotive lightweighting programs | +1.5% | Brazil, Argentina | Short term (≤2 years) |

| Corrosion-resistant linings capex upcycle | +1.2% | Regional mining and petrochemicals | Long term (≥4 years) |

| Solar-PV backsheets pivot to PVDF | +0.9% | Brazil renewable zones | Medium term (2–4 years) |

| Li-ion battery separator build-outs | +0.7% | Regional battery hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expanding Electrical and Electronics Demand for High-Temperature Wire and Cable Insulation

Grid modernization programs and renewable generation tie-ins are increasing the demand for fluoropolymer-insulated cables that remain functional at temperatures above 200 °C and resist exposure to hydrocarbons. Chilean copper mines and Brazilian iron-ore facilities specify PTFE, ETFE, and PFA jacketing sourced from AGC Chemicals’ local portfolio, while Tramar’s Brazilian plant shortens delivery cycles and trims import costs. Wind-farm expansions in Patagonia and solar arrays in Brazil’s northeast demand UV-stable, salt-spray-resistant jacketing that conventional polymers cannot match. Coupled with substation retrofits under Brazil’s PROINFRA program, these factors secure a multi-year pull-through for specialty resins across the South American fluoropolymer market.

Automotive Lightweighting Initiatives Boosting PVDF and PTFE Usage

Vehicle makers in Brazil’s São Paulo and Minas Gerais corridors are substituting metal and engineering plastics with fluoropolymer components to meet CO₂ targets and extend electric-vehicle (EV) range. PVDF’s chemical inertness under high-voltage conditions makes it the go-to binder for Li-ion battery housings, while PTFE’s self-lubricating properties reduce friction losses in dynamic seals, improving drivetrain efficiency. Cross-border trade data show that Brazilian plastic packaging exports to Argentina are growing, mirroring the increasing intra-regional collaboration on lightweight parts.

Chemical-Processing Corrosion-Resistant Linings Investment Upcycle

As ore grades decline, miners in Peru and Chile increase the concentration of acid, prompting a shift from expensive nickel-based alloys to powder-coated PVDF linings. Arkema testing demonstrates the integrity of PVDF in sulfuric acid up to 98% concentration, extending equipment life and reducing total ownership costs[1]Arkema, “Preventing Corrosion with PVDF,” hpp.arkema.com . Petrobras’ approval of ECTFE formulations has accelerated adoption across refineries and petrochemical sites, reinforcing steady resin consumption even during commodity-price swings.

Solar PV Backsheets Shift to PVDF in Brazil

Brazil’s solar nameplate additions exceeded 12 GW in 2024, sparking a surge in PVDF backsheets that deliver 25-year durability under tropical UV and humidity. Domestic module assemblers are increasingly sourcing PVDF film locally to hedge currency volatility, catalyzing investment in extrusion and coating lines. The shift supports incremental volume growth for PVDF grades within the South America fluoropolymer market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluorspar price volatility | -0.8% | Global supply chain affecting all regions | Short term (≤ 2 years) |

| Tightening global PFAS regulations | -0.6% | Export-dependent applications | Medium term (2-4 years) |

| PTFE phase-out in food-contact uses | -0.4% | Brazil and Argentina food processing sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluorspar Price Volatility

Limited domestic ore output forces manufacturers to import feedstock, exposing them to fluctuations in spot prices. Orbia’s Moroccan mine expansion illustrates efforts to insulate production economics; however, fluctuating freight rates and currency movements still create margin risk for converters throughout the South American fluoropolymer industry.

Tightening Global PFAS Regulations

New PFAS proposals in the EU and U.S. widen compliance scope to include processing aids, compelling regional exporters to certify formulations and invest in trace-analysis. SEMI guidance warns that even non-fluorinated backbones may fall under scrutiny if PFAS additives are present, adding documentation burdens and potential reformulation costs for flexible-packaging and consumer-goods suppliers[2]SEMI, “PFAS Additives & Non-PFAS Polymers,” semi.org .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Resin Type: PTFE Dominance Faces PVDF Challenge

PTFE maintained a 56.92% share of the South America fluoropolymer market in 2025, owing to its unrivaled chemical resistance, which mining, oil, and gas processors rely on for valve seats and gasket sheets. The segment captured the largest slice of the South America fluoropolymer market size, yet its volume growth is moderating as commodity PTFE imports face antidumping probes and buyers shift toward value-added grades. In contrast, PVDF volumes are increasing at a 6.77% CAGR due to energy-transition demand, propelling its share gain trajectory across separator films and photovoltaic backsheets.

PVDF also benefits from localization moves such as Syensqo’s new PVDF facility in Georgia, which curtails lead times for South American battery assemblers. ETFE and FEP occupy the communication-cable and aerospace niches, leveraging their dielectric properties, while PVF remains tied to architectural films. The interplay between PTFE’s entrenched base and PVDF’s momentum will shape the competitive positioning in the South American fluoropolymer market through 2031.

By End-User Industry: Automotive Leadership Challenged by Aerospace Growth

Automotive captured 27.08% of the South America fluoropolymer market share in 2025, reflecting the region’s vehicle-manufacturing depth and rising EV output. Sealing systems, battery casings, and fuel-line components constitute key pull-through channels that collectively anchor baseline demand. The South America fluoropolymer market size linked to aerospace is smaller today but expanding at a 6.71% CAGR as carriers renew fleets with composite-rich aircraft and defense ministries specify high-temperature wire insulation.

Building and construction uptake remains steady for weather-resistant PVDF coatings on metal panels, while electrical and electronics orders cater to grid refurbishment and semiconductor tooling. Industrial machinery—especially pumps, agitators, and pipework in mineral processing—provides a reliable replacement cycle, whereas packaging applications are gradually integrating fluorinated barrier films for shelf-life extension. Regulatory certifications such as FSSC 22000 and ISO 9001 continue to steer converters toward high-purity fluoropolymer grades.

Geography Analysis

Brazil’s 63.55% share of the South America fluoropolymer market in 2025 stems from its diversified industrial base, integrated access to petrochemical feedstock, and robust renewable-electricity mix that reduces polymer-processing emissions. Domestic producers like Tramar and Carbofluor shorten supply chains by fabricating specialty cables and PTFE seals locally, while Braskem’s gas-price renegotiation with Petrobras underpins potential resin-capacity expansion. Solar installations in Ceará and Piauí propel PVDF backsheet demand, while EV programs across São Paulo’s auto cluster drive battery-grade PVDF offtake, reinforcing Brazil’s anchor role in the South American fluoropolymer market.

Argentina, posting the quickest 8.29% CAGR through 2031, is leveraging Vaca Muerta’s ethane-rich gas stream to attract downstream investment in polymers. Corrosion-resistant PTFE linings for shale-gas separators and PVDF seals in cryogenic pumps are registering double-digit volume growth. Import-substitution policies under SIRA have nudged local converters to source resins from intra-bloc suppliers, while cross-border trade with Brazil brings technical support and machinery upgrades. As gigafactory and wind-turbine projects migrate to Córdoba and Santa Fe, demand for PVDF and ETFE will outpace broader industry averages.

The rest of South America—chiefly Chile, Peru, and Colombia—adds a stable yet smaller demand slice anchored in mining and infrastructure. Chile’s acidic leaching circuits employ PVDF and ECTFE pipework, whereas Peru’s copper-moly concentrators adopt PTFE pump parts to curb downtime. Colombian offshore gas expansions require FEP wire insulation and PVDF coatings for salinity resistance. Geographic fragmentation and varied standards adoption encourage distributors with application-engineering capability, especially for projects in remote Andean and Amazonian locales.

Competitive Landscape

Global majors wield scale economies, broad resin portfolios, and integrated research and development pipelines, enabling them to service multi-country contracts and co-develop specialty grades with OEMs. Regional challengers leverage their proximity to customers and the ability to customize valve assemblies to the same high German quality standards. Competitive differentiation increasingly hinges on stewardship credentials as PFAS scrutiny intensifies. Suppliers investing in surfactant-free polymerization gain favor with electronics and medical customers whose compliance thresholds are tightening.

South America Fluoropolymer Industry Leaders

The Chemours Company

Syensqo

3M

Arkema

AGC Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Arkema announced a 15% PVDF capacity increase at Calvert City, Kentucky, supported by USD 20 million investment and a 2026 start-up, to serve battery and semiconductor demand in South America.

- August 2024: AGC introduced a surfactant-free fluoropolymer process that eliminates fluorinated by-products while preserving key performance attributes.

South America Fluoropolymer Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. Ethylenetetrafluoroethylene (ETFE), Fluorinated Ethylene-propylene (FEP), Polytetrafluoroethylene (PTFE), Polyvinylfluoride (PVF), Polyvinylidene Fluoride (PVDF) are covered as segments by Sub Resin Type. Argentina, Brazil are covered as segments by Country.| Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) |

| Polytetrafluoroethylene (PTFE) |

| Polyvinyl Fluoride (PVF) |

| Polyvinylidene Fluoride (PVDF) |

| Other Sub-Resin Types |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| Argentina |

| Brazil |

| Rest of South America |

| By Sub-Resin Type | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinyl Fluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub-Resin Types | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | Argentina |

| Brazil | |

| Rest of South America |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the fluoropolymers market.

- Resin - Under the scope of the study, virgin fluoropolymer resins like Polytetrafluoroethylene, Polyvinylidene Fluoride, Polyvinylfluoride, Fluorinated Ethylene-propylene, Ethylenetetrafluoroethylene, etc. in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms