Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

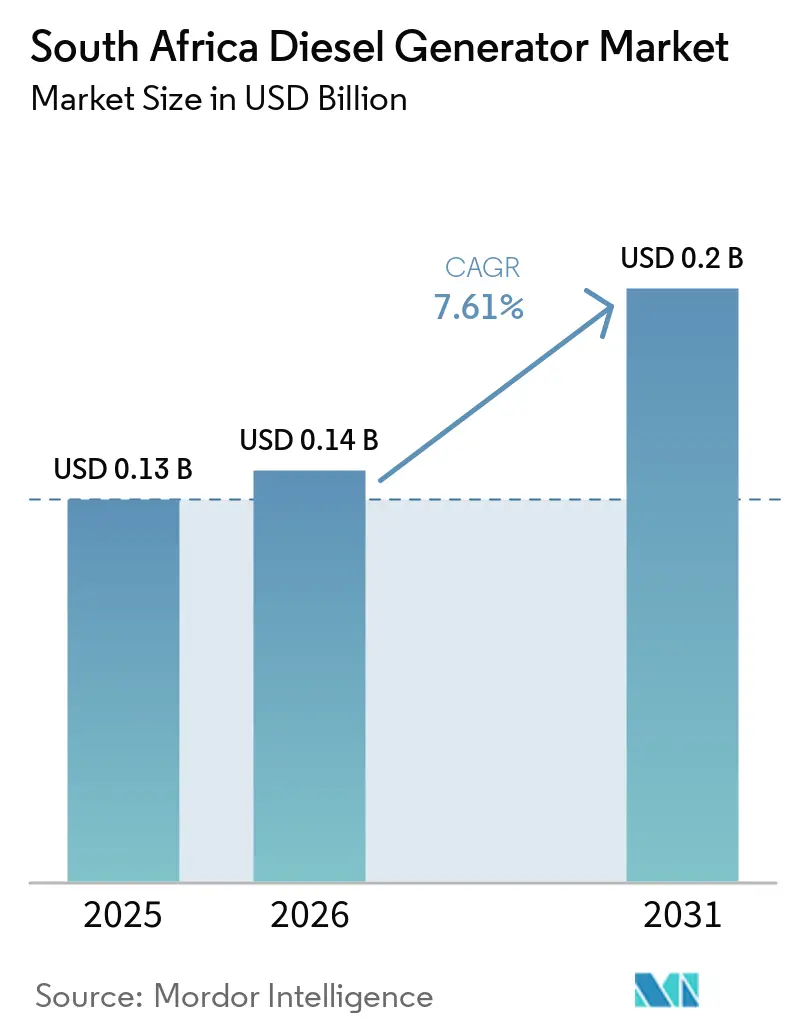

| Base Year Market Size (2025) | USD 0.13 Billion |

| Market Size (2026) | USD 0.14 Billion |

| Market Size (2031) | USD 0.2 Billion |

| Growth Rate (2026 - 2031) | 7.61% CAGR |

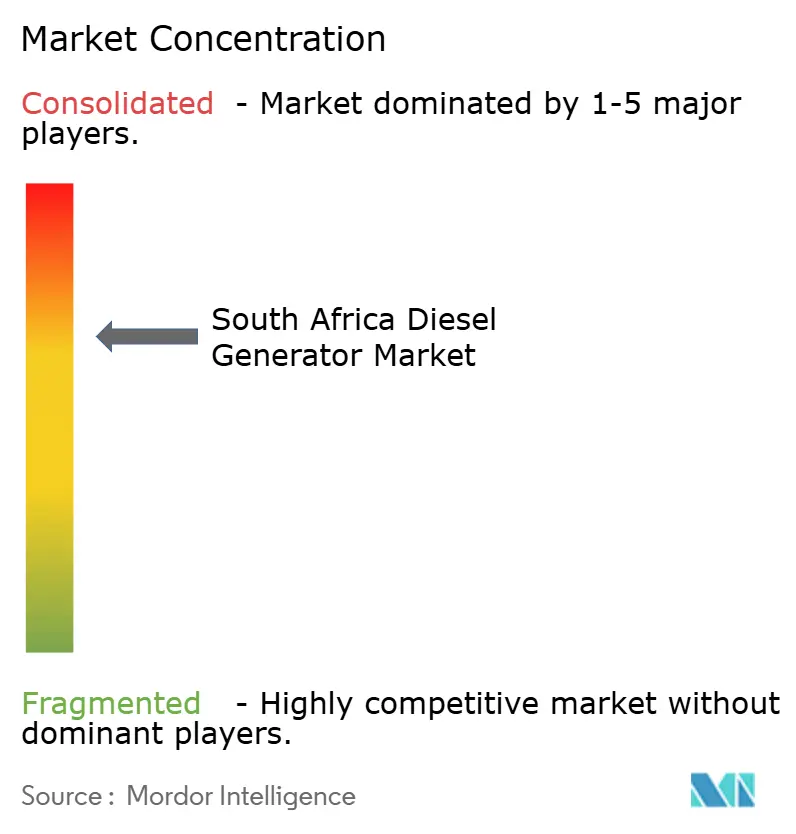

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Diesel Generator Market Analysis by Mordor Intelligence

The South Africa Diesel Generator Market size in 2026 is estimated at USD 0.14 billion, growing from 2025 value of USD 0.13 billion with 2031 projections showing USD 0.2 billion, growing at 7.61% CAGR over 2026-2031.

Commercial and industrial buyers continue to install gensets, as unplanned outages stood at 13,289 MW in January 2025, despite Eskom’s temporary suspension of load-shedding.(1)Eskom, “Energy Availability Factor and Load-Shedding Suspension,” eskom.co.za The sustained risk of Stage 4-6 curtailments keeps demand resilient among data centers, mines, and telecommunications towers, even as Eskom cut Open Cycle Gas Turbine diesel consumption by 48.4% year-on-year and saved roughly ZAR 16 billion in FY 2025. Mid-capacity units (75-375 kVA) benefit from rapid data-center and telco tower build-outs, while prime-power configurations above 2,000 kVA support mining operations in the Northern Cape and Limpopo. Hybrid packages that bundle gensets with solar panels, batteries, and telematics have become the default offer from global OEMs, aligning backup power reliability with tightening emission limits under the National Environmental Management: Air Quality Act (NEM: AQA) 2024.(2)Department of Forestry, Fisheries and the Environment, “NEM: AQA 2024 Amendments,” dffe.gov.za Financing also favors integrated solutions because local banks have introduced exclusion lists for pure-diesel projects but maintain carve-outs for hybrid backup serving critical infrastructure.

Key Report Takeaways

- By capacity, units below 75 kVA captured 39.75% of South Africa's diesel generator market share in 2025, while the 75-375 kVA segment is forecast to expand at an 8.25% CAGR through 2031.

- By application, standby and backup power held 55.10% share of the South Africa diesel generator market size in 2025, whereas prime and continuous power is growing at an 8.02% CAGR.

- By end user, commercial buyers commanded 44.20% share of the South Africa diesel generator market size in 2025, but industrial demand is accelerating at a 9.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Diesel Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging load-shedding frequency | 2.10% | Gauteng, Western Cape, KwaZulu-Natal | Short term (≤ 2 years) |

| Rapid data-center build-out | 1.80% | Gauteng, Western Cape | Medium term (2-4 years) |

| Mining sector electrification gaps | 1.30% | Northern Cape, Limpopo | Long term (≥ 4 years) |

| Telco tower backup mandates | 1.20% | National | Medium term (2-4 years) |

| Local OEM assembly incentives | 0.60% | National | Long term (≥ 4 years) |

| Off-grid hydrogen-diesel pilots | 0.40% | Northern Cape, Limpopo | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Load-Shedding Frequency Drives Standby Capacity Procurement

Eskom's Energy Availability Factor improved from approximately 55% in 2023 to 60-70% in 2024; however, unplanned outages remained elevated at 13,289 MW in January 2025. Commercial and industrial users, therefore, keep standby gensets on-site even during blackout-free periods. Telecommunications operators invested ZAR 930 million in 2023 to purchase approximately 3,268 generators, ensuring compliance with ICASA's quality-of-service rules.(3)ICASA, “State of the ICT Sector Report,” icasa.org.za Data-center operators added diesel redundancy alongside sizeable solar farms to meet both reliability and sustainability tests, as illustrated by Teraco's 40 MW JB7 expansion in Johannesburg.(4)Teraco, “JB7 Expansion,” teraco.co.za Procurement cycles accelerate whenever grid stress re-emerges, giving the driver a pronounced short-term influence on the South Africa diesel generator market. Medium-term impact depends on Eskom's ability to sustain an availability factor above 65% beyond 2026.

Rapid Data-Center Build-Out Anchors Mid-Capacity Demand

The local data center market grew from USD 471 million in 2024 to a projected USD 1.1 billion by 2029, lifting the critical IT load from 435 MW to almost 829 MW. Teraco alone operates 228 MW of critical power and will add 71,000 m² of white space by 2026, all supported by N+1 diesel gensets in the 750-2,000 kVA range. Although operators integrate sizable on-site solar capacity, diesel remains the principal backup fuel because batteries cannot yet provide multi-hour autonomy during prolonged grid failures. Caterpillar’s 80% diesel-reduction microgrids for telco towers prove the appetite for hybrid systems, yet Uptime Tier III and IV certifications still mandate redundant diesel strings. As hyperscale clouds cluster in Gauteng and Western Cape, the South Africa diesel generator market benefits from a predictable pipeline of mid-capacity orders through 2030.

Mining Sector Electrification Gaps Sustain Prime-Power Demand

Anglo American Platinum’s 2 MW hydrogen-battery haul truck, deployed in 2025, shows the sector’s long-term decarbonization ambition, but the innovation targets mobile equipment rather than a stationary plant. Remote pits require reliable electricity for crushers, conveyors, and ventilation systems; hence, mining firms still deploy gensets rated above 2,000 kVA for prime power. Kumba Iron Ore installed a 40 MW solar array at Sishen; however, diesel gensets remain the primary source of power for continuous loads. The Hydrogen Valley initiative positions Northern Cape and Limpopo as test beds for hydrogen-diesel dual-fuel systems, although high electrolyser costs curb near-term adoption. Mining’s multi-decade asset life means current diesel infrastructure will persist, underpinning long-term growth in the South Africa diesel generator market.

Telco Tower Backup Mandates Expand Distributed Generation

ICASA regulations stipulate uninterrupted service, compelling mobile operators to self-provision backup. Roughly 3,268 gensets were purchased in 2023, powering towers mainly in the 75-375 kVA class. Caterpillar’s hybrid design reduces diesel use by 80%, utilizing a combination of solar, batteries, and generators to lower operating costs. Because towers are excluded from NRS 048-9 critical-load priority, network owners cannot rely on expedited grid support, reinforcing dependency on distributed generation. Tower proliferation in the rural Eastern Cape and Limpopo, along with ongoing 4G and 5G densification, sustains medium-term momentum for this demand driver.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightened national emission limits | -1.10% | Priority Areas in Gauteng, Mpumalanga, Limpopo | Medium term (2-4 years) |

| Diesel price volatility | -0.90% | National, inland prices highest | Short term (≤ 2 years) |

| Rooftop solar plus BESS adoption | -1.40% | Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Green-financing exclusion lists | -0.70% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightened National Emission Limits Raise Compliance Costs

The NEM: AQA 2024 amendments require continuous monitoring and stricter ambient limits for sulfur dioxide, nitrogen dioxide, and particulate matter. Operators must retrofit selective catalytic reduction and diesel particulate filters, adding 8-12% to the capital expenditure (capex) for generators above 750 kVA. MTU’s Stage IIIA-compliant Series 4000 engines already meet the standard, giving larger OEMs a compliance advantage, whereas many legacy fleets in the below-375 kVA bracket face early retirement. Enforcement ramps up through 2027, moderating the CAGR of the South African diesel generator market during the transition.

Accelerating Rooftop Solar and BESS Adoption Displaces Diesel in Peak-Shaving

Scatec’s 540 MW solar and 1,140 MWh battery project in Kenhardt demonstrates how large-scale storage can replace diesel peakers for evening demand. Eskom’s own storage procurements plus three BESS IPP rounds totaling 1,744 MW and 6,976 MWh illustrate the policy push. At the customer level, C&I buyers in Gauteng and Western Cape achieve levelized storage costs below ZAR 2.00/kWh, undercutting diesel when pump prices exceed ZAR 20/liter. While data centers and telecom towers still require multi-hour diesel autonomy, solar-plus-storage now handles daytime peak shaving, reducing future operating hours for standby generators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Small Units Dominate, Mid-Range Accelerates

Below 75 kVA gensets secured 39.75% of South Africa's diesel generator market share in 2025, driven by a surge in residential demand during the 2022-2023 load-shedding crisis. Demand cooled once load-shedding was paused for 100 days in 2024, yet Generac's solar-battery-diesel packages continue to keep the segment active among homeowners seeking resilient power. The 75-375 kVA class, forecast to grow at 8.25% CAGR, matches telecom tower and edge-data-center requirements, and OEM incentives encourage local assembly that trims lead times and import duties. In contrast, the 375-750 kVA bracket caters to hospitals and municipal water plants that fall under NRS 048-9 critical-load rules, maintaining high utilization even as battery storage improves.

Units between 750 kVA and 2,000 kVA underpin Tier III data-center redundancy; Teraco's JB7 build specifies N+1 sets in this range to meet Uptime criteria. Above 2,000 kVA, prime-power mining orders dominate because grid extensions to remote Northern Cape sites remain uneconomic. Atlas Copco's new QAS 500 Vx rental model reflects a market shift toward modular, towable power that enables users to scale capacity as outage patterns change. Emission compliance favors Tier III engines, benefiting OEMs that deliver ready-to-operate packages, and creates a replacement cycle among older sub-375 kVA fleets.

By Application: Standby Dominates, Prime Power Gains in Mining

Standby and backup uses held 55.10% of South Africa's diesel generator market share in 2025, thanks to data centers, telecom towers, and South Africa commercial real estate that rely on grid power but maintain diesel generators for backup. Hybrid microgrids now curtail runtime, yet diesel strings remain essential because battery chemistries still struggle to achieve autonomy of more than 8 hours at acceptable costs. Prime and continuous duty, expanding at an 8.02% CAGR, is led by mining sites where crushers and conveyors require a 24/7 supply, which is unavailable from weak grids. Cummins' Johannesburg microgrid, capable of running on hydrotreated vegetable oil or biodiesel, showcases prime-power evolution toward lower-carbon fuels.

Peak-shaving applications lag because battery storage offers cheaper arbitrage. Nevertheless, Aggreko's rental hybrids reduce fuel use by up to 50% and provide construction clients with the flexibility to adjust capacity as project loads fluctuate. In standby scenarios, Caterpillar's telco tower system achieves an 80% fuel reduction by combining solar energy, lithium-ion batteries, and 75-375 kVA gensets. As long as ICASA mandates uninterrupted telecom service, mobile operators will maintain diesel redundancy, protecting the largest application's share through 2031.

By End User: Commercial Leads, Industrial Accelerates

Commercial facilities, including data centers, malls, hotels, and office parks, held 44.20% of South Africa's diesel generator market size in 2025. Teraco's R8 billion green-loan package underscores how lenders continue to support diesel backup when paired with on-site renewables that offset Scope 2 emissions. The industrial segment, however, shows the fastest growth rate of 9.35% CAGR, as mining companies in the Northern Cape and Limpopo deploy prime-power gensets and manufacturing plants run hybrid microgrids to secure production. Residential demand has moderated because rooftop solar panels, combined with lithium-ion batteries, now provide silent backup in suburban neighborhoods, reducing reliance on small petrol or diesel units.

Mining's FutureSmart strategy highlights long-term substitution risk; nonetheless, stationary gensets above 2,000 kVA remain entrenched until the costs of electrolyzers and batteries decline significantly. Sibanye-Stillwater and Kumba Iron Ore already integrate renewables; however, crushers and ventilation systems still draw from diesel due to high-load, multi-shift operations. Telecommunications straddles both commercial and industrial categories; the roughly ZAR 930 million spent on generators during 2023 attests to the ongoing relevance of diesel for distributed sites.

Geography Analysis

Gauteng anchors the South Africa diesel generator market with the densest cluster of data centers, corporate head offices, and retail complexes. Teraco's facilities provide 228 MW of critical power, and its JB7 expansion cements Johannesburg as the sub-Saharan cloud hub. Western Cape follows, leveraging Cape Town's strong fiber backbone and proactive municipal solar policies that encourage hybrid backup designs. KwaZulu-Natal features Durban at the southern end of the Hydrogen Valley corridor; local logistics assets and port operations require standby gensets to guard against grid disturbances. The Northern Cape and Limpopo dominate the country's prime power demand. Anglo American Platinum's Mogalakwena and Kumba Iron Ore's Sishen mines utilize diesel arrays exceeding 2,000 kVA, as grid reinforcement remains costly. While hydrogen pilots advance, stationary loads still depend on diesel for the foreseeable future. The Eastern Cape and Free State exhibit high telecom tower density in rural zones, driving the need for distributed power in the 75-375 kVA range, alongside Caterpillar's 80% fuel-savings hybrid tower solution. Mpumalanga, home to the bulk of coal-fired plants, paradoxically keeps standby generators on industrial sites because its older transmission infrastructure suffers from chronic faults.

Emission-control enforcement varies by province; Gauteng's Priority Area plan enforces stricter limits sooner, nudging operators toward Tier III hardware. Diesel pricing skews higher inland, reaching up to ZAR 22.45/liter in April 2025, which raises operating expenses for prime-power users compared to coastal buyers. Large-scale BESS procurements are concentrated in the Northern Cape's solar belt, where the Kenhardt project has already displaced some diesel peaking capacity, hinting at regional differences in substitution risk.

Competitive Landscape

Competition is moderately fragmented. Caterpillar, Cummins, Aggreko, MTU, and Atlas Copco head the field, but numerous regional distributors and rental specialists vie for a share. Global OEMs increasingly localize assembly to meet Department of Trade, Industry, and Competition incentives and to mitigate currency-linked import costs. Caterpillar’s alignment with the Africa Data Centres Association and its tower hybrids reflects a shift toward integrated power solutions rather than standalone generators. Aggreko’s Greener Upgrades rental model captures customers facing variable load-shedding schedules and sustainability reporting pressures.

Cummins differentiates itself through HVO-ready engines and on-site microgrids that blend solar energy with diesel, appealing to clients who need lower Scope 1 emissions while preserving reliability. MTU gains traction with Stage IIIA engines that meet NEM: AQA standards without costly retrofits. Atlas Copco’s QAS 500 Vx marks a shift toward modular rental, enabling quick redeployment as outage risks evolve. Green-financing exclusion lists from Standard Bank, Absa, and Nedbank steer borrowers toward hybrid solutions rather than pure-diesel projects, indirectly favoring OEMs able to integrate renewables. Opportunities remain in hydrogen-diesel dual-fuel systems and IoT-driven predictive maintenance that lower lifetime ownership costs for enterprise buyers.

South Africa Diesel Generator Industry Leaders

Cummins Inc.

Caterpillar Inc.

Aggreko plc

HIMOINSA (Yanmar)

Kohler SDMO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Teraco secured an R8 billion loan to expand the JB7 data center in Johannesburg, adding 40 MW of critical power with a co-located 120 MW solar plant.

- December 2024: Scatec commissioned the 540 MW solar plus 1,140 MWh battery Kenhardt project, South Africa’s largest utility-scale storage facility.

- November 2024: DMRE awarded 616 MW and 2,464 MWh in Battery Energy Storage IPP Programme Round 3, lifting the cumulative three-round total to 1,744 MW and 6,976 MWh.

- October 2024: Atlas Copco has added the 500 kVA QAS 500 Vx to its local rental fleet, targeting construction and event power clients.

- September 2024: Caterpillar joined the Africa Data Centres Association and rolled out tower hybrid microgrids that cut diesel use by 80%

- August 2024: Generac introduced the Mobile Link platform, which allows small-generator owners to track performance via smartphone apps.

South Africa Diesel Generator Market Report Scope

The South Africa diesel generator market report includes:

By Capacity (kVA)

| Below 75 kVA |

| 75 to 375 kVA |

| 375 to 750 kVA |

| 750 to 2,000 kVA |

| Above 2,000 kVA |

By Application

| Stand-by/Backup Power |

| Prime/Continuous Power |

| Peak-shaving/Load Management |

By End User

| Residential |

| Commercial |

| Industrial |

| By Capacity (kVA) | Below 75 kVA |

| 75 to 375 kVA | |

| 375 to 750 kVA | |

| 750 to 2,000 kVA | |

| Above 2,000 kVA | |

| By Application | Stand-by/Backup Power |

| Prime/Continuous Power | |

| Peak-shaving/Load Management | |

| By End User | Residential |

| Commercial | |

| Industrial |

Key Questions Answered in the Report

What is the forecast value for South African diesel genset demand by 2031?

The South Africa diesel generator market is estimated to reach USD 0.2 billion by 2031 based on a 7.61% CAGR.

Which capacity bracket shows the fastest growth?

Gensets rated 75-375 kVA are expected to expand at an 8.25% CAGR, driven by data-center edge nodes and telco towers.

Why do mines still rely on diesel?

Remote Northern Cape and Limpopo sites lack economical grid extensions, so operators use prime-power gensets above 2,000 kVA for continuous loads.

How are emission rules affecting purchasing decisions?

NEM: AQA 2024 introduces stricter limits, prompting buyers to select Tier III hardware or hybrid packages to remain compliant.

Are batteries replacing diesel in backup roles?

Battery energy storage handles peak-shaving economically, yet multi-hour autonomy needs keep diesel strings in place for data centers and telecom towers.

Which companies lead hybrid generator solutions?

Caterpillar, Cummins and Aggreko bundle gensets with solar and batteries, achieving fuel cuts of 50-80% in several pilot projects.

Page last updated on: