Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

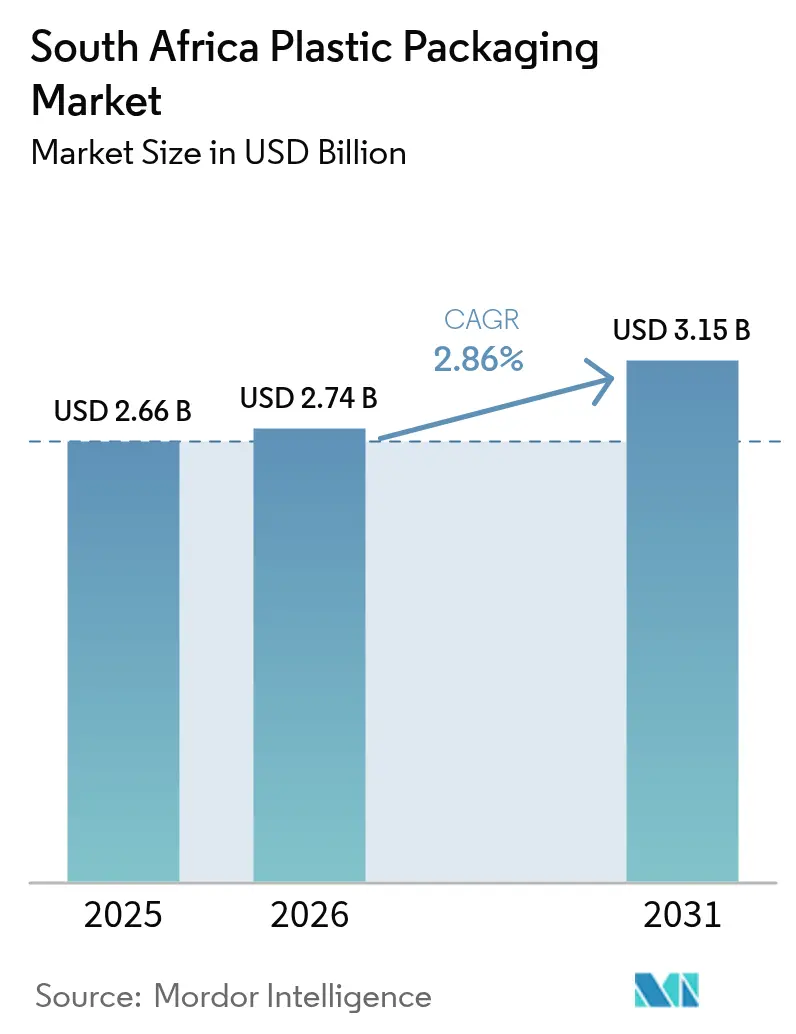

| Base Year Market Size (2025) | USD 2.66 Billion |

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 2.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Plastic Packaging Market Analysis by Mordor Intelligence

The South Africa plastic packaging market size was valued at USD 2.66 billion in 2025 and estimated to grow from USD 2.74 billion in 2026 to reach USD 3.16 billion by 2031, at a CAGR of 2.86% during the forecast period (2026-2031). Higher logistics activity, tighter recycled-content rules, and chronic electricity shortages are reshaping cost structures and competitive positioning throughout the value chain. Large converters are installing solar or backup power and integrating recycling plants to secure feedstock, whereas small and medium enterprises face escalating input costs and rising compliance fees. Regulatory pressure to close the circularity gap is steering brand owners toward mono-material flexible packs and bio-based alternatives, creating premium niches for innovation. Meanwhile, imported films and preforms from Asia intensify price competition, accelerating consolidation as scale becomes the primary hedge against margin compression.

Key Report Takeaways

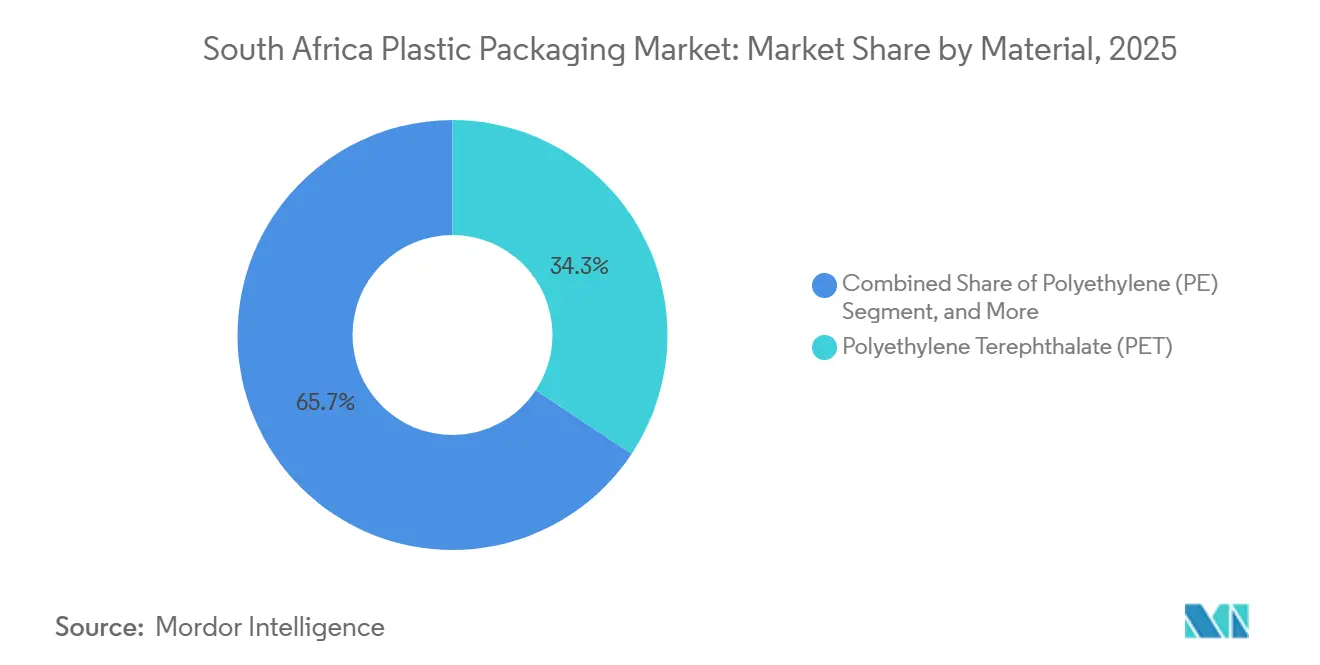

- By material, polyethylene terephthalate led with 34.32% of South Africa plastic packaging market share in 2025.

- By product type, bottles and jars accounted for 41.98% of revenue in 2025, while films and wraps are projected to expand at a 4.07% CAGR through 2031.

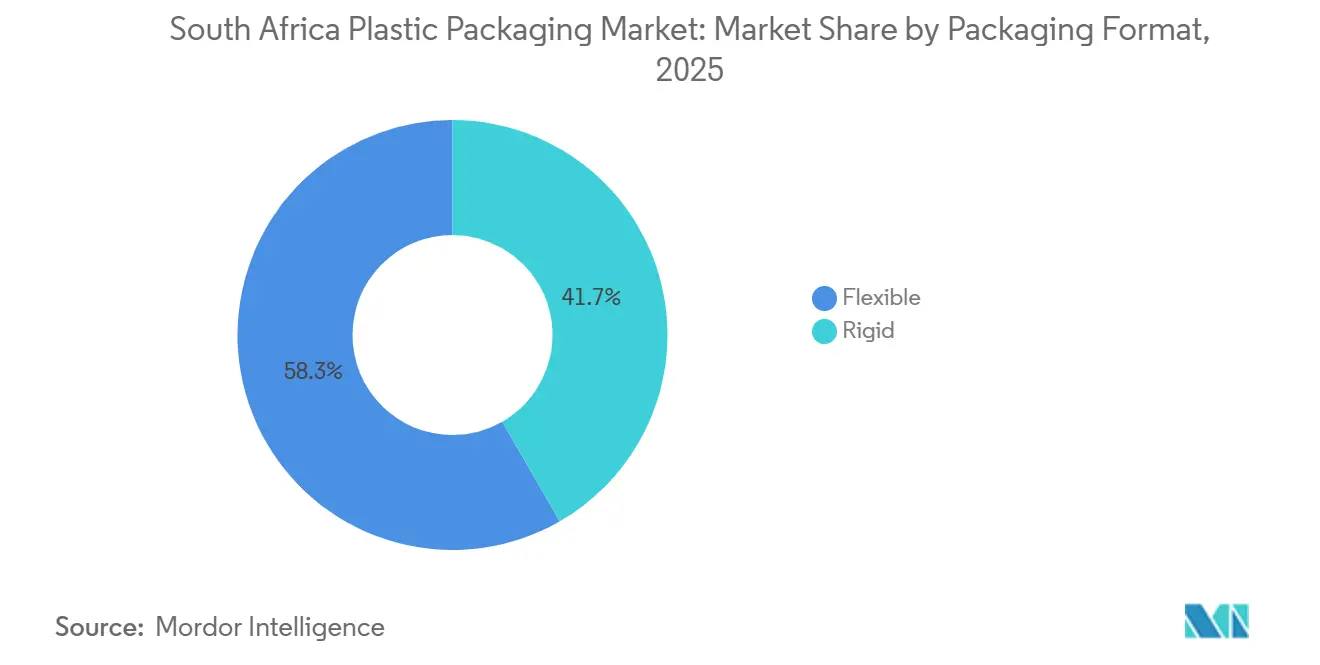

- By packaging format, flexible formats captured 58.31% of the South Africa plastic packaging market size in 2025 and are forecast to grow at a 3.32% CAGR to 2031.

- By end-user industry, food applications accounted for 39.21% of demand in 2025, whereas personal and home care is advancing at a 3.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Consumer Goods | +0.8% | Gauteng, Western Cape, KwaZulu-Natal urban centers | Medium term (2-4 years) |

| Favourable Material Properties of Plastics | +0.5% | National | Long term (≥ 4 years) |

| Expansion of E-commerce Logistics and Last-mile Delivery | +0.9% | Johannesburg, Cape Town, Durban metros | Short term (≤ 2 years) |

| Localisation Incentives under South Africa's Industrial Policy | +0.4% | Special Economic Zones and industrial corridors | Medium term (2-4 years) |

| Surge in Cannabis-derived Food and Pharma Packaging | +0.1% | Pharmaceutical facilities | Short term (≤ 2 years) |

| Rising Adoption of Mono-material Flexible Packs for Recyclability | +0.6% | Export-oriented FMCG producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Consumer Goods

Urban population growth and rising middle-income consumption in Gauteng, the Western Cape, and KwaZulu-Natal underpin sustained volume for food, beverage, and personal-care packs.[1]Statista, “E-commerce in South Africa,” STATISTA.COM Online retail platforms are forecast to serve nearly 38 million domestic users by 2027, driving higher throughput for pick-and-pack converters focused on short-run customization. Yet offshore direct-to-consumer parcels arrive pre-packed in foreign-made mailers, forcing local producers to compete on lead time, design agility, and value-added printing rather than on pure cost. Consumer research indicates that shoppers facing cost-of-living stress tolerate green premiums only when performance and price align, so recyclable or bio-based formats must target parity on shelf.[2]PwC South Africa, “Voice of the Consumer 2025,” PWC.CO.ZA

Expansion of E-commerce Logistics and Last-mile Delivery

Meal-kit, grocery, and quick-commerce platforms require moisture-resistant films, robust seals, and tamper-evident features that withstand multiple handling points. Couriers operating motorcycles or bicycles through variable weather favor co-extruded polyethylene wraps coupled with printed polyethylene terephthalate labels that remain legible after rain exposure. Distribution nodes in Johannesburg, Cape Town, and Durban are upgrading to high-speed form-fill-seal lines, stimulating demand for rollstock with laser-scoring and easy-open features. Brand owners now specify packaging line-side certifications such as ISO 22000 and Sedex, rewarding converters that invest in hygienic design and real-time traceability.

Rising Adoption of Mono-material Flexible Packs for Recyclability

Extended Producer Responsibility fees increase each year, incentivizing a shift from multilayer laminates to recyclable mono-polyethylene or polypropylene barriers. The South African Plastics Pact documented early commercial runs that match oxygen- and moisture-barrier performance via metallization or silicon-oxide coatings on mono-polyethylene films. Constantia Flexibles’ EcoLamHighPlus rollstock demonstrates shelf-life parity in dairy and processed-meat applications while satisfying European export rules.[3]Constantia Flexibles, “EcoLamHighPlus,” CFLEX.COM Adoption is tempered by a 15-20% cost premium and limited domestic capacity for recycling metallized film, yet multinational brand-owner mandates are accelerating qualification at top-tier plants.

Favourable Material Properties of Plastics

High clarity, toughness, and lightweight attributes keep polyethylene terephthalate and polyolefins central to beverage, edible oil, and industrial wrap formats. PETCO recorded a 71% bottle recovery rate in 2024, enabling a sizable recycled PET supply that supports closed-loop bottle production. In rigid formats, superior carbonation retention and shatter resistance maintain PET’s advantage over glass, particularly for carbonated soft drinks and flavored waters. Flexible polyethylene films deliver puncture resistance for pallet wrap and agricultural mulch, lowering spoilage and transport emissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Resin Prices and Environmental Concerns | -0.6% | Import-dependent converters | Short term (≤ 2 years) |

| Stricter Regulations on Single-use Plastics | -0.4% | Municipal jurisdictions | Medium term (2-4 years) |

| Electricity Load-shedding Disrupting Production Lines | -0.7% | Gauteng and KwaZulu-Natal hubs | Short term (≤ 2 years) |

| Recycled-resin Supply Constraints from Informal Collection | -0.3% | Urban collection networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Resin Prices and Environmental Concerns

Resin benchmark prices climbed sharply in 2025, with polyethylene terephthalate averaging USD 1.13 per kg, a 27.8% rise year-on-year.[4]ICIS, “Africa PET Price Update October 2025,” ICIS.COM Local converters struggled to absorb surcharges, and at least one major player closed a rigid-packaging mill after prolonged margin pressure. Food-grade recycled PET trades at a further premium because collection volumes remain insufficient, highlighting the cost-sustainability dilemma. Municipal levies on single-use packs compound the stress, forcing price-sensitive consumers toward value formats even as brand owners push greener solutions.

Electricity Load-shedding Disrupting Production Lines

Eskom maintained Stage 5-6 blackouts during peak winter 2025, cutting power several times daily and curtailing extrusion and blow-molding uptime. Diesel generators inflate conversion costs by up to ZAR 1.00 per kg, undermining the competitiveness of domestic film and performance producers. Major multinationals mitigate risk by installing rooftop solar or entering renewable power purchase agreements, yet small converters cannot finance equivalent resilience. Frequent restarts impair quality yields, leading to scrap rates that further erode margins and create delivery backlogs for FMCG contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PET Dominance Faces Bio-based Headwinds

Polyethylene terephthalate (PET) contributed 34.32% of South Africa plastic packaging market in 2025 revenue, underpinning beverage, edible-oil, and thermoform trays that demand clarity and gas-barrier integrity. A mature reverse-logistics network collected 2.29 billion PET containers in 2024, enabling closed-loop bottle-to-bottle production at recyclers integrated with major converters. Cost spikes in virgin resin nudged brand owners toward food-grade recycled PET, but supply remains tight, so price premiums persist. The South African plastic packaging market for PET applications is expected to expand moderately as health-conscious consumers migrate from sugary sodas to flavored waters and functional drinks, which still favor clear packs.

Bio-based and compostable polymers, though still below 1% penetration, are projected to grow 3.82% annually to 2031 as European buyers impose sustainability scorecards on export-oriented suppliers. Domestic universities are piloting smart bio-films with spoilage-indicator pigments, signaling longer-term opportunities. Polyvinyl chloride continues in blister packs for pharmaceuticals, but safety perceptions and recycling hurdles limit wider uptake. Polyolefin demand in flexible films remains buoyant because low melt temperatures cut energy use, an advantage during load-shedding cycles.

By Product Type: Films and Wraps Accelerate on E-commerce Tailwinds

Bottles and jars accounted for 41.98% of South Africa plastic packaging market in 2025 revenue, driven by beverage and personal-care fills. Recent line upgrades at a USD 68 million PET bottle plant added solar-powered capacity that supplies 3.5 billion units a year, underscoring investor confidence in rigid container demand. Nonetheless, films and wraps are advancing at the fastest 4.07% CAGR because online retail favors low-profile, tamper-evident overwraps. The South African plastic packaging market for film categories will benefit from rollstock innovations featuring laser-scored easy-open designs that reduce fulfillment time.

Flexible stand-up pouches are encroaching on the sauce, detergent, and pet-food niches previously dominated by rigid tubs. A recent acquisition of a Gauteng bag maker for ZAR 128 million expands in-house recycling that supplies recycled high-density polyethylene feedstock to support carrier-bag mandates. Looming 100% recycled-content rules for retail bags by 2027 are accelerating consolidation, as scale becomes mandatory to secure feedstock at stable prices.

By Packaging Format: Flexible Formats Capture Lightweighting Premium

Flexible formats accounted for 58.31% share in 2025, a lead explained by 50-70% weight savings that translate to freight and carbon reductions prized by retailers and brand owners. The South African plastic packaging market share for flexible options will widen, as tamper-evident seals and high-definition digital printing enable premium brand storytelling in small footprints. Global players have pledged to lift recycled or renewable content to 30% by 2030, steering capital into local extrusion and film metallization assets.

Rigid packaging retains a foothold where carbonation retention, barrier performance, and on-shelf impact are critical. Yet cost sensitivity, coupled with single-use bottle levies under review, positions refill and lightweight rigid containers as defensive strategies rather than growth engines. Small converters lacking capital for energy-efficient injection equipment face erosion of volumes and may pivot to niche closures or specialty caps.

By End-user Industry: Personal and Home Care Outpaces Food

Food-led demand at 39.21% of South Africa plastic packaging market in 2025, spanning fresh produce wrap, snack films, and vacuum meat packs. High unemployment and food-price inflation cut premium spending, restraining growth in high-barrier multilayer films destined for export meat cuts. The South Africa plastic packaging market size for food may therefore grow below trend until consumer confidence rebounds.

Personal and home care is the fastest-expanding end-user segment, with a 3.81% CAGR, driven by sachet shampoo, travel-size cosmetics, and refillable concentrate packs. Beauty brands adopt recyclable mono-material laminates and integrate QR codes for ingredient transparency, satisfying retailer sustainability scorecards. Pharmaceutical demand holds steady as serialized barcoding becomes mandatory, driving investment in tamper-proof blister films and compliant labeling. E-commerce electronics, industrial wraps, and agricultural films make up the balance, each sensitive to exchange rates and seasonal demand swings.

Geography Analysis

The South Africa plastic packaging market is geographically concentrated in Gauteng, the Western Cape, and KwaZulu-Natal, provinces that host most converters, brand owners, and logistics assets. Gauteng’s industrial corridors around Johannesburg and Pretoria provide proximity to corporate head offices and major FMCG distribution centers, making it the natural launchpad for new pack formats. KwaZulu-Natal’s Durban port processed 2.35 million TEU in 2025, ensuring resin imports and finished-good exports move efficiently to regional markets in Botswana, Namibia, and Mozambique, albeit subject to congestion surcharges in peak season.

Western Cape’s innovation community around Cape Town nurtures pilot lines for bio-based films and smart labels, while wine and horticulture exporters demand high-integrity modified-atmosphere bags that protect premium produce on long-haul routes to Europe. Yet regional electricity shortages affect all three hubs, compelling firms to budget for diesel back-up and pushing rooftop solar penetration above 10 MW across the top ten converters. Smaller provinces, such as the Eastern Cape with its automotive cluster, rely on rigid and technical pack formats linked to component exports, whereas Mpumalanga focuses on agricultural mulch and silage films tied to grain production cycles.

Cross-border trade agreements inside the Southern African Development Community open modest yet consistent outlets for flexible sacks and shrink sleeves shipped to Zimbabwe and Zambia. Export volumes remain low relative to domestic consumption, but stringent EU circular-economy requirements attach to canned fruit and wine consignments, motivating pack redesign toward mono-material or recycled-content compliance. Municipal enforcement of carrier-bag by-laws varies: Cape Town levies fines up to ZAR 10 million for non-compliance, but inland municipalities lack inspectors, creating a patchwork that rewards national chains able to harmonize specifications and source compliant suppliers.

Competitive Landscape

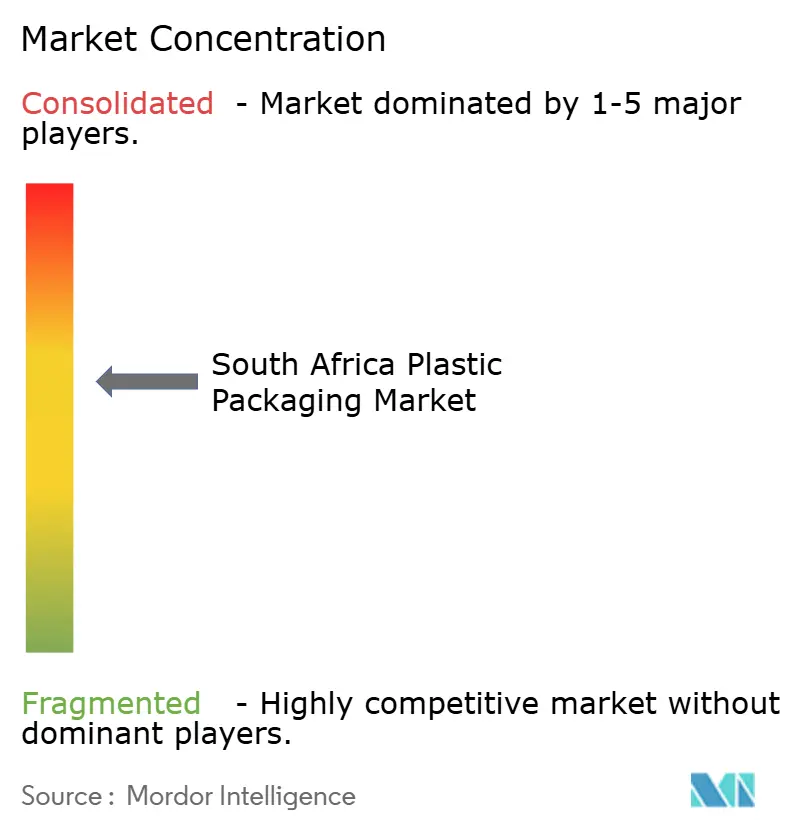

Competitive dynamics in the South Africa plastic packaging market sit midway between fragmentation and consolidation. The ten largest converters together account for just under 50% of value, leaving room for niche specialists and contract converters. Multinationals such as Amcor, Mondi, Constantia Flexibles, and Sealed Air leverage global R and D pipelines to localize high-barrier films and recyclable laminates, often bundling supply across multiple African markets to secure scale contracts. Domestic majors Nampak and Mpact pursue vertical integration: Mpact’s recycling arm produces 144 000 tonnes of PET flake annually, feeding its bottle operations and insulating the group from virgin-resin shocks.

Private capital is accelerating consolidation. A February 2026 deal saw RMB Corvest and Alito Fund 2 acquire a controlling stake in flexible-pack producer Packaging World, banking on premium FMCG clients and growth in recyclable pouches. Earlier, Transpaco purchased Premier Plastics for ZAR 128 million, adding carrier-bag and recycled-polyethylene expertise. The Competition Commission cleared Amcor’s plan to buy Berry Global’s local assets in March 2025, signalling official tolerance for consolidation provided small-business set-asides remain intact.

Strategically, leading firms expand renewable power, digital printing, and smart-packaging features such as NFC tags for refill tracking. Scale remains the chief defense against resin volatility and load-shedding downtime, yet innovation niches persist. Start-ups developing bio-based films partner with universities to tap grant funding, while tech platforms integrate informal waste reclaimers to secure recycled feedstock. The USD 68 million Ballito recycled-PET plant anchors local high-grade flake supply but still meets only a fraction of forecast demand, indicating further capacity announcements are likely.

South Africa Plastic Packaging Industry Leaders

Amcor plc

Nampak Ltd

Mpact Ltd

Constantia Flexibles GmbH

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: RMB Corvest and Alito Fund 2 bought a majority stake in Packaging World to accelerate recyclable-pouch penetration.

- February 2026: Mpact confirmed the closure of its Springs mill, retrenching nearly 400 employees amid import pressure.

- November 2025: Transpaco acquired Premier Plastics for ZAR 128 million, effective Jul 2025, broadening its retail carrier-bag footprint.

- July 2025: Tetra Pak committed new capital for localizing carton supply and expanding recycling partnerships.

South Africa Plastic Packaging Market Report Scope

The South Africa Plastic Packaging Market Report is Segmented by Material (Polyethylene, Polypropylene, Polyvinyl Chloride, Polyethylene Terephthalate, Other Materials), Product Type (Bottles and Jars, Pouches, Bags, Films and Wraps, Other Product Types), Packaging Format (Rigid, Flexible), End-user Industry (Food, Beverages, Healthcare and Pharmaceuticals, Personal and Home Care, Other End-user Industries), and Geography (South Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyvinyl Chloride (PVC) |

| Polyethylene Terephthalate (PET) |

| Other Materials |

By Product Type

| Bottles and Jars |

| Pouches |

| Bags |

| Films and Wraps |

| Other Product Types |

By Packaging Format

| Rigid |

| Flexible |

By End-user Industry

| Food |

| Beverages |

| Healthcare and Pharmaceuticals |

| Personal and Home Care |

| Other End-user Industries |

| By Material | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyvinyl Chloride (PVC) | |

| Polyethylene Terephthalate (PET) | |

| Other Materials | |

| By Product Type | Bottles and Jars |

| Pouches | |

| Bags | |

| Films and Wraps | |

| Other Product Types | |

| By Packaging Format | Rigid |

| Flexible | |

| By End-user Industry | Food |

| Beverages | |

| Healthcare and Pharmaceuticals | |

| Personal and Home Care | |

| Other End-user Industries |

Key Questions Answered in the Report

How large will the South Africa plastic packaging market be in 2031?

It is projected to reach USD 3.16 billion by 2031, advancing at a 2.86% CAGR from 2026.

Which material currently leads demand in South African plastic packs?

Polyethylene terephthalate holds the lead with 34.32% revenue share because clarity and barrier properties meet beverage requirements.

Why are flexible formats growing faster than rigid ones?

Flexible packs deliver 50-70% weight savings, lower freight emissions, and comply more easily with recycled-content rules, driving a 3.32% CAGR to 2031.

What is the fastest-growing end-use segment?

Personal and home care packaging is expanding at a 3.81% CAGR thanks to sachets, trial sizes, and refill pouch innovations.

How does electricity load-shedding affect packaging converters?

Intermittent power cuts force plants onto diesel generators, adding up to ZAR 1.00 per kg in extra cost and reducing uptime, which compresses margins for smaller firms.

Which policy is accelerating adoption of mono-material flexible films?

South Africa’s Extended Producer Responsibility regulations impose escalating fees that reward recyclable mono-material formats over multilayer laminates.

Page last updated on: