Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.15 Billion |

| Market Size (2026) | USD 4.23 Billion |

| Market Size (2031) | USD 4.65 Billion |

| Growth Rate (2026 - 2031) | 1.93% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Energy Drink Market Analysis by Mordor Intelligence

The South American energy drinks market size was valued at USD 4.15 billion in 2025 and estimated to grow from USD 4.23 billion in 2026 to reach USD 4.65 billion by 2031, at a CAGR of 1.93% during the forecast period (2026-2031). he market growth is driven by increasing consumer preference for functional beverages, with a notable shift toward products containing natural ingredients and reduced sugar content. Product innovation focuses on introducing new flavors, healthier formulations, and enhanced functional benefits. Celebrity endorsements and strategic marketing campaigns significantly influence consumer purchasing decisions, particularly among the youth demographic. The rising participation in sports activities and fitness trends has created additional demand for energy-boosting beverages. The younger population's interest in performance enhancement and mental alertness continues to support market expansion, especially in urban areas and among university students and young professionals. However, growing health concerns about high caffeine and sugar content, coupled with stringent regulatory requirements for energy drink manufacturers, moderate the overall growth rates in the region.

Key Report Takeaways

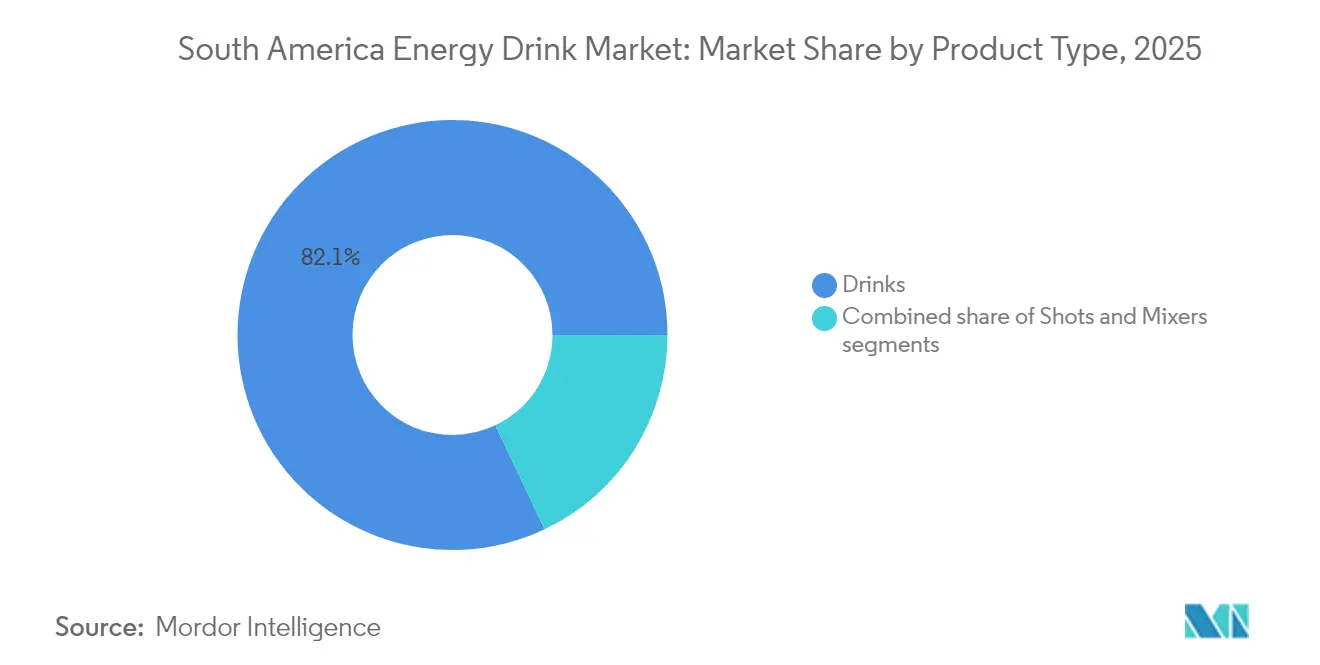

- By product type, drinks led with 82.05% of the South American energy drinks market share in 2025, while shots are projected to expand at a 2.38% CAGR through 2031.

- By packaging type, cans captured 71.20% share of the South American energy drinks market in 2025; PET/glass bottles are set to grow at a 2.55% CAGR between 2026-2031.

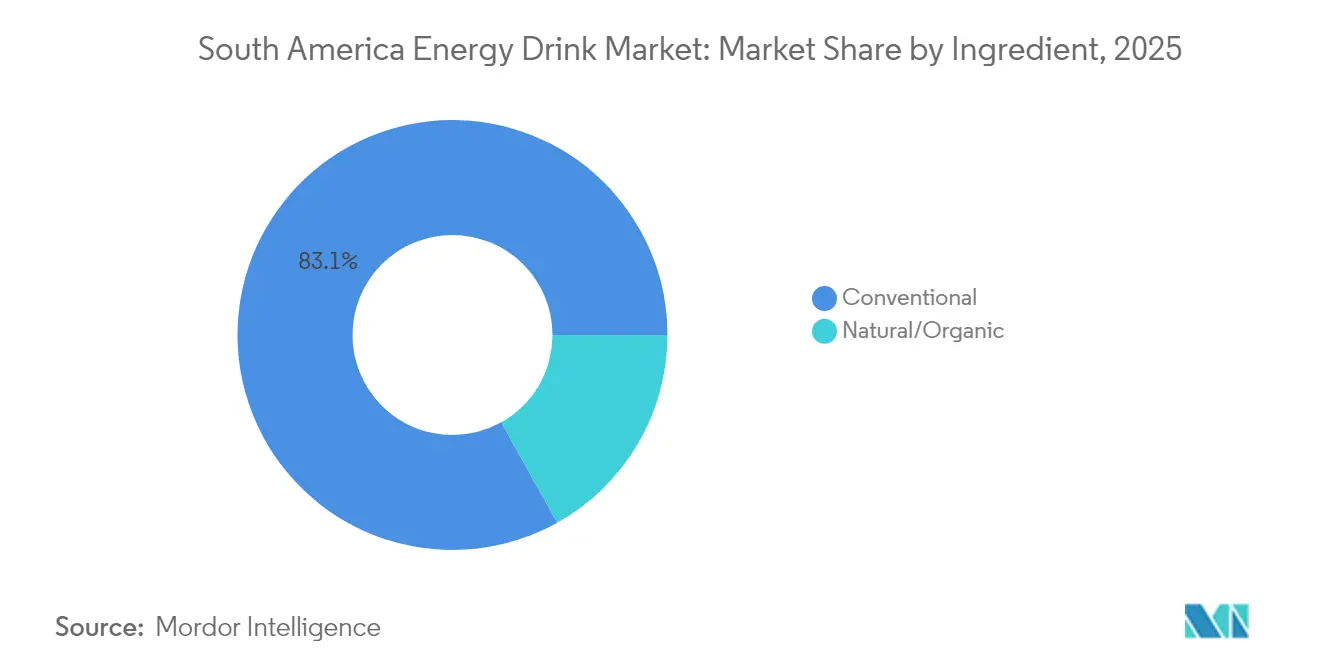

- By ingredient, conventional formulations held 83.10% share of the South American energy drinks market in 2025, whereas natural/organic variants are forecast to rise at a 2.74% CAGR to 2031.

- By distribution channel, off-trade accounted for 77.30% share of the South American energy drinks market in 2025, with on-trade outlets expected to post a 2.16% CAGR during 2026-2031.

- By geography, Brazil commanded 48.10% of the South American energy drinks market in 2025; Argentina is poised for the fastest growth at a 3.50% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Energy Drink Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Product innovation in terms of flavor and ingredients | +0.7% | Brazil, Argentina, Rest of South America | Medium term (2-4 years) |

| Growing influence of endorsements and social media marketing | +0.6% | Brazil, Argentina, with spillover to Rest of South America | Short term (≤ 2 years) |

| Rising sports participation rate coupled with strong demand from fitness conscious consumers | +0.8% | Brazil, Argentina | Medium term (2-4 years) |

| Growing demand for on-the-go healthy beverages | +0.5% | Whole region, with stronger impact in Brazil | Long term (≥ 4 years) |

| Strategic marketing and sponsorships | +0.5% | Brazil, Argentina, with expansion to Rest of South America | Short term (≤ 2 years) |

| Young demographic appeal | +0.6% | Brazil, Argentina, Rest of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product innovation in terms of flavor and ingredients

Product innovation drives growth in South America's energy drinks market, as manufacturers introduce new flavors and formulations to meet consumer preferences. The market shows increasing demand for natural ingredients, particularly yerba mate, which contains natural caffeine and holds cultural significance in the region. This shift toward natural ingredients reflects consumers' growing preference for healthier alternatives in their energy drink choices. Manufacturers are responding by developing products that combine traditional energy-boosting properties with natural components. In September 2024, Monster Beverage Corporation launched Juice Monster Rio Punch, featuring Brazilian fruit flavors, reflecting the market's focus on regional taste preferences. The introduction of locally inspired flavors demonstrates how companies are adapting their product portfolios to align with regional consumer preferences while maintaining their market position.

Growing influence of endorsements and social media marketing

High internet penetration rates across South America have enabled energy drink companies to execute effective digital marketing campaigns and celebrity endorsements. According to World Bank data in 2023, internet users comprised 89% of Argentina's population, 84% of Brazil's, 80% of Peru's, and 77% of Colombia's [1]The World Bank Group, "Individuals using the Internet (% of population)," data.worldbank.org. This digital reach has influenced younger consumers, whose purchasing decisions are shaped by influencer recommendations, such as athletes, musicians, and social media personalities, and social media marketing. The widespread social media adoption in these countries has provided energy drink brands with platforms for digital content, promotional campaigns, and interactive marketing, resulting in increased brand awareness and consumption among target demographics. In May 2025, Anheuser-Busch launched an energy drink called Phorm Energy in collaboration with UFC's Dana White, demonstrating the impact of strategic endorsements on market growth.

Rising sports participation rate coupled with strong demand from fitness conscious consumers

The rise in sports participation and fitness awareness across South America has increased energy drink consumption significantly. Consumers consistently associate energy drinks with enhanced athletic performance and mental alertness during physical activities, which continues to drive strong demand for functional beverages across the region. A FSB Pesquisa survey in Brazil in 2023 found that 22% of the population performs daily physical activity, while 13% exercise at least three times weekly, indicating substantial market potential [2]Empresa Brasil de Comunicação, "Survey reveals that 52% of Brazilians do not exercise,"www.ebc.com.br. This strong connection between sports participation and energy drink consumption creates a stable and sustainable demand base that persists through various economic changes and market conditions, though health authorities increasingly express concerns about high caffeine intake during exercise and its potential health implications.

Growing demand for on-the-go healthy beverages

Consumer preferences in South America are experiencing a significant shift toward convenient, portable beverages that deliver functional benefits without compromising health considerations. Many consumers, particularly from current generations, have increasingly replaced their regular coffee consumption with energy drinks, seeking alternatives that align with their active lifestyles. In response to this evolving consumer behavior, manufacturers have strategically adapted their formulations by reducing ingredients previously targeted at athletes, such as glucono delta-lactone, caffeine, and sugar. Currently, a 500cc energy drink contains caffeine equivalent to a double espresso, making it more accessible for daily consumption. This market evolution is clearly demonstrated in recent developments, as exemplified by Score, a Chilean energy drink with a German formula, which launched in February 2025 and is actively expanding its presence into the growing markets of Peru and Brazil. The trend toward on-the-go healthy options is particularly pronounced in urban centers, where busy lifestyles drive consumption of functional beverages that promise sustained energy without the crash associated with traditional high-sugar energy drinks.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Health concerns over chemical ingredients | -0.4% | Brazil, Argentina, with growing impact across South America | Medium term (2-4 years) |

| Consumer inclination towards fresh juice products | -0.3% | Brazil, with moderate impact in Argentina | Long term (≥ 4 years) |

| Competition from alternative beverages | -0.5% | Brazil, Argentina, Rest of South America | Medium term (2-4 years) |

| Regulatory and labeling pressures | -0.4% | Argentina, Brazil, with expansion to Rest of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over chemical ingredients

Health concerns regarding artificial ingredients in energy drinks are impacting market growth in South America. Regional regulatory authorities are enforcing more stringent policies, particularly front-of-package (FoP) warning labels. Research conducted in Uruguay demonstrated that caffeine warning labels affected young adults' purchasing decisions. Mexico and Chile have introduced taxes on sugar-sweetened beverages and mandatory FoP labeling, resulting in reduced consumption of sugary drinks, including energy beverages. The Pan American Health Organization's concerns about ultra-processed beverages and obesity have led to increased demands for tighter regulations across Latin America. In response, manufacturers are working to reformulate products with natural ingredients while attempting to maintain their energy-enhancing effects.

Consumer inclination towards fresh juice products

South America's traditional preference for fresh, natural beverages challenges the growth of energy drinks, particularly as consumer health awareness increases. Brazil's strong cultural connection to fresh fruit juices creates direct competition for energy drink manufacturers, as consumers view local natural alternatives as healthier and more authentic. The Brazilian National Health Surveillance Agency (ANVISA) implemented RDC 839/2023, which establishes regulations for new ingredients and foods, supporting innovation in the natural beverage segment[3]United States Department of Agriculture, "FAIRS Country Report Annual,"apps.fas.usda.gov . This regulatory framework, combined with the region's abundant fruit resources, enhances the competitive position of fresh alternatives in the beverage market. Energy drink manufacturers must address these market conditions by emphasizing their products' functional benefits while incorporating natural ingredients to address health-related concerns. The strong cultural preference for natural beverages and a supportive regulatory environment for fresh alternatives act as a significant restraint on energy drink market growth in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Drinks Dominate While Shots Accelerate

The drinks segment accounted for 82.05% of South America's energy drinks market share in 2025. The segment's dominance stems from extensive product distribution networks across supermarkets, convenience stores, and retail outlets, coupled with established consumer preferences for ready-to-drink formats. Major companies maintain this market position through regular product development initiatives, including new flavor variants, sugar-free alternatives, and enhanced formulations with added vitamins and functional ingredients. The segment's growth is further supported by aggressive marketing campaigns, competitive pricing strategies, and increasing consumer demand for convenient energy-boosting beverages in the region.

The shots segment is expected to achieve the highest growth rate at 2.38% CAGR during 2026-2031driven by its convenience and concentrated formula that appeals to on-the-go consumers seeking immediate energy boosts. This growth is particularly evident in urban centers where busy lifestyles create demand for quick, portable energy solutions. The segment's expansion is also supported by innovative formulations that address health concerns, with companies developing shots that contain natural caffeine sources like green tea extract. This trend toward healthier, more concentrated energy solutions positions the shots segment for continued growth, particularly among younger consumers seeking functional benefits without the volume of traditional energy drinks.

By Packaging Type: Aluminum Dominates Amid Sustainability Push

Cans dominate the South American energy drinks market with a 71.20% market share in 2025. Their popularity stems from multiple advantages: superior portability for on-the-go consumption, extended shelf stability without refrigeration, and enhanced brand visibility through 360-degree product labeling. The recyclable nature of aluminum cans strengthens their market position, particularly as sustainability becomes a key consumer consideration. Ball Corporation, a major can manufacturer in the region, demonstrates this environmental commitment through its transition to 100% renewable energy in manufacturing operations. This initiative aims to reduce carbon emissions across the supply chain while meeting the growing demand from environmentally conscious consumers who prioritize sustainable packaging solutions. The combination of practical benefits and environmental considerations continues to reinforce cans as the preferred packaging format in South America's energy drinks sector.

PET/glass bottles are experiencing a growth rate of 2.55% CAGR (2026-2031), surpassing other packaging formats in the energy drinks market. This growth aligns with market premiumization trends and heightened environmental consciousness among consumers and manufacturers. The shift towards these packaging materials reflects changing consumer preferences and regulatory pressures for sustainable packaging solutions. Major beverage manufacturers have implemented comprehensive bottle-to-bottle recycling programs and increased the use of post-consumer recycled (PCR) PET in their packaging. These initiatives include establishing collection networks, investing in recycling infrastructure, and developing advanced recycling technologies. Companies are also focusing on reducing the weight of PET bottles while maintaining structural integrity to further minimize environmental impact. Glass bottles maintain strong demand in premium and natural/organic energy drink segments, where they align with consumer perceptions of quality and sustainability.

By Ingredient: Natural Options Challenge Conventional Dominance

Conventional energy drinks maintained their market leadership with an 83.10% share in 2025, leveraging established brand recognition and widespread distribution networks across South America. These products, typically formulated with synthetic caffeine, taurine, and various B vitamins, continue to dominate retail shelves due to their proven efficacy and competitive pricing. However, the segment faces increasing scrutiny from health authorities and changing consumer preferences, creating both challenges and opportunities for reformulation toward cleaner labels while maintaining functional benefits.

The natural/organic segment is growing at a faster rate of 2.74% CAGR (2026-2031), driven by increasing health consciousness and cultural connections to indigenous ingredients. Companies are transforming traditional yerba mate into modern energy drinks by offering flavored, sweetened, and ready-to-drink versions in individual-sized containers that appeal to convenience-seeking consumers. The market is also seeing growth in other natural ingredients like guayusa, demonstrated by GURU Organic Energy's introduction of GURU Guayusa Tropical Punch, a plant-based energy drink inspired by Ecuador's Jivaro people. This segment's growth reflects a broader shift toward clean label products that deliver energy without artificial ingredients.

By Distribution Channel: Off-Trade Leads Despite On-Trade Recovery

The off-trade channel holds a dominant 77.30% share of South America's energy drinks market in 2025. This dominance stems from extensive product availability across supermarkets, hypermarkets, and convenience stores. Brazil exemplifies this trend through its expanded modern retail formats, providing consumers broad access to energy drinks. Convenience and grocery stores serve as key points for impulse purchases, while supermarkets and hypermarkets attract consumers through competitive pricing and promotions. In Brazil, the availability of installment payment options increases purchasing power in these retail channels, reinforcing their market position.

The on-trade channel, despite its smaller market share, is expected to grow at a 2.16% CAGR during 2026-2031, exceeding overall market growth rates as social activities recover post-pandemic. This segment includes bars, restaurants, clubs, and fitness centers where consumers drink energy beverages on-premise or mix them with alcohol. Urban areas with active nightlife demonstrate significant growth, as energy drinks become essential components of cocktail offerings. The channel benefits from increasing consumer preference for premium consumption experiences in social settings, with energy drinks marketed as lifestyle products. This repositioning enables higher profit margins and strengthens brand presence through experience-based marketing that appeals to younger consumers who view beverage choices as social statements.

Geography Analysis

Brazil accounts for 48.10% of South America's energy drinks market in 2025, supported by its large population and extensive distribution networks. The country's young demographic, particularly those aged 18-34, provides a strong consumer base for energy drinks. The market growth is further enhanced by Brazil's well-developed retail infrastructure, including supermarkets, convenience stores, and e-commerce platforms. Coca-Cola FEMSA Brasil has expanded its presence in this market by offering multiple Monster Energy variants to address different consumer preferences. The company's strategic partnerships with local distributors and retailers have strengthened its market position and improved product accessibility across urban and suburban areas.

Argentina shows the highest growth potential with a projected CAGR of 3.50% (2026-2031), exceeding the regional average. The country produced 986.7 thousand metric tons of yerba mate in 2024, according to the Brazilian Institute of Geography and Statistics, making it Latin America's largest producer . This indigenous ingredient presents opportunities for energy drink innovation. However, new regulations targeting energy drink consumption among youth may affect marketing and product development.

Chile, Peru, Colombia, and Uruguay present varied growth opportunities and regulatory frameworks. Chile's Ministry of Health has enacted food labeling regulations that affect energy drink marketing and consumer behavior. Companies across these markets are adapting their strategies to meet increasing demand for healthier beverages while complying with local regulations and consumer preferences. Colombia's growing network of convenience stores is increasingly embracing cold-chain offerings. Meanwhile, Uruguay, acting as a policy trendsetter, is conducting caffeine-warning trials that could influence the entire region.

Regulatory Landscape

Energy drinks across South America face fragmented, country-specific compliance requirements covering caffeine limits, product categorization, labeling, and pre-market approvals. In Brazil, the Brazilian National Health Surveillance Agency (ANVISA) governs food and beverage rules, including caffeine limits used for energy drink formulations (commonly referenced at 35 mg/100 ml). ANVISA implemented Normative Instruction IN No. 281 in February 2024 to clarify categorization and documentation requirements for food products, tightening technical substantiation and dossier discipline for launches and renovations.

In the Southern Cone and Andean markets, labeling and sanitary registration can be as decisive as formulation. Chile applies mandatory front-of-package warning labels under Law 20.606 and updates to the Sanitary Food Regulations (DS 977) for products exceeding thresholds such as added sugars and calories, directly affecting energy drink packs and claims. Colombia requires sanitary registration via INVIMA under Resolucion 4150 of 2009, while Argentina regulates energy drinks under the Argentine Food Code with defined maximum limits for caffeine and taurine, pushing manufacturers toward country-by-country recipes and pack compliance rather than a single regional SKU strategy.

Competitive Landscape

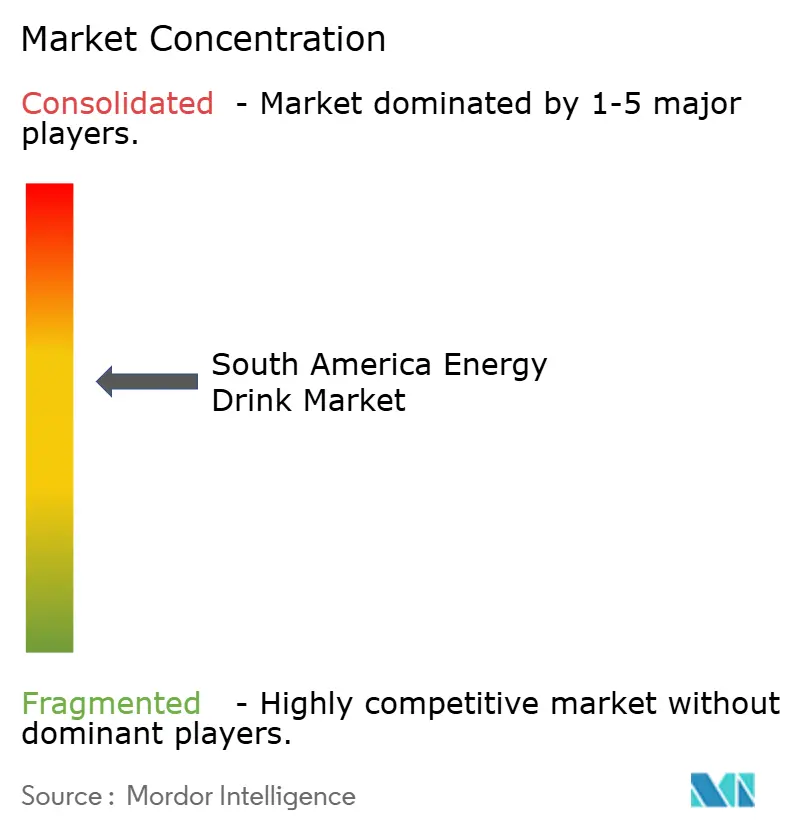

The South American energy drinks market demonstrates moderate concentration, featuring both global giants and emerging regional players, including Red Bull GmbH, Monster Beverage Corp., PepsiCo Inc., AJE Group, and Anheuser-Busch InBev. The competitive landscape continues to evolve through strategic moves, as evidenced by Monster's acquisition of Bang Energy in July 2023. Through its partnership with Monster and its independent brands, Relentless and Powerade Energy, Coca-Cola boasts a strong presence in organized retail coolers, capitalizing on its decades-long distribution strength. Meanwhile, Ambev, with its Fusion brand and unique RTD coffee hybrids, has carved out a market niche, ensuring access to micro traders often overlooked by its larger competitors.

White-space opportunities are particularly notable in the natural/organic segment, where regional ingredients like yerba mate and guayusa provide unique positioning advantages. Companies like Guayakí have successfully capitalized on yerba mate's indigenous South American roots, while regulatory variations across countries create complex compliance requirements that favor organizations with strong regulatory capabilities. By the decade's end, the South American energy drinks industry may witness a reshuffling of its leadership tables, driven by forward-looking strategies such as vertical integration into herbal plantations, AI-guided flavor mapping, and blockchain batch tracking.

The market's growth trajectory is supported by emerging national economies, modernizing retail channels, and rising middle-class incomes across South America. Companies are adapting their formulations to address increasing health concerns, focusing on reduced sugar content and natural ingredients while maintaining functional benefits. Manufacturers are aligning their brands with the preferences of younger, urban consumers and enhancing communication strategies to reach the growing urban population and migrant communities in the region.

South America Energy Drink Industry Leaders

-

Red Bull GmbH

-

Monster Beverage Corp.

-

PepsiCo Inc.

-

AJE Group

-

Anheuser-Busch InBev

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reformulation and portfolio architecture around sugar and caffeine constraints remain a central opportunity across South America. Manufacturers manage front-of-package warnings and sugar-related levies in parts of Latin America by expanding reduced-sugar and zero-sugar lines and by shifting stimulation positioning toward botanicals such as yerba mate, guarana, and guayusa. This is reinforced by observed product activity in the region, including the entry of mate-based, zero-sugar propositions into Brazil (for example, Machu Picchu Energy distributing through retail chains such as St. Marche, Mambo, and Pao de Acucar), which points to shelf traction for cleaner-label energy formats beyond conventional high-sugar profiles.

Operational whitespace is also visible in localized capacity, packaging availability, and distribution infrastructure that can improve cost-to-serve and execution in off-trade heavy channels. In February 2026, Baly Brasil acquired an industrial facility in Ararangua, Santa Catarina, to establish an additional manufacturing plant and scale output, highlighting how domestic production is being used to defend price points and widen geographic reach in Brazil. In May 2026, Coca-Cola FEMSA invested in a new distribution center in Argentina (Nuevo Norte) with clean-technology positioning, and it also inaugurated a can production line in Uruguay, underscoring ongoing investments aimed at route-to-market reliability and packaging optionality for energy and broader beverage portfolios in key South American corridors.

Recent Industry Developments

- June 2026: Monster Beverage Corporation reported a 19% increase in international markets growth in the first quarter of 2026, underscoring the role of non-US performance in overall momentum. The update also reinforces the strategic importance of scaled bottler-led distribution in Latin America, where availability and cooler execution can materially shape share in modern and convenience retail.

- May 2026: AJE Group launched Cielo Antiox in Colombia, extending its functional beverage lineup in a market where consumers increasingly compare energy and functional propositions side-by-side. The launch strengthens AJE's regional portfolio depth and broadens its participation in better-for-you demand spaces that overlap with energy drink consumption occasions.

- September 2024: Monster Beverage Corporation launched Juice Monster Rio Punch with Brazilian fruit flavor cues, aligning product development with local taste preferences. The launch shows how global brands use localized flavors to protect shelf visibility and relevance while competing against regional players and expanding into natural-ingredient adjacencies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers retail and on-trade sales value of energy drinks across South America, counted at the price level that reflects what buyers pay in each country, and then converted into USD for comparability.

Scope exclusions: Alcoholic energy drinks, sports drinks, and non-energy functional beverages are excluded from this market sizing.

Segmentation Overview

-

By Product Type

- Drinks

- Shots

- Mixers

-

By Packaging Type

- PET/Glass Bottles

- Cans

- Other Packaging Types

-

By Ingredient

- Conventional

- Natural/Organic

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Convenience Stores/Grocery Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Others Distribution Channel

-

By Country

- Brazil

- Argentina

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

We start with desk research to set the demand and supply context for energy drinks in South America and to anchor the model with public data series that can be checked year over year. Common inputs include government trade statistics (imports and exports under beverage-related HS codes), central bank and national statistics offices for inflation and exchange rates, and food regulator portals for labeling rules and caffeine related guidance.

To further validate the structure, we also review sources such as UN Comtrade, FAO statistics, and trade association publications covering non-alcoholic beverages, followed by company annual reports, investor presentations, and reputable business press for portfolio and channel commentary. A few paid database subscriptions are used only for company financials, news monitoring, and selective shipment level import-export checks where available. The sources listed here are illustrative, and many other public documents were also used to collect, validate, and clarify data points during the study.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk research cannot fully show, especially channel mix, typical price movements, and how product formats (drinks, shots, and mixers) are actually stocked and promoted. We spoke with manufacturers, bottlers, distributors, modern trade and convenience channel stakeholders, and on-trade buyers across major South American countries, and then used their inputs to confirm assumptions, close data gaps, and align the final market totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 41% |

| Mid tier: 52% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 20% | Managers: 45% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where total non-alcoholic ready-to-drink beverage consumption and retail sales signals are reconstructed by country, and then narrowed to energy drinks using penetration and category share checks by channel and format. Once the country totals are obtained, they are further filtered through packaging and ingredient splits that match how products are sold on shelves and in on-trade outlets.

The totals are then corroborated with selective bottom-up approximations, mainly by rolling up sampled brand volumes and prices from channel checks, and by using manufacturer and distributor feedback on shipment patterns to major retailers. Key inputs used in the model include: off-trade versus on-trade mix, typical can versus bottle price gaps, inflation-linked price progression, currency conversion timing, and the share of energy shots and mixers within the broader category.

For forecasting, we use scenario analysis supported by short-run time series smoothing, since energy drink growth in the region is sensitive to macro conditions and price resets. Assumptions for variables such as real income trends, retail expansion pace, and expected pricing actions are reviewed with primary respondents before the final forecast is locked. Where bottom-up data is patchy in smaller countries, we apply proxy ratios from comparable markets and then re-check them with distributor interviews to avoid overstating demand.

Data Validation & Update Cycle

Validation is done in multiple steps so that one data source does not drive the full story. We compare model outputs against independent signals such as trade flows, channel expansion commentary, and reported beverage revenue trends, and then investigate any country-level jumps that do not match pricing or distribution realities.

Before sign-off, the work is reviewed by another analyst who checks the calculations, unit logic, and the consistency of assumptions across countries and years. Reports are refreshed annually, and interim updates are made when material events affect pricing, regulation, or distribution. Right before delivery, we run a final pass to confirm that the latest macro inputs and any major market moves are reflected in the published numbers.

Mordor Intelligence's South America Energy Drink Market Size Measured Against Other Published Estimates

Published market sizes for South America energy drinks can differ widely, even when the time period looks similar, because the product basket and pricing basis are not always aligned. Differences also show up when one estimate is built mainly from retail value assumptions, while another leans on broader beverage groupings or longer-range growth narratives.

Energy and sports drinks counted together is a common inclusion that pushes totals upward, and energy drink concentrates or adjacent functional beverages are sometimes added without being called out clearly. Energy shots and mixers may also be treated differently across studies, and currency conversion and inflation timing can shift USD values in a region with frequent price resets. Alcoholic energy drinks sit outside Mordor Intelligence's scope, which reduces the risk of double counting with ready-to-drink alcoholic categories when channel checks are used.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.15 B (2025) | |

| Regional Consultancy A | USD 3.00 B (2024) | Uses an earlier base year and a different product-type grouping that emphasizes traditional and functional variants, which can understate value when inflation-linked price steps in 2025 are not fully captured. |

| Industry Publisher B | USD 3.08 B (2022) | Relies on an older point estimate and a longer study window, with limited visibility on how off-trade versus on-trade splits and price progression were refreshed, which can lag the latest channel mix shifts. |

The table shows that the biggest spread is explained by year alignment and what gets grouped into the category, followed by how prices are carried forward in USD terms. By keeping the scope tight and re-checking channel and price assumptions with field inputs, the final number stays traceable to a clear demand pool and repeatable steps.

Key Questions Answered in the Report

What is the current value of the South American energy drinks market?

The market is worth USD 4.23 billion in 2026 and is projected to reach USD 4.65 billion by 2031 at a 1.93% CAGR.

Which country holds the largest share in the region?

Brazil leads with a 48.10% share, supported by a young population and broad retail coverage.

Which segment is growing fastest by ingredient?

Natural/organic formulations are forecast to grow at 2.74% CAGR, driven by interest in yerba mate and other botanicals.

How significant is on-trade sales growth?

On-trade channels are set to expand at a 2.16% CAGR as bars, gyms, and restaurants recover post-pandemic.

Page last updated on: