Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.76 Billion |

| Market Size (2026) | USD 6.02 Billion |

| Market Size (2031) | USD 7.23 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore 3PL Market Analysis by Mordor Intelligence

The Singapore 3PL Market size was valued at USD 5.76 billion in 2025 and is estimated to grow from USD 6.02 billion in 2026 to reach USD 7.23 billion by 2031, at a CAGR of 3.74% during the forecast period (2026-2031).

The Singapore 3PL market demonstrates strong structural maturity, supported by the country’s strategic position as a regional logistics gateway in Asia-Pacific. The presence of world-class trade infrastructure, including the Port of Singapore and Changi Airport, enables efficient multimodal logistics operations and strengthens the country’s role as a regional distribution hub. Market growth is primarily driven by increasing demand for outsourced logistics services, as manufacturers and retailers seek to optimize supply chains, reduce operational complexity, and enhance service flexibility. In addition, the expansion of e-commerce and high-value industries such as electronics, pharmaceuticals, and precision manufacturing is accelerating the adoption of value-added 3PL services, including contract logistics, inventory management, and integrated supply chain solutions. However, high land costs and space constraints in Singapore continue to influence warehouse development strategies, prompting logistics providers to invest in automation, vertical warehousing, and technology-enabled supply chain optimization.

Key Report Takeaways

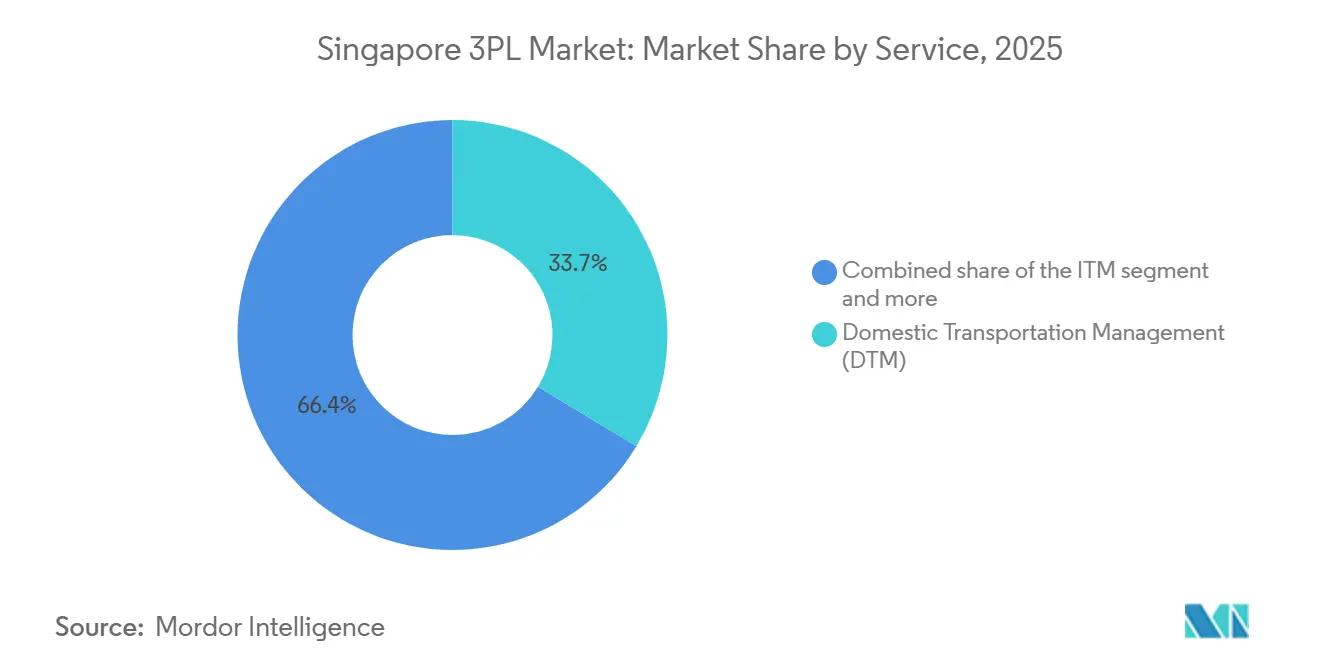

- By service, Domestic Transportation Management led the Singapore 3PL market with 33.65% share in 2025, while Value-Added Warehousing & Distribution is projected to expand at a 4.80% CAGR through 2031.

- By end user, Technology & Electronics accounted for a 33.16% share in 2025, while the e-commerce segment is set to grow at a 5.74% CAGR through 2031.

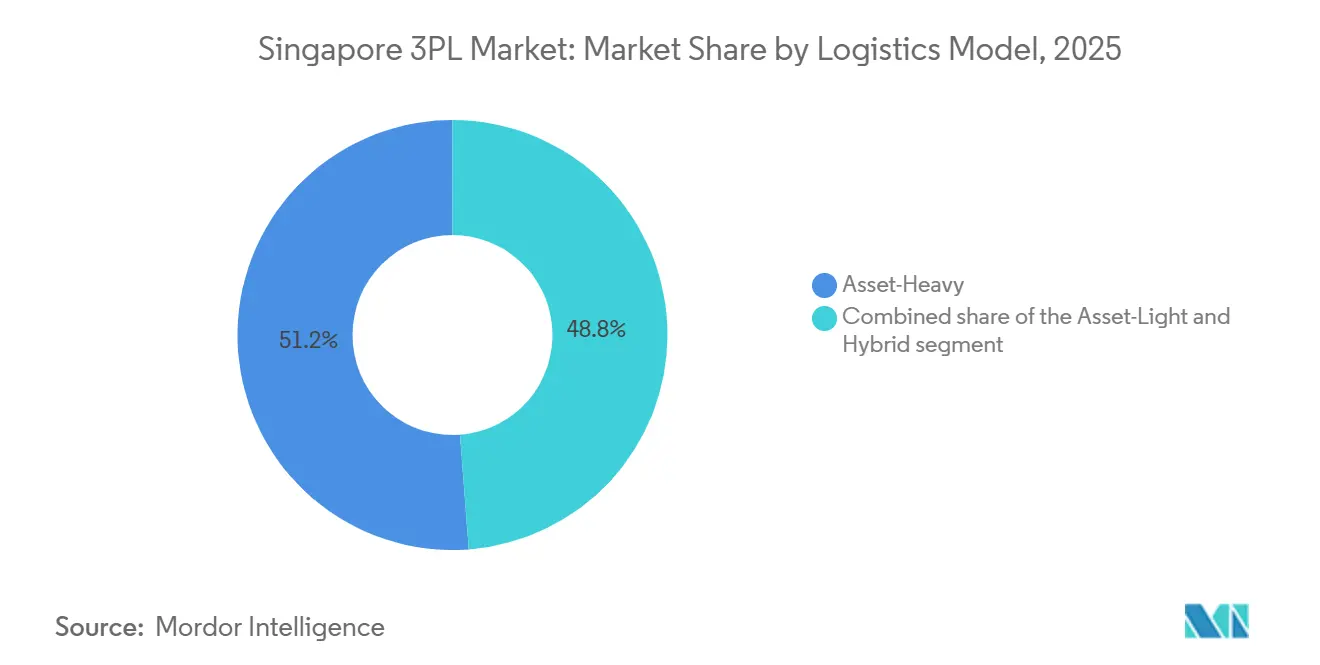

- By logistics model, asset-heavy models captured 51.21% of the Singapore 3PL market size in 2025, while hybrid models are forecast to record the fastest growth at a 5.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Cross-Border E-Commerce and Regional Fulfilment Demand | +0.9% | ASEAN core, spill-over to APAC | Medium term (2-4 years) |

| Expansion of ASEAN Trade and Supply Chain Integration | +0.6% | Singapore-Malaysia-Indonesia triangle, broader ASEAN | Long term (≥ 4 years) |

| Digital Logistics Platforms with Real-Time Visibility & Automation | +0.7% | Global, with Singapore as APAC pilot hub | Short term (≤ 2 years) |

| Deployment of Smart Warehousing and Robotics Solutions | +0.8% | Singapore national, selective ASEAN cities | Medium term (2-4 years) |

| Government Investment in Changi Logistics & Tuas Port Connectivity | +0.5% | Singapore, regional transshipment lanes | Long term (≥ 4 years) |

| Rise in Cold Chain & Temperature-Controlled Logistics Requirements | +1.0% | Singapore, high-value corridors to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Cross-Border E-Commerce and Regional Fulfilment Demand

Cross-border programs are scaling faster fulfillment links between Singapore and major consumption centers across Asia and North America. FedEx’s first direct Boeing 777F service from Singapore to Anchorage launched in April 2025, trimming 10-14 days from selected routings and enabling Saturday pick-ups in Singapore, Malaysia, and Thailand to arrive in the continental U.S. by Monday, strengthening service propositions for time-sensitive parcels and SMEs. Ninja Van extended international coverage to 41 additional destinations, giving local brands new cost-to-serve options and packaging support that improve repeat purchase performance in adjacent markets. Singapore’s proximity to key ASEAN markets and its airport-to-sea connectivity keep two-to-five-day delivery windows achievable for many cross-border SKUs that can be staged or fast-replenished from Singapore. Express air and regional linehaul providers use route optimization, weekend uplift, and consolidated drop-off networks to compress dwell time and lower end-to-end variance for exporters. These enhancements pull more cross-border volumes into Singapore for first sort and hub injection, reinforcing the Singapore 3PL market as a staging node for omnichannel growth across ASEAN.

Expansion of ASEAN Trade and Supply Chain Integration

Trade and investment flows across ASEAN continue to support cross-border warehousing, cross-dock, and multi-country consolidation models anchored in Singapore. The ASEAN Business Advisory Council’s Unique Business Identification Number program, moving into implementation, aims to enable “verify once, trust everywhere” identity checks that are projected to unlock USD 80-240 billion in incremental intra-ASEAN commerce and reduce friction costs across customs and compliance. Multinational shippers treat Singapore as the orchestrator for high-value, highly regulated cargo while distributing production footprints across Malaysia, Vietnam, Thailand, and Indonesia. Kerry Logistics Network reported strong performance in the rest of Asia, supported by customers 'Southeast Asian expansion plans and warehouse footprints linking Singapore with Vietnam and Malaysia. Harmonized processes and identity standards are expected to reduce documentation handoffs and enable faster border clearance, supporting just-in-time replenishment across regional e-commerce and high-tech flows. As this integration deepens, the Singapore third-party logistics market gains more opportunities in control tower services, bonded inventory pooling, and cross-border returns programs.[2]Source: ASEAN Business Advisory Council, “ASEAN’s Next Trade Breakthrough: Accelerating Cross-Border Growth Through Interoperable Identity,” ASEAN-BAC, asean-bac.org

Digital Logistics Platforms with Real-Time Visibility & Automation

Singapore has accelerated the digitization of port, vessel, and cargo documentation through platforms that aggregate data and cut manual entries across multiple forms. MPA’s digitalPORT@SG integrates submissions into a single portal and supports just-in-time vessel scheduling to reduce anchorage wait times and bunker consumption, thereby lowering demurrage risk for shippers and stabilizing planning for 3PLs[1]Source: Maritime and Port Authority of Singapore, “Port of the Future,” Maritime and Port Authority of Singapore, mpa.gov.sg. Electronic Bunker Delivery Notes rolled out to digitize the world’s largest bunkering hub, improving transaction accuracy and traceability across fuel suppliers and carriers. Public-private data exchanges are maturing to enable transparent handoffs from ocean carriers to forwarders and warehouses, which reduces exception management and manual reconciliation at checkpoints. On the ground, parcel hubs have deployed AI-enabled sortation and automation to raise throughput during peaks without proportional ramp-up in headcount, with operators reporting accuracy improvements and faster cycle times in late 2025. These end-to-end visibility and automation capabilities reinforce the Singapore 3PL market as a pilot ground for APAC digital logistics solutions.

Deployment of Smart Warehousing and Robotics Solutions

Investments in high-density, multi-level facilities and automation continue to modernize Singapore’s warehousing backbone. DSV Pearl combines large multi-temperature zones with automation, such as AutoStore, to increase storage density and retrieval speed in a ramp-up footprint designed for land-scarce conditions. In July 2025, DSV opened RedLion2 as an energy-positive logistics hub designed for semiconductors and high-tech manufacturing, signaling the appetite for advanced automation that pairs with resilient, sustainable power design. DHL Supply Chain introduced a fully autonomous electric vehicle into in-plant operations for a major electronics client, integrating the vehicle into warehouse management systems to automate dock-to-line transfers. These deployments are paired with analytics, robotics-as-a-service, and energy optimization to shift cost structures from fixed to variable and to improve quality for industries with regulated handling needs. The combined effect is faster cycle times, more precise inventory control, and greater resilience during seasonal surges, which benefit the Singapore third-party logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Global Trade Volumes and External Demand Cycles | -0.8% | Global, acute sensitivity in Singapore transshipment | Short term (≤ 2 years) |

| Port Congestion and Transshipment Capacity Constraints | -0.5% | Singapore, knock-on to Malaysia and Indonesia | Short term (≤ 2 years) |

| Increasing Sustainability and Carbon Compliance Costs | -0.6% | Singapore national, EU-linked supply chains | Medium term (2-4 years) |

| Margin Pressure from Large E-Commerce and MNC Clients | -0.4% | Singapore, regional 3PL hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on Global Trade Volumes and External Demand Cycles

Singapore’s logistics performance is highly sensitive to swings in global trade policy and tariff regimes because a large share of cargo flows is transshipment rather than domestic consumption. U.S. tariff changes and the associated uncertainty weighed on business confidence in the second half of 2025, even as early-quarter activity held up, which injected volatility into shipping plans and hedging behavior. The Red Sea route disruptions and potential reopening add further complexity for Asia–Europe loops, introducing clustering effects at European ports that can ripple back to Singapore through bunching and re-routings. While PSA has increased berth capacity and uses AI to improve scheduling, operators still face planning risk when voyage patterns remain off schedule. These dynamics pressure the Singapore 3PL market with fluctuating volume forecasts that complicate workforce and fleet deployment cycles. The upside is that improvements in control tower orchestration and allocations can mitigate some of the variability as schedules normalize.

Port Congestion and Transshipment Capacity Constraints

In mid-2025, Singapore faced a spike in vessel wait times due to out-of-sequence arrivals and bottlenecks that stretched beyond normal congestion episodes. Off-schedule arrivals from rerouting around the Cape of Good Hope and reduced port calls contributed to container dumping and a higher transshipment workload, straining available quay and yard space. Authorities and terminal operators mitigated the surge by making additional berth capacity available and tightening berth planning with carriers to reduce dwell times, but normalization was expected to take time. These episodes highlight the sensitivity of the Singapore 3PL market to synchronized ocean schedules, especially when global disruptions cascade across regions. As Tuas ramps and digital yard planning expand, the system gains more shock absorbers to handle bunching and re-routing. The key for operators is to maintain agile capacity buffers without overcommitting fixed assets during temporary peaks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Fulfilment Models Diverge Across Speed and Complexity

Domestic Transportation Management holds a 33.65% share in 2025, making it the largest service in the Singapore 3PL market, as last-mile density, retail networks, and parcel hubs underpin stable domestic flows. The service benefits from route optimization, drop-off partnerships, and tighter integration between the express and postal networks, which raise throughput without adding equivalent fleet capacity. International Transportation Management leverages Singapore’s role as one of the world’s busiest container hubs, with 44.66 million TEUs in 2025, to provide a base for transshipment and consolidation strategies that move goods efficiently across Asia and beyond. Air connectivity upgrades also reinforce time-definite offerings, as FedEx’s direct Singapore–Anchorage flight compresses delivery cycles to key U.S. gateways for high-value shipments. Value-Added Warehousing & Distribution is the fastest-growing service with a forecast 4.80% CAGR, and the Singapore 3PL market size for this segment is supported by demand for multi-temperature storage, high-density automation, and compliance-heavy handling. Providers are scaling larger multi-customer platforms, as shown by recent capacity additions around Tuas and the Airport Logistics Park that target bonded inventory and faster short-to-ship cycles.

The service landscape is moving toward facility-led differentiation, with deep automation and specialized capability sets for regulated and high-value cargo. DSV’s network investments pair energy-efficient warehousing with automated storage and retrieval systems that compress pick times and increase storage density, improving service reliability for semiconductor and electronics clients. Contract logistics footprints at the Airport Logistics Park continue to add temperature-controlled zones and healthcare-specific workflows to address tight GDP and GMP standards. International freight execution is also benefiting from digitized port processes that reduce anchorage time variability and enable more predictable cutoffs for ocean and air. These dynamics sustain a balanced mix across domestic, international, and value-added services in the Singapore 3PL industry while steering incremental growth toward warehousing-centric solutions.

By End User: Healthcare Outpaces as E-Commerce Margins Compress

E-commerce is the fastest-growing end-user with a 5.74% CAGR, supported by express air uplift, weekend pickups, and cross-border staging that connect local sellers to international buyers. Parcel carriers deepened cooperation with postal networks to expand consumer drop-off options and reduce first-mile friction for SMEs, while automated hubs delivered accuracy and speed gains during peak season. At the same time, buyer consolidation and aggressive rate negotiations among large platforms sustain pressure on unit margins, which pushes providers to rely more on automation and routing intelligence to maintain profitability. Technology and electronics flows use Changi-linked gateways and specialized semiconductor hubs to support high-value movements that rely on short lead times and low damage risk. Cross-border haulage investments by global integrators expand options for high-tech and e-commerce customers across Thailand and Malaysia, strengthening Singapore’s role as a coordination node.[3]Source: Singapore Post, “News Releases,” Singapore Post, singpost.com

The life sciences and healthcare segment is also growing at a significant pace of 5.34% CAGR, underpinned by expanded GDP-compliant capacity and air corridors tailored for clinical shipments and biologics. UPS Healthcare’s new Tuas facility adds freezer capacity and on-site dry ice production to support stringent temperature requirements and end-to-end chain of custody for sensitive products. CEVA’s specialized platforms extend the cold chain beyond pharma into aerospace and vision care components that also require temperature stability and fast customs clearance. E-commerce and FMCG remain volume anchors, but the higher value density of life sciences skews incremental growth toward temperature-controlled, compliance-heavy services. This shift reinforces the Singapore 3PL industry as a hub for regulated cargo where service quality and audit readiness are central to shipper decisions.

By Logistics Model: Hybrid Models Emerge as Balance-Sheet Optimization Tool

Asset-heavy models capture 51.21% of the market in 2025, reflecting the capital intensity of multi-story ramp-up facilities and the need for in-house control over specialized environments for electronics, healthcare, and aerospace. Operators deploy high-density automation, AS/RS, and robotics to lock in long-term contracts with compliance-heavy customers and to lift reliability at scale. Asset-light models emphasize orchestration through digital platforms and cross-border road and air networks that monetize access without owning large footprints, including long-haul certified networks and 24/7 security operations for higher-risk cargo. Postal and express tie-ups in Singapore also illustrate how platform integration can extend range and lower first-mile barriers for SMEs.

Hybrid models are forecast to grow the fastest, at a 5.90% CAGR, and the pairing of owned strategic nodes with subscription-based robotics and third-party linehaul supports the Singapore 3PL market for hybrid approaches. This approach allows global 3PLs to retain control over high-touch value-added services such as conditioning, labeling, and compliance checks while flexing transport capacity up or down through partners. New facilities show the hybrid logic in action, blending temperature-controlled zones, automation, and energy efficiency with outsourced elements where appropriate. Cross-border road and air corridors anchor the asset-light portion, supported by certified fleets and real-time tracking to cover e-commerce and high-tech flows. The resulting mix favors agile scalability and lower balance-sheet intensity, which align with demand variability and compliance needs in the Singapore 3PL industry.

Geography Analysis

Singapore’s logistics base has a domestic footprint but regional reach, with 44.66 million TEUs of container throughput in 2025, supporting a large transshipment role that far exceeds local consumption. The Singapore 3PL market benefits from tight port-to-airport connectivity, enabling rapid handoffs and supporting two- to five-day delivery windows for many ASEAN corridors. As Tuas Port scales and airside processing accelerates, integrators and forwarders can consolidate inventory and orchestrate cross-border flows that balance speed and landed cost for shippers. E-commerce and high-tech shipments gain from weekend uplift and expanded drop-off options that shorten first-mile delays and improve injections to major export routes. The direction of travel positions Singapore to remain a staging and control center while manufacturing footprints diversify across ASEAN.

North–south corridors linking Singapore with Malaysia and Indonesia continue to deepen through infrastructure and regulatory cooperation. Cross-border road capacity expansions by global integrators increase options for e-commerce and high-tech clients and improve predictability for over-the-road flows between Thailand, Malaysia, and Singapore. The ASEAN-BAC UBIN initiative seeks to reduce identity and documentation frictions, thereby accelerating clearance and reducing idle time at borders. Singapore’s orchestrator role also connects to Vietnam and Thailand, where contract logistics and manufacturing bases are growing, spreading risk, and supporting multi-country inventory pooling. For time-definite lanes, express providers strengthened trans-Pacific reach from Singapore to the U.S. through direct uplift, compressing transit times and expanding weekend injection options. The effect is a larger catchment for the Singapore 3PL market, both by sea and by air.

Trade policy and routing shifts still shape near-term performance by lane. Red Sea disruptions and potential realignments can redistribute calls and cause bunchy arrivals, complicating schedule adherence and port capacity planning. As Tuas adds berths and deepens automation, Singapore gains more flexibility to handle temporary surges and out-of-sequence voyages. Postal and express partnerships within Singapore improve access to cross-border services for SMEs, broadening the exporter base and increasing the utilization of linehaul capacity. Operators that combine Singapore-based orchestration with scalable cross-border capacity into ASEAN remain best placed to grow share over the forecast period. This structure allows the Singapore 3PL market to capture value from both transshipment leadership and specialized services that command premium yields.

Competitive Landscape

Competition features integrated global incumbents and regionally focused specialists, with consolidation and facility upgrades shaping share outcomes. DHL Group is scaling specialized healthcare logistics capabilities through dedicated airfreight cold-chain services and end-to-end control for temperature-sensitive cargo, while also deploying automation in parcel operations to handle peak loads more efficiently. UPS Healthcare doubled its cold chain footprint at Tuas to deliver freezer capacity and on-site dry ice production, which supports clinical and commercial therapies with tight temperature bands. DSV is building a benchmark for energy-efficient, automated warehousing with Pearl and RedLion2, targeting high-tech manufacturing and semiconductor customers with stringent quality and uptime requirements. These moves create defensible niches in the Singapore 3PL market by pairing compliance, automation, and sustainability credentials that are hard to replicate quickly.

Regional players and postal-linked networks complement the global incumbents with targeted cross-border and last-mile capabilities. Kuehne Nagel invested in cross-border road capacity and equipment in Thailand to support e-commerce and high-tech clients across ASEAN, plugging into Singapore as a regional coordination point. Sing Post refocused its portfolio on parcels by divesting its freight-forwarding business in mid-2025 and expanding its collaboration with express carriers to expand drop-off points and broaden access for SMEs. Ninja Van expanded international delivery to 41 new destinations from Singapore, helping local brands scale regionally and supporting inventory localization alongside cross-border fulfillment. GEODIS expanded its certified road networks and security operations to improve resilience and sustainability outcomes for cross-border lanes connecting Singapore with major ASEAN destinations. This mix of capabilities increases shipper choice across service levels and cost-to-serve configurations.

Macro volatility and buyer consolidation shaped 2025 performance, prompting operators to lean harder into automation and service design to defend margins. Domestic parcel providers faced margin headwinds from volume mix and pricing pressure, but AI-driven sorting and routing lifted throughput and accuracy without proportionate labor growth. Facility investments around Tuas and the Airport Logistics Park show an ongoing commitment to cold chain and high-tech handling, and these assets are likely to channel more regulated cargo to Singapore over the forecast period. The strategic pattern favors hybrid models that pair owned, high-touch nodes with flexible transport capacity, reducing balance-sheet strain while maintaining quality for compliance-heavy cargo. As automation and sustainability investments compound, the Singapore 3PL market increasingly rewards scale operators and specialists who can quantify service quality and emissions outcomes credibly for large shippers.

Singapore 3PL Industry Leaders

Deutsche Post DHL Group

DSV

CEVA Logistics

CWT Ltd

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: CEVA Logistics commenced operations at its Airbus Helicopters regional distribution center in Singapore's Airport Logistics Park, featuring temperature-controlled warehousing (5°C to 25°C) and 24/7 AOG support for aerospace components across the Asia Pacific. The partnership leverages CEVA's 40-year collaboration with Airbus Helicopters and aims to capitalize on the USD 24.99 billion Asia-Pacific helicopter market forecast for 2030.

- February 2026: Ninja Van Singapore launched international delivery lanes covering 41 new countries beyond Southeast Asia, targeting local brands' global market access. By Invite Only Jeweler’s 234% Malaysia sales increase after switching to Ninja Van's local inventory support underscores the value proposition.

- December 2025: DHL Supply Chain deployed Singapore's first autonomous electric vehicle for supply chain operations at Infineon's facility, in partnership with Zelostech, achieving over 80% annual carbon reduction compared to diesel trucks. The fully electric AV integrates with warehouse management systems and features advanced navigation, marking Phase 1 of DHL's autonomous logistics roadmap.

- February 2025: DHL Group announced the expansion of its dedicated airfreight cold-chain network, with Singapore prioritized among eight countries (India, Japan, South Korea, Brazil, USA, Germany, Ireland) for GDP-compliant Boeing 777F routes under its EUR 2 billion (USD 2.35 billion) DHL Health Logistics investment. The Brussels-Cincinnati initial route demonstrates full end-to-end visibility for cell & gene therapies, reducing reliance on third-party carriers.

Singapore 3PL Market Report Scope

The report covers a comprehensive background analysis of the Singaporean Third-Party Logistics (3PL) market, including an assessment of the economy, market overview, market size estimates for key segments, emerging trends, market dynamics, and key company profiles. The impact of COVID-19 has also been incorporated into the study.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the growth outlook through 2031 for Singapore 3PL?

The Singapore 3PL market is USD 5.76 billion in 2025. It is projected to reach USD 7.23 billion by 2031 at a 3.74% CAGR.

Which customer segments lead and accelerate in Singapore 3PL?

E-commerce is the largest end user at 27.55% share in 2025. Life sciences and healthcare shows the fastest growth at 5.23% CAGR through 2031 as GDP-compliant cold chain capacity expands.

Which service lines present the best near term upside in Singapore 3PL?

Domestic Transportation Management holds a 33.65% share in 2025, anchoring scale for the last mile and the middle mile. Value-Added Warehousing and Distribution is expected to grow the fastest, at a 4.80% CAGR. Recent capacity additions include UPS Healthcare’s 11,500-square-meter Tuas site and CEVA’s healthcare hub expansions.

How will Tuas Port and digital initiatives change service reliability in Singapore 3PL?

Phase 1 of Tuas Port is planned to deliver 21 berths and 20 million TEUs of annual capacity by 2027, enabled by electrified automated yard cranes and a private 5G network. Just-in-time vessel scheduling and digital document flows via platforms like digitalPORT@SG aim to reduce anchorage wait times and improve predictability for forwarders and 3PLs.

What risks could disrupt execution in 2026 for logistics providers in Singapore?

The system remains exposed to global trade swings and port congestion, as mid-2025 arrivals bunched and off-schedule voyages led to container dumping and longer wait times before mitigation steps took hold. Operators are investing in AI-based planning and capacity at Tuas to build buffers against volatility.

How should shippers choose between asset heavy, asset light, and hybrid models in Singapore 3PL?

Asset-heavy providers hold a 51.21% share in 2025, while hybrid models are projected to grow the fastest at a 5.90% CAGR through 2031. Hybrid designs balance agility and control by pairing owned, high-touch nodes with partner transport and robotics-as-a-service, as seen at DSV Pearl’s automated multi-level facility.

Page last updated on: