Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

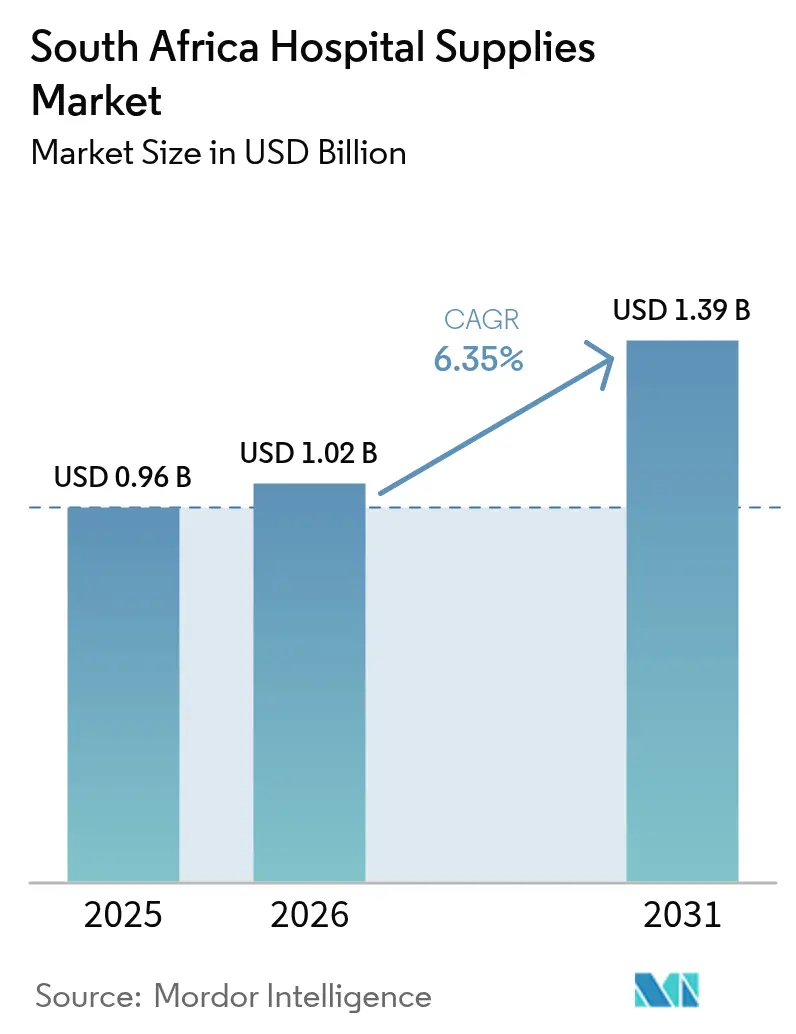

| Base Year Market Size (2025) | USD 0.96 Billion |

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.39 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Hospital Supplies Market Analysis by Mordor Intelligence

The South Africa Hospital Supplies Market size is expected to grow from USD 0.96 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 1.39 billion by 2031 at 6.35% CAGR over 2026-2031.

The panorama blends resilient demand from an ageing population, the widening impact of non-communicable diseases, and a steady pipeline of private-sector bed additions. Disposables remain the largest revenue contributor because infection-control rules create compulsory, recurrent orders, whereas sterilisation devices show the fastest unit growth as facilities tighten hygiene protocols. The 2023 National Health Insurance (NHI) Act signals a medium-term shift toward a single-payer model that will reward value-based tenders, yet near-term momentum still favours well-capitalised private groups extending footprints into secondary cities. Supply-side vulnerability persists because more than 90% of devices are imported, exposing the South Africa hospital supplies market to foreign-exchange swings, freight bottlenecks, and import-duty costs that narrow hospital margins even as local manufacturing incentives gain traction

Key Report Takeaways

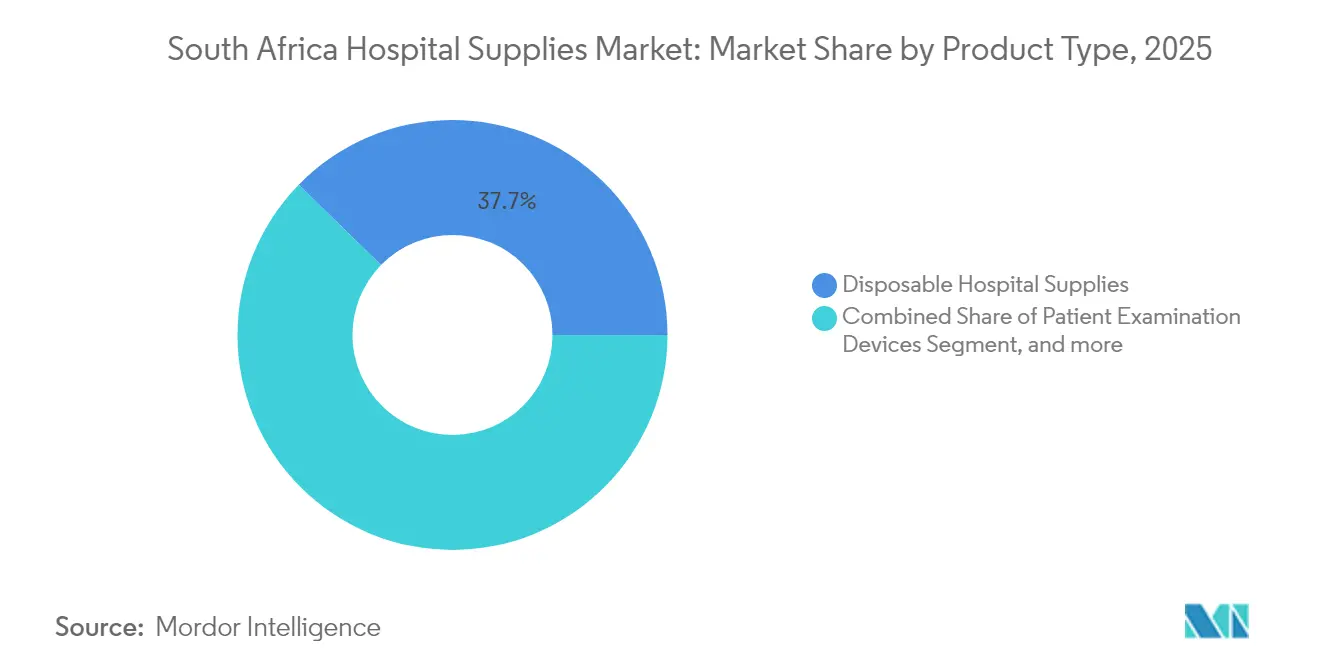

- By product type, disposables led with 37.68% of South Africa hospital supplies market share in 2025 and sterilisation and disinfectant equipment is set to advance at an 7.78% CAGR through 2031.

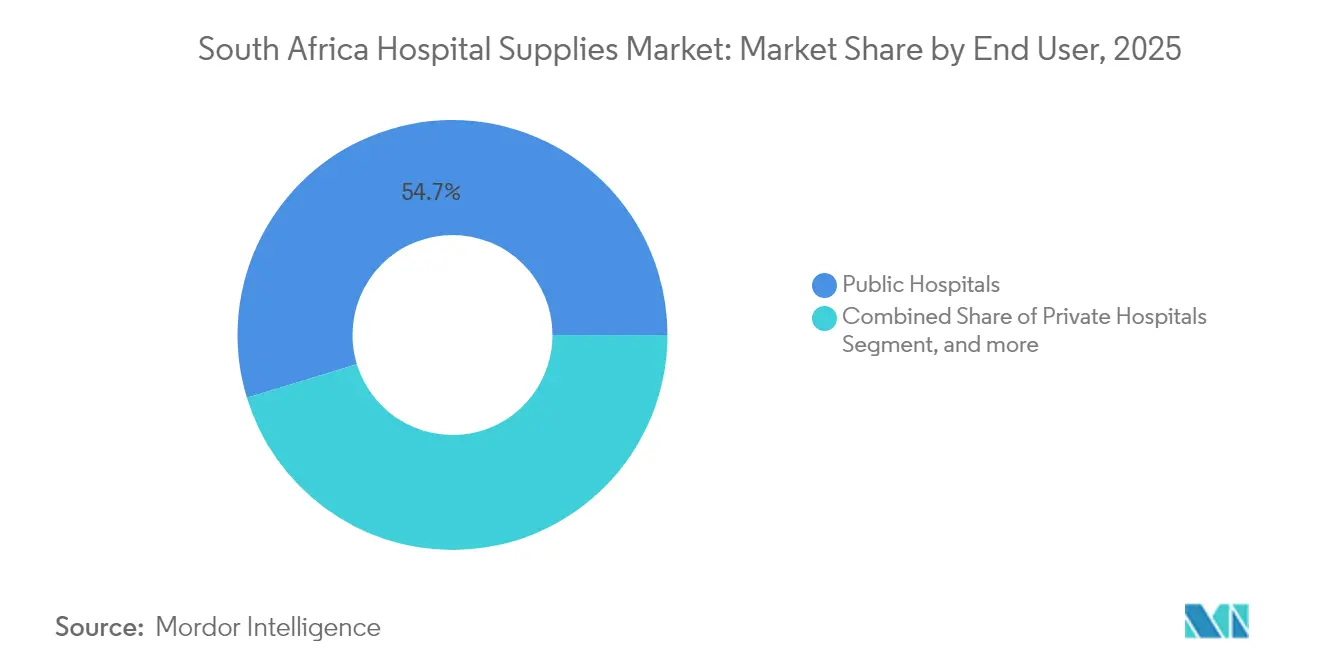

- By end user, public hospitals held 54.72% of South Africa hospital supplies market share in 2025 and specialty clinics and day surgery centres are projected to expand at a 6.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Hospital Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Population & Rising Burden of Non-Communicable Diseases Requiring In-Patient Care | +1.8 | National, urban concentration | Long term (≥ 4 years) |

| Expansion of Private Hospital Groups and Bed Capacity | +2.2 | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Growing Medical Tourism in Region | +0.7 | Johannesburg, Cape Town, Durban | Medium term (2-4 years) |

| Rising Surgical Volumes & Emergency Preparedness | +0.6 | National trauma hubs | Short term (≤ 2 years) |

| Local Manufacturing & Supply Chain Resilience | +0.4 | Gauteng, Eastern Cape | Medium term (2-4 years) |

| Government Initiatives for Universal Healthcare | +0.9 | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing population & rising burden of non-communicable diseases requiring in-patient care

South Africa’s quadruple disease burden now skews toward chronic conditions that demand longer admissions and specialised consumables. Non-communicable diseases account for 55% of national deaths, and a 2025 Nature study showed 55% of adults overweight and 38.2% physically inactive, factors that elevate cardiac, renal, and oncology caseloads.[1]M. Barry, “Obesity and Inactivity in South African Adults,” Nature, nature.com Hospitals respond by expanding telemetry, infusion, and dialysis consumable stockpiles, lifting average supply spend per occupied bed. The South Africa hospital supplies market therefore sees predictable volume growth in drug-delivery sets, glucose strips, and cardiovascular probes even when tariff pressures curb discretionary purchases. Urban tertiary facilities subsequently deploy remote-monitoring peripherals to shorten stays, broadening the addressable base for wearables and home-care extension kits supplied via discharge packs.

Expansion of private hospital groups and bed capacity

Life Healthcare added 58 acute and 24 rehabilitation beds in 2025, committing R2.3 billion (USD 123 million) to imaging suites and operating theatres.[2]Life Healthcare Group, “FY 2025 Interim Results,” lifehealthcare.co.za Lenmed grew total capacity 8.4% to 2,388 beds and targets nearly 3,000 by 2028. Each new ward requires patient monitors, ventilators, and RFID-tagged disposables long before patient intake, creating forward-booked demand that cushions suppliers against procurement lulls elsewhere. Private operators also refresh equipment on five- to seven-year cycles, far quicker than public facilities, which lifts replacement volume for anaesthesia workstations and low-temperature sterilisers. Digitally enabled builds support EMR-interfaced smart pumps and asset-tracking kits, anchoring a higher share of software-linked consumables within the South Africa hospital supplies market.

Growing medical tourism in the region

Inbound patients travel for orthopaedic, cardiac, and cosmetic procedures priced 30-40% below many OECD tariffs. A 2025 study underscored the link between equipment upgrades and medical-tourism growth.[3]B. Deonarain, “Opportunities in South African Medical Tourism,” South African Journal of Science, sajs.co.za Flagship hospitals position for Joint Commission International accreditation by procuring robotic instruments, 4K endoscopes, and hotel-grade patient amenities. Post-operative demand from visiting patients spills into rehabilitation centres, boosting orders for physiotherapy consumables and advanced wound dressings. Private insurers often bundle tourism packages that stipulate high-spec consumables, raising the value per case within the South Africa hospital supplies market.

Government initiatives for universal healthcare

The NHI Act designates the state as single buyer over time, a move set to reshape tender rules without dampening absolute demand. Six new academic hospitals announced in 2024 will extend teaching-facility pipelines for diagnostic imaging, high-throughput sterilisation, and pathology reagents. Domestic-content thresholds embedded in the MEDTECH Master Plan create joint-venture opportunities for tubing, drape, and syringe production, gradually diversifying the South Africa hospital supplies market away from import-only dependence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward Home-Based Care and Day Surgery Centres | -1.2 | Major metropolitan areas | Medium term (2-4 years) |

| High Import Duties on Specialised Equipment | -0.7 | National | Short term (≤ 2 years) |

| Regulatory Complexity & Approval Delays | -0.6 | National | Short term (≤ 2 years) |

| Infrastructure Gaps in Rural Areas | -0.5 | Limpopo, Northern Cape | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift toward home-based care and day surgery centres

The American Hospital Association’s 2025 Workforce Scan highlights global growth in outpatient services, echoing trends in Johannesburg and Cape Town. Smaller-footprint facilities need portable monitors, single-use anaesthesia circuits, and compact sterilisation kits rather than bulky ward stock. Although this transition boosts certain disposables, it suppresses bulk orders for gowns, linens, and multipatient devices typical of lengthy admissions, trimming the South Africa hospital supplies market growth curve.

High import duties on specialised equipment

Medical devices face duties of 10-25% plus permit fees for used units, inflating landed costs. The International Trade Administration notes that public hospitals, which serve 85% of citizens, face budget ceilings that delay replacements. Import Control regulations administered by ITAC add paperwork, prolonging lead times and forcing facilities to run assets beyond optimal service windows. These hurdles impede capital-equipment turnover, indirectly depressing associated high-value consumable sales in the South Africa hospital supplies market until local manufacturing capacity scales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Drive Revenue Stability

Disposable items captured 37.68% of the South Africa hospital supplies market in 2025, a leadership position underpinned by mandatory infection-control compliance. The segment’s defensive profile shields revenues from procurement cycles because gloves, drapes, and syringes are replenished daily regardless of capex freezes. A 2025 Journal of Cleaner Production review flagged significant waste volumes tied to single-use medical plastics, prompting hospitals to trial recyclable polymers and audit supply chains. Even so, immediate infection-control priorities outweigh sustainability concerns, keeping order frequency high.

Sterilisation and disinfectant equipment, though holding a smaller base, is projected to record an 7.78% CAGR to 2031, making it the fastest-growing slice of the South Africa hospital supplies market. COVID-19 legacy protocols expanded ultraviolet room-disinfection cycles and spurred procurement of low-temperature plasma sterilisers. Provincial hospital managers now bake sterilisation capacity into commissioning plans for new theatres, raising average spend per square metre. Patient examination devices and operating-room hardware show mid-single-digit growth as private operators upgrade theatres, while mobility aids cater to the swelling elderly demographic. Collectively, product-type dynamics illustrate a market balancing non-discretionary consumables with technology-heavy investments that unlock safety certifications prized by insurers and foreign patients.

By End User: Speciality Clinics Sector Leads Procurement

Public hospitals accounted for 54.72% of the South Africa hospital supplies market in 2025 thanks to robust cash flows and flexible procurement. Netcare lifted FY 2024 revenue 6.3% to R25.2 billion (USD 1.41 billion) and completed the first phase of an integrated EMR system, spurring demand for device-software interoperability. Private players typically order premium disposables and high-throughput sterilisers to sustain quick-turn theatre schedules, boosting supplier margins.

Specialty clinics and day surgery centres are expected to log a 6.69% CAGR through 2031, reflecting insurer incentives to migrate procedures from high-overhead inpatient wards. These facilities favour compact, easily re-sterilised instrument sets, niche drapes, and portable imaging units that suit short-stay workflows. Public hospitals, though responsible for most patient volumes, secure smaller value shares because treasury-driven tenders focus on lowest-price compliant bids. However, International Finance Corporation loans such as the R200 million facility extended to Lenmed in 2024 widen access to fresh equipment in underserved provinces, nudging public-sector quality upward. Across user categories, procurement strategies increasingly merge device performance with digital-tracking capability, encouraging suppliers to bundle consumables with cloud-based stock-management dashboards.

Geography Analysis

Gauteng, Western Cape, and KwaZulu-Natal collectively absorb the bulk of the South Africa hospital supplies market because these metropolitan provinces house the largest concentrations of private beds and tertiary teaching hospitals. Johannesburg-centred Gauteng benefits from more than one-third of national specialists, leading to dense orders for advanced diagnostics, perfusion kits, and robotic surgical consumables. Durban’s trauma-heavy network in KwaZulu-Natal continuously replaces airway consumables and emergency ultrasound probes to manage high road-accident volumes.

Secondary growth nodes like Mpumalanga and North West Provinces are seeing incremental demand as private groups plant satellite clinics to decongest flagship facilities. These centres typically start with outpatient theatres and diagnostics, creating early-stage demand for modular CSSD (central sterile services department) packs, point-of-care kits, and portable autoclaves. Local governments incentivise investment through accelerated depreciation allowances that partly offset high logistics costs for inbound supplies. Over time, secondary-city penetration levels out geographic concentration by redirecting a fraction of spend away from the traditional tri-metro cluster, yet overall tonnage still anchors around major ports where supply chains are most reliable.

Rural regions such as Limpopo and Northern Cape continue to face infrastructure bottlenecks that slow adoption of sophisticated equipment. Poor road connectivity raises freight expense, prompting public facilities to prioritise basic consumables gloves, IV sets, sutures over capital devices. The National Department of Health’s 2024/25 performance plan allocates refurbishment funds to rural clinics, but progress is gradual. NHI roll-out aims to standardise procurement cross-province, potentially aggregating rural demand into larger, more predictable tenders that favour volume-priced suppliers. Until transport and cold-chain hurdles ease, sophisticated devices will remain concentrated in metropolitan centres, while rural consumption patterns maintain a focus on essential, low-complexity items within the South Africa hospital supplies market.

Regulatory Landscape

South Africa regulates hospital supplies primarily through the South African Health Products Regulatory Authority (SAHPRA) under the Medicines and Related Substances Act and the Medical Device Regulations (Government Gazette 40480). Establishment licensing remains central: manufacturers, importers, exporters, and distributors of Class B, C, and D medical devices need a SAHPRA licence, which standardizes compliance expectations across the import and domestic supply base.

Regulatory requirements have tightened around quality systems and product oversight. SAHPRA communicated that, from 1 June 2025, holders of medical device establishment licences must provide documentary proof of ISO 13485:2016 certification (with verification timelines extending to April 2028). In March 2026, SAHPRA completed a Medical Devices Registration Feasibility Study that moves toward a risk-based approach for device and IVD registration. SAHPRA also reinforced licensing and compliance expectations through stakeholder engagement, including a May 2026 webinar on medical device licensing compliance, adding operational detail for suppliers supplying both public tenders and private hospital groups.

Value Chain Analysis

The value chain spans predominantly imported finished devices and consumables, alongside local production concentrated in lower-complexity categories and selected in-country manufacturing footprints. Upstream activities are driven by global OEM manufacturing and local converting or assembly where applicable; midstream depends on SAHPRA-licensed importers, distributors, and wholesalers. Downstream demand concentrates in public hospital tenders and private hospital group procurement, with clinics and day surgery centres taking on more importance for high-turnover consumables and compact sterilisation needs.

Bottlenecks tend to cluster around regulatory and procurement execution, as well as working-capital constraints. SAHPRA has tightened supply-chain governance by formalizing oversight for outsourced or contracted activities via updated licensing guidance issued in April 2026, lifting compliance expectations for third-party logistics, service providers, and contracted operations supporting distribution and post-market activities. In the public channel, delayed payments and administrative frictions have pressured supplier cash flows. Manual inventory practices and maintenance gaps can also drive stock-outs and service interruptions, increasing the value of distributors with financing capacity, warehousing discipline, and hospital-facing inventory management support.

Competitive Landscape

The South Africa hospital supplies market shows moderate concentration, with the top five multinational and local suppliers holding major combined revenue. Global majors 3M, B. Braun, Becton Dickinson, and Medtronic leverage broad catalogues and R&D pipelines to secure hospital formularies for premium wound care, infusion systems, and electrosurgery disposables. Their ability to bundle consumables with service contracts creates lock-in advantages, especially in private settings that value uptime guarantees.

Local firms such as Aspen Pharmacare and Adcock Ingram exploit intimate knowledge of provincial tender cycles to compete on needles, syringes, and basic drapes. Aspen secured a EUR 500 million (USD 570.3 million) IFC financing package in April 2025 to expand vaccine and essential-medicine manufacturing in Gqeberha, potentially integrating allied plastic-ware production under its “Africa for Africa” strategy. Such moves align with the MEDTECH Master Plan, which requires minimum local-content thresholds in upcoming public tenders. Domestic entrants also benefit from shorter logistics chains that mitigate forex volatility, a selling point when public buyers wrestle with fluctuating rand exchange rates.

Strategic alliances are reshaping market dynamics. Netcare collaborates with Philips to embed bedside-monitor data directly into EMRs, a tie-up that pre-qualifies Philips disposables for system-wide deployment. Lenmed cooperates with Steris for automated CSSD infrastructure in its new wards, securing multi-year consumable commitments. Meanwhile, 3M channels capital into South African adhesive-technology capacity to meet local-content rules. As government procurement gravitates toward value-based frameworks, suppliers must complement catalogue breadth with in-country assembly or technology transfer, reinforcing moderate yet intensifying competition within the South Africa hospital supplies market.

South Africa Hospital Supplies Industry Leaders

B. Braun Melsungen AG

Becton Dickinson and Company

Cardinal Health

3M

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Centralized purchasing and multi-year contracting are creating clear whitespace for suppliers that can scale compliant, high-volume delivery into the public system while maintaining service continuity for private hospital groups. The National Health Insurance (NHI) framework (Act 20 of 2023) establishes a Health Products Procurement Unit for coordinated procurement, and procurement reform work in 2026 introduces tools such as framework agreements and transversal term contracts for recurring, high-volume health products. The RT252-2025 transversal contract structure for surgical instruments and equipment, with a 60-month term running into 2029, shows how demand aggregation is being operationalized, favoring suppliers that can support standardized product catalogs, consistent availability, and reporting across provinces.

Regulatory and localization programs also add differentiated market-entry routes. SAHPRA published the Medical Devices Reliance Guideline in February 2026 to streamline pre- and post-market activities via reliance pathways, which supports faster lifecycle management for multinational portfolios when paired with robust local technical files and vigilance systems. At the same time, SAHPRA communications on ISO 13485:2016 certification (mandatory proof for establishment licence holders since June 2025, with verification to April 2028) and the revised local manufacturing policy (June 2025) reinforce opportunities for in-country manufacturing, assembly, or qualified local partnering. These steps matter most for tender readiness and local-content considerations, particularly in recurrent disposable categories and sterilisation workflows tied to infection-control compliance and theater throughput.

Recent Industry Developments

- April 2026: Becton, Dickinson and Company announced the global launch of the HemoSphere Stream Module for continuous, noninvasive blood pressure monitoring. The release expands BD's advanced monitoring technology stack and strengthens its ability to bundle monitoring hardware with disposables and connected-care workflows used in acute care settings.

- May 2025: Life Healthcare Group announced plans to add 58 acute hospital beds and 24 rehabilitation beds and to expand diagnostic facilities, supported by FY2025 capital expenditure guidance of about R2.3 billion. The build-out lifts baseline consumption of infection-control disposables and increases installed capacity for operating rooms and diagnostics that drive recurring procedure-linked supplies.

- June 2024: IFC and Lenmed Hospital Group partnered on a local-currency senior loan facility of R200 million to support expansion, equipment purchases, and capacity growth across underserved communities. The financing underpins procurement of advanced medical equipment and associated consumables, widening addressable demand beyond the largest metro-based private hospital clusters.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of hospital supplies sold and used in South Africa across core care settings, including items needed for patient examination, operating rooms, mobility support, sterilization, and routine disposable usage.

Scope exclusions: We exclude pharmaceuticals, standalone lab reagents, and consumer retail health products that are not procured for use inside clinical facilities.

Segmentation Overview

- By Product Type

- Patient Examination Devices

- Operating Room Equipment

- Mobility Aids & Transportation Equipment

- Sterilisation & Disinfectant Equipment

- Disposable Hospital Supplies

- Other Types

- By End User

- Public Hospitals

- Private Hospitals

- Speciality Clinics & Day Surgery Centres

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the market boundary, map public and private healthcare demand, and set realistic price and utilization assumptions. We reviewed public health system references such as Statistics South Africa datasets, National Department of Health releases, South African Health Products Regulatory Authority updates, and National Treasury budget documents, which helped anchor the size of the addressable hospital activity.

To translate activity into supply demand, we also relied on sources such as WHO and World Bank health indicators, South African trade and customs statistics for relevant medical supply imports, peer-reviewed clinical and health economics articles, and hospital group annual reporting and investor presentations. When needed, paid subscriptions for company financials and intelligence, and an import and export shipment level database, were used to cross-check supplier exposure and product flow patterns. These examples are not exhaustive, and many other public and subscription sources were used to collect, validate, and clarify the final assumptions.

Primary Interviews and Surveys

Primary work was used to pressure-test desk assumptions on procurement behavior, tender timing, mix shifts between public and private facilities, and typical replacement cycles for key supply categories. We spoke with a mix of hospital procurement and operations leaders, distributors, and category specialists, and then checked consistency across major provinces with higher facility concentration and purchasing activity.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | |

| Mid tier: 52% | Functional/Unit leaders: 31% | |

| Smaller Players: 21% | Managers: 54% |

Market-Sizing & Forecasting

Sizing started from a top-down build where hospital activity, bed capacity, procedure intensity, and procurement budgets are converted into a demand pool for supplies, and then filtered by the share that is actually fulfilled through formal channels. To keep the total realistic, we then corroborated it using selective bottom-up approximations, such as rolling up a sample of supplier and distributor revenues, and sanity-checking with unit volume times average selling price for high-usage categories.

Key inputs used in the model included public versus private facility mix, tender cycles and contract durations, import dependence for selected product groups, price inflation and currency-linked landed-cost movements, replacement and utilization cycles for reusable equipment, and consumption rates for disposable supplies tied to patient throughput. Where bottom-up signals were missing for smaller categories, we used conservative penetration rates and aligned them back to the larger demand indicators.

For forecasting, we leaned on scenario analysis supported by simple regression checks, where drivers like healthcare spending trends, utilization growth, and input-cost pressures were varied and then validated through expert consensus from interviews. Assumptions were kept traceable, so changes in utilization or pricing could be clearly seen in the forecast outputs.

Data Validation & Update Cycle

Validation was done through stepwise triangulation, where totals were checked against independent signals like import trends for relevant product classes, hospital capacity expansion, and procurement pattern changes across the public and private mix. When a line item showed an unusual jump, it was rechecked for unit conversion errors, double counting between product buckets, or an unrealistic price step, and then reviewed again before sign-off.

The report is refreshed annually, and interim updates are triggered if material policy, currency, or supply chain events meaningfully shift demand or pricing. Before delivery, an analyst does a fresh pass across the core inputs and recent developments so the numbers reflect the latest available view.

Mordor Intelligence's South Africa Hospital Supplies Market Size Compared Against Other Published Estimates

Published market sizes for hospital supplies in South Africa can vary even when the titles look similar, because the counted product buckets and the end-user boundary are not always the same. Differences also show up when one estimate leans more on import values, while another leans more on facility spending or supplier revenue coverage.

By tracking category-level inclusion rules and then refreshing currency-linked pricing and tender-cycle timing checks, Mordor Intelligence keeps the total tied to hospital procurement reality rather than a broader medical equipment or consumables universe.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.96 B (2025) | |

| Global Consultancy A | USD 1.80 B (2025) | Uses a wider end-user net that can include clinics, laboratories, and nursing homes, which expands volumes beyond hospital procurement. The scope also appears to bundle adjacent device and furniture categories, which lifts the total for the same base year. |

| Industry Portal B | USD 0.90 B (2022) | Anchors the estimate in an earlier year and can understate current value if pricing and exchange-rate effects are not carried forward consistently. The underlying scope is not clearly separated by hospital-only purchasing, which can also create omissions or overlap across supply buckets. |

The spread in the table is mainly explained by scope boundaries and timing, not just growth assumptions. Once the end-user definition is kept to hospitals, and the pricing and procurement cadence are treated consistently, the estimate becomes easier to reproduce and to update when conditions change.

Key Questions Answered in the Report

What is the current size of the South Africa hospital supplies market?

The market is valued at USD 1.02 billion in 2026.

What compound annual growth rate (CAGR) is forecast for the market?

A CAGR of 6.35% is projected between 2026 and 2031.

Which product segment currently generates the highest revenue?

Disposable hospital supplies lead with a 37.68% share in 2025.

Which product segment is expected to grow the fastest through 2031?

Sterilisation and disinfectant equipment is forecast to expand at an 7.78% CAGR.

Which end-user category accounts for the largest market share?

Public hospitals dominate with 54.72% of market value in 2025.

How will the National Health Insurance (NHI) scheme influence procurement?

NHI will centralize purchasing under a single government buyer, driving larger, value-based tenders and boosting volume certainty for suppliers.

Page last updated on: