Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

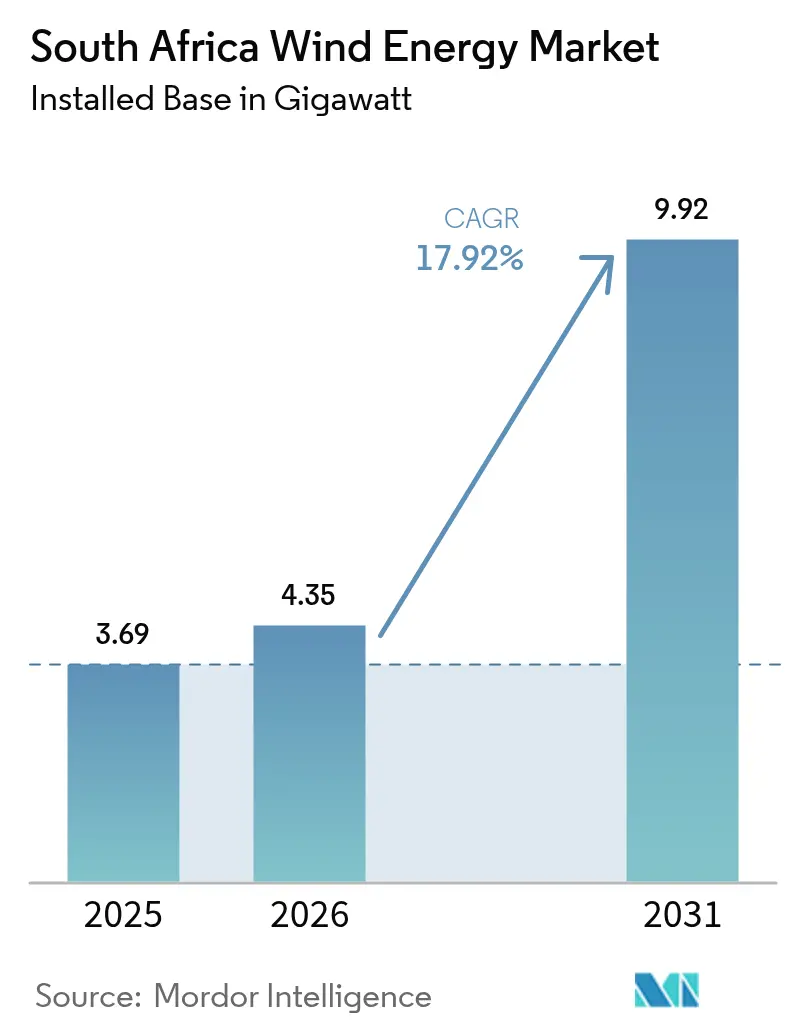

| Base Year Market Size (2025) | 3.69 gigawatt |

| Market Volume (2026) | 4.35 gigawatt |

| Market Volume (2031) | 9.92 gigawatt |

| Growth Rate (2026 - 2031) | 17.92% CAGR |

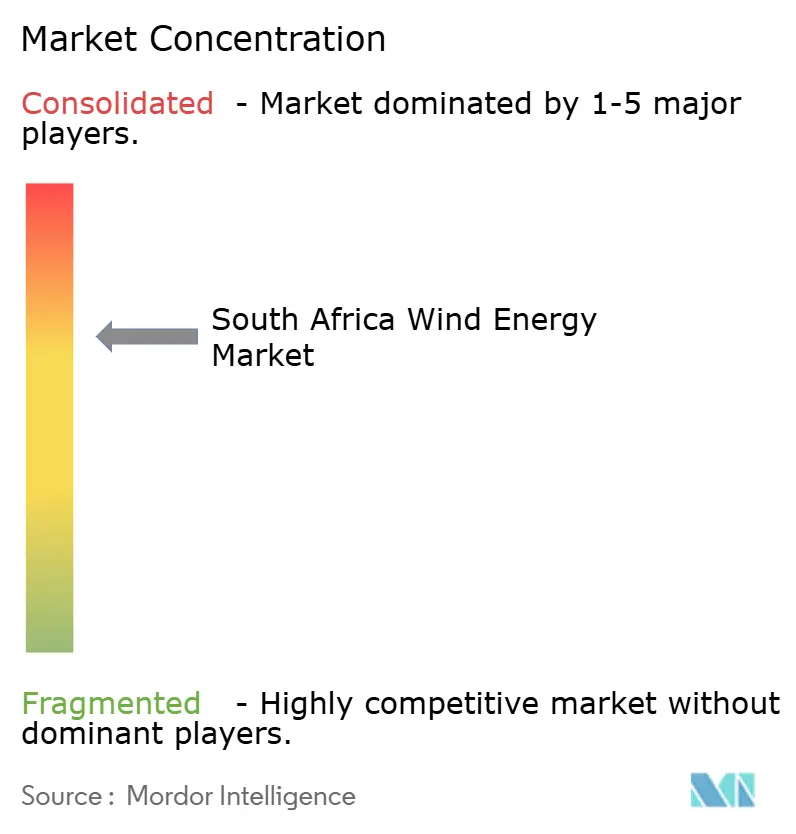

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Wind Energy Market Analysis by Mordor Intelligence

The South Africa Wind Energy Market size was valued at 3.69 gigawatt in 2025 and estimated to grow from 4.35 gigawatt in 2026 to reach 9.92 gigawatt by 2031, at a CAGR of 17.92% during the forecast period (2026-2031).

Policy reforms that eliminated the 100 MW cap on distributed generation, the legalization of competitive wholesale trading, and the surge in corporate PPAs have redirected investment away from Eskom-only procurement toward private offtake. Transmission constraints in the Northern and Western Cape still temper the deployment speed, yet local-content incentives and a maturing wheeling framework are strengthening domestic manufacturing and financing ecosystems. Competitive intensity is rising as Chinese OEMs leverage turbine-plus-financing packages while European suppliers defend premium pricing through service networks. Overall, the South Africa wind energy market is advancing from a policy-led to an infrastructure-constrained growth phase, where grid reinforcement and streamlined permitting are the decisive variables.

Key Report Takeaways

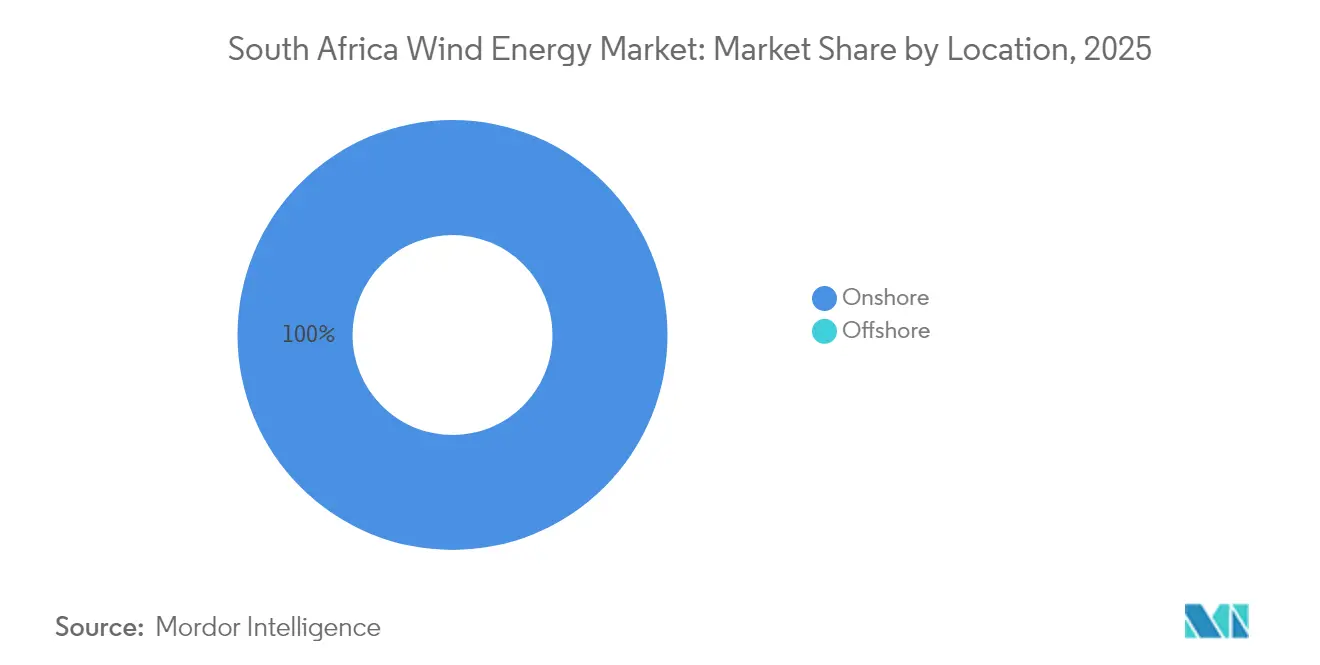

- By location, onshore installations accounted for 100.00% of the South Africa wind energy market share in 2025, while offshore remains at the feasibility stage, leaving onshore to expand at an 17.86% CAGR through 2031.

- By turbine capacity, platforms rated 3-6 MW commanded 55.80% of the South Africa wind energy market size in 2025; the Above 6 MW class is forecast to lead growth at a 20.12% CAGR to 2031.

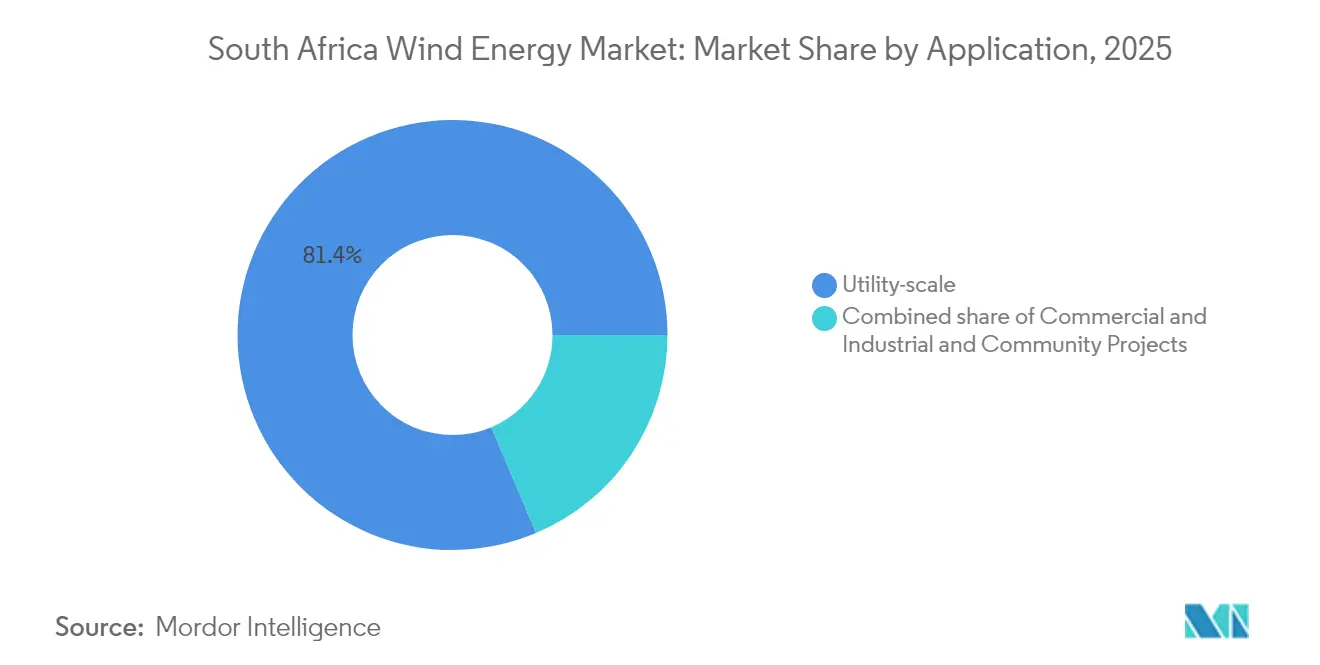

- By application, utility-scale projects held 81.35% share of the South Africa wind energy market size in 2025 and are projected to grow at a 19.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IRP-2019 wind quota of 1.6 GW/yr ensures steady pipeline | +3.2% | Northern Cape, Eastern Cape, Western Cape | Medium term (2-4 years) |

| Rapid LCOE decline keeps wind cheaper than new coal & CCGT | +2.8% | National, strongest in Mpumalanga and KwaZulu-Natal | Short term (≤ 2 years) |

| REIPPPP auctions unlocking > 7 GW private investment | +4.1% | National, project clusters in Cape provinces | Medium term (2-4 years) |

| Surge in corporate-PPA wheeling deals post-2024 grid code | +3.5% | Mining belts in Limpopo & North West, industrial zones nationwide | Short term (≤ 2 years) |

| Transmission-company spin-off unlocks grid-expansion finance | +2.3% | Cape transmission corridors | Long term (≥ 4 years) |

| Local-content incentives under 2025 Renewable-Energy Masterplan | +1.9% | Manufacturing hubs in Eastern Cape | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IRP-2019 Wind Quota of 1.6 GW/yr Ensures Steady Pipeline

A fixed 1.6 GW annual procurement target gives developers visibility to lock in turbine supply, negotiate debt at tighter spreads, and shorten construction cycles, contrasting with earlier stop-start bid windows.[1]Global Wind Energy Council, “Global Wind Report 2025,” GWEC.NET The quota’s Cape-province focus aligns grid reinforcement priorities with the highest capacity-factor zones, encouraging efficient capital deployment. Draft IRP-2024 scenarios raise cumulative wind ambition to as high as 76 GW by 2050, yet near-term momentum still hinges on timely auction calendars. Predictability is already compressing project development timelines by up to nine months as financiers view repeatable bid rounds as lower-risk. This certainty is also stimulating domestic tower fabrication commitments in Humansdorp.

Rapid LCOE Decline Keeps Wind Cheaper Than New Coal & CCGT

Onshore wind’s LCOE has fallen to USD 40-50 / MWh, far below new coal and gas alternatives when carbon costs are included.[2]International Renewable Energy Agency, “Floating Offshore Wind Outlook,” IRENA.ORG Turbine scaling to 5-6 MW machines with 180 m rotors lifts capacity factors in South Africa’s coastal regimes to 35-45%. Mining majors such as Rio Tinto now secure 20-year PPAs priced beneath Eskom’s escalating tariffs, using wind as a hedge against price inflation and emissions compliance. The cost gap is widening as coal plants confront retrofit expenses, while wind projects see negligible variable costs post-commissioning. Declining costs also underpin the economics of hybrid wind-battery plants that can arbitrage curtailment periods.

REIPPPP Auctions Unlocking > 7 GW Private Investment

Since 2011, the REIPPPP scheme has contracted more than 7 GW of wind, with 3.34 GW already online and Bid Window 5 projects moving toward financial close. The Electricity Regulation Amendment Act restores confidence by mandating transparent timelines following earlier delays that forced tariff renegotiations. Local lenders such as Standard Bank and DBSA financed the 380 MW Overberg facility at competitive rates, proving domestic appetite when grid and offtake risks are mitigated.[3]Development Bank of Southern Africa, “DBSA Finances South Africa’s Largest Wind Farm,” DBSA.ORG Revived auctions are expected to re-activate idle manufacturing capacity and attract foreign equity partners.

Surge in Corporate-PPA Wheeling Deals Post-2024 Grid Code

Operationalization of the National Wheeling Framework in January 2025 triggered at least 1.94 GW of announced private-offtake wind deals, notably Cennergi’s 140 MW agreement with Northam Platinum that transports power across Eskom’s network at wheeling tariffs near ZAR 0.12/kWh. Aggregators such as NOA Group reduce transaction costs by bundling generation and distributing it to multiple buyers. Early adopters report 15-20% savings versus grid supply, prompting copy-cat deals among ferrochrome and cement producers. Improved revenue certainty is expanding the South Africa wind energy market by broadening the buyer universe beyond Eskom.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cape-province grid congestion & queue backlogs | -2.7% | Northern Cape, Eastern Cape, Western Cape | Short term (≤ 2 years) |

| Lengthy EIA & land-use permitting timelines | -1.5% | National, with delays concentrated in coastal zones and protected areas | Medium term (2-4 years) |

| Policy uncertainty around IRP-2023 draft revisions | -1.8% | National, affecting procurement pipeline and investor confidence | Medium term (2-4 years) |

| Rising mid-day curtailment risk from rooftop-solar oversupply | -1.2% | Cape provinces and Gauteng, where rooftop solar penetration exceeds 15% | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cape-Province Grid Congestion & Queue Backlogs

Curtailment climbed to 307 GWh in 2024 and already exceeds 403 GWh in 2025 as saturated corridors force grid operators to prioritize conventional generation. Connection queues lack transparency, leaving new developers facing three-year waits even after permits. Projects with legacy allocations enjoy priority, producing a two-tier market that dampens competition. Frequency excursions tied to rising inverter-based penetration have led NTCSA to tighten grid-code rules, raising project costs. Although the Independent Transmission Projects model promises relief, tariff-recovery mechanisms remain untested.

Lengthy EIA & Land-Use Permitting Timelines

EIAs average 18-24 months and can stretch beyond 30 months for sites intersecting bird corridors or heritage zones. Multi-agency reviews invite appeals that delay financial close and favor experienced developers with deeper capital reserves. Communal land tenure in the Eastern Cape further complicates acquisition, requiring protracted negotiations with traditional authorities. Aviation-lighting requirements introduced in 2024 added blade-patterning costs and technical reviews, extending procurement schedules. Industry proposals for standardized low-risk site protocols remain unimplemented, perpetuating bottlenecks that hold back the South Africa wind energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Onshore Dominance, Offshore Nascent

Onshore capacity totaled 3.69 GW in 2025, capturing the entire South Africa wind energy market share, and is projected to expand at an 17.86% CAGR as developers exploit 35-45% capacity factors along the Cape coastline. Proven resource data, existing transmission nodes, and standardized permitting templates shorten project cycles, making onshore the low-risk growth avenue. Balance-of-plant savings from larger turbines further enhance onshore economics, consolidating its primacy within the South Africa wind energy market.

A fledgling offshore segment is emerging through feasibility studies on floating platforms off KwaZulu-Natal, yet it contributes 0.00% to the South Africa wind energy market size today. Deep waters, absence of leasing regulations, and port-infrastructure gaps keep commercial deployment unlikely before 2035. Nonetheless, the Agulhas Current offers high and consistent wind speeds that could one day diversify geographic risk away from constrained onshore corridors.

By Turbine Capacity: Scaling Toward 6+ MW Platforms

Machines rated 3-6 MW dominated installations with a 55.80% South Africa wind energy market share in 2025, leveraging proven platforms such as Vestas V150-4.2 MW. The Above 6 MW segment, however, is accelerating at a 20.12% CAGR, reflecting developers’ pursuit of economies of scale and grid operators’ preference for fewer interconnection points. Goldwind’s 6.2 MW units at the 380 MW Overberg cluster exemplify this trend, yielding 15-20% more annual energy per turbine.

Transitioning to larger rotors reshapes logistics and supply-chain demands, requiring blade-handling infrastructure and specialized transport. The South Africa wind energy market size for turbines above 6 MW is benefiting from localized tower fabrication that offsets transport complexity. Grid-code updates mandating advanced power electronics also favor the newest high-capacity machines, reinforcing the migration to 6-8 MW platforms.

By Application: Utility-Scale Leads, C&I Gains Traction

Utility-scale projects held 81.35% of installed capacity in 2025 and are projected to expand at a 19.08% CAGR, underpinning the bulk of the South Africa wind energy market size. Large PPAs such as Richards Bay Minerals’ 230 MW offtake from Overberg illustrate how single-buyer demand can underwrite multi-hundred-megawatt plants. Standardized contracts and lender familiarity minimize transaction costs and attract foreign equity.

Commercial and industrial buyers are accelerating adoption through wheeling, shrinking Eskom exposure, and meeting decarbonization mandates. The Cennergi–Northam Platinum deal highlights cost savings and risk hedging achievable for mid-tier users. Community projects remain marginal due to financing hurdles, yet transformation targets in the Renewable-Energy Masterplan could unlock concessional funding that broadens participation, adding resilience to the South Africa wind energy market.

Geography Analysis

South Africa’s wind fleet is concentrated in the Northern, Eastern, and Western Cape provinces, jointly hosting more than 90% of capacity due to 8 m/s wind speeds and existing 400 kV lines. The Northern Cape leads the pipeline with projects like Scatec’s Kenhardt hybrid, yet its Aries and Hydra nodes are curtailment hotspots, spilling over 150 GWh in 2024. NTCSA’s 765 kV backbone proposal aims to reroute surplus to Gauteng by 2029, potentially unlocking 5-7 GW of new capacity.

The Eastern Cape benefits from Coega port logistics and a skilled manufacturing base pivoting from automotive to renewable components. Nordex’s Humansdorp facility signals the rise of a localized tower supply chain. However, biodiversity safeguards within the Cape Floral Kingdom lengthen EIA reviews, elevating development risk. The Western Cape’s proximity to Cape Town’s load centers reduces wheeling fees, making projects such as Overberg attractive to corporate buyers despite stricter environmental protocols.

Mpumalanga, historically coal-dependent, is emerging through Seriti Green’s 900 MW wind plan, aligning with the Just Energy Transition and repurposing mine land. KwaZulu-Natal’s deepwater offshore prospect remains speculative, pending leasing rules. Limpopo and North West host wheeling-based projects feeding platinum and ferrochrome plants, demonstrating that grid-rich but wind-moderate regions can still contribute incremental growth through private PPA structures.

Regulatory Landscape

South Africa's wind buildout is governed by a mix of national planning, procurement rules, and market-opening legislation. The Electricity Regulation Amendment Act (2024) formalized the move toward competitive electricity trading and underpins the role of the National Transmission Company South Africa (NTCSA) as the transmission system operator, while the Integrated Resource Plan (IRP 2025) remains the primary national capacity-planning framework for new generation, including wind allocations.

Project authorizations continue to run through the National Energy Regulator of South Africa (NERSA) via generation licensing and registration pathways, with stated processing timelines (for complete applications) used by developers and lenders to plan financial close. Public-sector procurement remains centered on the DMRE-led REIPPPP program (with Bid Window 7 bidders identified by December 2025), while industrial policy support is framed by the South African Renewable Energy Masterplan (SAREM), approved by Cabinet in March 2025, which links bid and localization requirements to the development of domestic wind component value chains.

Competitive Landscape

Vestas, Siemens Gamesa, and Nordex collectively hold roughly 60% of cumulative installations, underpinning a moderately concentrated market. Chinese OEMs, led by Goldwind, are rapidly gaining share by bundling equipment, EPC, and concessional finance. Goldwind’s Johannesburg service center addresses historic concerns over after-sales support, narrowing European suppliers’ advantage. Price competition is now supplemented by digital-service differentiation, with Vestas GridStreamer and Siemens Gamesa PowerBoost specified in NERSA filings to satisfy stricter grid-code demands.

Developer consolidation is intensifying as smaller IPPs exit due to grid-access hurdles, creating acquisition opportunities for Mainstream Renewable Power and Enel Green Power. Energy traders such as NOA Group introduce flexibility by decoupling generation from single-buyer PPAs, fostering a secondary market for offtake contracts. Hybrid wind-battery projects, like Oya Energy’s 86 MW wind component paired with 92 MW/242 MWh storage, illustrate new competitive niches where value comes from dispatchable renewable power.

South Africa Wind Energy Industry Leaders

Nordex SE

Vestas Wind Systems A/S

Siemens Gamesa Renewable Energy SA

Enel Green Power SpA

Mainstream Renewable Power Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Corporate and industrial offtake continues to open whitespace for utility-scale wind that is not solely dependent on Eskom-backed procurement, especially where wheeling structures can move energy from high-resource Cape sites to load centers. A visible proof point is Enel Green Power RSA bringing the 330 MW Impofu Wind Farm cluster into commercial operation in 2026 underpinned by long-term PPAs with Sasol and Air Liquide, reinforcing the bankability of private offtake and multi-site wind clusters.

System constraints and policy responses are shaping near-term opportunity areas around grid access and dispatchability. Western Cape and Eastern Cape grid capacity limitations are highlighted as a primary bottleneck, directing developer focus to projects with earlier grid allocations, hybridization, and congestion-mitigation solutions that can better fit within available network headroom. In parallel, SAREM (Cabinet-approved in March 2025) provides a framework for local manufacturing and services expansion (towers, blades, balance-of-plant, O&M) tied to renewable deployment, while the IRP 2025 wind build targets and the cited advanced wind project pipeline (around 17 GW) indicate a large addressable project funnel once transmission expansions and queue management translate into actionable connection capacity.

Recent Industry Developments

- June 2026: Enel Green Power RSA brought online the 330 MW Impofu Wind Farm cluster in the Eastern Cape, comprising three 110 MW facilities (Impofu North, Impofu East, and Impofu West). The project is anchored by long-term PPAs with Sasol and Air Liquide, reinforcing the role of private offtake in scaling utility-scale wind outside Eskom-only procurement.

- February 2025: The Ishwati Emoyeni wind farm (140 MW) reached financial close and moved into construction, using 32 Vestas 4.5 MW turbines and aggregated offtake via an energy trader model. The structure broadens the buyer pool for new wind projects by reducing reliance on single-buyer PPAs.

- April 2024: Nordex Group secured orders totaling 295 MW from EDF Renewables for the Koruson 2 cluster (Umsobomvu and Hartebeesthoek wind farms), comprising multiple sites and signaling continued OEM competition for large-scale wind deployment in South Africa.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers wind-based electricity generation assets in South Africa, tracked mainly through installed capacity and new additions, and then linked to build activity and operating performance.

Scope exclusions: We exclude broader renewable power, general grid transmission investments that are not directly tied to wind projects, and downstream electricity retail and trading revenues.

Segmentation Overview

- By Location

- Onshore

- Offshore

- By Turbine Capacity

- Up to 3 MW

- 3 to 6 MW

- Above 6 MW

- By Application

- Utility-scale

- Commercial and Industrial

- Community Projects

- By Component (Qualitative Analysis)

- Nacelle/Turbine

- Blade

- Tower

- Generator and Gearbox

- Balance-of-System

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public energy and power-system references to anchor the demand and build pipeline, including national energy planning publications, grid connection disclosures, and permitting or auction documentation where available. We also used global and local sources such as IRENA statistics, International Energy Agency datasets, World Bank macro indicators, and peer-reviewed articles focused on South Africa wind resource and capacity factors.

To translate capacity movement into a consistent market view, we screened company annual reports, investor presentations, and project announcements to understand timelines, commissioning dates, and the turbine ratings used in recent builds. Supporting checks were pulled from a paid subscription for company financials and intelligence and, where import dependence mattered, from a shipment-level import and export database to infer equipment flow timing. These sources are illustrative only, and many other public references were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with developers, EPC and O&M participants, component distributors, and large power buyers, along with independent specialists who track auctions and private procurement. Inputs were used to confirm commissioning slippage, grid constraint impact by corridor, typical capacity factors, and practical pricing trends for turbine supply, balance of plant, and long-term service, so desk assumptions did not remain untested.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 18% | |

| Mid tier: 47% | Functional/Unit leaders: 37% | |

| Smaller Players: 20% | Managers: 45% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the national wind capacity base is reconstructed year by year from the installed base, retirements (if any), and commissioning additions, then stress-tested against what is realistically connectable to the grid in the period. Bottom-up checks were used selectively, including a sampled roll-up of announced projects by COD window and approximate MW, followed by a reasonableness check using typical MW per project and observed procurement cadence.

A few market fingerprints were treated as key inputs, including installed capacity in MW, annual additions by project status, auction versus private offtake share shifts, average turbine nameplate ratings used in new builds, typical capacity factors by wind corridors, and grid availability signals that change effective commissioning. Forecasting relied on scenario analysis with a central case, because build-out is shaped by policy rounds, private procurement timing, and connection constraints more than by smooth time-series patterns. When project or pricing details were missing, gaps were handled with conservative assumptions based on comparable South Africa projects and then adjusted after primary checks validated what was achievable in the next 2 to 5 years.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals, including published capacity totals, observed commissioning announcements, and the implied build rate versus known grid constraints. If a year showed an unusual jump or dip, the drivers were re-reviewed, and follow-up calls were triggered to confirm whether it was a data issue or a real market shift.

A multi-step internal review is followed so assumptions, unit handling, and conversions are consistent from history to forecast. The study is refreshed annually, and interim updates are made when material events occur, such as new procurement rounds, major policy changes, or a clear revision in connection availability. Before delivery, a final analyst pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's South Africa Wind Energy Market Size Measured Against Other Published Estimates

Published market sizes can differ a lot in this space because some authors report capacity in MW or GW, while others report investment value, and the year used for the snapshot is not always aligned. Differences also show up when one estimate counts only utility-scale grid supply, but another includes broader component spending or regional value-add assumptions.

In South Africa, a common gap driver is whether the number tracks installed and commissioned capacity, or whether it tries to price the full project ecosystem using assumed capex per MW and local content, which can swing totals when currency timing and inflation are handled differently. The other big swing factor is how the pipeline is treated, since projects in procurement or with grid constraints can be pulled into the forecast too early, which then lifts the near-term market size.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.69 B (2025) | |

| Global Report Aggregator A | USD 1.22 B (2023) | This estimate is value-based and tied to an earlier base year, and it appears to include component and infrastructure value assumptions that do not map one-to-one with installed capacity movement in the same way. |

| Industry Publisher B | USD 4.90 B (2024) | This figure is presented as a wind farms value number, which can embed project capex intensity assumptions and different onshore versus offshore treatment, thereby pushing totals above a capacity-led build-out view. |

The table shows that the spread is mostly explained by unit choice, base year selection, and whether spending is modeled from assumed capex per MW versus tracking the installed capacity base and additions. By keeping the core sizing tied to installed capacity movement and then checking the build rate against grid connection reality, the result stays closer to what is actually commissioned, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

How fast is South Africa's wind capacity expected to grow by 2031?

Installed capacity is projected to rise from 4.35 GW in 2026 to 9.92 GW by 2031 at an 17.92% CAGR.

What is driving corporate demand for wind power in South Africa?

Grid-code reforms now permit wheeling, enabling mining and industrial firms to lock in fixed-price PPAs that undercut Eskom tariffs by up to 20%.

Which turbine class is expanding the quickest?

Above 6 MW turbines are growing at a 20.12% CAGR as developers favor scale economies and grid operators seek fewer connection points.

Where are the main geographic bottlenecks for new wind projects?

The Northern and Western Cape provinces suffer from transmission congestion, causing hundreds of GWh in curtailment each year.

How is local manufacturing being promoted?

The 2025 Renewable-Energy Masterplan offers preferential bid scores and duty relief, pushing towers, blades, and balance-of-plant toward 40-60% local content by 2025.

What role do hybrids play in the market?

Projects coupling wind with batteries, such as Oya Energy's hybrid, mitigate curtailment risk and supply dispatchable renewable power to industrial buyers.

Page last updated on: