Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.46 Billion |

| Market Size (2026) | USD 4.66 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Nutraceuticals Market Analysis by Mordor Intelligence

South Africa nutraceuticals market size in 2026 is estimated at USD 4.66 billion, growing from 2025 value of USD 4.46 billion with 2031 projections showing USD 5.82 billion, growing at 4.55% CAGR over 2026-2031. Consistent population aging, consumer pivot toward preventive nutrition, and a stricter yet supportive regulatory climate steer demand, while indigenous botanical resources give manufacturers a unique supply advantage. Dietary supplements retain leadership through widespread micronutrient deficiencies, whereas functional beverages surge on the back of sports-nutrition momentum. Distribution consolidation favors large modern retail formats, yet rapid e-commerce growth reflects a digitally confident consumer base. Competitive intensity remains moderate, with both pharmaceutical majors and agile wellness startups leveraging South Africa’s WHO Maturity Level 3 regulatory status to introduce compliant, science-backed formulations.

Key Report Takeaways

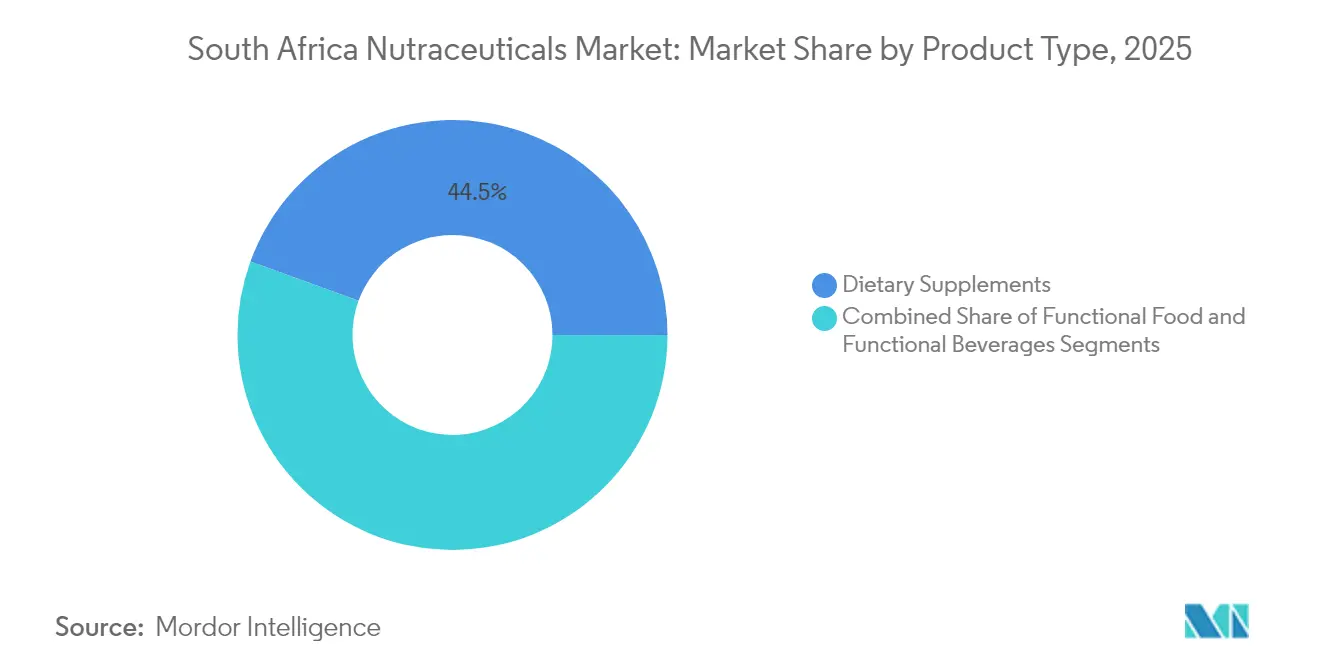

- By product type, dietary supplements captured 44.45% of the South Africa nutraceuticals market share in 2025, while functional beverages are forecast to post a 5.78% CAGR to 2031, the fastest among all segments.

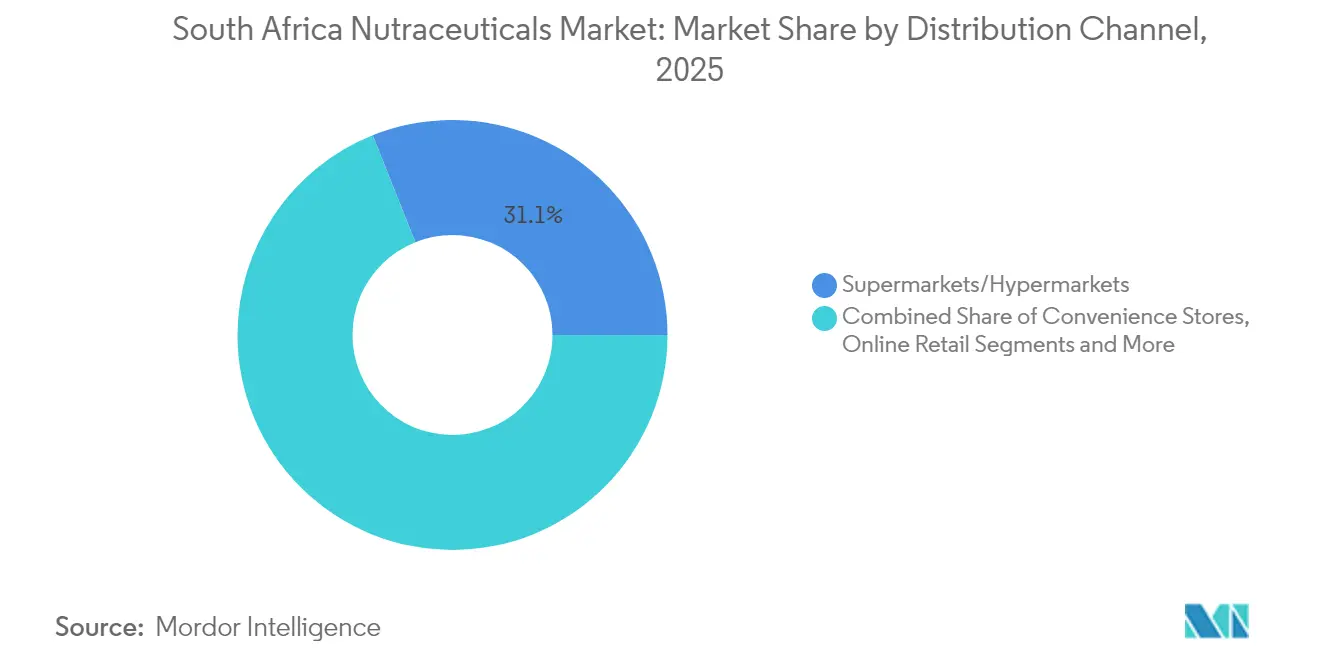

- By distribution channel, supermarkets and hypermarkets held 31.05% of the South Africa nutraceuticals market size in 2025, online retail is projected to expand at a 6.08% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population seeking preventative health solutions | +1.2% | National, with concentration in Western Cape and Gauteng | Medium term (2-4 years) |

| Rising incidence of lifestyle diseases (obesity, diabetes) | +1.5% | National, with higher impact in urban areas | Short term (≤ 2 years) |

| Preference for natural and plant-based products | +0.8% | National, with premium segments in major metros | Medium term (2-4 years) |

| Product innovation in formulation and delivery | +0.7% | National, driven by manufacturing hubs | Long term (≥ 4 years) |

| Government health initiatives | +0.4% | National, with rural focus areas | Long term (≥ 4 years) |

| Advancements in research and development | +0.3% | National, centered in academic institutions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging population seeking preventative health solutions

South Africa's aging population is creating a substantial demand for preventative health products. As of June 2024, Statistic South Africa reports that 6.13 million individuals aged 60 and older are contributing to this growing trend [1]Source: Statistics South Africa, "2024 Mid-year population estimates", statssa.gov.za. The white and Indian/Asian demographics are experiencing the most pronounced aging trends, with aging indices showing that older populations now outnumber the youth. This demographic shift has created premium market segments, particularly for specialized nutraceuticals that address cognitive health, bone density, and cardiovascular wellness. Urban seniors are increasingly adopting Western dietary patterns, which often lack traditional nutrient-dense foods. As a result, the demand for supplements such as calcium, vitamin D, and omega-3s has grown substantially. Additionally, the government actively supports preventative health measures through its National Development Plan, which aims to raise life expectancy to at least 70 years. This policy initiative seeks to reduce the burden on the healthcare system while promoting healthier aging.

Rising incidence of lifestyle diseases (obesity, diabetes)

Lifestyle diseases, such as obesity and diabetes, are on the rise, significantly driving the growth of the South Africa nutraceuticals market. The increasing prevalence of these conditions has led to a growing demand for functional foods, dietary supplements, and other nutraceutical products that help manage and prevent such diseases. Consumers are becoming more health-conscious and are actively seeking products that support better health outcomes, further fueling market growth. In 2024, the International Diabetes Federation reported a 7.2% prevalence of diabetes among adults [2]Source: International Diabetes Federation, "Diabetes in South Africa (2024)", idf.org, highlighting the urgent need for effective health management solutions. Additionally, the shift in dietary patterns, coupled with urbanization and sedentary lifestyles, has exacerbated the prevalence of these diseases, prompting individuals to adopt preventive healthcare measures. Nutraceuticals are increasingly perceived as a viable solution to bridge nutritional gaps and address specific health concerns, including weight management and blood sugar control. This trend is further supported by rising disposable incomes, enabling consumers to invest in premium health products.

Preference for natural and plant-based products

Consumers in South Africa are increasingly favoring natural and plant-based products, which is emerging as a significant driver in the South Africa Nutraceuticals Market. This preference is fueled by growing awareness of the health benefits associated with natural ingredients and plant-based alternatives. Additionally, the rising concerns over synthetic additives and their potential side effects have further propelled the demand for these products. The trend aligns with the global shift toward sustainable and eco-friendly consumption patterns, as consumers seek products that are not only beneficial for their health but also environmentally responsible. This inclination is evident across various nutraceutical categories, including dietary supplements, functional foods, and beverages, where manufacturers are incorporating plant-based ingredients to cater to this growing demand. The increasing availability of such products in the market, coupled with targeted marketing strategies emphasizing their natural and health-centric attributes, is expected to sustain this trend during the forecast period.

Government health initiatives

Health initiatives spearheaded by the government play a significant role in driving the South Africa Nutraceuticals Market. The South African government has implemented various programs and policies aimed at improving public health and addressing nutritional deficiencies. For instance, the Department of Health has launched campaigns to promote awareness about the importance of balanced diets and the consumption of fortified foods. Additionally, government-led initiatives such as the National Nutrition Week and the Food Fortification Program emphasize the role of nutraceuticals in combating malnutrition and enhancing overall health. South African government has also introduced the Integrated Nutrition Programme (INP), which focuses on improving the nutritional status of vulnerable groups, including children, pregnant women, and the elderly [3]Source: Western Cape Government, "Integrated Nutrition Programme", d7.westerncape.gov.za. This program highlights the importance of micronutrient supplementation and fortified products, which directly align with the growth of the nutraceuticals market. Such proactive measures by the government are expected to significantly contribute to the growth of the nutraceuticals market in South Africa during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory requirements | -0.9% | National, with higher compliance costs in manufacturing | Short term (≤ 2 years) |

| High cost and complexity of product development | -0.7% | National, affecting smaller manufacturers disproportionately | Medium term (2-4 years) |

| Lack of extensive clinical evidence | -0.5% | National, with international market access implications | Long term (≥ 4 years) |

| Consumer skepticism on efficacy and safety | -0.4% | National, with higher impact in rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory requirements

South African Health Products Regulatory Authority (SAHPRA) mandates extensive documentation for nutraceutical registration. Under the Medicines and Related Substances Act, dietary supplements must adhere to Good Manufacturing Practices (GMP), accurate labeling, and undergo regular inspections. The regulatory landscape becomes more intricate with the involvement of multiple agencies, including the Department of Health, South African Bureau of Standards (SABS), and National Regulator for Compulsory Specifications (NRCS). This complexity results in compliance costs, disproportionately affecting smaller manufacturers aiming for market entry. Recent tightening includes a March 2025 ban on cannabis in food, prohibiting the sale, import, or manufacture of foodstuffs with cannabis or hemp components. This has compelled companies, previously using hemp seed oil or flour, to reformulate products and adjust supply chains. While SAHPRA's evolution towards stricter oversight aims to ensure product safety and efficacy, it inadvertently creates hurdles for rapid product innovation and extends the time-to-market for new formulations. Achieving WHO Maturity Level 3 status underscores SAHPRA's regulatory sophistication. However, this status also brings more rigorous evaluation processes, potentially delaying product approvals and escalating development costs for nutraceutical manufacturers.

High cost and complexity of product development

Nutraceutical product developers face hefty costs due to clinical trials, bioavailability studies, and stability testing. These expenses are further amplified by the specialized extraction and formulation technologies needed for bioactive compounds. Working with natural ingredients introduces challenges in standardization, quality control, and ensuring consistency from batch to batch. This is especially true for products sourced from indigenous plants, where active compound concentrations fluctuate based on their geographical origin and harvesting conditions. Advanced delivery systems, such as nano-encapsulation and liposomal formulations, necessitate a robust manufacturing infrastructure. However, these systems require significant capital and technical expertise, which many local companies lack, hindering their ability to adopt such innovations. Moreover, the fragmented food safety landscape, governed by multiple regulatory agencies, complicates compliance and inflates costs. Companies must adeptly navigate varying requirements for food products, dietary supplements, and complementary medicines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Supplements Lead Functional Innovation

Dietary supplements hold the largest share in the South African nutraceuticals market, accounting for 44.45% in 2025. This dominance is largely driven by the prevalence of widespread micronutrient deficiencies within the population, especially among young adults in low socioeconomic regions. Critical nutrients such as iron, calcium, and vitamin D are commonly lacking, prompting increased consumer demand for supplements that address these gaps. The awareness around nutritional deficiencies has heightened public health initiatives and consumer interest, positioning dietary supplements as essential for improving overall health. Furthermore, these products are accessible, easy to consume, and often affordable, contributing to their strong market presence. The segment’s growth is supported by ongoing education campaigns and government programs aimed at combating malnutrition.

In contrast, functional beverages represent the fastest growing segment in the South African nutraceuticals market, registering a CAGR of 5.78% between 2026 and 2031. This rapid growth reflects shifting consumer preferences towards convenient and ready-to-consume nutrition solutions. Functional beverages are particularly popular due to their ease of use and the ability to deliver essential nutrients alongside hydration. The booming sports nutrition sector also significantly contributes to this trend, with consumers increasingly seeking beverages that support fitness, energy, and recovery. Innovation in flavors, formulations, and packaging has further enhanced their appeal across different age groups and lifestyle segments. As a result, functional beverages are positioned as a dynamic and expanding segment within South Africa’s nutraceutical landscape.

By Distribution Channel: Digital Transformation Accelerates

Supermarkets and hypermarkets continue to hold the largest share of the distribution segment in the South African nutraceuticals market, accounting for 31.05% in 2025. Their dominance is attributed to well-established consumer relationships and strong brand loyalty built over time. These retail outlets offer a wide range of products, making them convenient one-stop shops for consumers seeking nutraceuticals. Additionally, supermarkets and hypermarkets play a crucial role in educating customers through in-store demonstrations and promotional activities, which help to increase product awareness and trust. Their extensive physical presence across urban and suburban areas further strengthens their market position. By combining accessibility with personalized customer engagement, they maintain a leading share in the distribution landscape.

On the other hand, online retail stores represent the fastest-growing distribution channel, expanding at a CAGR of 6.08%. This rapid growth is driven by the ongoing digital transformation in consumer purchasing behaviors, especially for health and wellness products. Increasing internet penetration and smartphone usage have made online platforms more accessible and convenient for a broader audience. The ability to browse extensive product selections, read reviews, and compare prices from home appeals to tech-savvy consumers. Furthermore, the rise of e-commerce has enabled personalized marketing strategies and subscription models that foster customer loyalty. As a result, online retail is rapidly reshaping the South African nutraceuticals market by enhancing convenience and broadening consumer reach.

Geography Analysis

The South Africa nutraceuticals market is geographically diverse, with significant growth concentrated in urban and semi-urban regions where consumer health awareness is higher. Major cities such as Johannesburg, Cape Town, and Durban serve as primary markets due to their larger populations, growing middle class, and higher disposable incomes. These urban centers have well-established retail and healthcare infrastructures that support the distribution and availability of nutraceutical products. Consumer preferences in these areas are increasingly shifting towards preventive healthcare measures, driving demand for functional foods, dietary supplements, and functional beverages. As a result, manufacturers and retailers focus their marketing and distribution efforts heavily on these populous and economically vibrant regions.

In contrast, rural and less developed regions in South Africa present both challenges and opportunities for market expansion. Limited access to healthcare facilities and lower consumer purchasing power in these areas often restrict the penetration of high-value nutraceutical products. However, growing government initiatives addressing malnutrition and micronutrient deficiencies create a favorable environment for targeted product introductions designed to improve overall nutritional status. The presence of traditional dietary practices combined with increasing health education campaigns is gradually encouraging acceptance of nutraceuticals as complementary health solutions. Companies leveraging localized product formulations and affordable price points are better positioned to tap into these emerging rural markets, contributing to a more inclusive growth trajectory for the sector.

From a regional perspective, the South African nutraceuticals market also benefits from strong cross-border trade with neighboring countries within the Southern African Development Community (SADC). South Africa’s position as a regional economic hub facilitates the distribution of nutraceutical products not only domestically but also across borders, expanding market reach. Additionally, the country’s robust logistics network, including advanced transportation and cold chain systems, enhances product availability and quality assurance. Collaborative efforts between local manufacturers and international companies help drive innovation and cater to both regional and global demand. This geographical positioning affirms South Africa’s role as a gateway for nutraceutical growth in the wider African continent, enhancing its strategic importance within the industry.

Competitive Landscape

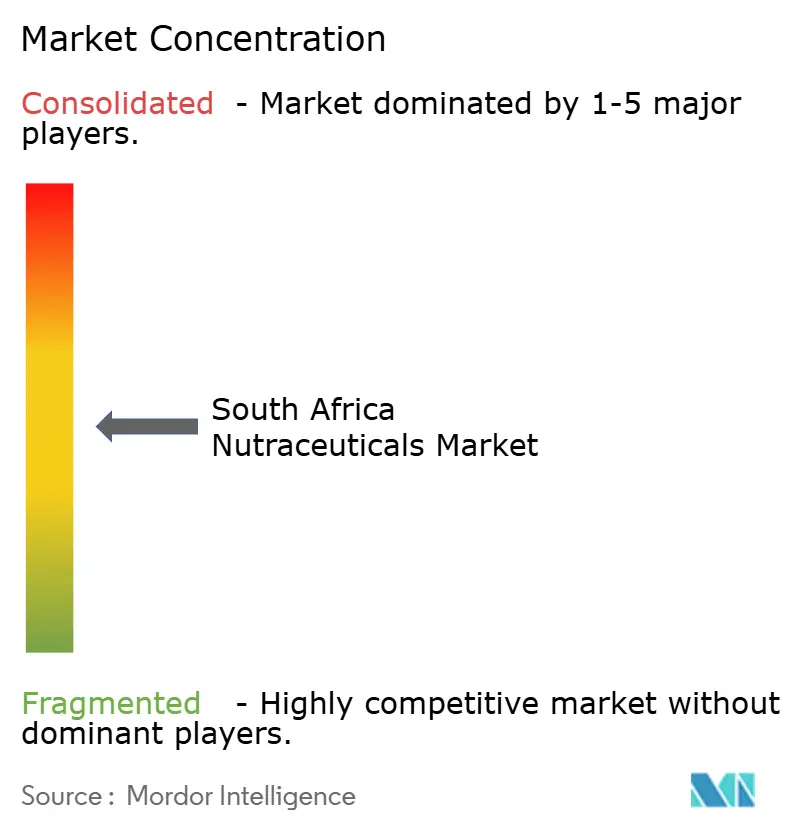

The South Africa nutraceuticals market demonstrates moderate fragmentation, with a concentration index of 5 out of 10. This level of fragmentation creates a competitive environment where both multinational pharmaceutical companies and local wellness brands actively participate. The market's structure allows for a diverse range of players to coexist, fostering innovation and competition within the industry. Multinational pharmaceutical companies leverage their extensive resources, global expertise, and established brand presence to capture a significant share of the market. These companies often focus on introducing advanced nutraceutical products, backed by robust research and development capabilities, to cater to the growing consumer demand for health and wellness solutions. Their ability to scale operations and maintain consistent product quality gives them a competitive edge in the market.

On the other hand, local wellness brands capitalize on their understanding of regional consumer preferences and cultural nuances. These brands often adopt differentiated strategies, such as offering affordable, locally sourced, and customized nutraceutical products, to appeal to the domestic audience. By focusing on affordability and tailoring their offerings to meet the specific needs of South African consumers, local players have carved out a niche for themselves in the market. Additionally, these brands often emphasize sustainability and the use of indigenous ingredients, which resonate well with environmentally conscious consumers. Their agility in responding to market trends and consumer demands further strengthens their position in the competitive landscape.

This dual presence of global and local players ensures a dynamic and competitive landscape, driving growth and innovation in the South Africa nutraceuticals market. The interplay between multinational corporations and local brands fosters a healthy level of competition, encouraging continuous product development and market expansion. As consumer awareness regarding health and wellness continues to rise, the nutraceuticals market in South Africa is expected to witness sustained growth. The competitive dynamics within the market are likely to evolve further, with both global and domestic players striving to enhance their market share through strategic initiatives, partnerships, and product diversification.

South Africa Nutraceuticals Industry Leaders

-

Nestlé S.A.

-

Ascendis Health

-

Cipla Limited

-

Ultimate Sports Nutrition (USN)

-

Amway Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Cipla Limited has invested ZAR 900 million in Cipla Medpro South Africa Proprietary Limited to strengthen its presence in the South African pharmaceutical market. This investment aims to enhance Cipla Medpro's operational capabilities and expand its product portfolio in the region.

- March 2024: Adcock Ingram Critical Care has partnered with Convatec to enhance the supply of advanced medical products, including a comprehensive range of nutraceutical products. This collaboration aims to leverage the expertise of both companies to address the growing demand for high-quality healthcare solutions in the market.

- December 2023: Paarl-based Afriplex upgraded its South African plant to establish Africa's first SAHPRA-compliant gummy production facility. The facility featured automated equipment, advanced laboratories, and GMP-compliant production, ensuring high-quality functional gummies. With a Category A SAHPRA license, it reinforced Afriplex's reputation as a trusted functional product manufacturer.

South Africa Nutraceuticals Market Report Scope

Nutraceutical is a term used to describe any product derived from food sources with health benefits and basic nutritional requirements. The market studied is segmented by Type and by Distribution Channel. By Type, the market studied is segmented into Functional Foods, Functional Beverages, and Dietary Supplements on a broad scale. Furthermore, Functional Beverages are segmented into Energy Drinks, Sports Drinks, and Other Functional Beverages. Dietary Supplements are segmented into Vitamins and Minerals, Fatty Acids, and Other Dietary Supplements. By Distribution Channel, the market studied is segmented into Supermarkets/ Hypermarkets, Convenience Stores, Drug Stores/Pharmacies, Online Retail Stores, and Other Distribution Channels. The report offers market size and forecasts in value (USD million) for all the above segments.

By Product Type

| Functional Foods | Cereal |

| Bakery and Confectionery | |

| Dairy | |

| Snacks | |

| Other Functional Foods | |

| Functional Beverages | Energy Drink |

| Sports Drink | |

| Fortified Juice | |

| Dairy and Dairy-Alternative Beverage | |

| Other Functional Beverages | |

| Dietary Supplements | Vitamins and Minerals |

| Botanical | |

| Herbal | |

| Enzyme | |

| Fatty Acid | |

| Other Supplements |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Drug Stores / Pharmacies |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Functional Foods | Cereal |

| Bakery and Confectionery | ||

| Dairy | ||

| Snacks | ||

| Other Functional Foods | ||

| Functional Beverages | Energy Drink | |

| Sports Drink | ||

| Fortified Juice | ||

| Dairy and Dairy-Alternative Beverage | ||

| Other Functional Beverages | ||

| Dietary Supplements | Vitamins and Minerals | |

| Botanical | ||

| Herbal | ||

| Enzyme | ||

| Fatty Acid | ||

| Other Supplements | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Drug Stores / Pharmacies | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the projected value of the South Africa nutraceuticals market in 2031?

The market is expected to reach USD 5.82 billion by 2031, reflecting a 4.55% CAGR from 2026.

Which product segment holds the largest share of revenue?

Dietary supplements lead with 44.45% of market revenue in 2025, driven by multinutrient and botanical formulations.

Which distribution channel is growing the fastest?

Online retail is advancing at a 6.08% CAGR through 2031, propelled by AI-based personalization and wider e-commerce adoption.

How does regulation impact new product launches?

SAHPRA’s stringent GMP and labeling requirements lengthen approval timelines, adding cost pressures but ensuring safety and quality.

Page last updated on: