Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

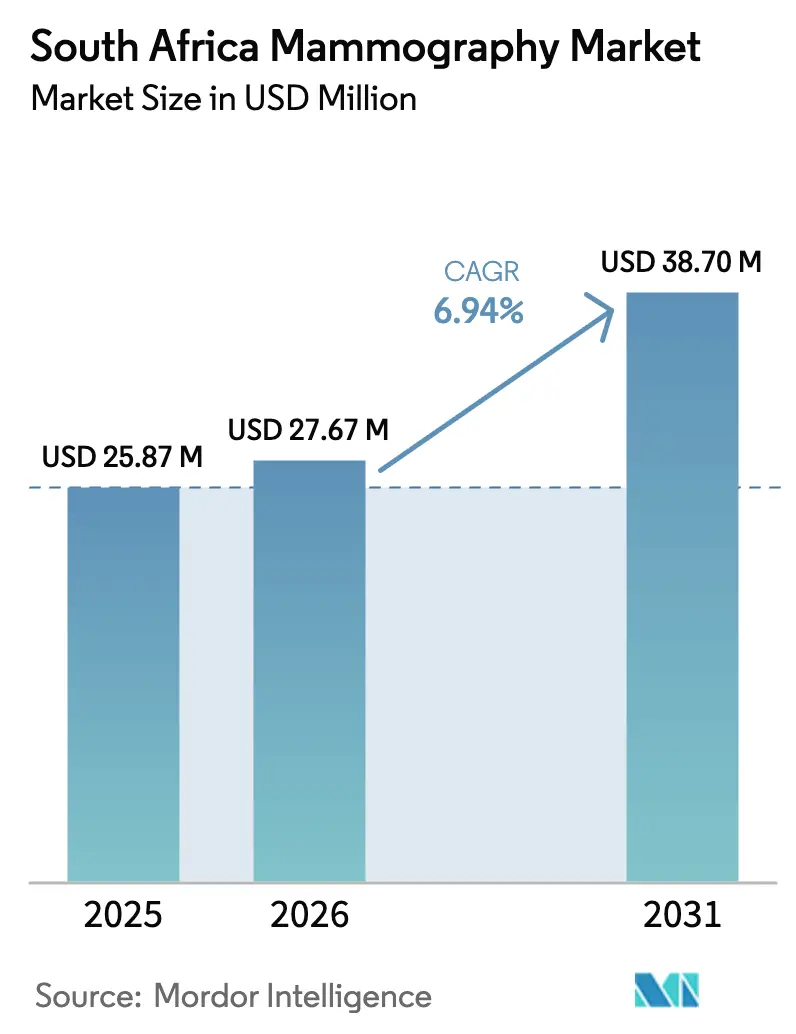

| Base Year Market Size (2025) | USD 25.87 Million |

| Market Size (2026) | USD 27.67 Million |

| Market Size (2031) | USD 38.7 Million |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Mammography Market Analysis by Mordor Intelligence

South Africa mammography market size in 2026 is estimated at USD 27.67 million, growing from 2025 value of USD 25.87 million with 2031 projections showing USD 38.7 million, growing at 6.94% CAGR over 2026-2031. This growth reflects the combined influence of the May 2024 National Health Insurance (NHI) Act, an accelerating analog-to-digital replacement cycle, and sustained investment in 3-D tomosynthesis platforms. Demand is further strengthened by rising breast-cancer incidence, corporate ESG funding for women’s health programs, and hospital strategies that prioritize AI-ready imaging infrastructure. Procurement momentum is strongest in Gauteng, Western Cape, and KwaZulu-Natal, yet mobile screening units targeting rural provinces provide the fastest volumetric upside. Regulatory scrutiny from SAHPRA favors established vendors with complete quality documentation, steering public tenders toward globally recognized suppliers while still allowing niche entrants to win on service flexibility. Workforce shortages in radiography and medical physics continue to tighten capacity, which in turn amplifies interest in algorithm-based productivity tools.

Key Report Takeaways

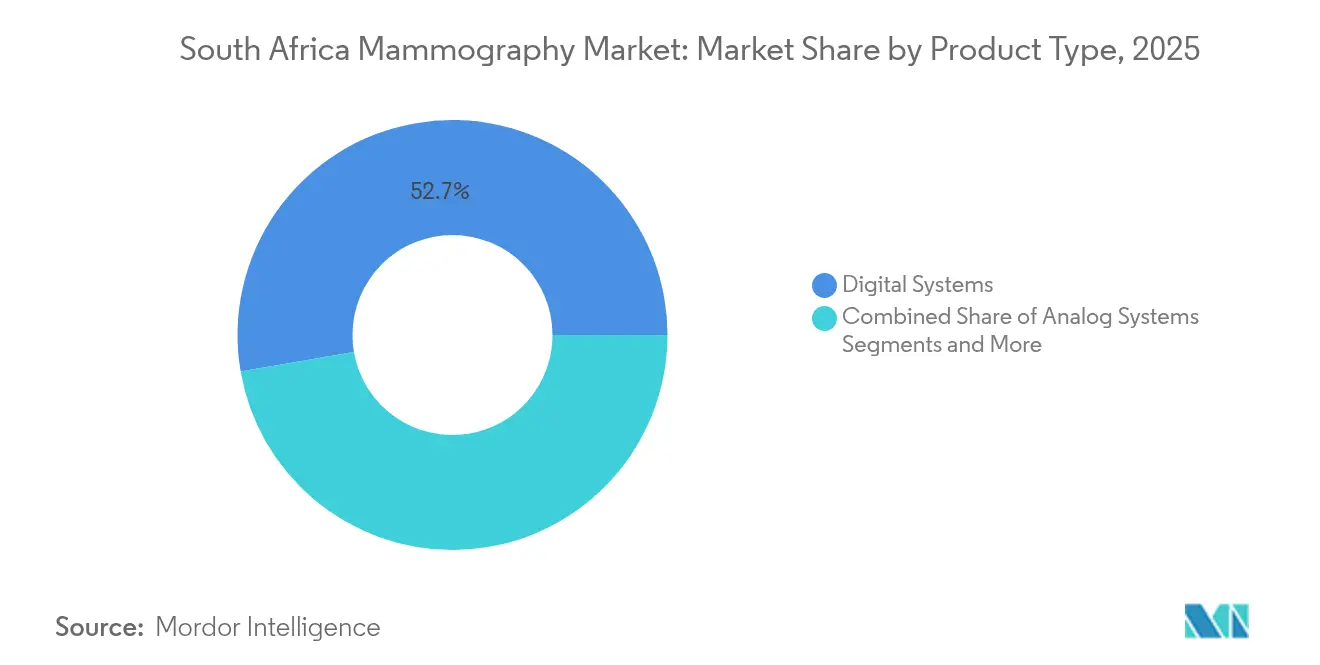

- By product type, digital systems captured 52.72% revenue share in 2025 while breast tomosynthesis is projected to rise at a 7.86% CAGR to 2031.

- By technology, 2-D full-field digital mammography held 47.65% of South Africa mammography market share in 2025 whereas 3-D tomosynthesis is on track for a 7.38% CAGR through 2031.

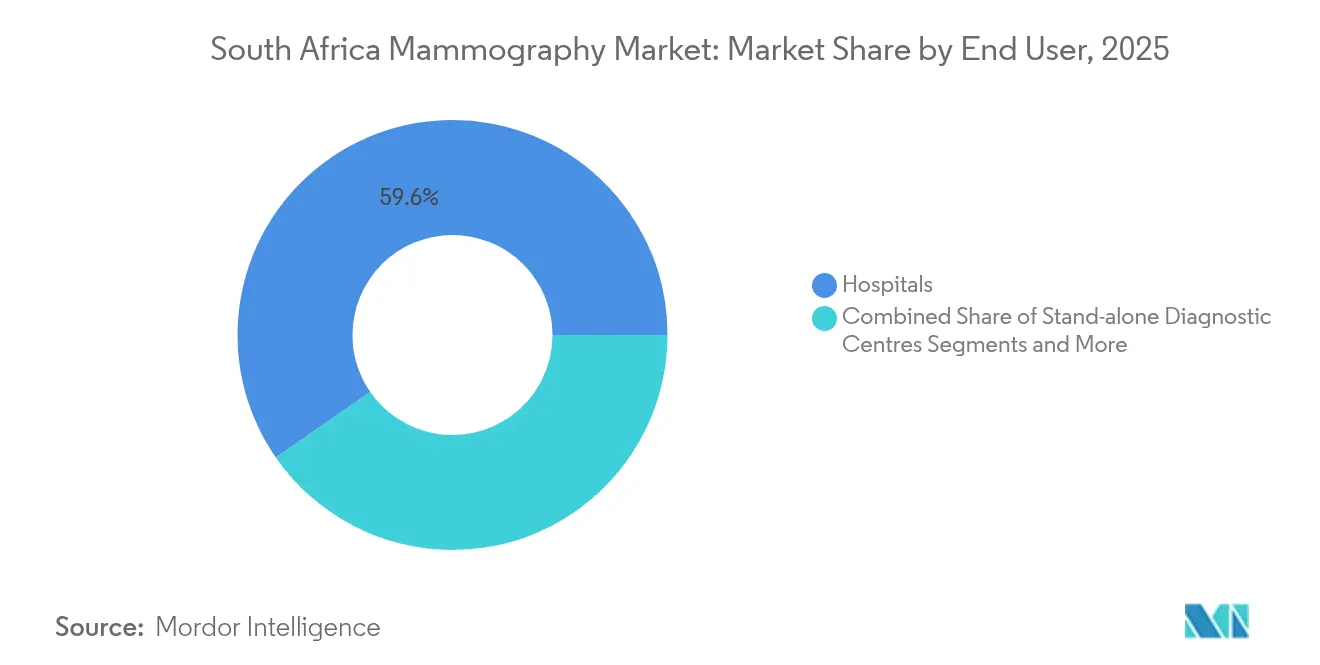

- By end user, hospitals accounted for 59.64% of the South Africa mammography market size in 2025 and mobile screening units are forecast to advance at an 8.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising breast-cancer incidence in SA | +1.8% | National with urban concentration | Medium term (2-4 years) |

| Government NHI roll-out expanding access | +2.1% | National early gains in Gauteng, Western Cape, KwaZulu-Natal | Long term (≥4 years) |

| Digitization and 3-D tomosynthesis upgrades | +1.5% | National prioritizing tertiary hospitals | Short term (≤2 years) |

| Mobile mammography outreach to rural provinces | +1.2% | Eastern Cape, Limpopo, Northern Cape, North West | Medium term (2-4 years) |

| AI-enabled workflow and decision support | +0.8% | Urban private networks | Short term (≤2 years) |

| Corporate ESG funding for women’s health | +0.6% | National corporate headquarters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Breast-Cancer Incidence in SA

Incidence rates have trended upward since 2024, prompting both public and private providers to scale screening capacity beyond large urban hospitals. Increased awareness campaigns, shifting lifestyle factors, and better diagnostic reporting combine to elevate demand for equipment capable of early lesion detection. The South Africa mammography market therefore benefits from budget prioritization that treats breast imaging as a preventive necessity rather than an optional service. Urban tertiary centers responded first, yet provincial hospitals in secondary cities are now issuing purchase requisitions to match national care guidelines. Procurement urgency is expected to persist through 2030, given projections that breast-cancer prevalence will continue rising faster than other female cancers.

Government NHI Roll-Out Expanding Screening Access

The NHI Act guarantees universal coverage for breast-cancer screening, removing patient-side financial barriers that historically dampened utilization. Centralized equipment tenders bundled with five-year maintenance contracts give hospitals predictable cash-flow horizons, which supports multiyear capital planning. Provincial health departments are allocating ring-fenced funds for mobile units to meet initial rural targets, a move that further enlarges total addressable volume for system suppliers. Parallel policy emphasis on preventive care aligns seamlessly with mammography program objectives, turning the South Africa mammography market into a key beneficiary of the broader universal-health rollout.

Digitization & 3-D Tomosynthesis Upgrade Cycle

Hospitals replacing aging film units routinely select 2-D digital detectors, yet many are skipping directly to 3-D tomosynthesis because published studies confirm superior sensitivity in dense breast tissue [1]Pammla Petrucka, “Status of African Research and Its Contribution to Global Health Research,” Springer, SPRINGER.COM . Upgrade momentum is amplified by AI algorithms that require high-resolution digital inputs to achieve peak performance. Vendors respond by bundling analytics software with detector upgrades, creating a value proposition that blends clinical gains with workflow speed. Price premiums remain steep, though total-cost-of-ownership models show acceptable payback when reduced recall rates and shorter exam times are quantified. Replacement demand is forecast to crest between 2026 and 2028 as early adopters reach the end of their initial five-year depreciation schedules.

Mobile Mammography Outreach to Rural Provinces

Portable units bridge care gaps in sparsely populated regions, proving their worth through higher first-time-screen rates among women aged 40–54. Provincial pilots in Northern Cape and Limpopo logged participation gains of 18–22% during 2024–2025 cycles, which now serve as proof points for national scaling. Equipment specifications prioritize rugged chassis, battery backup, and satellite connectivity for cloud-based reads. Private-sector donors frequently underwrite fleet expansion as part of ESG commitments, making mobile programs one of the most reliable growth vectors for the South Africa mammography market.

AI-Enabled Workflow & Decision-Support Adoption

Diagnostic imaging departments face 18.1% radiographer vacancy rates, a shortage that pushes facilities toward software tools capable of automating routine image quality checks and preliminary reads [2]Medical Device Network Staff, “Carestream Unveils New Imaging Software and System Upgrades,” Medical Device Network, MEDICALDEVICE-NETWORK.COM . Early pilot sites report reading-time reductions of up to 35% for screening exams when AI triage flags low-risk studies for single review. Vendors with Food and Drug Administration clearance find their algorithms welcomed by SAHPRA, provided full validation datasets accompany applications. AI readiness therefore functions as both a competitive differentiator and a capacity multiplier, reinforcing adoption intent.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation-dose and over-diagnosis concerns | −0.9% | National influenced by global guidelines | Medium term (2-4 years) |

| High capex and limited reimbursements | −1.4% | National public-sector focus | Long term (≥4 years) |

| Shortage of radiographers and medical physicists | −1.1% | National acute in rural zones | Long term (≥4 years) |

| SAHPRA device-approval backlog | −0.7% | National regulatory framework | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Radiation-Dose & Over-Diagnosis Concerns

Clinicians remain cautious about screening younger low-risk populations because longitudinal studies question net mortality gains when false positives trigger unnecessary biopsies. Health-technology-assessment panels periodically revisit recommended screening intervals, which can temporarily suppress exam volumes. Vendor responses include lower-dose detector materials and AI-assisted lesion scoring meant to cut false positives. These mitigations ease but do not fully eliminate risk-benefit debates, so a modest drag on unit sales persists.

High Capex & Limited Reimbursements

Premium tomosynthesis systems cost up to 1.7 times more than conventional 2-D platforms, stretching hospital budgets operating on fixed-price diagnostic codes. Public hospitals often rely on multiyear Treasury allocations, which introduces procurement lags that defer volume realization. Private insurers reimburse screening at fee schedules that do not yet differentiate for 3-D value, dampening return-on-investment calculations for smaller clinics. Vendor financing and operating-lease structures partly offset up-front cost barriers but cannot fully resolve payback apprehensions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Systems Lead the Tomosynthesis Surge

Digital systems anchored 52.72% of total revenue in 2025 as most urban hospitals completed film-to-digital conversions. That dominance is projected to hold through 2031, supported by service contracts that bundle detector calibrations and AI software updates. Breast tomosynthesis recorded the fastest trajectory with a 7.86% CAGR and its share is forecast to approach one-quarter of the South Africa mammography market by decade’s end. Analog units now sell mainly to budget-constrained community clinics and are expected to phase out of tenders after 2027. The segment mix reflects a preference for image quality gains that instantly improve cancer-detection metrics without necessitating parallel infrastructure overhauls. Tomosynthesis popularity also benefits from patient satisfaction scores related to reduced callbacks. Vendors providing hybrid configurations capable of both 2-D and synthesized 3-D images enhance asset utilization for providers juggling mixed-insurance populations. Clinical validation continues to affirm dense-breast advantages, a salient factor given ethnic diversity in South African breast-density profiles .

Healthcare administrators increasingly reference internal audits showing 40% fewer false positives once tomosynthesis displaces legacy 2-D units. That performance has a direct financial impact because public hospitals carry the downstream cost of unnecessary biopsies. Consequently, the South Africa mammography market registers steady upgrades even when capital budgets are restricted. Some facilities adopt a phased replacement, placing tomosynthesis in high-volume centers first and allocating trickle-down digital units to peripheral clinics. Overall, digital products are entrenched as the platform of choice, while tomosynthesis provides the premium upsell path that manufacturers rely on for margin expansion.

By Technology: 3-D Tomosynthesis Disrupts 2-D Dominance

Full-field 2-D digital mammography secured 47.65% share in 2025, reflecting early adoption advantages and lower price points. Nonetheless 3-D tomosynthesis posted a 7.38% CAGR and is forecast to capture an incremental 14 percentage-point share by 2031. Demand is catalyzed by studies that link 3-D modalities to 27% higher invasive cancer detection rates relative to 2-D scans. Providers weigh these performance metrics against higher acquisition and maintenance costs. Early adopters often finance upgrades through public-private partnership grants or donor contributions, circumventing capex ceilings. The South Africa mammography market size attributed to tomosynthesis is expected to surpass USD 10.84 million by 2031, marking a strategic inflection point where 3-D systems shift from premium option to de facto standard.

Emerging niche technologies such as contrast-enhanced mammography populate the “Others” category and target diagnostic work-ups rather than routine screening. Market penetration for these modalities remains below 4% yet offers upside once reimbursement codes mature. AI overlays run seamlessly on both 2-D and 3-D datasets, though algorithm performance metrics rise when fed multi-plane images. Hospitals therefore perceive 3-D compatibility as essential for future-proofing. As SAHPRA accelerates clearance of synthesized 2-D solutions that cut additional exposures, dose-related objections are expected to recede, giving tomosynthesis an even firmer foothold.

By End User: Hospitals Dominate While Mobile Units Accelerate

Hospitals owned 59.64% of installed systems in 2025, leveraging centralized radiology departments and cross-specialty referral networks to maintain patient throughput. These institutions benefit from economies of scale in service contracts and training programs. Stand-alone diagnostic centers comprise a mid-tier segment that attracts cash-pay patients seeking short wait times. Although their aggregate share sits near 25%, expansion has moderated as insurance contracts funnel more volume into integrated hospital pathways.

Mobile screening units represent the most dynamic subsector with an 8.05% CAGR fueled by NHI mandates to reach underserved populations. Transport-grade chassis equipped with onboard generators enable daily clinic rotations across villages lacking electricity access. Early pilots show detection-stage migration toward stage I diagnoses, supplying hard evidence for cost-effectiveness claims. Equipment suppliers that pair rugged hardware with cloud-based image archiving gain a competitive edge because mobile setups rely heavily on teleradiology reads. Consequently, the South Africa mammography market sees diversified revenue streams where hospital renewals guarantee base volume and mobile fleets drive incremental growth.

Geography Analysis

Gauteng alone hosts nearly one-third of active units, buoyed by Johannesburg’s cluster of tertiary hospitals and private oncology centers. Western Cape follows with Cape Town-based academic hospitals that often act as pilot sites for 3-D tomosynthesis studies. KwaZulu-Natal ranks third and benefits from a provincial cancer-registry initiative that allocates dedicated screening budgets. Collectively these provinces anchor core demand for high-specification systems and advanced AI modules.

Eastern Cape, Limpopo, Northern Cape, and North West provinces experienced a double-digit rise in mobile unit deployments during 2024–2025 cycles. Rural geography and dispersed population densities make fixed-site clinics less feasible, so provincial departments emphasize mobile fleets to meet NHI coverage ratios. The South Africa mammography market size allocated to rural mobile programs is small in absolute dollars yet shows the highest forward CAGR, indicating sustained vendor interest despite lower margins.

Inter-provincial procurement schemes are moving toward pooled tenders that stipulate common service-level agreements, aiming to standardize uptime metrics across the national grid. Vendors with province-wide service depots and bilingual training teams score higher on tender evaluations. Geography thus shapes competitive dynamics as keenly as technology specifications, driving manufacturers to invest in logistics hubs beyond major metros.

Competitive Landscape

The market hosts a mix of global imaging majors, mid-sized European manufacturers, and locally anchored distributors. Top vendors collectively account for less than 60% of installed base, signifying moderate concentration. Global players leverage broad product portfolios and existing CT or MRI footprints to cross-sell mammography units. Their advantage lies in established SAHPRA dossiers and in-country engineering teams capable of 24-hour response.

Mid-tier firms differentiate on price and service flexibility, often bundling extended warranties and remote-diagnostic dashboards. These suppliers win share in tenders where total-cost-of-ownership scoring outweighs brand prestige. Local distributors add value via import-duty optimization and rapid parts sourcing, especially in provinces distant from Johannesburg customs depots.

Competitive intensity is shifting toward AI partnerships. Vendors embedding FDA-cleared algorithms earn RFP bonus points for workflow efficiency. For example, one leading supplier bundled a triage algorithm that reduced radiologist read time by one-third at a Durban pilot site, a result now referenced in multiple public-sector tenders. Protection of intellectual property and robust cybersecurity protocols have therefore become principal differentiators alongside detector sensitivity.

South Africa Mammography Industry Leaders

Siemens AG

GE Healthcare

Fujifilm Holdings Corporation

Hologic Inc.

Planmed OY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Radhiant Diagnostic Imaging SA Inc., founded by Dr. Anith Chacko, launched the country’s first fully mobile mammography service to reach women in underserved rural regions.

- July 2024: Rio Tinto and Richards Bay Minerals teamed with NGO PinkDrive to deliver two-week screening campaigns across KwaZulu-Natal and Eastern Cape in celebration of Mandela Month.

- April 2024: The RSNA and GE HealthCare supplied mammography technology and training to Muhimbili National Hospital in Tanzania to bolster regional early-detection capacity.

South Africa Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. South Africa Mammography Market is segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End Users (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Breast Tomosynthesis |

| Others |

By Technology

| 2-D Full-Field Digital Mammography |

| 3-D Digital Breast Tomosynthesis |

| Others |

By End User

| Hospitals |

| Stand-alone Diagnostic Centres |

| Mobile Screening Units |

| By Product Type | Digital Systems |

| Analog Systems | |

| Breast Tomosynthesis | |

| Others | |

| By Technology | 2-D Full-Field Digital Mammography |

| 3-D Digital Breast Tomosynthesis | |

| Others | |

| By End User | Hospitals |

| Stand-alone Diagnostic Centres | |

| Mobile Screening Units |

Key Questions Answered in the Report

How big is the South Africa Mammography Market?

The South Africa Mammography Market size is expected to reach USD 27.67 million in 2026 and grow at a CAGR of 6.94% to reach USD 38.7 million by 2031.

Which product segment is expanding the quickest?

Breast tomosynthesis systems are advancing at a 7.86% CAGR, making them the fastest-growing product category.

Who are the key players in South Africa Mammography Market?

Siemens AG, GE Healthcare, Fujifilm Holdings Corporation, Hologic Inc. and Planmed OY are the major companies operating in the South Africa Mammography Market.

Why are mobile screening units important?

Mobile units extend breast-cancer screening to rural provinces where fixed facilities are scarce, and they are forecast to grow at an 8.05% CAGR.

Page last updated on: