Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.02 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Metal Packaging Market Analysis by Mordor Intelligence

The South Africa metal packaging market size was valued at USD 1.02 billion in 2025 and estimated to grow from USD 1.06 billion in 2026 to reach USD 1.27 billion by 2031, at a CAGR of 3.69% during the forecast period (2026-2031). Moderate expansion accompanies a maturing demand base, tighter Extended Producer Responsibility (EPR) enforcement, and a steady shift in consumer preference toward recyclable formats. Aluminum’s lightweight profile, national recycling infrastructure, and fuel-saving logistics economics sustain its dominance, while steel’s value proposition in heavy-duty industrial uses unlocks incremental gains. Craft breweries, direct-to-consumer (DTC) grocery platforms, and aerosol exports diversify demand nodes, partially cushioning the margin pressure sparked by raw material inflation and port bottlenecks. Consolidation-both domestic and cross-border-accelerates as scale becomes essential for hedging base-metal price swings and financing coating innovations that eliminate BPA, PFAS, and PVC.

Key Report Takeaways

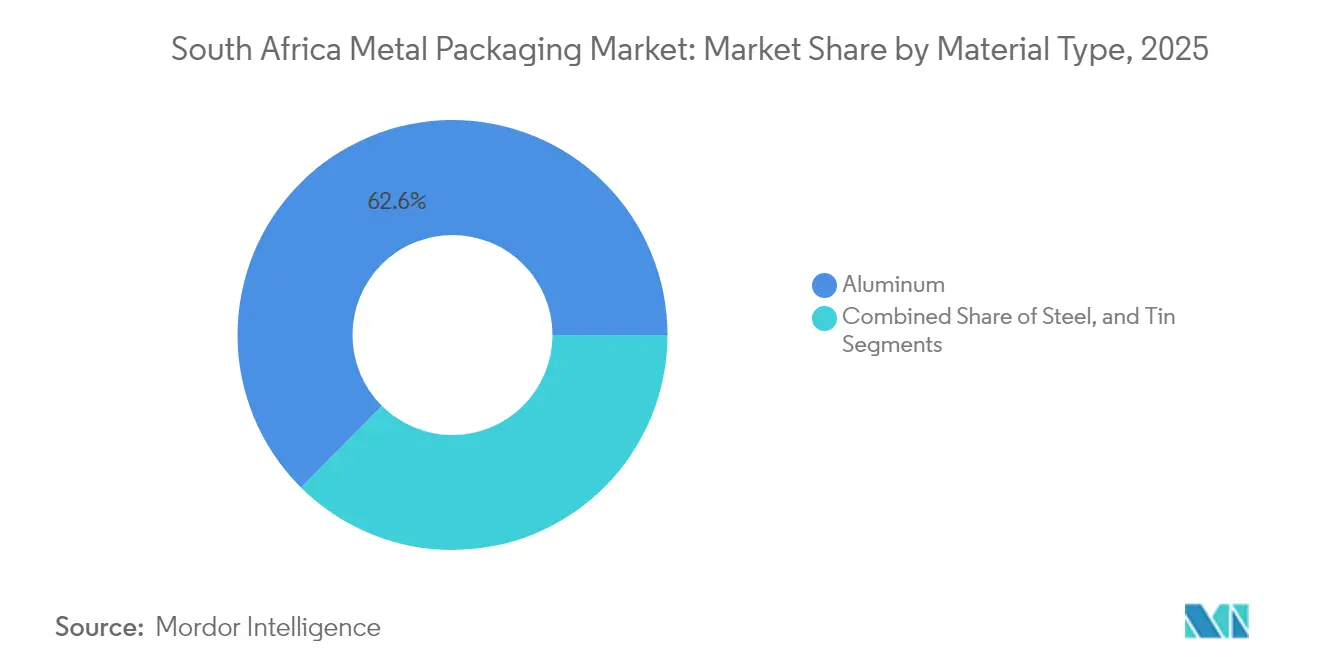

- By material, aluminum captured 62.55% of the South Africa metal packaging market share in 2025; steel is projected to expand at a 4.43% CAGR through 2031.

- By product type, cans contributed 39.15% revenue share in 2025, while bulk containers are forecast to record a 4.88% CAGR to 2031.

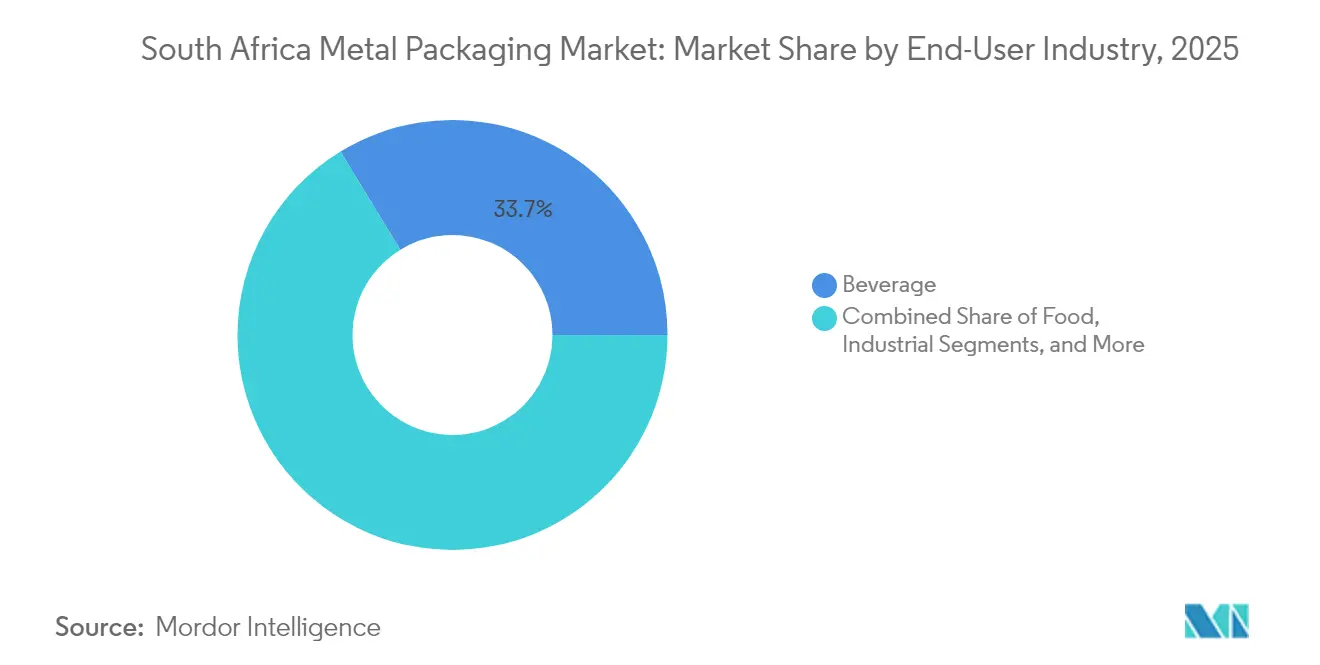

- By end-user industry, beverages accounted for 33.72% of the South Africa metal packaging market size in 2025; the industrial segment is advancing at a 4.91% CAGR through 2031.

- By coating type, epoxy phenolic held 45.98% share in 2025, whereas BPA-free alternatives are poised for a 3.92% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Metal Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Beverage Can Demand From Craft Brewers | +0.8% | National, concentrated in Western Cape and Gauteng | Medium term (2-4 years) |

| Shift Toward Lightweight Aluminum Substituting Steel | +0.6% | National, led by major beverage producers | Long term (≥ 4 years) |

| Extended Producer Responsibility Legislation Tightening | +0.5% | National, administered through MetPac-SA | Short term (≤ 2 years) |

| Rise of Direct-to-Consumer Food Brands Requiring Premium Metal Packs | +0.4% | National, urban-focused distribution | Medium term (2-4 years) |

| On-Site Solar Power Lowering Operational Energy Costs for Can Makers | +0.3% | National, industrial manufacturing hubs | Medium term (2-4 years) |

| Surging Automotive Aerosol Exports Boosting Aerosol Can Consumption | +0.2% | National, export-oriented manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Beverage Can Demand From Craft Brewers

South Africa’s vibrant craft-brew ecosystem is driving a steep trajectory in aluminum can usage as microbrewers seek to differentiate their shelves through colorful, short-run graphics and eco-friendly messaging. Tiny Keg’s ability to service 40% of national craft breweries with 6 million cans in 2023 exemplifies the scalability of these niche players. Premium price tolerance offsets lower batch volumes, ensuring attractive margins for converters. Concentrated cluster activity in the Cape Town and Johannesburg corridors leverages tourism flows and urban retail channels that value locally produced beverages. Regulatory flexibility under the Liquor Products Act simplifies licensing, encouraging further start-ups and line extensions into canned wines and ready-to-drink cocktails. This dynamic positions craft brewers as influential advocates for closed-loop aluminum collection programs tied to EPR targets.

Shift Toward Lightweight Aluminum Substituting Steel

A decisive 2013 shift by Coca-Cola to aluminum cans under a ZAR 5.6 billion (USD 306.0 million) supply contract with Nampak catalyzed a sector-wide move away from tin-plated steel. Aluminum’s 95% energy-saving recycle loop aligns with climate pledges and lowers freight costs amid sustained fuel price volatility. Although the World Bank forecasts a 4% increase in aluminum prices for 2025,[1]World Bank analysts, “Commodity Markets Outlook,” World Bank, worldbank.org the net total cost of ownership remains favorable when factoring in logistics and recycling credits. The switch gains further momentum from aluminum’s superior printability, enabling the creation of limited-edition designs that reinforce brand storytelling. Consequently, material mix forecasts indicate that aluminum is solidifying its front-runner status, while steel is migrating toward bulk bins, drums, and reconditioned industrial containers.

Extended Producer Responsibility Legislation Tightening

Full EPR implementation under MetPac-SA places mandatory recovery and recycling quotas on every packaging producer, sharpening the economic rationale for infinitely recyclable metals. Financial penalties for shortfalls incentivize capital spending on collection nodes and sorting technology, exemplified by the May 2025 MetPac-SA and GeT Metal Group partnership.[2]Giampietri Zweli, “MetPac-SA and GeT Metal Group Celebrate Metal Packaging Circular Economy,” MetPac-SA, metpacsa.org.za Clear compliance protocols de-risk investments in domestic smelting and coating facilities, while simultaneously accelerating industry consolidation as smaller firms struggle with administrative overhead. The policy environment thereby enlarges the addressable pool of post-consumer scrap, further strengthening the competitive edge of aluminum and steel substrates in the South Africa metal packaging market.

Rise of Direct-to-Consumer Food Brands Requiring Premium Metal Packs

DTC grocery platforms require robust containers that survive extended shipping legs without compromising product integrity. Hermetic metal cans outperform flexible formats in terms of puncture resistance, oxygen ingress, and tamper-evident visibility-attributes critical for online brands that assume full liability for spoilage and recalls. Superior surface aesthetics enable photorealistic graphics that enhance the unboxing experience, which is crucial to customer retention. Urban millennials in Johannesburg and Cape Town constitute the core DTC demographic, and their preference for sustainable packaging dovetails with metal’s almost limitless recyclability. Converters capable of quick-turn, micro-lot production are securing recurring orders from fast-pivot DTC food entrepreneurs, strengthening premium-price resilience within the South Africa metal packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Base Metal Prices Pressuring Margins | -0.9% | National, affecting all metal packaging producers | Short term (≤ 2 years) |

| Plastic Pouch Substitution in Paints and Chemicals | -0.6% | National, industrial applications | Medium term (2-4 years) |

| Consumer BPA Concerns Dampening Epoxy-Lined Can Uptake | -0.4% | National, food and beverage applications | Long term (≥ 4 years) |

| Port Congestion and Rail Bottlenecks Disrupting Raw Material Supply | -0.5% | National, concentrated impact on coastal operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Base Metal Prices Pressuring Margins

Aluminum and tin feedstock cost swings erode converter profitability, especially for firms lacking hedging lines or multiyear supply contracts. The rand’s chronic volatility amplifies imported coil costs, while load-shedding injects scheduling inefficiencies that inflate unit energy consumption. Passing through surcharges proves challenging in price-sensitive beverage and staple food categories, prompting tier-two players to exit or consolidate. Working capital stresses elevate borrowing needs precisely when South African interest rates trend higher, compressing spreads and delaying maintenance spending. Larger incumbents leverage procurement scale to secure favorable terms, reinforcing an already concentrated hierarchy within the South Africa metal packaging market.

Plastic Pouch Substitution in Paints and Chemicals

Industrial fillers increasingly specify high-density polyethylene (HDPE) pouches, enticed by weight savings, ergonomic handles, and spout dispensers that cut residue loss. Shipping efficiencies drive down freight budgets in a sector where packaging can eclipse 15% of delivered costs. For commodity chemicals in particular, brand equity exerts limited influence, amplifying price elasticity that works against metal. Yet metal retains an edge where chemical compatibility, vapor-barrier performance, or long-term storage stability is mission-critical. Metal converters, therefore, must articulate total cost-of-ownership narratives-such as reusability cycles or triple-seamed leak security-to reclaim share from flexible rivals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Dominance Drives Sustainability Transition

Aluminum accounted for 62.55% of the South African metal packaging market in 2025, as beverage producers adopted the substrate for its recyclability and weight savings. Steel’s 4.43% CAGR between 2026 and 2031 underscores its rising appeal for bulk bins and aerosol shells that prioritize puncture resistance over lightness. Tin, constrained by cost and supply limits, continues to cede niche territories. The South Africa metal packaging market size benefits from Hulamin’s domestic can-body investment, which trims import dependence and shortens lead times. AkzoNobel’s Securshield coating series removes BPA, PFAS, and PVC, thereby future-proofing aluminum’s penetration into high-acid food lines. Collectively, these developments entrench the South Africa metal packaging market share of aluminum while allocating growth white-space to steel in industrial drums and reconditioned chemical barrels.

Aluminum’s circularity aligns seamlessly with EPR quotas that demand verifiable recycling outcomes; each recovered can returns enough valuable metal to offset collection costs, bolstering the substrate’s dominant margin profile. Steel’s magnetic properties simplify separation at materials recovery facilities, giving it a pragmatic sustainability narrative that resonates with bulk lubricant and paint fillers. Tin retains relevance in specialty aerosol valves and niche gourmet lines where corrosion resistance overrides all-in cost. As converter portfolios broaden to encompass multi-substrate options, the South Africa metal packaging market demonstrates adaptive capacity to service both high-velocity consumer categories and heavy-duty industrial sectors.

By Product Type: Industrial Applications Reshape Growth Dynamics

Cans captured 39.15% of total revenue in 2025, driven by entrenched beverage volume. However, bulk containers are projected to post a 4.88% CAGR through 2031. The South Africa metal packaging market size for drums and barrels expands with mining and agrochemical exports that require UN-certified containers capable of withstanding the shocks of sea freight. DPI Recyclers’ model of refurbishing 210-liter drums illustrates the circular economy potential embedded in industrial segments. Decorative cans attract craft beverage and gourmet food brands seeking to make a lasting impression on the shelf.

Advancements in aerosol valve accuracy fuel incremental demand for monobloc and two-piece aerosol cans, targeting automotive polish and personal-care sprayers. Caps and closures, buoyed by Bericap’s acquisition of Coleus Packaging, supply both domestic bottlers and regional exporters with crown corks and roll-on pilfer-proof (ROPP) solutions. The product mix shift necessitates retooling at converter plants to accommodate a variety of diameters and micro-batch print runs. This diversification enhances the overall resilience of the South Africa metal packaging market.

By End-User Industry: Industrial Sector Leads Growth Trajectory

Beverages remained the largest demand node at 33.72% in 2025; however, industrial customers will spearhead future expansion with a 4.91% CAGR, driven by the demand for mining chemicals, lubricants, and construction coatings. The South Africa metal packaging market share devoted to lubricants grows alongside the country’s 17% contribution to Africa’s total lubricant consumption. Aerosolized paints and cleaners, destined for export markets, further increase volume throughput. Meanwhile, food processors embrace premium canisters for shelf-stable ready meals marketed via DTC channels.

Pharmaceutical fillers value metal’s tamper visibility and sterility, and their orders create high-margin niches despite lower absolute tonnage. Paint and coating brands weigh plastic pouches for decorative markets but preserve metal for solvent-resistant industrial grades that demand barrier integrity. This split highlights how the South Africa metal packaging market size evolves by aligning container attributes with end-use performance requirements, rather than pursuing uniform material substitution.

By Coating Type: BPA-Free Innovation Drives Market Evolution

Epoxy phenolic coatings supplied nearly half of the unit volumes in 2025, owing to their balanced cost and chemical resistance profile. However, BPA-free formulations trend upward at a 3.92% CAGR, as retailers and regulators flag endocrine-disruptor risks. Securshield demonstrates that next-generation polymers can meet retort durability requirements without PFAS or PVC, thereby removing compliance uncertainties for exporters targeting European Union markets. Acrylic and polyester chemistries fulfill specialty needs, such as UV-cured graphics or highly acidic contents, by carving out defensible micro-segments.

Converters differentiate through in-house application know-how, line speed, and rapid switchover that support smaller production runs demanded by craft beverages and DTC brands. Coating innovation thus becomes a decisive wedge in competitive bidding, elevating technical capability as a cornerstone of procurement decisions within the South Africa metal packaging market.

Geography Analysis

Gauteng, South Africa’s commercial hub, accounts for the highest packaging consumption, owing to its 26.3% share of national waste generation and a dense beverage bottling footprint. KwaZulu-Natal follows with 17.9%, yet chronic port congestion at Durban-where vessels waited up to 16 days in 2024-has forced converters to increase finished-goods safety stock. Western Cape contributes 14.7% and leads craft beverage innovation, leveraging Cape Town’s tourism economy and robust municipal recycling schemes.

Inland provinces such as Mpumalanga and North West generate steady industrial demand tied to coal and platinum mining, reinforcing the South Africa metal packaging market’s exposure to commodity cycles. EPR mandates apply uniformly nationwide, harmonizing collection targets and enabling economies of scale in back-haul scrap logistics. Cross-border trade with the Southern African Development Community (SADC) is expected to receive incremental tailwinds as the African Continental Free Trade Area progressively reduces tariffs, positioning South African converters to supply Botswana, Namibia, and Zimbabwe.

Infrastructure disparities remain acute: while Gauteng enjoys integrated rail-road links, Limpopo’s limited paved road coverage inflates last-mile costs. Government plans to concession parts of Transnet’s rail freight corridors could unlock throughput gains by 2028, benefiting steel drum producers reliant on manganese and chrome concentrate shipments. Overall, geographic heterogeneity necessitates flexible inventory positioning and multiport export strategies for firms competing in the South Africa metal packaging market.

Competitive Landscape

Market structure is moderately concentrated. Nampak leverages three-piece and two-piece can lines, plus proprietary ends, to secure multi-year beverage contracts, including the pivotal Coca-Cola aluminum transition. Its vertical integration into printing, sewing, and recycling streamlines cost and quality control. Ball Corporation and Crown Holdings deploy global R&D to introduce lightweight ends and D&I body stock, challenging local incumbents on performance metrics. Ardagh taps its European design studios to co-create limited-edition craft beer wraps, heightening brand appeal.

Sonoco’s USD 3.9 billion acquisition of Eviosys overlays the world’s largest food-can platform onto local distributor relationships, likely intensifying competition in aerosol and retort categories. Hulamin’s upstream expansion shortens coil lead times, enhancing domestic supply reliability. Smaller specialists, such as DPI Recyclers and Tiny Keg, thrive by targeting reconditioned industrial drums and craft-focused micro-print can runs, respectively, niches that large players struggle to serve economically.

Technology leadership centers on coating chemistry, line automation, and scrap recovery yield. Companies investing in on-site solar arrays cut grid exposure and earn ESG credits prized by multinational brand owners. Customer stickiness magnifies for suppliers able to validate cradle-to-cradle metrics, a core procurement criterion for beverage majors and DTC disruptors alike. Such capabilities dictate bargaining power and margin stability in the South Africa metal packaging market.

South Africa Metal Packaging Industry Leaders

Nampak Limited

Ardagh Metal Packaging S.A.

Crown Holdings Inc.

Ball Corporation

CAN-PACK S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Industry commentary reaffirmed South Africa’s leadership role in African packaging output.

- January 2025: MetPac-SA partnered with GeT Metal Group to host a circular-economy showcase in Johannesburg, spotlighting producer-to-recycler collaboration.

- August 2024: Mauser Packaging Solutions acquired a South African plastic drums business, broadening its industrial packaging offering.

- August 2024: Guala Closures finalized the Coleus Packaging deal and relaunched the Durban plant as Bericap South Africa.

South Africa Metal Packaging Market Report Scope

Packaging provides a protective and informative covering, protects the product during handling, storage and movement, and provides useful information about the content of the package. The use of metals, such as steel, aluminum, tin, etc., for packaging, is termed metal packaging. The study tracks the demand for South Africa Metal Packaging Market in terms of value (USD Million) from the sale of such packaging solutions offered by various vendors. The South Africa Packaging Market is segmented by Materials Type (Aluminum, Steel), Product Type (Cans, Bulk Containers, Shipping Barrels and Drums, Caps and Closures), and End-User Vertical (Beverage, Food, Paints, and Chemicals, Industrial). The market sizes and forecasts are provided in terms of value (in USD million) for all the above segments.

By Material Type

| Aluminum |

| Steel |

| Tin |

By Product Type

| Cans | Food Cans |

| Beverage Cans | |

| Aerosol Cans | |

| Decorative Cans | |

| Bulk Containers | |

| Drums and Barrels | |

| Caps and Closures | |

| Other Product Types |

By End-User Industry

| Food |

| Beverage |

| Paints, Coatings and Chemicals |

| Pharmaceuticals and Healthcare |

| Industrial |

| Other End-user Industries |

By Coating Type

| Epoxy Phenolic |

| Acrylic |

| Polyester |

| BPA-Free Alternatives |

| Other Coating Types |

| By Material Type | Aluminum | |

| Steel | ||

| Tin | ||

| By Product Type | Cans | Food Cans |

| Beverage Cans | ||

| Aerosol Cans | ||

| Decorative Cans | ||

| Bulk Containers | ||

| Drums and Barrels | ||

| Caps and Closures | ||

| Other Product Types | ||

| By End-User Industry | Food | |

| Beverage | ||

| Paints, Coatings and Chemicals | ||

| Pharmaceuticals and Healthcare | ||

| Industrial | ||

| Other End-user Industries | ||

| By Coating Type | Epoxy Phenolic | |

| Acrylic | ||

| Polyester | ||

| BPA-Free Alternatives | ||

| Other Coating Types | ||

Key Questions Answered in the Report

What is the projected value of the South Africa metal packaging market by 2031?

The market is forecast to reach USD 1.27 billion by 2031, growing at a 3.69% CAGR.

Which material leads unit demand?

Aluminium held 62.55% share in 2025 thanks to its recyclability and weight advantages.

Which end-user segment will grow fastest through 2031?

Industrial applications, covering mining chemicals and lubricants, are set to advance at a 4.91% CAGR.

How does EPR legislation influence packaging choices?

Mandatory recovery quotas favor infinitely recyclable metals, prompting converters to invest in aluminium and steel capacity.

What geographic areas drive the highest consumption?

Gauteng and KwaZulu-Natal together generate more than 40% of national packaging demand, with Western Cape prominent in craft beverage cans.

Which coating segment is expanding the quickest?

BPA-free alternatives are projected to grow at 3.92% CAGR as health-conscious consumers and regulators push for safer linings.

Page last updated on: