Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

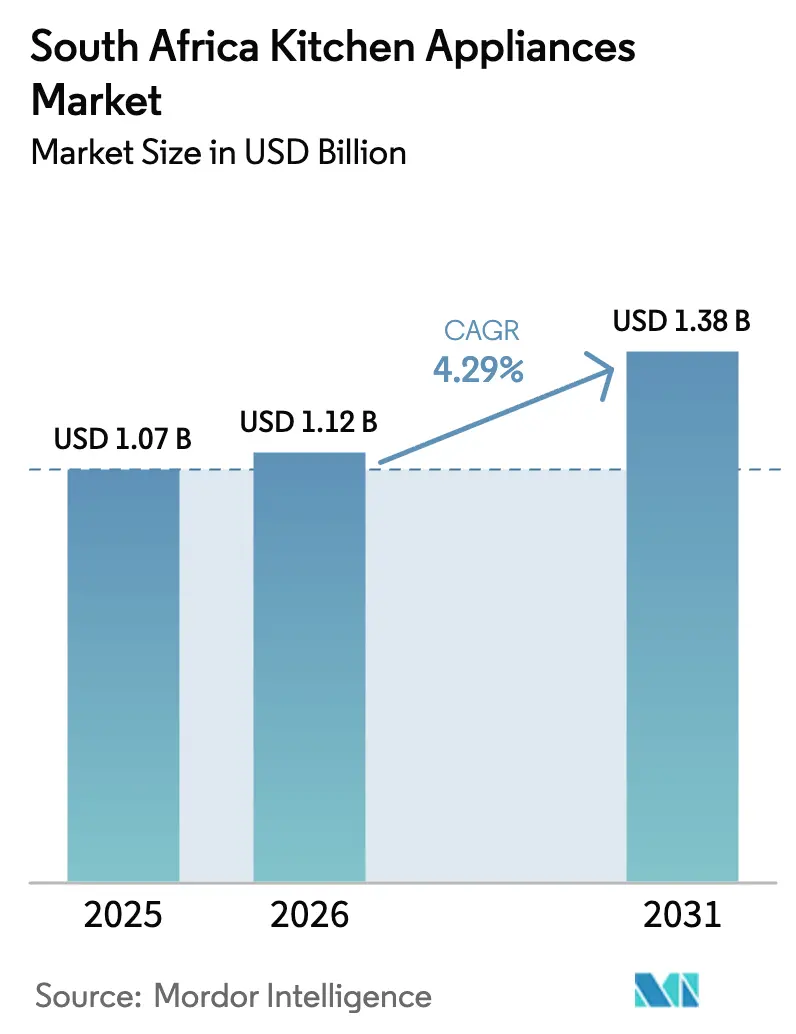

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

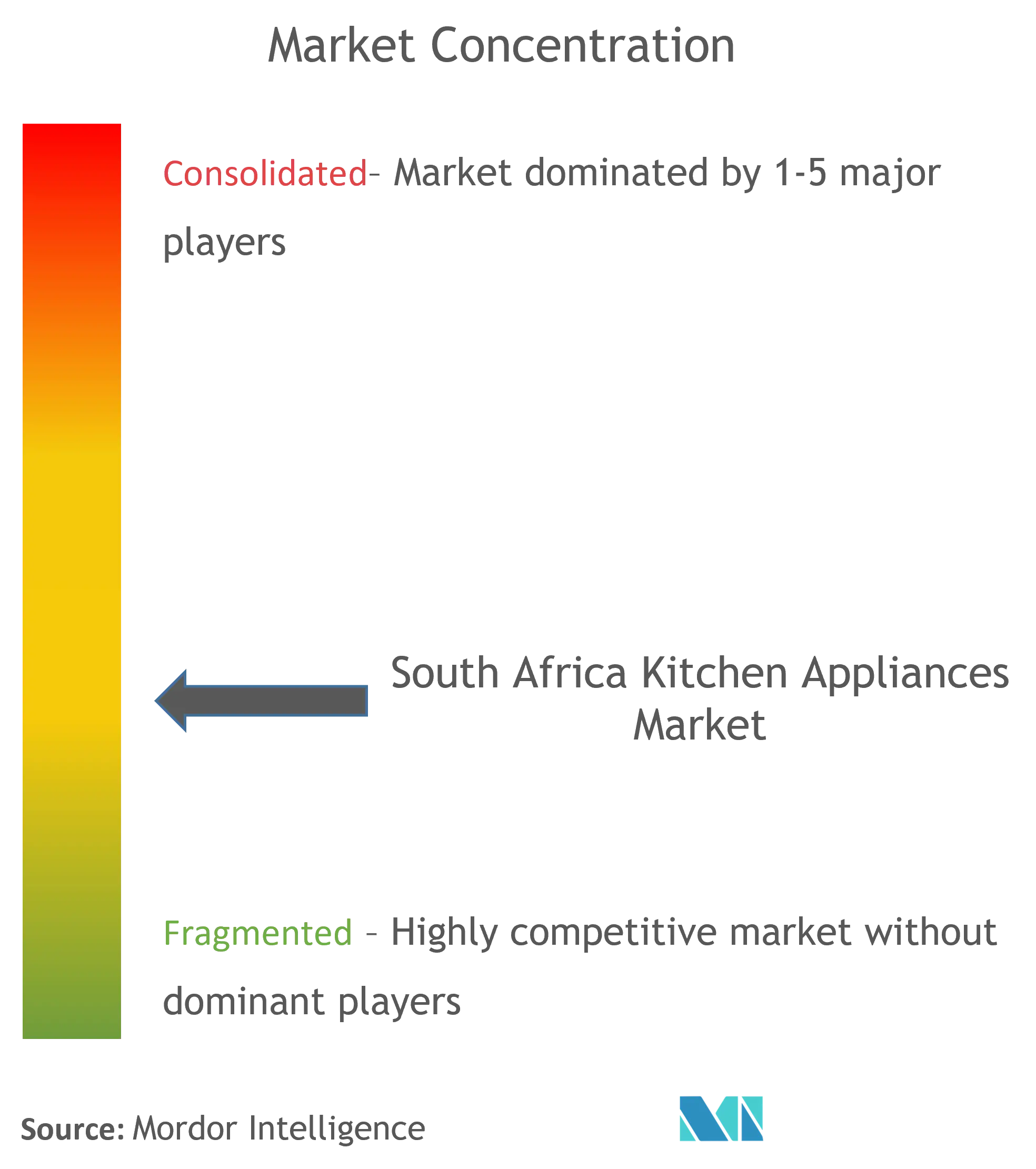

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Kitchen Appliances Market Analysis by Mordor Intelligence

The South Africa kitchen appliances market size is expected to grow from USD 1.07 billion in 2025 to USD 1.12 billion in 2026 and is forecast to reach USD 1.38 billion by 2031 at a 4.29% CAGR over 2026–2031. A mix of resilient household demand for inverter-ready products, localized assembly moves by global brands, and steady adoption of installment financing across retail channels drives growth. The South African kitchen appliances market continues to benefit from targeted manufacturing incentives that favour energy-efficient investments and the integration of renewables at the plant level. Seismic load-shedding patterns and tariff pressure push feature prioritization toward inverter compatibility, solar-readiness, and app-enabled devices that manage consumption within constrained power budgets. Expanding formal housing pipelines in peri-urban areas supports a shift in the South Africa kitchen appliances market toward compact, multi-function devices that fit smaller footprints and enable flexible household use cases[1]Source: Social Housing Regulatory Authority, “Strategic Plan 2025–2030,” SHRA, shra.org.za.

Key Report Takeaways

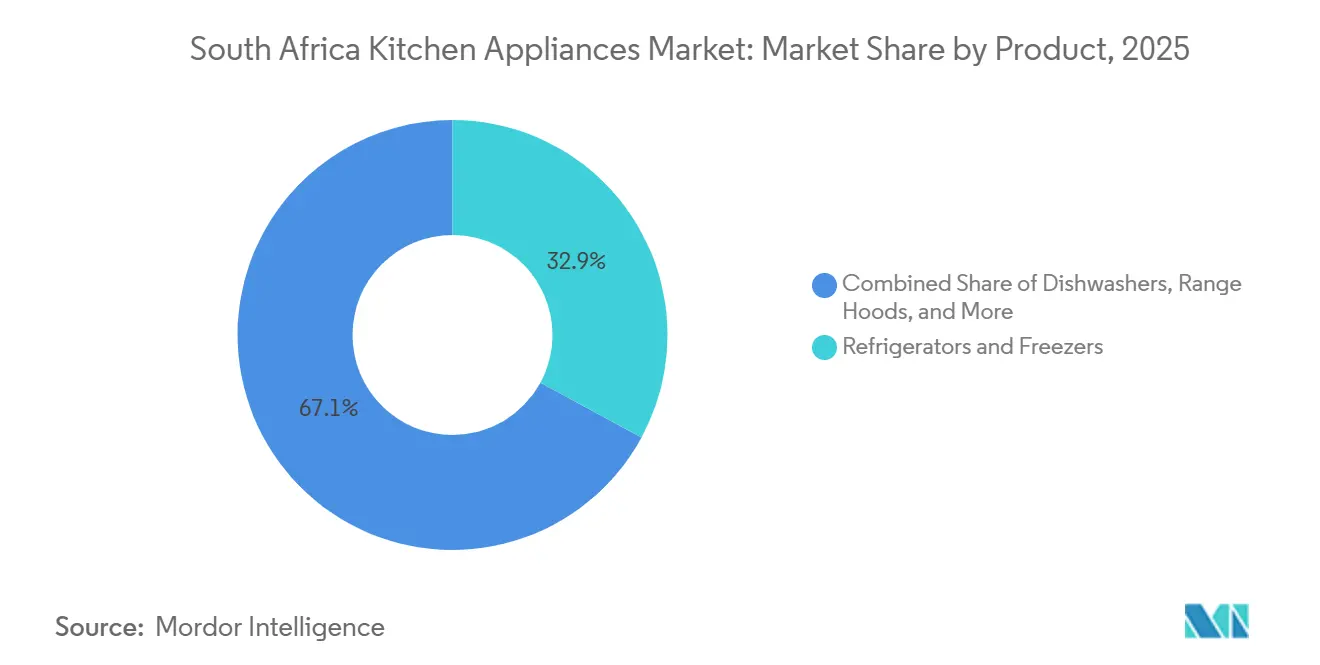

- By product type, refrigerators and freezers led with 32.91% of the South Africa kitchen appliances market share in 2025, while air fryers are projected to expand at a 4.62% CAGR through 2031.

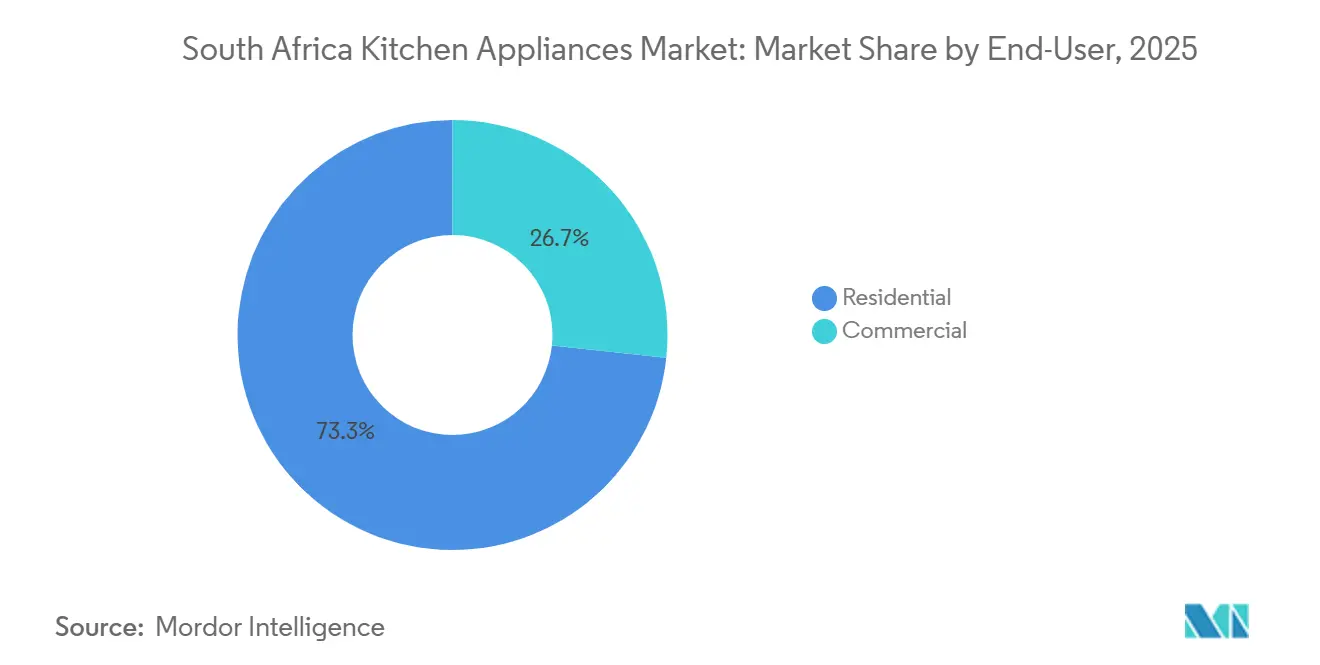

- By end user, the residential segment accounted for 73.32% of the South Africa kitchen appliances market share in 2025 and is forecast to grow at a 4.35% CAGR through 2031.

- By distribution channel, B2C retail captured 72.31% of the South Africa kitchen appliances market share in 2025, and the online sub-segment is set to advance at a 5.16% CAGR through 2031.

- By geography, Gauteng held 41.23% of the South Africa kitchen appliances market share in 2025, and the Western Cape records the fastest projected 4.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inverter-ready "load-shedding-proof" appliances | +0.9% | National, with peak adoption in Gauteng and Western Cape industrial zones | Medium term (2-4 years) |

| Growing middle-income housing stock in peri-urban zones | +0.7% | National, concentrated in Tshwane, Ekurhuleni, and Cape Town metro fringes | Long term (≥ 4 years) |

| Migration of global brands' assembly lines to South Africa | +0.8% | Western Cape, KwaZulu-Natal, Gauteng | Long term (≥ 4 years) |

| Surge in e-commerce "pay-as-you-cook" financing models | +1.0% | National, led by Gauteng and Western Cape urban centres | Short term (≤ 2 years) |

| Government rebates for local energy-efficient manufacturing | +0.5% | National, with manufacturing clusters in the Western Cape and KwaZulu-Natal | Medium term (2-4 years) |

| Rising demand for smart IoT-enabled kitchen devices | +0.6% | National, early adoption in high-income urban enclaves | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inverter-Ready "Load-Shedding-Proof" Appliances

The South Africa kitchen appliances market is seeing strong pull for inverter-ready and solar-hybrid models as households look to maintain food storage and cooking routines throughout outages and higher power tariffs. Manufacturers have introduced design shifts such as integrated batteries and optimized power electronics that decouple essential functions from grid volatility, with Defy’s solar-hybrid refrigerator-freezer illustrating the pivot to self-supply capability for up to 24 hours under typical use[2]Defy Appliances, “Defy Launches Solar-Powered Off-Grid Fridge, Freezer Range,” Engineering News, engineeringnews.co.za. Retail dynamics in Gauteng show cautious expansion and a focus on resilience-driven assortments, which sustains the emphasis on energy-optimized appliances across large and small formats. Tariff increases implemented in 2025 keep the spotlight on consumption management features that reduce operating costs over the appliance lifecycle. This combination of tariff signals and reliability concerns is reinforcing willingness to pay for inverter compressors, efficient insulation, and feature sets that extend runtime during load-shedding events. As a result, the South Africa kitchen appliances market shows an elevated share of product launches built around energy resilience and power quality protection for 2026 ranges.

Growing Middle-Income Housing Stock in Peri-Urban Zones

In South Africa, policy focus on energy-efficient housing and addressing unreliable electricity supply (load shedding) is driving electrified kitchen adoption. This shift expands the market for energy-efficient appliances, as consumers increasingly seek products offering cost savings and energy security, particularly in formal and transitioning communities. The Social Housing Regulatory Authority’s 2025–2030 plan prioritizes energy-efficient infrastructure in designated zones, which supports the uptake of efficient refrigerators, cookers, and countertop devices that balance performance and low power draw. For first-time buyers and rental households, compact multi-function appliances are favoured for flexibility and space efficiency, while nuclear families continue to anchor demand for core large appliances such as refrigerators and ovens. Refrigerators and freezers retain category leadership by value as households prioritize food safety and storage, while quick-cook devices such as air fryers expand fastest, reflecting evolving meal-prep habits in urban corridors. This housing-driven mix effect contributes to steady volume circulation across the South Africa kitchen appliances market through 2031.

Migration of Global Brands' Assembly Lines to South Africa

Localized assembly strategies are accelerating as multinationals position South Africa to serve domestic and sub-Saharan demand, a shift underscored by Haier’s acquisition of Kwikot and associated product ramp plans through 2026[3]Source: Haier Smart Home Co., Ltd., “Haier Smart Home Announces to Complete Acquisition of Kwikot,” PR Newswire, prnewswire.com. Coastal logistics platforms and industrial zones provide advantages for component inflows and finished goods distribution, enabling brands to capture duty preferences and reduce time to market for high-velocity SKUs. Policy incentives for renewable energy investments at the plant level further support cost management and power reliability for assembly operations, particularly where rooftop generation and wheeled power can offset grid constraints. As localization deepens, brands can tailor features like inverter compressors and smart diagnostics to local power conditions, which increases product-market fit across price tiers. The South Africa kitchen appliances market gains resilience from this manufacturing pivot, as closer-to-demand assembly enhances availability and stabilizes supply chains in the face of global disruptions.

Surge in E-Commerce "Pay-as-You-Cook" Financing Models

Credit-enabled retail remains a core lever for appliance access and supports online and omnichannel growth as consumers spread payments on mid-ticket items. Lewis Group reported merchandise growth in its latest fiscal year, with appliances representing a meaningful share of sales, a signal that installment plans continue to underpin purchase decisions in a tight consumer environment. As leading platforms and retailers integrate buy-now-pay-later providers, smaller countertop appliances like air fryers and electric cookers benefit from lower upfront cost hurdles, which boosts frequency of purchase in dense urban markets. The South Africa kitchen appliances market thus sees rising online penetration for small appliances, while large-format purchases still rely on omnichannel journeys that include in-store evaluation and delivery coordination. Credit-backed channel innovation supports both replacement cycles and first-time ownership, keeping sell-through steady despite macro headwinds. The convergence of credit retail and e-commerce is expected to sustain demand for energy-efficient product configurations in 2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent power-supply instability & higher tariffs | -1.1% | National, most acute in Gauteng and Eastern Cape municipalities | Medium term (2-4 years) |

| Currency volatility is inflating imported component costs | -0.6% | National, affecting brands reliant on Chinese and Turkish sub-assemblies | Short term (≤ 2 years) |

| Limited rural after-sales & cold-chain service coverage | -0.4% | KwaZulu-Natal, Eastern Cape, Limpopo, and Mpumalanga rural districts | Long term (≥ 4 years) |

| Low household credit approval rates for appliance financing | -0.8% | National, concentrated where unemployment is above 30% | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Power-Supply Instability & Higher Tariffs

Power tariffs increased in 2025 and remain a material headwind for appliance operating costs, which influences purchase timing and capacity choices for large appliances such as refrigerators. Households prioritize products with efficient compressors and insulation as part of bill management, which in turn affects the mix within the South Africa kitchen appliances market toward higher-efficiency models. Load-shedding persistence also compels buyers to weigh resilience features and to defer non-essential upgrades in favour of essential categories, which moderates growth in certain small appliance lines. Retailers and manufacturers respond with awareness campaigns on energy-efficient operation and with promotions centred on inverter-ready bundles that amplify savings under new tariff schedules. This environment compresses discretionary segments while supporting the core categories that are most sensitive to power reliability.

Currency Volatility Inflating Imported Component Costs

Exchange rate swings affect the landed cost of compressors, control boards, and metals that feed local assembly lines, with pricing decisions reflecting a balance between margin protection and consumer affordability. Local assembly reduces exposure to some finished-good duties but does not eliminate reliance on imported subcomponents, which keeps sensitivity to currency movements elevated for mid and high-end models. The South Africa kitchen appliances market reacts with price segmentation that preserves entry-level access while channelling premium features into models with stable supply contracts. Procurement teams extend hedging horizons and adjust SKU portfolios to maintain availability, yet intermittent volatility can still prompt mid-cycle price adjustments that dampen volume. Continued investment in localized content and strategic sourcing helps moderate these cost pressures over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refrigerators Dominate, Yet Air Fryers Lead Growth

Refrigerators and freezers captured 32.91% of the South Africa kitchen appliances market share in 2025, supported by sustained prioritization of cold storage, energy-efficient compressors, and resilience features that preserve food quality during outages. Air fryers are the fastest-growing small appliance category at a 4.62% CAGR through 2031, reflecting changing meal-preparation patterns and buyer preference for compact, multi-use devices. IoT integration and app-based guidance strengthen the small-appliance value proposition, with Philips integrating NutriU to enable guided cooking and energy-aware decisions. In the South Africa kitchen appliances market, dishwashers maintain a niche profile, while demand for range hoods and modern cooktops grows in step with formal housing delivery. Premium ovens and built-in formats remain more sensitive to tariff-linked running costs, where buyers weigh energy and space considerations before replacing legacy units.

The South Africa kitchen appliances market size for air fryers is forecast to expand at a 4.62% CAGR through 2031 as compact formats and rapid-cook features gain adoption within rentals and smaller homes. Refrigerators and freezers continue to anchor value due to essential storage needs and the priority buyers place on efficient operation under tariff and grid constraints. Smart features are spreading within core categories, where predictive maintenance and cycle optimization add perceived value to mid and premium tiers. Solar-hybrid refrigerators and inverter-driven motors reflect a clear design pivot, with local availability improved by manufacturers’ localization strategies. Overall, the South Africa kitchen appliances market shows a balanced product mix that aligns feature sets to household budgets and operating realities.

By End User: Residential Segment Anchors Demand

The residential segment accounted for 73.32% of sales in 2025 and is forecast to expand at a 4.35% CAGR, driven by household formation in peri-urban zones and increased availability of efficient appliances through retail finance options. Policy frameworks that target energy-efficient housing and infrastructure upgrades create multi-year momentum for kitchen appliance adoption in formal developments and upgrading communities. Within households, refrigerators, microwaves, and cookers anchor the essential set, while countertop formats such as air fryers and blenders scale with lifestyle trends. The South Africa kitchen appliances market benefits from the breadth of the residential installed base and from repeat purchases tied to replacement cycles. Financing access through retailers supports steady throughput for both essential and upgrade purchases under budget constraints.

Commercial buyers represent the remaining share and focus on performance, reliability, and service agreements that minimize downtime, with procurement often concentrated in hospitality, catering, and institutional kitchens. Load-shedding considerations and tariff structures influence the business case for capital equipment, which elevates the role of energy efficiency and maintenance support in decision-making. The South Africa kitchen appliances industry continues to see commercial investment in efficient refrigeration and cooking lines where throughput and power stability are most critical. Over the forecast window, residential volumes remain the primary growth engine, while commercial demand expands in targeted categories aligned to service-level needs. This two-speed profile keeps category leaders focused on differentiated road maps for home and professional use cases.

By Distribution Channel: Online Gains Accelerate

B2C retail channels accounted for 72.31% in 2025, with multi-brand stores and exclusive brand outlets anchoring showroom-driven sales for large appliances and higher-end small appliances. The online sub-segment is projected to grow at a 5.16% CAGR through 2031, supported by installment-led affordability, quick delivery for small appliances, and improved after-sales coordination. The South Africa kitchen appliances market continues to diversify channel participation as retailers improve omnichannel experiences that combine in-store consultation with digital checkout. Direct-to-consumer brand sites support exclusive launches and curated bundles that emphasize energy-efficient features. B2B channels serve institutional buyers through negotiated contracts, logistics coordination, and service-level commitments that support critical operations.

The South Africa kitchen appliances market size allocated to online channels is projected to expand at a 5.16% CAGR as digital credit partners and straightforward fulfillment models improve conversion in urban areas. Multi-brand chains maintain strong reach through broad assortments and finance desks that streamline approvals for qualified buyers. Exclusive brand stores concentrate in major metros where experiential displays support premium positioning and service enrolments. B2B flows remain more concentrated in refrigeration and cooking equipment for hospitality and corporate kitchens, with procurement tied to reliability and total cost of ownership. The South Africa kitchen appliances market shows a channel mix that balances reach, experience, and affordability across the value chain.

Geography Analysis

Gauteng held 41.23% in 2025, reflecting its concentration of retail infrastructure and logistics nodes across Johannesburg and Pretoria within the South Africa kitchen appliances market. The province recorded zero quarterly growth in GDP-R during Q1 2025 and posted soft retail expansion, which signals cautious inventory and a focus on resilient product lines suited to current power and income conditions. Retailers adjusted assortments toward inverter-ready and efficient appliances as households navigated tariff increases and load-shedding. Gauteng’s logistics density continues to support quick replenishment and broad brand availability across price points. The South Africa kitchen appliances market in Gauteng remains the benchmark for nationwide channel execution and urban consumer adoption patterns.

The Western Cape is the fastest-growing geography with a projected 4.34% CAGR through 2031, supported by a strong base of formal retail, manufacturing clusters, and affluent urban demand that values smart features and energy efficiency. Local industrial platforms and export-facing logistics underpin supply availability and enable responsive product flow to retailers. The South Africa kitchen appliances market in the Western Cape also benefits from product differentiation that pairs design with energy-aware operation for a premium-leaning customer base. Brand stores and curated assortments rise in prominence as buyers seek guided experiences and connectivity features embedded in their kitchen ecosystems. As manufacturers localize assembly and logistics routines, coastal proximity sustains a consistent supply into the province.

KwaZulu-Natal and the Rest of South Africa reflect a mix of urban core opportunities and rural coverage gaps, with logistics improvements and industrial investments enhancing supply positions in coastal hubs. Port and trade zone infrastructure in KwaZulu-Natal supports component inflows for local assembly and distribution into inland markets, which strengthens retailer inventory reliability across key categories. Rural districts still face after-sales limitations that temper premium adoption, which skews assortments toward durable, simpler designs in outlying regions. As service networks expand and cold-chain resilience improves, appliance demand outside major metros can progress in step with power stabilization and income support programs. The South Africa kitchen appliances market therefore grows across provinces with distinct channels and service strategies that reflect local infrastructure realities.

Competitive Landscape

The South Africa kitchen appliances market features a high concentration with global and local brands balancing technology, price points, and service reach to position for steady growth through 2031. Global players emphasize premium features such as AI-assisted cycles, inverter compressors, and app ecosystems that align with energy management and convenience. Local champions leverage brand familiarity and service networks while adding resilience features tailored to load-shedding conditions. The South Africa kitchen appliances market is thus segmented into clear value tiers, where energy performance and connectivity differentiate models at the top, and repairability and endurance lead at the entry level. Geographic reach and after-sales responsiveness are key battlegrounds that influence brand preference across metros and secondary towns.

Strategic moves in 2025 and 2026 underscore localization and portfolio depth across brands. Haier’s acquisition of Kwikot established a base for expanded product lines and local market entry, with continued rollout in 2026 that targets mainstream price bands. Samsung advanced its AI-enabled home lineup and in-store experiences that foreground energy-saving modes and predictive maintenance[4]Samsung South Africa, “Samsung Unveils AI Bespoke Home Appliances in SA,” Samsung, samsung.com. LG announced a joint development and manufacturing collaboration focused on budget-tier appliances intended for multiple regions, with South Africa positioned as a pilot for competitive pricing and feature sets. The South Africa kitchen appliances market continues to see product launches and marketing campaigns that tie value propositions to tariff realities and load-shedding resilience.

Product road maps merge connected features with durability to meet diverse household needs. Philips leverages its NutriU platform to extend recipe and energy guidance into air fryer experiences, while Defy integrates solar-hybrid capabilities targeting grid-constrained users. Marketing alliances include event sponsorships and regional showcases that boost brand visibility and attach products to lifestyle aspirations. Retail support remains critical, with financing partners enabling monthly repayments that spread ownership into mid-income cohorts. Across 2026, the South Africa kitchen appliances market rewards brands that combine energy efficiency, reliable service, and accessible financing with clear value communication.

South Africa Kitchen Appliances Industry Leaders

Defy Appliances

Samsung Electronics

LG Electronics

Hisense South Africa

Bosch Home Appliances SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Makro introduced the "Beautiful by Drew Barrymore" collection of small kitchen appliances in South Africa in November 2025. The range, featuring air fryers, kettles, blenders, toasters, and stand mixers, is available in physical stores and online, focusing on delivering a combination of modern aesthetics and practical functionality.

- July 2025: Midea announced its official sponsorship of the TotalEnergies CAF Africa Cup of Nations 2025, leveraging tournament reach to promote its Smart Home ecosystem across Southern and East Africa. The activation supports brand visibility in South Africa across retail and online channels. Product storytelling centred on efficiency and connected usage builds awareness within the South Africa kitchen appliances market.

- July 2025: LG Electronics confirmed a joint-development-and-manufacturing agreement for budget-tier refrigerators and washing machines for multiple regions, naming South Africa as a pilot for value-focused SKUs.

- July 2025: Defy committed USD 133.23 million (SAR 500 million) over five years to expand its Jacobs facility in Durban. Producing over 2 million appliances annually, the facility integrates a 1-megawatt rooftop solar system supplying 13% of its electricity, aligning with the company’s cost leadership and renewable energy strategies.

South Africa Kitchen Appliances Market Report Scope

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers & Blenders | |

| Grills & Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Retail Channels | |

| B2B (Direct from Manufacturers) |

By Geography

| Gauteng |

| Western Cape |

| KwaZulu-Natal |

| Rest of South Africa |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers & Blenders | ||

| Grills & Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Countertop Ovens | ||

| Other Small Kitchen Appliances | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Retail Channels | ||

| B2B (Direct from Manufacturers) | ||

| By Geography | Gauteng | |

| Western Cape | ||

| KwaZulu-Natal | ||

| Rest of South Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the South Africa kitchen appliances market?

The South Africa kitchen appliances market size is USD 1.12 billion in 2026 and is projected to reach USD 1.38 billion by 2031 at a 4.29% CAGR.

Which categories lead by value and which are growing fastest in South Africa?

Refrigerators and freezers lead by value with a 32.91% share in 2025, while air fryers are the fastest-growing small appliance category at a 4.62% CAGR through 2031.

How are power tariffs and load-shedding shaping product features in South Africa?

Higher tariffs and reliability concerns are shifting purchases toward inverter-ready, solar-hybrid, and energy-efficient appliances that manage operating costs during power constraints.

What role does financing play in the South Africa kitchen appliances market?

Installment-based retail credit and buy-now-pay-later options support access to both large and small appliances, with retailers reporting ongoing traction for financed purchases.

Which provinces are most important for sales momentum in South Africa?

Gauteng leads by value share in 2025 while the Western Cape is the fastest-growing province to 2031 due to formal retail density and premium adoption.

What company strategies stand out in 2025–2026 in South Africa?

Brands localize assembly, launch AI and smart-connected features, and promote inverter and solar-hybrid products that fit tariff realities, with notable moves by Haier, Samsung, LG, Defy, and Midea.

Page last updated on: