Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

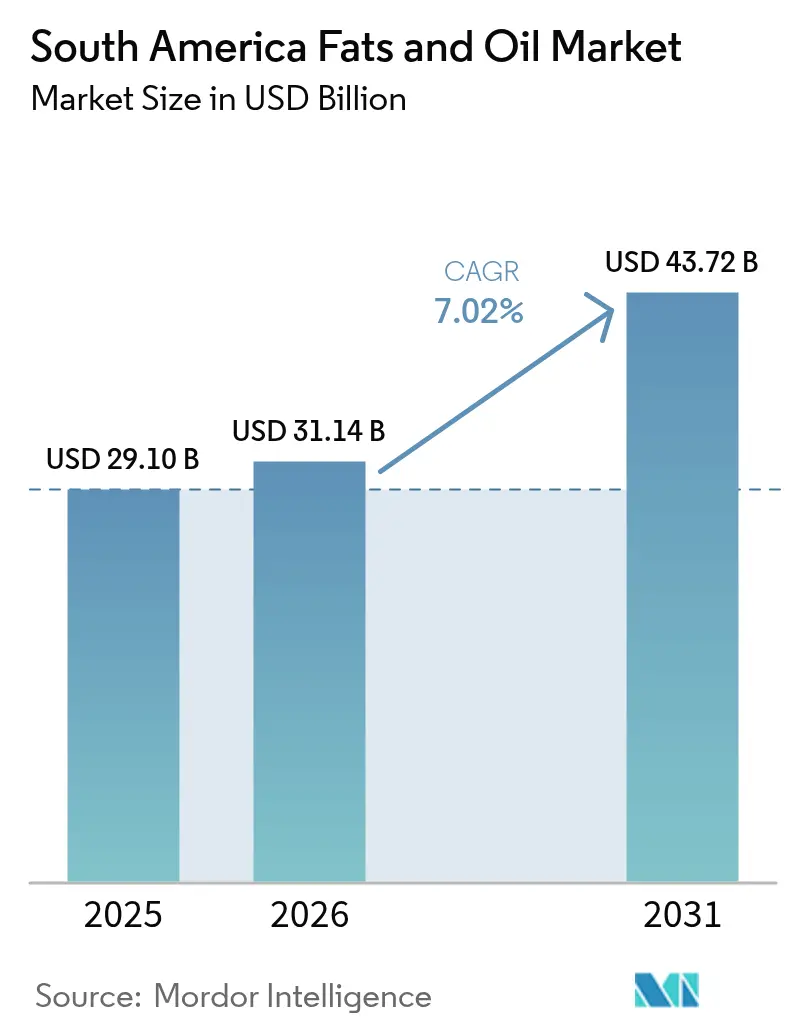

| Base Year Market Size (2025) | USD 29.10 Billion |

| Market Size (2026) | USD 31.14 Billion |

| Market Size (2031) | USD 43.72 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Fats and Oils Market Analysis by Mordor Intelligence

South America fats and oils market size in 2026 is estimated at USD 31.14 billion, growing from 2025 value of USD 29.10 billion with 2031 projections showing USD 43.72 billion, growing at 7.02% CAGR over 2026-2031. Strong biofuel mandates, expanding soybean-crush capacity, and rising demand for higher-value specialty fats collectively underpin this growth trajectory. Policymakers are steering domestic feedstock toward biodiesel plants, tightening exportable supplies and elevating regional processing margins. At the same time, specialty bakery and confectionery manufacturers are accelerating the shift to trans-fat-free formulations, supporting premium pricing for tailored fat systems. Investments in traceable, deforestation-free supply chains are now table stakes for large traders seeking continued access to North American and European customers. Competitive intensity is high, yet niche processors focused on sustainability and flexible feedstock technologies are carving defensible positions across the South America fats and oils market

Key Report Takeaways

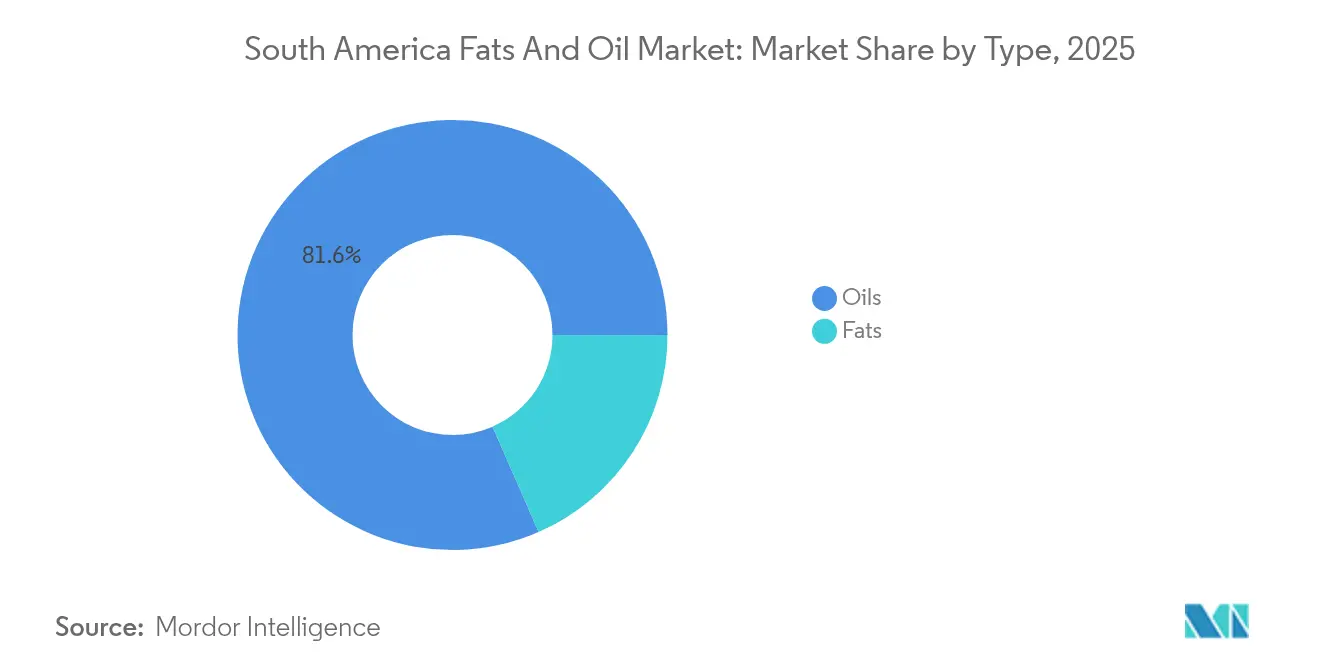

- By type, oils led with 81.56% of South America fats and oils market share in 2025, while fats are projected to expand at a 7.61% CAGR through 2031.

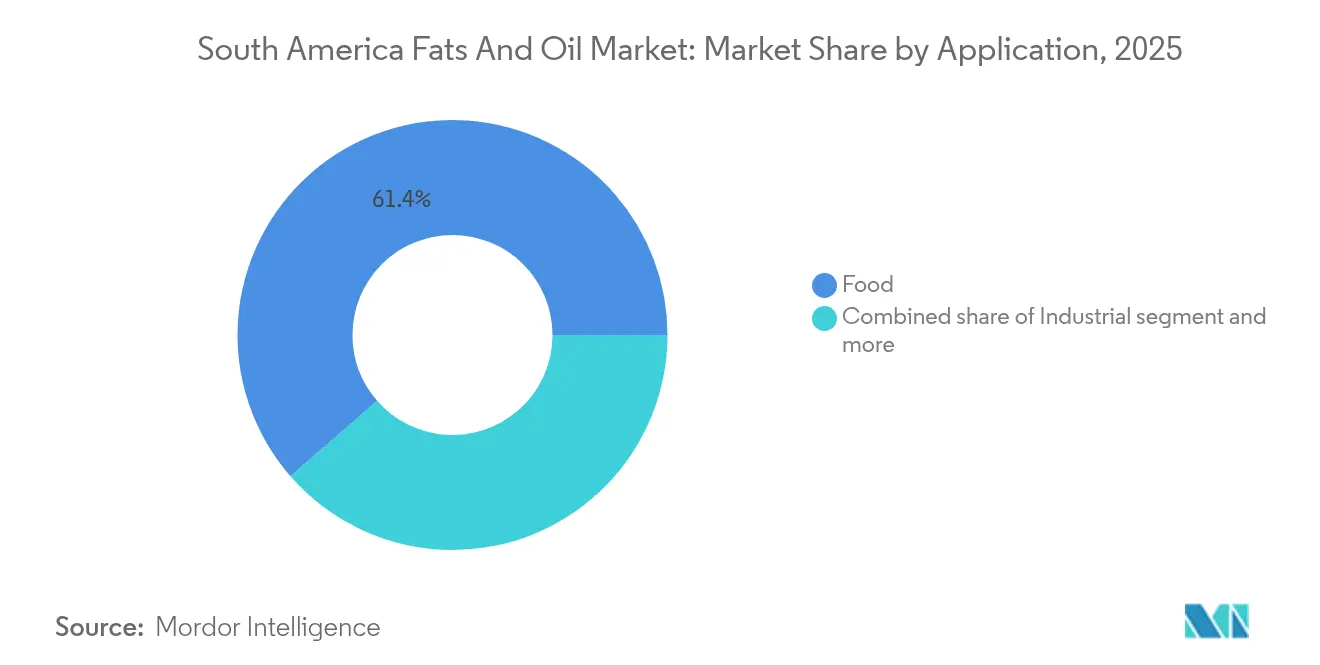

- By application, the food segment commanded 61.42% of 2025 revenue; the industrial segment is advancing at a 9.41% CAGR during 2026-2031.

- By geography, Brazil accounted for 53.88% of 2025 revenue, whereas Argentina is poised to grow the fastest at an 8.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of South America Fats and Oils Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for biodiesel feedstock | +1.2% | Brazil dominant, Argentina accelerating | Medium term (2-4 years) |

| Processed food and bakery products accelerate demand | +1.8% | Regional, with Brazil and Argentina leading | Long term (≥ 4 years) |

| Expansion of soybean-crush capacity | +1.5% | Brazil core, spillover to Paraguay and Bolivia | Medium term (2-4 years) |

| Widespread adoption of high-oleic oil in food processing | +0.9% | Regional, concentrated in urban centers | Long term (≥ 4 years) |

| Government-backed sustainable initiatives | +0.8% | Brazil and Colombia primary focus | Short term (≤ 2 years) |

| Surge in vegan and health-conscious lifestyle | +0.6% | Brazil metropolitan areas, Chile emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Biodiesel Feedstock

Brazil's biodiesel sector has fundamentally transformed traditional export-oriented oil markets into domestic industrial consumption markets. The country's industrial soybean oil consumption has increased by more than 100% in the past decade, with soybean oil making up 69% of biodiesel feedstock. This significant shift in domestic demand limits exportable supplies, despite projected soybean oil production reaching 12 million metric tons in 2024/25, restricting exports to 1.3 million tons. Argentina's Liga Bioenergetica legislation proposes increasing biodiesel mandates to B15 by January 2027, which may require expanded crushing capacity and feedstock diversification beyond soybean oil[1]Source: United States Department of Agriculture, "Report Name: Biofuels Annual," fas.usda.gov. The implementation of these mandates could reshape the regional supply chain dynamics. The broader regional shift toward higher blending mandates generates consistent industrial demand, resulting in premium pricing for vegetable oils and reduced export market volatility. This transformation indicates a long-term structural change in South American vegetable oil markets, with implications for global trade patterns and price dynamics.

Processed Food and Bakery Products Accelerate Demand

The growth of the processed food industry drives demand for specialized fat formulations that command premium pricing over commodity oils. The increasing complexity of processed food products requires tailored fat solutions with specific melting points, crystallization behaviors, and functional properties. Specialty fats for confectionery applications, particularly cocoa butter equivalents (CBE), are gaining importance as manufacturers seek cost-effective alternatives to cocoa butter while maintaining product quality. The use of high-oleic sunflower oil in sugar coating applications demonstrates how food processors are replacing palm oil with regional alternatives that offer better oxidative stability and clean-label attributes[2]Source: Cargill, "Sustainable Soy," cargill.com. The demand for premium bakery fats reflects consumer preference for healthier options and artisanal quality, with manufacturers adopting trans-fat-free formulations to meet regulatory requirements. This shift has led to the development of innovative fat blends that combine functionality with nutritional benefits, supporting the creation of premium baked goods that align with modern dietary preferences.

Expansion of Soybean-Crush Capacity

Soybean crushing capacity expansion is driven by rising biodiesel mandates and evolving export demand patterns, which fundamentally reshape regional oil supply dynamics. This expansion generates a significant multiplier effect, as increased crushing operations yield abundant soybean meal supplies (maintaining a consistent 4:1 meal-to-oil ratio), which can exert downward pressure on meal prices and necessitate the development of new export markets to absorb excess production. Export flows face substantial constraints from infrastructure limitations and inadequate investment in storage and transportation facilities, making robust domestic demand increasingly vital for industry sustainability. The severe 2022/23 drought in Argentina, which significantly reduced crushing capacity and operational efficiency, clearly illustrates how weather-related disruptions create temporary export opportunities for other producers while emphasizing the strategic importance of maintaining distributed processing capacity across different regions[3]Source: United States Department of Agriculture, "U.S. Renewable Diesel Production Growth Drastically Impacts Global Feedstock Trade," fas.usda.gov.

Widespread Adoption of High-Oleic Oil in Food Processing

High-oleic oil varieties address health concerns and functional requirements in food processing applications. Cargill's Clear Valley® portfolio shows how high-oleic sunflower oil functions as a palm oil alternative in sugar coating applications, providing oxidative stability without trans-fat formation during processing. The use of these oils has expanded into specialty segments where oxidative stability and clean-label attributes command higher prices. Brazilian specialty oils, including açaí, passion fruit seed, pequi, and guava oils, are emerging in premium food applications due to consumer interest in indigenous and functional ingredients. Food processors select high-oleic varieties to remove hydrogenation processes and meet trans-fat regulations while preserving product shelf life and sensory qualities. This shift requires seed development programs and farmer training initiatives, creating opportunities for agricultural technology companies and specialty oil processors. High-oleic adoption enhances export competitiveness as international buyers seek healthier oil profiles that meet nutritional guidelines and consumer preferences.

Restraints Impact Analysis of South America Fats and Oils Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns regarding saturated trans fats | -0.7% | Regional, with Colombia and Argentina leading regulatory action | Short term (≤ 2 years) |

| Commodity-price volatility in veg-oil complex | -0.5% | Global impact, concentrated in export-dependent regions | Short term (≤ 2 years) |

| Northern-Brazil port and storage bottlenecks | -0.4% | Brazil concentrated, spillover to Paraguay and Bolivia | Medium term (2-4 years) |

| Reformulation costs from trans-fat phase-outs | -0.3% | Regional, affecting food processors and manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Regarding Saturated Trans Fats

Regulatory momentum against trans fats creates reformulation pressures that increase costs while potentially constraining certain traditional fat applications. Colombia implemented comprehensive trans fat regulations limiting industrial trans fats to 2g per 100g and banning partially hydrogenated oils (PHO), forcing manufacturers to reformulate products using alternative fat systems[4]Source: Food Compliance International, "Colombia Drafts New Technical Regulation on Trans Fats," foodcomplianceinternational.com. Argentina's ANMAT updated food labeling requirements to enhance trans fat disclosure, while Venezuela implemented front-of-package warning labels that specifically highlight trans fat content above regulatory thresholds. The Pan American Health Organization (PAHO) trans fat elimination initiative creates region-wide pressure for policy harmonization, potentially accelerating regulatory timelines across smaller markets. Reformulation costs include ingredient substitution, process optimization, shelf-life testing, and consumer acceptance studies, creating barriers for smaller manufacturers while benefiting suppliers of trans-fat-free alternatives. The regulatory trend favors liquid oils and specialty fats that maintain functionality without hydrogenation, creating market opportunities for high-oleic varieties and structured fat systems.

Commodity-Price Volatility in Veg-Oil Complex

Price volatility in vegetable oil markets creates significant operational challenges across the region. Global vegetable oil prices increased substantially in early 2025, driven by reduced soybean oil exports from Brazil and decreased palm oil production from Southeast Asian producers. This demonstrated how regional supply limitations can affect global prices. The Argentinian biodiesel industry faces specific challenges, as the Secretariat of Energy's monthly purchase price regulations often do not keep pace with inflation, causing financial difficulties for producers when raw material costs increase rapidly. The situation is further complicated by currency fluctuations, as regional producers must manage both commodity price changes and exchange rate variations in export markets. This volatility impacts long-term contracting and investment planning, with processors unable to commit to fixed-price agreements due to unpredictable input costs. Supply disruptions from weather events, such as Argentina's 2022/23 drought affecting soybean crushing operations, can cause rapid price increases that affect established trade relationships and require buyers to identify new suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

South America Fats and Oils Market Segment Analysis

By Type:

Oils Dominate While Fats AccelerateThe oils segment holds 81.56% market share in 2025, primarily due to soybean oil's established position in biodiesel production and food processing across South America. The fats segment is growing at a higher rate of 7.61% CAGR through 2031, supported by increasing demand in confectionery and bakery applications that require specific functional properties. Soybean oil remains the dominant oil type due to substantial regional production capacity and well-developed processing infrastructure. Coconut oil occupies premium market segments, particularly in health-focused consumer products and specialized food applications. Sunflower oil benefits from Argentina's production capabilities and the availability of high-oleic variants that provide specific advantages in food processing.

The fats segment includes butter, tallow, lard, and specialty fats. Animal-derived fats are increasingly used in biodiesel production as manufacturers diversify their feedstock options beyond vegetable oils. Specialty fats used in confectionery command higher prices due to their specific functional properties in chocolate and bakery products. Manufacturers are developing trans-fat-free formulations to meet health regulations. The segment's growth is supported by advances in enzymatic processing technology, which allows for the use of diverse raw materials, including high free fatty acid oils and waste-derived materials.

By Application:

Food Segment Leads Industrial GrowthFood applications hold a 61.42% market share in 2025, spanning confectionery, bakery, dairy products, margarine, spreads, and other processed food categories. The industrial segment grows at a 9.41% CAGR, driven by biodiesel production and renewable diesel feedstock demand. In food applications, confectionery and bakery segments achieve premium pricing through specialty fat formulations that provide specific functionality without trans-fat content. Dairy product applications expand due to increasing consumer demand for premium dairy items and plant-based alternatives requiring advanced fat systems for texture and mouthfeel. While margarine and spreads face challenges from health-conscious consumer preferences, they maintain volume through healthier fat profiles and functional ingredients.

Animal feed applications support the region's livestock sector, with Brazil's beef and pork exports driving demand for feed-grade fats and oils that enhance energy density and palatability. The segment benefits from vertical integration, allowing crushing operations to optimize product distribution between food-grade oils, industrial applications, and feed-grade materials based on market prices. RSPO and similar sustainability framework requirements increasingly affect industrial application sourcing decisions, especially for export-oriented products.

Geography Analysis

Brazil Fats and Oils Market

Brazil maintains its commanding position in the South American soybean market, holding 53.88% market share in 2025. This dominance stems from its status as the world's largest soybean producer and significant biodiesel consumer. The country's extensive crushing infrastructure, combined with farmer-friendly agricultural policies, enables efficient processing and distribution. Additionally, Brazil's well-developed transportation networks and port facilities facilitate both domestic distribution and international exports, further strengthening its market leadership.

Argentina Fats and Oils Market

Argentina emerges as the region's fastest-growing market, projecting an 8.07% CAGR through 2031. This growth trajectory is primarily driven by proposed biofuel legislation that aims to increase biodiesel mandates to B15 by 2027. The country's planned reforms to deregulate pricing mechanisms, which currently restrict industry profitability, are expected to attract new investments and expand processing capacity. Argentina's established agricultural sector and experienced farming community provide a strong foundation for this anticipated growth, while its strategic location offers excellent access to major shipping routes.

Broader South America Fats and Oils Market

Other South American countries contribute significantly to the regional market dynamics. Colombia leverages its substantial palm oil production capacity and progressive government sustainability initiatives, including deforestation-free sourcing protocols, to attract environmentally conscious buyers. Peru, despite its smaller market presence, demonstrates growth potential through expanding food processing operations and increasing urban consumer purchasing power. The Rest of South America, encompassing Paraguay, Bolivia, and Uruguay, focuses on agricultural expansion and processing capacity development. Paraguay's strategic location provides logistical advantages for serving Brazilian and Argentine markets, while Bolivia's agricultural potential remains constrained by infrastructure limitations. Regional integration is further enhanced through trade agreements and MERCOSUR harmonization efforts, which facilitate cross-border commerce and regulatory alignment across national boundaries.

Competitive Landscape

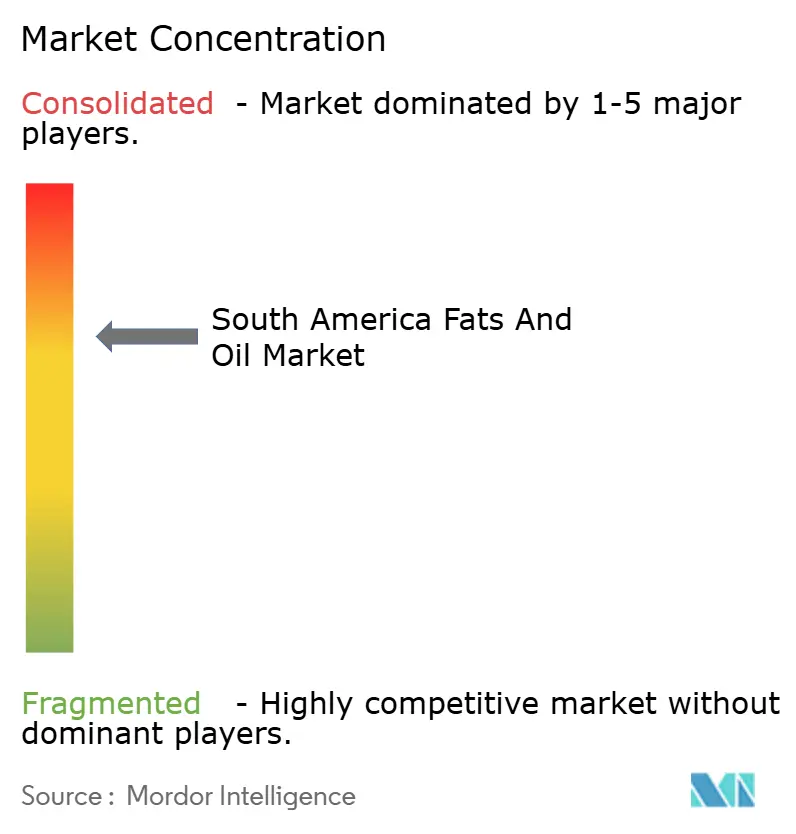

The South American fats and oils market demonstrates moderate concentration, with a market concentration ratio of 7 out of 10. The market landscape is primarily controlled by the ABCD traders (ADM, Bunge, Cargill, Louis Dreyfus), who have established strong vertical integration across the supply chain. Asian companies like COFCO and Wilmar are actively expanding their regional footprint through strategic acquisitions and partnerships, further intensifying the competitive environment.

Sustainability has become a crucial differentiator in the market, with major players investing significantly in environmental initiatives. Companies are implementing comprehensive deforestation-free sourcing programs and sophisticated traceability systems to maintain access to premium markets and ensure compliance with evolving regulatory requirements. The adoption of RSPO and similar sustainability certifications has become increasingly important for market access and premium pricing, reflecting the growing demand for environmentally responsible products.

The market presents significant opportunities in specialty segments, particularly through technological advancements. Smaller companies are leveraging innovations in enzymatic processing and flexible feedstock utilization to enhance their competitive position. These technological capabilities enable them to achieve operational efficiencies and product differentiation beyond traditional commodity pricing competition. The combination of advanced processing technologies and sustainability credentials creates new pathways for market participants to establish stronger positions in premium market segments.

South America Fats and Oils Industry Leaders

-

Cargill Inc.

-

Bunge Limited

-

Olam International Limited

-

Fuji Oil Holding Inc.

-

ADM

- *Disclaimer: Major Players sorted in no particular order

South America Fats and Oils Market Companies Covered in this Report

- AAK AB

- Archer Daniels Midland Company

- Bunge Limited

- Cargill Incorporated

- Fuji Oil Holdings Inc.

- Olam International Limited

- Sime Darby Plantation Berhad

- Agropalma S.A.

- Aceitera General Deheza S.A.

- Wilmar International Ltd.

- Louis Dreyfus Company

- COFCO International

- Granol Indústria

- Algar Agro

- Molinos Río de la Plata

- Vicentin S.A.I.C.

- Oleoplan S.A.

- Grupo Nutresa (Comercial Colombia)

- JBS (Tallow Division)

- CBI Indústria de Óleos

Recent Industry Developments in South America Fats and Oils Market

- July 2025: Cargill acquired complete ownership of its soybean oil crushing, refining, and bottling plant in Barreiras, Bahia, Brazil. This acquisition strengthens Cargill's position in Brazil, the world's largest soybean producer and exporter, while demonstrating its commitment to regional expansion.

- August 2025: Louis Dreyfus Company (LDC) expanded its oilseed and grain operations through a new port terminal in Santa Elena, Argentina. This investment addresses the increasing demand for edible oils and bio-based feedstocks in South America's fats and oils market.

- July 2023: Bunge and Chevron's Renewable Energy Group acquired Chacraservicios S.r.l., an Argentine company that specializes in cultivating Camelina sativa, a high-oil-content cover crop. The acquisition expands their global supply chain by adding a new oil source, supporting their efforts to meet increasing demand for lower-carbon renewable feedstocks.

South America Fats and Oils Market Report Scope

The South American fats and oils market is segmented by type into fats, specialty fats, and oils. Based on the application, the market is classified according to the application of fats and oils in food, industrial, and animal feed applications. The market is also differentiated on the basis of geography.

Segmentation Overview

By Type

| Fats | Butter |

| Tallow | |

| Lard | |

| Specialty Fats | |

| Oils | Soybean Oil |

| Palm Oil | |

| Coconut Oil | |

| Sunflower Seed Oil | |

| Other Oils |

By Application

| Food | Confectionary |

| Bakery | |

| Dairy Products | |

| Margarine and Spreads | |

| Others | |

| Industrial | |

| Animal Feed |

Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Type | Fats | Butter |

| Tallow | ||

| Lard | ||

| Specialty Fats | ||

| Oils | Soybean Oil | |

| Palm Oil | ||

| Coconut Oil | ||

| Sunflower Seed Oil | ||

| Other Oils | ||

| By Application | Food | Confectionary |

| Bakery | ||

| Dairy Products | ||

| Margarine and Spreads | ||

| Others | ||

| Industrial | ||

| Animal Feed | ||

| Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the South America fats and oils market in 2031?

The market is expected to reach USD 43.72 billion by 2031, reflecting a 7.02% CAGR from 2026.

Which product type is growing the fastest?

Fats are forecast to expand at a 7.61% CAGR, outpacing commodity oils due to rising demand for specialty bakery and confectionery applications.

Why is Brazil maintaining a dominant share of regional demand?

Obligatory biodiesel blending, abundant soybean supply, and extensive crushing infrastructure keep Brazil at 53.88% of 2025 revenue.

How will Argentina’s proposed biofuel legislation affect industry growth?

If enacted, the Liga Bioenergética bill could raise the national blend to B15 by 2027 and propel Argentina’s market to an 8.07% CAGR.

Page last updated on: