Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

The United States Fitness Rings Market Report is Segmented by Product Type (Basic Fitness Rings and Smart Fitness Rings), Distribution Channel (Online E-Commerce, and More), End-User (General Consumers, Professional Athletes, and More), Application (Activity and Fitness Tracking, Sleep and Recovery Monitoring, and More), and Sensor Type (Heart-Rate and HRV, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

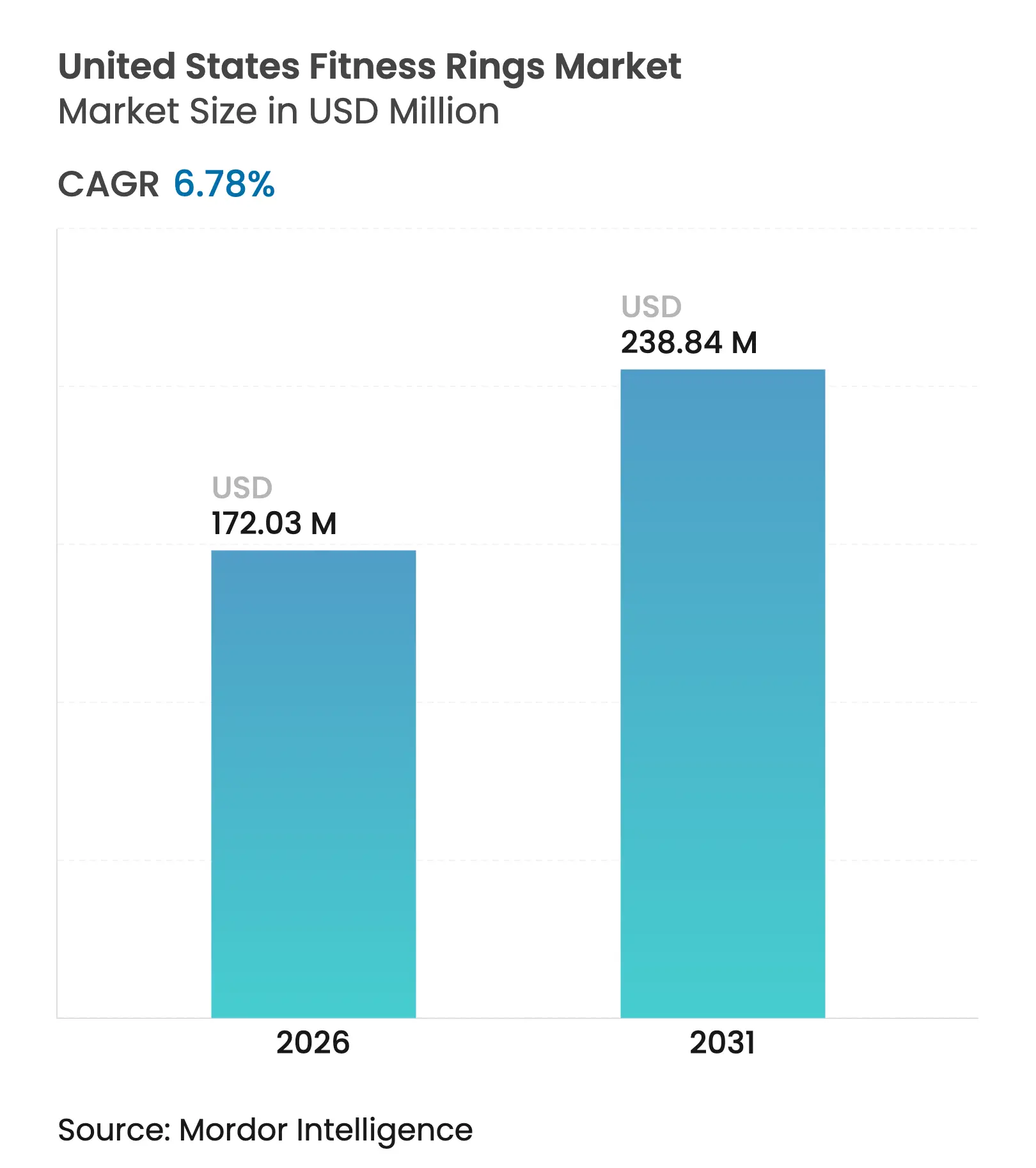

| Market Size (2026) | USD 172.03 Million |

| Market Size (2031) | USD 238.84 Million |

| Growth Rate (2026 - 2031) | 6.78 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The United States fitness rings market size in 2026 is estimated at USD 172.03 million, growing from 2025 value of USD 161.11 million with 2031 projections showing USD 238.84 million, growing at 6.78% CAGR over 2026-2031. Growing insurer and employer sponsorships, Remote Patient Monitoring (RPM) reimbursement, and sensor miniaturization are positioning the United States fitness rings market as an unobtrusive alternative to wrist-worn wearables. Clinical validation studies, FDA 510(k) clearances targeting sleep apnea and pulse oximetry, as well as partnerships that integrate glucose data, are expanding the medical use case profile. Hardware differentiation is narrowing, so proprietary algorithms, subscription platforms, and third-party health-data integrations are becoming decisive competitive levers. Supply-chain easing for sub-5 mm microcontroller units is alleviating prior component shortages, yet state-level privacy laws and short replacement cycles continue to present headwinds. Device makers are responding by baking consent workflows into onboarding, extending trade-in incentives, and marketing recycling programs to environmentally conscious buyers.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expanding adoption of wearable wellness technologies Expanding adoption of wearable wellness technologies | +1.8% | National, with higher penetration in West and Northeast urban centers | Medium term (2-4 years) | (~) % Impact on CAGR Forecast :+1.8% | Geographic Relevance :National, with higher penetration in West and Northeast urban centers | Impact Timeline :Medium term (2-4 years) |

Rising health insurance incentives for biometrics-based monitoring Rising health insurance incentives for biometrics-based monitoring | +1.5% | National, accelerated by Medicare Advantage programs in South and Midwest | Short term (≤ 2 years) | |||

Integration of fitness rings into employer wellness benefits Integration of fitness rings into employer wellness benefits | +1.2% | National, concentrated in corporate hubs (West Coast tech, Northeast finance) | Medium term (2-4 years) | |||

Miniaturisation of low-power biometric sensors Miniaturisation of low-power biometric sensors | +1.0% | Global supply chains, design centers in West Coast and Northeast | Long term (≥ 4 years) | |||

FDA fast-track interest in ring-based sleep apnea screening FDA fast-track interest in ring-based sleep apnea screening | +0.9% | National, regulatory pathway centered on FDA headquarters (Maryland) | Medium term (2-4 years) | |||

Growth of closed-loop metabolic coaching ecosystems Growth of closed-loop metabolic coaching ecosystems | +0.8% | National, early adoption in health-conscious West and Northeast markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Expanding Adoption of Wearable Wellness Technologies

Insurers now subsidize hardware costs, with programs such as Discovery Vitality offering members up to 25% premium discounts when activity and sleep targets are verified through approved devices.[1]Discovery Limited, “Vitality Rewards Premium Discounts,” discovery.co.za In 2024, Essence Healthcare announced that it would provide free Oura Rings to Medicare Advantage members starting in 2025, marking the first large-scale insurer-funded ring deployment in the United States. RPM CPT codes 99453, 99454, 99457, and 99458 reimburse USD 19–64 per patient per month for connected-device data, turning ring-generated metrics into billable services.[2]Centers for Medicare & Medicaid Services, “Remote Patient Monitoring FAQ,” cms.gov Employer wellness programs follow suit, subsidizing devices when employees consent to share de-identified biometrics for premium negotiations. This convergence of insurer incentives, RPM billing, and employer cost containment is accelerating the penetration of the United States fitness ring market among previously price-sensitive demographics.

Rising Health-Insurance Incentives for Biometrics-Based Monitoring

Medicare Advantage plans, which cover 31 million Americans, leverage ring-sourced data to improve Star Ratings and lower claims costs. The 2024 addition of Remote Therapeutic Monitoring CPT codes 98975-98981 covers non-physiologic data points, such as medication adherence, broadening the reimbursement scope. Private insurers integrate rings into diabetes, hypertension, and sleep disorder programs, aiming to avert hospitalizations. The Oura–Essence tie-up exemplifies alignment of patient incentives (free hardware), provider revenue (RPM codes), and payer savings (fewer acute claims). State biometric and privacy statutes impose granular consent mandates, but compliant insurers view data stewardship as a table-stakes requirement rather than a deterrent.

Integration of Fitness Rings into Employer Wellness Benefits

Corporations subsidize rings to manage group-insurance premiums, with Silicon Valley and Wall Street firms offering USD 200–300 hardware credits. Oura for Business provides comprehensive readiness dashboards that correlate sleep deficits with absenteeism, while protecting individual data. EEOC guidance issued in December 2024 clarifies that wellness programs must be voluntary; however, incentives remain permissible as long as non-participants are not penalized. Integrations with Virgin Pulse and Wellable reduce deployment friction, propelling corporate adoption within high-stress industries where recovery metrics correlate to performance and safety.

Miniaturization of Low-Power Biometric Sensors

Bosch Sensortec’s BHI385 motion sensor consumes as little as 38 µA during activity tracking and incorporates on-device AI for fall detection and gesture control. Advances in PPG LED arrays enable accurate heart rate and SpO₂ readings from finger arteries, improving data quality for individuals with darker skin tones. Thermistor-based temperature sensors achieve a ±0.1 °C accuracy, enabling the tracking of menstrual cycles and early fevers. Ultra-low-power MCUs from Nordic Semiconductor integrate BLE radios and DSPs into 3 mm packages, extending ring battery life to 7 days. Nature Electronics reported hybrid multimodal chips that integrate bioimpedance and ECG measurements from a single contact point, foreshadowing the potential for future metabolic and stress biomarkers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Data-privacy litigation risk for continuous biometric capture Data-privacy litigation risk for continuous biometric capture | -1.3% | National, concentrated in Illinois (BIPA) and California (CCPA/CPRA) | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast :-1.3% | Geographic Relevance :National, concentrated in Illinois (BIPA) and California (CCPA/CPRA) | Impact Timeline :Short term (≤ 2 years) |

Short product replacement cycles driving e-waste concerns Short product replacement cycles driving e-waste concerns | -0.8% | National, with regulatory pressure emerging in West Coast states | Medium term (2-4 years) | |||

Semiconductor supply volatility for ultra-small MCU packages Semiconductor supply volatility for ultra-small MCU packages | -0.6% | Global supply chains, design dependencies in Asia and Europe | Short term (≤ 2 years) | |||

Niche perception versus smart-watch multifunctionality Niche perception versus smart-watch multifunctionality | -0.9% | National, strongest in demographics preferring multifunctional devices | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Data-Privacy Litigation Risk for Continuous Biometric Capture

Illinois Biometric Information Privacy Act exposes violators to USD 1,000–5,000 statutory damages per breach, and class actions have already surpassed USD 100 million in settlements.[3]Illinois General Assembly, “Biometric Information Privacy Act,” ilga.gov California Consumer Privacy Act and its successor, CPRA, require opt-out and deletion rights, raising compliance costs. EEOC guidance warns that wearables may violate ADA or GINA if linked to employment decisions, chilling aggressive employer mandates. Manufacturers respond by embedding consent flows, anonymizing datasets, and purchasing cyber liability insurance, but litigation risk remains a drag on the rapid enterprise rollout.

Short Product Replacement Cycles Driving E-Waste Concerns

United Nations data show that small electronics are the fastest-growing e-waste category, yet fewer than 20% of them enter formal recycling streams. Fitness rings, sealed around non-replaceable micro-batteries, complicate disassembly and material recovery. EU battery regulations requiring replaceable cells by 2027 may raise design costs for global SKUs. Right-to-Repair activists push for modular architectures, but miniaturization limits physical space. Take-back incentives remain underutilized, putting sustainability messaging at odds with rapid innovation cycles in the United States fitness rings market.

By Product Type: Smart Rings Cement Leadership

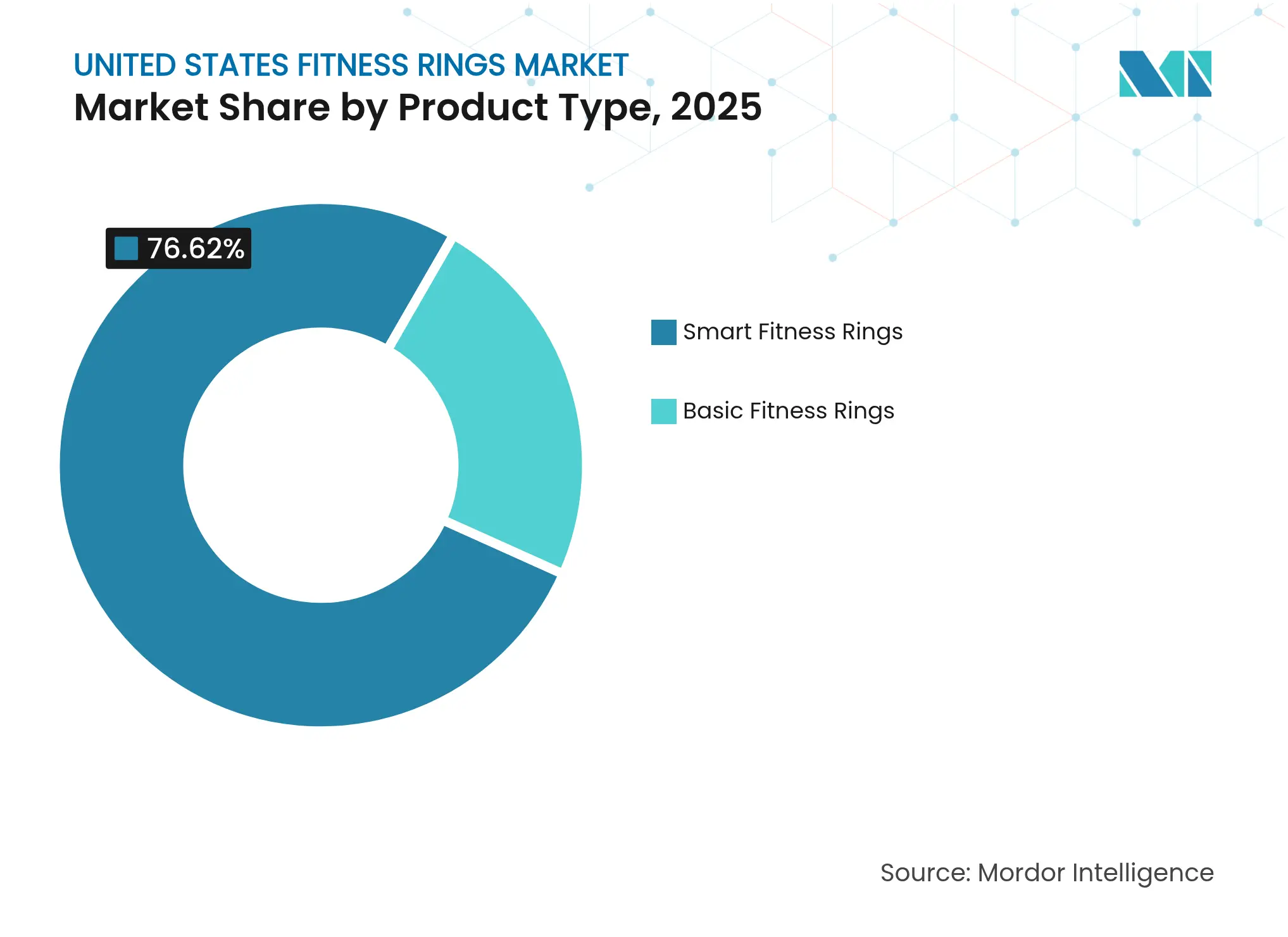

Smart Fitness Rings accounted for 76.62% of 2025 revenue and are projected to rise at an 8.12% CAGR to 2031, underscoring their role as the revenue engine of the United States fitness rings market. Oura’s third-generation model, priced at USD 299 plus a USD 5.99 monthly subscription, combines 5-day battery life with menstrual-cycle and recovery analytics, locking users into recurring services. Samsung’s July 2024 Galaxy Ring counters with USD 399.99 hardware and no fees, leveraging Galaxy Health integration to appeal to existing Samsung owners. Basic Fitness Rings are losing ground as feature-rich devices push prices below USD 300, and ecosystem lock-in deters downgrades. The Dexcom–Oura collaboration, integrating glucose data, illustrates how smart rings expand beyond activity tracking into metabolic coaching, a frontier that basic rings cannot reach. Regulatory divergence is also widening: Movano’s FDA-bound Evie Ring seeks medical-device status, unlocking reimbursement channels that wellness-only rings cannot access.

Smart rings, therefore, serve both lifestyle and medical niches, tightening their grip on the United States fitness rings market. As component costs fall and sensor fusion improves, the perceived gap between basic and smart models will continue to widen, consolidating demand around the latter. The United States fitness ring market size attributable to smart rings is projected to reach USD 197.2 million by 2031, sustaining its dominance while raising entry barriers for simpler devices.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Clinics Accelerate While Online Remains Dominant

Online storefronts maintained a 63.12% share in 2025, confirming direct-to-consumer as the default strategy for new entrants. However, RPM reimbursement has catalyzed clinic-based prescribing, propelling Healthcare Provider Clinics to a forecast 9.36% CAGR, the fastest within the United States fitness rings market. Movano’s Evie Ring, aiming for pulse-ox clearance, will enter pulmonology and cardiology offices where physicians can bill RPM codes, illustrating the channel’s momentum. Big-box electronics retailers play a marginal role as consumers favor web research and free shipping, while sporting-goods chains focus on footwear and apparel.

Clinics provide credibility and embedded follow-up, allowing fitness rings to graduate from wellness gadgets to reimbursable medical tools. Consequently, the United States fitness rings market size generated through provider clinics is projected to reach USD 36.86 million by 2031, nudging market leaders to staff healthcare sales teams and secure HIPAA-ready cloud architectures.

By End-User: Corporate Wellness Shows Fastest Uptake

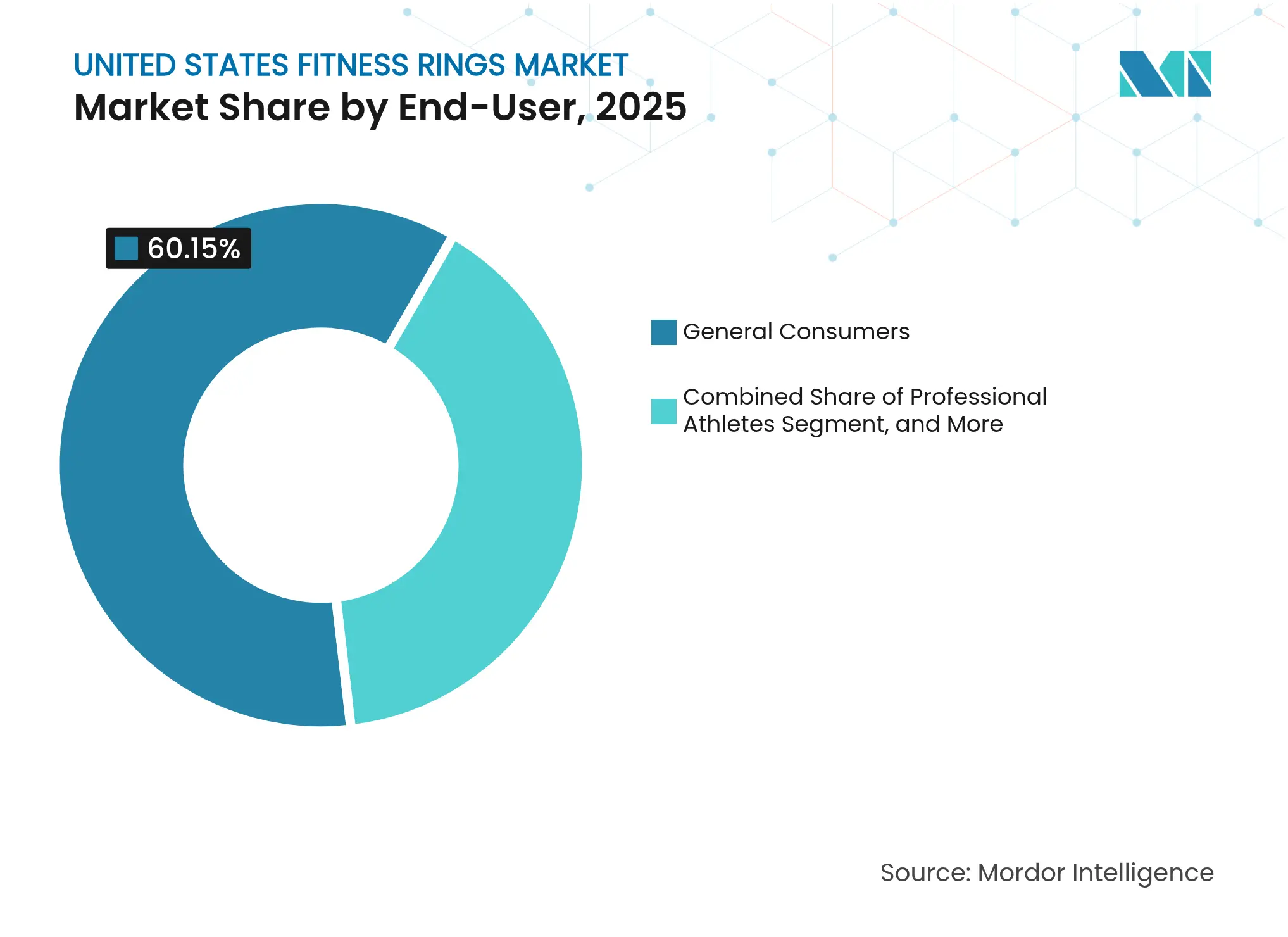

General Consumers accounted for 60.15% of the 2025 volume, yet Corporate Wellness Subscribers are expected to rise at a 9.44% CAGR through 2031, reflecting employers’ desire to control medical premiums. HR departments deploy rings to monitor aggregate readiness and sleep scores, offering hardware subsidies in exchange for anonymized metrics. EEOC mandates voluntary participation, but attractive incentives keep uptake high. Professional Athletes remain a niche but influential group of adopters; National Basketball Association teams rely on overnight HRV to calibrate their training loads. Research institutions integrate rings into decentralized clinical trials, valuing continuous data streams that occur outside of lab settings.

Corporate uptake broadens brand exposure and builds longitudinal datasets across diverse demographics, enhancing algorithm robustness. As enterprises negotiate bulk contracts, the United States fitness rings market share, currently commanded by corporate buyers, is expected to reach 25.60% by 2031, reshaping pricing and product roadmap priorities.

Note: Segment shares of all individual segments available upon report purchase

By Application: Metabolic Health Steals Spotlight

Activity tracking secured 49.31% of revenue in 2025; however, Metabolic Health Management is forecast to outpace all other applications at a 9.47% CAGR, unlocking premium software tiers that increase the average revenue per user. The November 2024 Dexcom investment values Oura above USD 5 billion, merging continuous glucose data with sleep and activity insights to create closed-loop coaching unseen in traditional wearables. Ultrahuman’s Air ring, paired with Abbott Libre sensors, similarly combines ring metrics and glucose readings to inform nutritional choices. Stress and mental wellness rely on HRV analytics, yet lack robust clinical validation, tempering growth prospects.

By tying actionable metabolic insights to gamified targets, Rings leapfrog step-count commoditization, anchoring themselves at the core of preventative-health routines. Consequently, the United States fitness rings market size tied to metabolic-health software is projected to quadruple between 2024 and 2030, even as hardware revenues grow more modestly.

By Sensor Type: Multi-Modal Fusion Leads Next Phase

The Heart-rate and HRV modules held a 47.62% share in 2025, underscoring their status as table-stakes sensors. Yet Multi-modal Sensor Fusion will expand at a 9.58% CAGR, driven by BHI385 AI-on-sensor chips and Nature Electronics’ hybrid stacks that fold ECG and bioimpedance into a single die. Skin-temperature sensing enables women’s health features and early illness flags, while SpO₂ remains central to sleep-apnea screening. By correlating accelerometry, HRV, SpO₂, and temperature in a single algorithm, fusion architectures deliver insights superior to those of single-sensor devices, thereby increasing switching costs for users.

As firmware updates unlock new composite metrics without requiring hardware refreshes, sensor-fusion leadership is likely to opt for premium-tier adoption. Market leaders that aggregate diverse data streams will capture outsized value, further consolidating the United States fitness rings market around algorithm-rich ecosystems.

California and broader West Coast markets lead demand thanks to high disposable incomes, technology-centric workforces, and an early-adopter culture. Silicon Valley hosts design centers for several ring brands and serves as a proving ground for RPM pilots with integrated delivery networks. The Northeast, anchored by New York’s finance sector and Boston’s med-tech cluster, follows closely, leveraging corporate wellness budgets and academic research grants. Medicare Advantage penetration in Southern states drives insurer-funded deployments, such as the Essence Oura giveaway, boosting uptake among seniors who previously bypassed wearables due to cost. The Midwest’s slower adoption reflects lower urban density and fewer clinical RPM programs, although logistics and manufacturing employers in the region are starting to pilot ring-based recovery monitoring.

State privacy laws create regional compliance friction. Illinois’ BIPA drives conservative deployment strategies in Chicago-area offices, while California’s CCPA/CPRA adds data-processing costs for nationwide brands. Conversely, uniform federal RPM reimbursement levels the playing field for clinic channels, enabling rural practices in the South and Midwest to prescribe rings and bill CMS at the same rate as coastal peers. Telehealth expansion further erodes geographic barriers, allowing patients to synchronize their data with specialists hundreds of miles away. Overall, the West is expected to retain its leadership position with a 31.65% share of the United States fitness rings market by 2031, while the South is projected to post the fastest CAGR at 8.12%, driven by Medicare Advantage dynamics. Regional strategies, therefore, hinge on tailoring distribution to direct consumers on the coasts, through insurer and employer channels inland, and navigating a patchwork of privacy statutes that influence marketing and user-consent workflows.

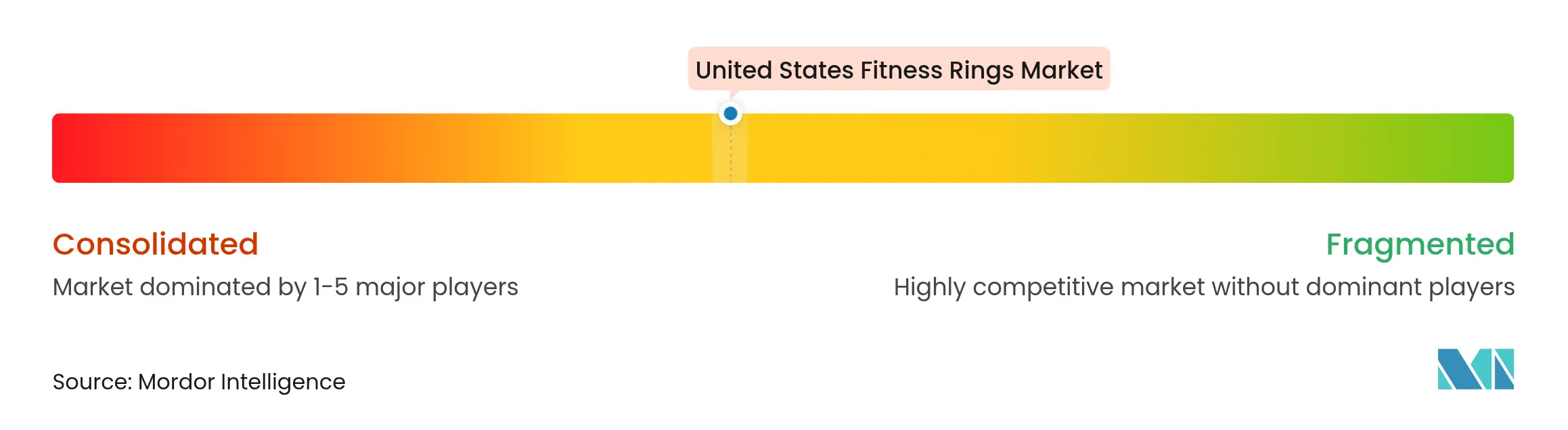

Market Concentration

Oura Health remains the category’s best-known brand, pairing a recurring-revenue subscription with a clinically validated sensor stack. Samsung’s Galaxy Ring launch in July 2024 injected a heavyweight rival that leverages the broader Galaxy ecosystem and a subscription-free model, challenging Oura’s ARPU economics. Patent litigation between the two firms underscores the scarcity of ring-form-factor IP and foreshadows a defensive patent race. Emerging challengers are staking differentiated claims: Ultrahuman integrates continuous glucose monitoring, RingConn undercuts pricing to below USD 300, and Movano is pursuing FDA clearances specific to women. Apple’s September 2024 FDA nod for sleep-apnea notifications on Watch fuels speculation about a ring product, backed by its expanding patent portfolio.

Strategic moves favor ecosystem lock-in. Dexcom’s USD 75 million investment in Oura hard-wires glucose telemetry into readiness scores, while Samsung bundles ring metrics into Galaxy Health without recurring fees. Movano’s USD 10 million capital raise will fund clinical trials, indicating a reimbursement-led go-to-market strategy. Compliance competencies, such as SOC 2, HITRUST, and HIPAA, are becoming prerequisites for B2B deals, advantaging well-capitalized incumbents.

The competitive field is likely to bifurcate. One tier will focus on consumer wellness, competing on brand aesthetics and lifestyle marketing; another will pursue medical validation, targeting CPT-billed care pathways and payer partnerships. Algorithmic differentiation, not sensor SKU choice, will decide winners, as raw data becomes commoditized and insights define user stickiness in the United States fitness rings market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The US fitness rings market tracks the revenue incurred through the sale of smart fitness tracker rings offered by market vendors (directly, through partners, and through e-commerce platforms) to consumers in China.

The US fitness rings market is segmented by product type (basic fitness rings, smart fitness rings). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

Mapping Real Estate Opportunities in Bali

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.