South Africa Oral Anti-Diabetic Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

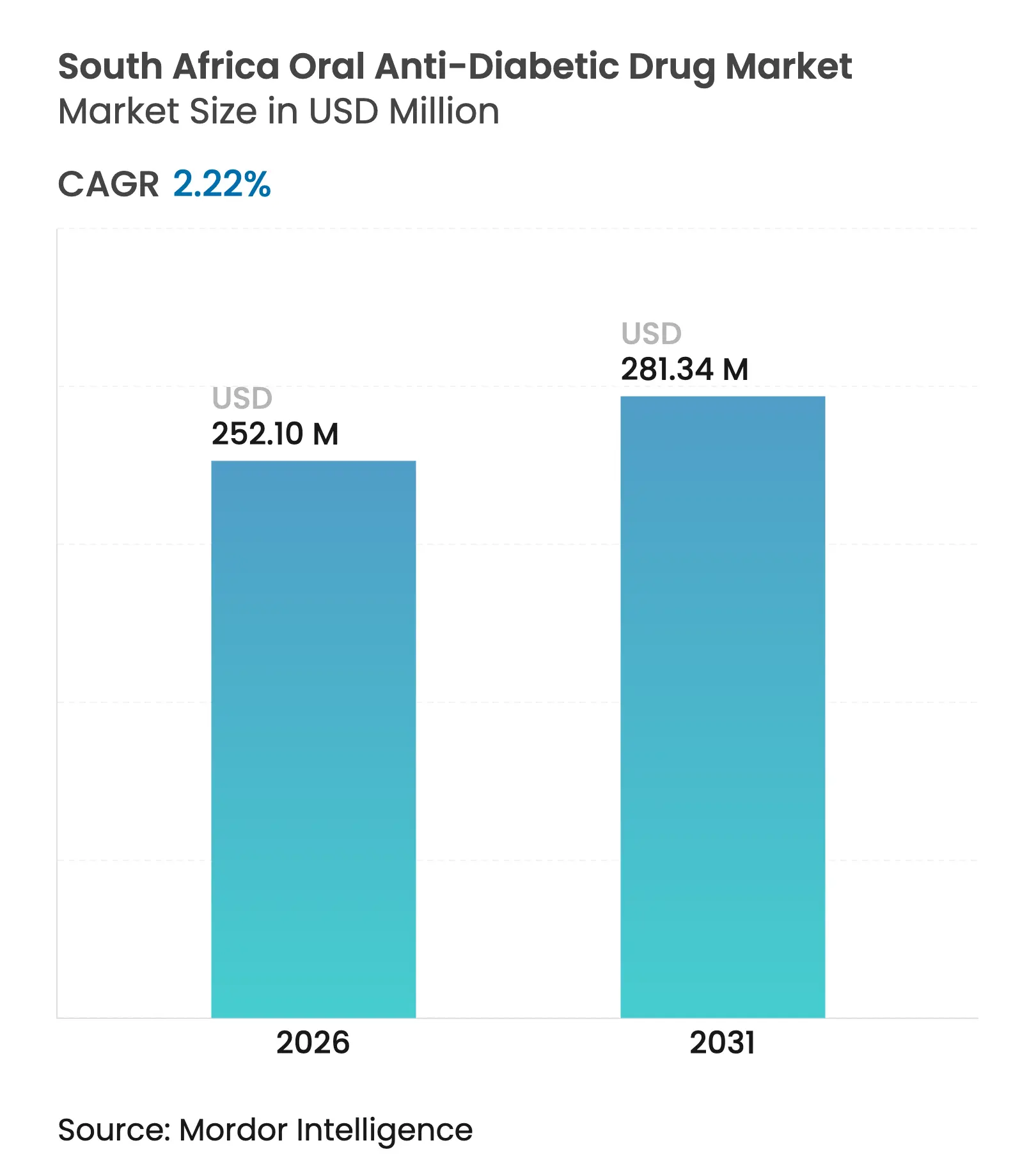

| Market Size (2026) | USD 252.1 Million |

| Market Size (2031) | USD 281.34 Million |

| Growth Rate (2026 - 2031) | 2.22 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

South Africa Oral Anti-Diabetic Drug Market Analysis by Mordor Intelligence

The South Africa oral anti-diabetic drug market size is expected to grow from USD 246.62 million in 2025 to USD 252.1 million in 2026 and is forecast to reach USD 281.34 million by 2031 at 2.22% CAGR over 2026-2031. Demand continues to grow because more than 4 million South Africans live with diabetes, yet only 23% achieve recommended glycemic targets [1]University of Pretoria, “Glycemic Control Audit,” up.ac.za , signaling large volumes of undertreated patients. Momentum is reinforced by cardiovascular-outcome data for newer agents, the government’s non-communicable disease (NCD) strategy, and accelerating uptake of e-pharmacy services that improve refill convenience. Conversely, single-exit price controls, high out-of-pocket costs for innovative molecules, and periodic active-pharmaceutical-ingredient shortages temper revenue growth, requiring manufacturers to balance volume aspirations with pricing realities [2]Daniel V. O’Hara, "Applications of SGLT2 inhibitors beyond glycaemic control," Nature Reviews Nephrology, nature.com. Competitive positioning now hinges on pipeline depth in SGLT-2 inhibitors, local manufacturing resilience, and the ability to secure public-sector tenders in the South Africa oral anti-diabetic drug market.

Key Report Takeaways

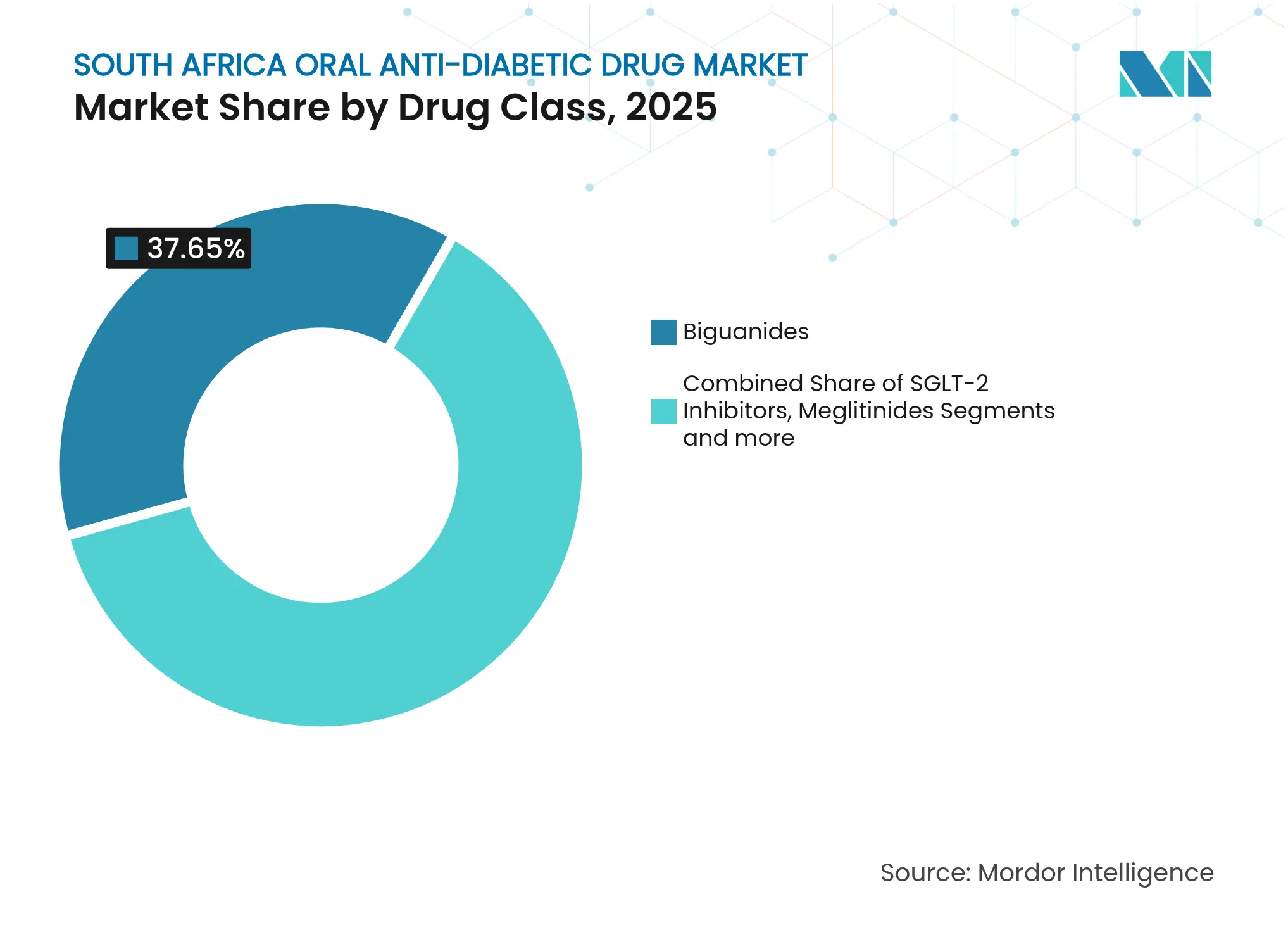

- By drug class, biguanides led with a 37.65% revenue share in 2025, while SGLT-2 inhibitors post the fastest 3.06% CAGR through 2031 in the South Africa oral anti-diabetic drug market.

- By age group, adults held 65.80% of the South Africa oral anti-diabetic drug market share in 2025; the geriatric cohort is expanding at a 3.03% CAGR to 2031.

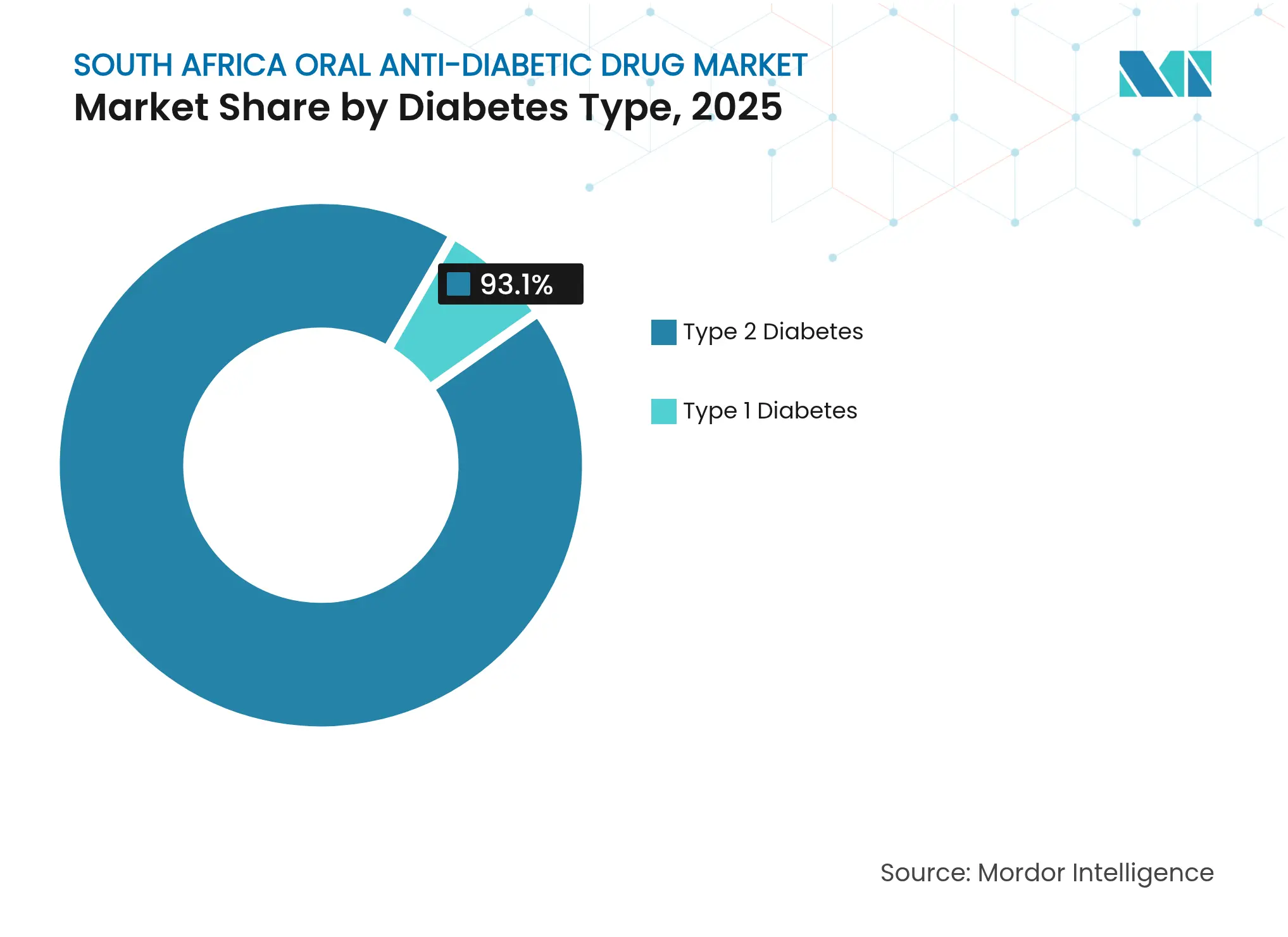

- By diabetes type, Type 2 diabetes accounted for a dominant 93.10% share in 2025 and records the highest 2.97% CAGR to 2031.

- By distribution channel, hospital pharmacies controlled 68.90% of revenues in 2025, whereas online pharmacies grow the quickest at 3.15% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Oral Anti-Diabetic Drug Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Prevalence surge in Type-2 diabetes

Prevalence surge in Type-2 diabetes

| +0.8% | National; highest in urban areas | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+0.8%

|

Geographic Relevance

:

National; highest in urban areas

|

Impact Timeline

:

Long term (≥ 4 years)

|

National NCD strategic plan boosting access

National NCD strategic plan boosting access

| +0.6% | National; early gains in public facilities | Medium term (2-4 years) | |||

Cardiovascular-outcome data favouring SGLT-2s

Cardiovascular-outcome data favouring SGLT-2s

| +0.4% | National; private-sector early adoption | Medium term (2-4 years) | |||

Private-insurance expansion into lower-income tiers

Private-insurance expansion into lower-income tiers

| +0.3% | National; focus on emerging middle class | Long term (≥ 4 years) | |||

Fixed-dose generic combinations gaining traction

Fixed-dose generic combinations gaining traction

| +0.2% | National; public-sector emphasis | Short term (≤ 2 years) | |||

Rapid growth of e-pharmacy channels

Rapid growth of e-pharmacy channels

| +0.2% | National; urban concentration | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Prevalence Surge in Type-2 Diabetes

South Africa’s diabetes prevalence has climbed to 22%, while two-thirds of adults are pre-diabetic, creating a continually enlarging treatment pool in the South Africa oral anti-diabetic drug market. Urbanization, higher caloric intake, and obesity—which drives 87% of Type 2 diabetes cases—underpin the rise, and the International Diabetes Federation projects affected individuals to reach 7.5 million by 2045, a 78% jump that outpaces population growth [3]International Diabetes Federation, “IDF Diabetes Atlas 2024,” idf.org . The economic impact is equally stark: annual diabetes spending is forecast to escalate from USD 7.2 billion in 2021 to USD 10.4 billion in 2045, bolstering demand for cost-effective oral therapies over injectables. Undiagnosed cases still account for 45.4% of the total, so screening programs promise to bring millions of new patients into formal care pathways. Together these factors translate into sustained baseline demand that pharmaceutical firms must meet with scalable supply and competitive pricing in the South Africa oral anti-diabetic drug market.

National NCD Strategic Plan Boosting Access

The Department of Health’s cascade approach—screen 25 million citizens annually, link 60% to care, and achieve glycemic control in 50%—is institutionalizing proactive diabetes management nationwide. Embedded within Central Chronic Medication Dispensing and Distribution (CCMDD), the plan simplifies access to oral agents and standardizes prescribing protocols across provinces. Integration with pending National Health Insurance will push formulary alignment, intensifying generic substitution but stabilizing demand volumes for listed molecules. Early implementation already shows higher adherence in public clinics that leverage CCMDD medicine pick-up points, suggesting improved long-term outcomes. Manufacturers that secure essential-medicine listing and maintain uninterrupted supply are better positioned to capture incremental volumes in the South Africa oral anti-diabetic drug market.

Cardiovascular-Outcome Data Favouring SGLT-2s

Robust evidence shows SGLT-2 inhibitors cut major adverse cardiovascular events and heart-failure hospitalizations independent of baseline metformin use. Given that 35% of South African adults with diabetes also have hypertension, cardioprotective benefits resonate strongly with prescribers. Meta-analyses additionally highlight renal protection, with patients experiencing no estimated-glomerular-filtration decline at week 13 and significant improvement at week 64. Local guidelines now recommend these agents for high-risk patients, allowing premium pricing compared with sulfonylureas. As evidence accumulates, payers increasingly accept reimbursement for SGLT-2s, accelerating their penetration in the South Africa oral anti-diabetic drug market despite restrained overall growth.

Private-Insurance Expansion into Lower-Income Tiers

Medical schemes are broadening coverage to emerging middle-income groups and include diabetes within prescribed minimum benefits, creating clear reimbursement routes for oral therapies. For patients, direct annual diabetes costs of ZAR 2,452–2,486 remain significant, yet insurance diffusion offsets expenses and supports uptake of newer classes such as DPP-4 and SGLT-2 inhibitors. As benefit packages widen, pharmaceutical firms can segment offerings: branded innovative solutions for insured members and high-volume generics for public-sector tenders. This dual-channel strategy improves portfolio resilience in the South Africa oral anti-diabetic drug market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Pricing caps on essential medicines

Pricing caps on essential medicines

| -0.4% | National; public-sector emphasis | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-0.4%

|

Geographic Relevance

:

National; public-sector emphasis

|

Impact Timeline

:

Long term (≥ 4 years)

|

High out-of-pocket cost of novel agents

High out-of-pocket cost of novel agents

| -0.3% | National; private-sector concentration | Medium term (2-4 years) | |||

API import-linked supply-chain fragilities

API import-linked supply-chain fragilities

| -0.2% | National; manufacturing-sector impact | Short term (≤ 2 years) | |||

Low long-term medication adherence

Low long-term medication adherence

| -0.3% | National; rural and low-income focus | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Pricing Caps on Essential Medicines

South Africa’s single-exit price regime obliges suppliers to sell all customers at one state-regulated price, limiting margin potential for legacy molecules like metformin. Periodic price reviews rarely keep pace with inflation, prompting continued deflation in real terms. Essential-medicine designation secures high volume but compresses profitability, challenging companies to streamline supply chains and localize production where feasible. Regulatory convergence with European standards further lengthens approval timelines and raises compliance costs, intensifying pressure on smaller firms. These mechanisms collectively restrain topline expansion in the South Africa oral anti-diabetic drug market.

High Out-Of-Pocket Cost of Novel Agents

First-line GLP-1 receptor agonists can cost ZAR 2,700–4,000 monthly (USD 150–220), a prohibitive payment for the uninsured majority. Limited scheme reimbursement for weight-management indications compounds barriers, leaving price-sensitive patients reliant on older oral agents. Affordability gaps skew treatment patterns, perpetuating clinical inertia and underutilization of innovative classes. Until competitive domestic manufacturing or broader reimbursement emerges, uptake of premium molecules will remain confined to affluent urban households, curbing the aggregate value trajectory of the South Africa oral anti-diabetic drug market.

Segment Analysis

By Drug Class: SGLT-2 Inhibitors Drive Innovation Despite Biguanide Dominance

Biguanides delivered 37.65% of 2025 sales, anchoring the South Africa oral anti-diabetic drug market through metformin’s proven efficacy, safety, and inclusion on the public essential-medicine list. The segment’s volume advantage keeps manufacturing lines running at scale and underpins predictable tender forecasts, ensuring that biguanides will continue to form the therapeutic backbone through 2031. Meanwhile, the South Africa oral anti-diabetic drug market size for SGLT-2 inhibitors is projected to advance at a 3.06% CAGR, catalyzed by multidisciplinary guidelines endorsing cardioprotection and renal-sparing profiles.

Patent cliffs in DPP-4 inhibitors and rising physician familiarity with fixed-dose combinations also shuffle competitive positions. Multinationals prioritize SGLT-2 lifecycle management, while local firms bank on imminent sitagliptin-metformin generic opportunities. This duality intensifies price competition, yet SGLT-2 value propositions around hospitalization reduction maintain premium space. Consequently, differentiated evidence packages and robust pharmacovigilance programs will dictate future South Africa oral anti-diabetic drug market share movements.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Geriatric Segment Emerges as Growth Driver

Adults retained 65.80% of revenue in 2025, reflecting prevalent lifestyle-related risk factors among working-age cohorts. However, geriatric patients, now the fastest-expanding bracket with a 3.03% CAGR, command growing attention because longer disease duration amplifies complication risks and necessitates combination therapy escalation. The South Africa oral anti-diabetic drug market size attributed to seniors will rise as life expectancy improves and retirement populations swell.

Clinical focus in older adults centers on hypoglycemia mitigation and renal dosing considerations, giving SGLT-2 and DPP-4 inhibitors an edge over sulfonylureas. Community-health-worker interventions tailored to polypharmacy management enhance adherence, underpinning sustained demand. Pediatric incidence remains low, but mounting childhood obesity could open a future niche, making early-obesity screening pivotal to long-term South Africa oral anti-diabetic drug market health.

By Diabetes Type: Type 2 Dominance Reflects Epidemiological Reality

Type 2 diabetes captured 93.10% of 2025 revenues and is forecast to expand at 2.97% CAGR through 2031, confirming lifestyle disorders as the central performance driver of the South Africa oral anti-diabetic drug market. Aggressive screening under the NCD cascade will uncover undiagnosed adults, driving earlier pharmacologic intervention and larger treatment cohorts.

Type 1 diabetes, though a small share, relies primarily on insulin, yet adjunctive metformin use for insulin resistance introduces limited crossover volume. Research into oral immunomodulation therapies could temper insulin doses, but commercialization remains distant. In the medium term, product development and marketing resources will direct toward Type 2 differentiation, safeguarding dominant South Africa oral anti-diabetic drug market share for oral modalities.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Pharmacies Challenge Hospital Dominance

Hospital pharmacies generated 68.90% of 2025 turnover, leveraging state purchasing power and CCMDD distribution nodes that foster predictable monthly volumes for essential oral agents. Still, the South Africa oral anti-diabetic drug market size managed via online platforms is mounting quickly at a 3.15% CAGR thanks to e-commerce penetration and regulatory clarity from SAHPRA regarding legal internet pharmacy operations.

Digital ordering appeals to chronic-care patients needing routine refills, with registered pharmacists verifying prescriptions before dispatch. Payment gateways partner with medical schemes, integrating reimbursements and widening customer bases. As logistics networks improve rural reach, click-and-collect models will reduce travel burden and dilute traditional retail advantage, progressively eroding hospital share in the South Africa oral anti-diabetic drug market.

Geography Analysis

Provincial heterogeneity shapes demand patterns across Gauteng, Western Cape, and KwaZulu-Natal, the three provinces housing most private medical scheme members and specialist endocrinology services. Gauteng accounts for the largest treatment volumes, buoyed by Johannesburg’s dense urban population and numerous tertiary hospitals with dedicated diabetic clinics. Western Cape achieves the highest adherence rates, assisted by well-resourced community health centers that leverage CCMDD pick-up points and digital app reminders, supporting consistent consumption in the South Africa oral anti-diabetic drug market.

KwaZulu-Natal shows elevated prevalence but slightly lower medicine uptake because rural districts endure transportation barriers. Here, mobile outreach units stock oral therapies and collect finger-stick glucose data, feeding analytics that refine regional forecasting. Limpopo and Eastern Cape confront the widest physician gaps; NGOs provide point-of-care HbA1c testing, uncovering latent demand ahead of National Health Insurance scale-up.

Cross-border trade into Botswana, Namibia, and Mozambique remains modest but offers upside for South African manufacturers with regional logistics hubs. SAHPRA’s vision for Southern African Development Community regulatory harmonization could streamline registration, unlocking export growth that complements domestic sales. Until then, the South Africa oral anti-diabetic drug market remains principally inward-focused, yet provinces that build telehealth infrastructure fastest will capture a disproportionate share of future value.

Competitive Landscape

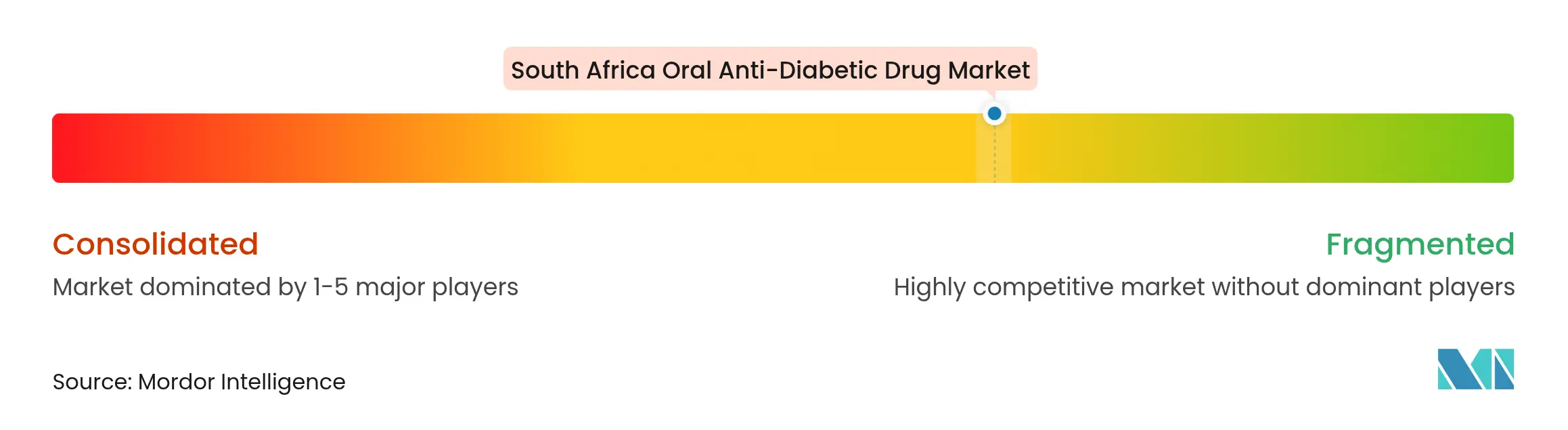

Market Concentration

The South Africa oral anti-diabetic drug market features moderate concentration: Aspen Pharmacare, Adcock Ingram, and Cipla Medpro dominate generics, while Sanofi, AstraZeneca, and Novo Nordisk steer innovation segments. Aspen’s forthcoming GLP-1 capacity, slated for 2026, signals its ambition to capture high-value therapy areas and echoes national industrial-policy aims for local biologic production. Meanwhile, Sanofi enhances physician education on cardiometabolic synergy, and AstraZeneca deepens post-marketing surveillance of dapagliflozin, reinforcing brand confidence among specialists.

Supply-chain robustness proves decisive. Novo Nordisk’s 2024 insulin-pen shortage prompted public appeals from Médecins Sans Frontières and highlighted vulnerabilities inherent in concentrated import dependency. In response, competitors upgraded buffer inventories and considered dual-sourcing APIs to safeguard continuity. Technology adoption further separates players: robotic dispensing pilots at Adcock Ingram’s Johannesburg warehouse cut error rates and accelerate public-tender order fulfillment. Marketing moves now extend to telemedicine partnerships, allowing firms to embed drug information within remote-consult platforms, thereby influencing prescribing in the South Africa oral anti-diabetic drug market.

Upcoming patent expiries, most notably the sitagliptin-metformin combination in 2029, will intensify competition. Local licensees prepare dossier submissions to SAHPRA to ensure day-one launch readiness, betting on swift substitution. Branded originators counter with patient-support programs and real-world evidence of long-term outcome gains. Success will balance price discounts, pharmacoeconomic data, and transparent supply performance.

South Africa Oral Anti-Diabetic Drug Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Aspen Pharmacare confirmed a strategic pivot toward GLP-1 production with plans for commercial launch in 2026 to serve emerging markets, including South Africa.

- February 2025: The U.S. FDA issued a warning letter to Aspen Pharmacare for CGMP breaches at its Port Elizabeth facility, suspending exports to the United States pending remediation.

- January 2025: The Medicines Information Centre announced restored supply of high-dose Ozempic, easing prior shortages in private pharmacies.

Table of Contents for South Africa Oral Anti-Diabetic Drug Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Prevalence Surge in Type-2 Diabetes

- 4.2.2National NCD Strategic Plan Boosting Access

- 4.2.3Cardiovascular-Outcome Data Favouring SGLT-2s

- 4.2.4Private-Insurance Expansion into Lower-Income Tiers

- 4.2.5Fixed-Dose Generic Combinations Gaining Traction

- 4.2.6Rapid Growth Of E-Pharmacy Channels

- 4.3Market Restraints

- 4.3.1Pricing Caps on Essential Medicines

- 4.3.2High Out-Of-Pocket Cost of Novel Agents

- 4.3.3API Import-Linked Supply-Chain Fragilities

- 4.3.4Low Long-Term Medication Adherence

- 4.4Regulatory Landscape

- 4.5Porters Five Forces Analysis

- 4.5.1Bargaining Power of Suppliers

- 4.5.2Bargaining Power of Consumers

- 4.5.3Threat of New Entrants

- 4.5.4Threat of Substitute Products & Services

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Drug Class

- 5.1.1Biguanides

- 5.1.2Sulfonylureas

- 5.1.3Meglitinides

- 5.1.4Thiazolidinediones

- 5.1.5Alpha-Glucosidase Inhibitors

- 5.1.6DPP-4 Inhibitors

- 5.1.7SGLT-2 Inhibitors

- 5.1.8Others

- 5.2By Age Group

- 5.2.1Adults

- 5.2.2Pediatric

- 5.2.3Geriatric

- 5.3By Diabetes Type

- 5.3.1Type 1 Diabetes

- 5.3.2Type 2 Diabetes

- 5.4By Distribution Channel

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies

- 5.4.3Online Pharmacies

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Aspen Pharmacare

- 6.3.2Adcock Ingram

- 6.3.3Sanofi

- 6.3.4Cipla Medpro

- 6.3.5AstraZeneca

- 6.3.6Merck & Co.

- 6.3.7Boehringer Ingelheim

- 6.3.8Takeda

- 6.3.9Novo Nordisk

- 6.3.10Eli Lilly

- 6.3.11Bristol Myers Squibb

- 6.3.12Johnson and Johnson

- 6.3.13Astellas Pharma

- 6.3.14Pfizer

- 6.3.15Novartis

- 6.3.16Sun Pharma

- 6.3.17Mylan Viatris

- 6.3.18Lupin

- 6.3.19Dr Reddys Laboratories

- 6.3.20Torrent Pharma

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

South Africa Oral Anti-Diabetic Drug Market Report Scope

Oral antihyperglycemic agents lower glucose levels in the blood. They are commonly used in the treatment of diabetes mellitus. The South Afric oral anti-diabetic drug market is set to witness a cagr of more than 2% during the forecast period. The South Africa oral anti-diabetic drug market is segmented into drugs. The report offers the market size in value terms in USD and Volume in terms of Units for all the abovementioned segments.