Polysiloxane Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

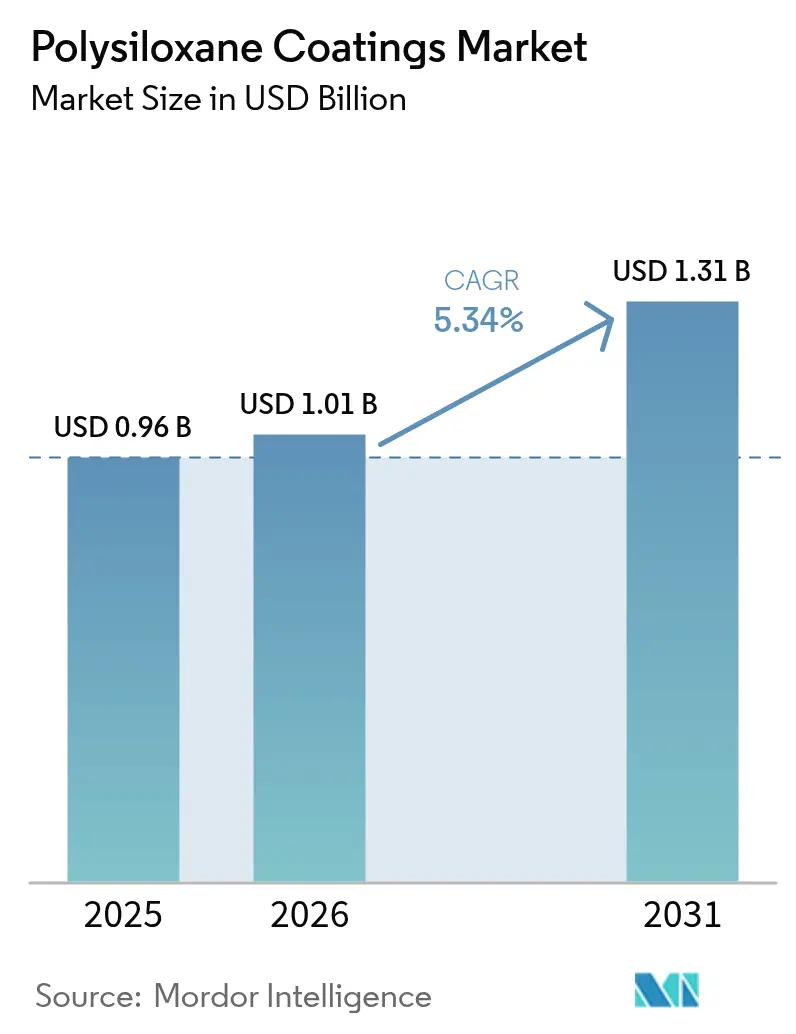

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polysiloxane Coatings Market Analysis by Mordor Intelligence

The Polysiloxane Coatings Market size was valued at USD 0.96 billion in 2025 and is estimated to grow from USD 1.01 billion in 2026 to reach USD 1.31 billion by 2031, at a CAGR of 5.34% during the forecast period (2026-2031). Offshore energy operators and shipbuilders are driving changes in adoption by committing to multi-year supply contracts for ultra-high-solid hybrid chemistries. These chemistries comply with stricter VOC regulations while withstanding thermal cycling on complex geometries. Increased LNG carrier construction, modular floating wind-tower yards in Europe, and the expansion of African crude oil and gas pipelines are extending demand cycles. The leading suppliers, including Akzo Nobel, PPG Industries, Hempel, Jotun, and The Sherwin-Williams Company, cater to global specifications, while regional specialists address niche performance requirements. The Asia-Pacific region leads with 55.22% share in 2025; however, Europe’s 2026 cap on cyclic siloxanes is compelling Asian formulators to either re-engineer export batches or lose market share to compliant European producers.

Key Report Takeaways

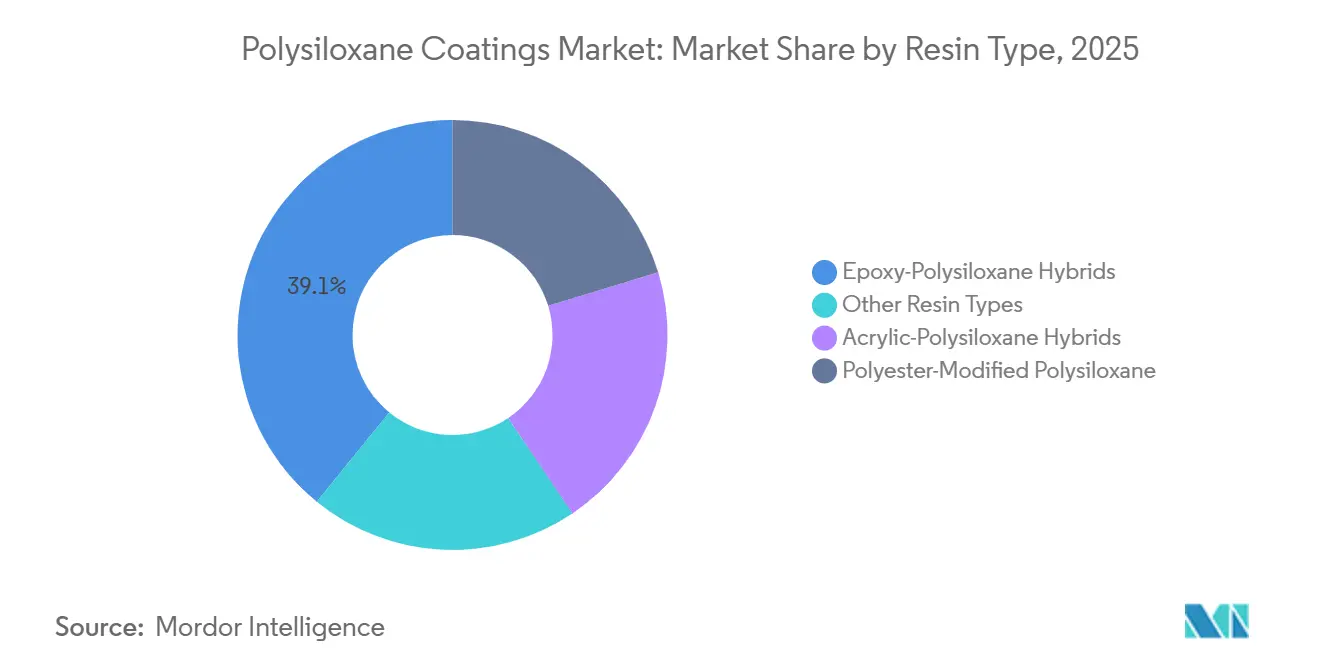

- By resin type, epoxy-polysiloxane hybrids held 39.12% of the polysiloxane coatings market share in 2025, while acrylic-polysiloxane hybrids are forecast to grow at a 5.71% CAGR through 2031.

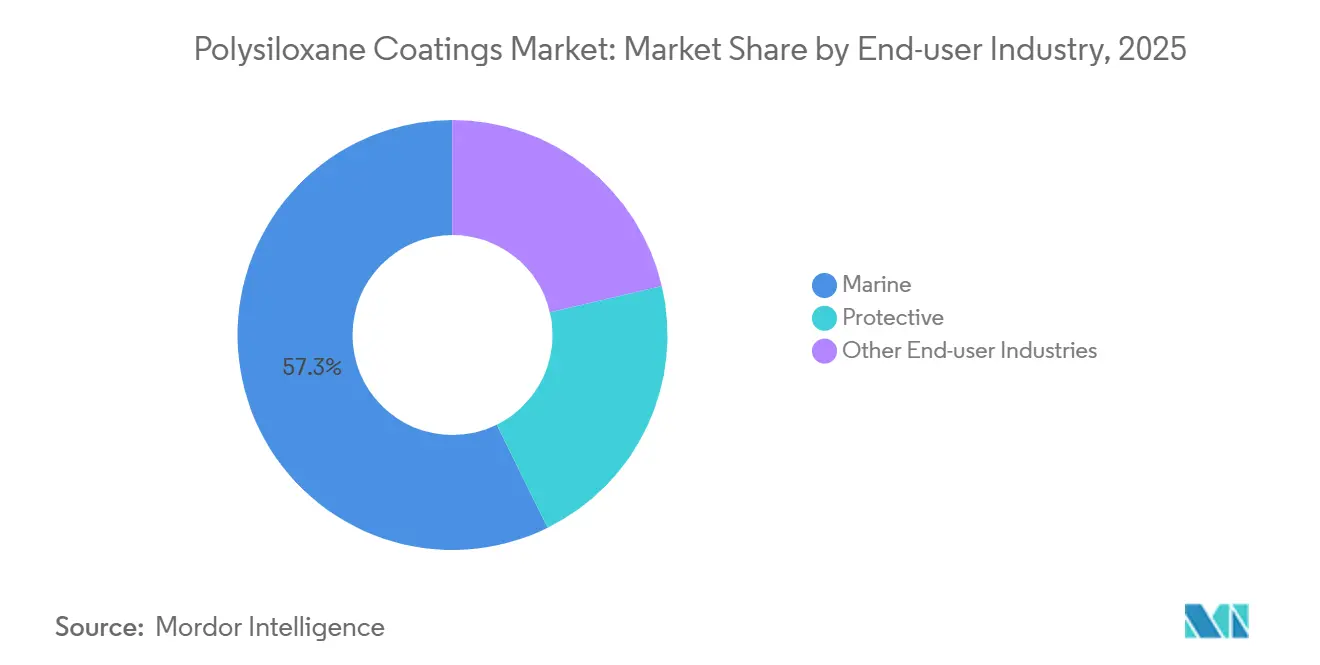

- By end-user industry, the marine segment commanded 57.31% of the polysiloxane coatings market share in 2025 and is projected to advance at a 6.12% CAGR through 2031.

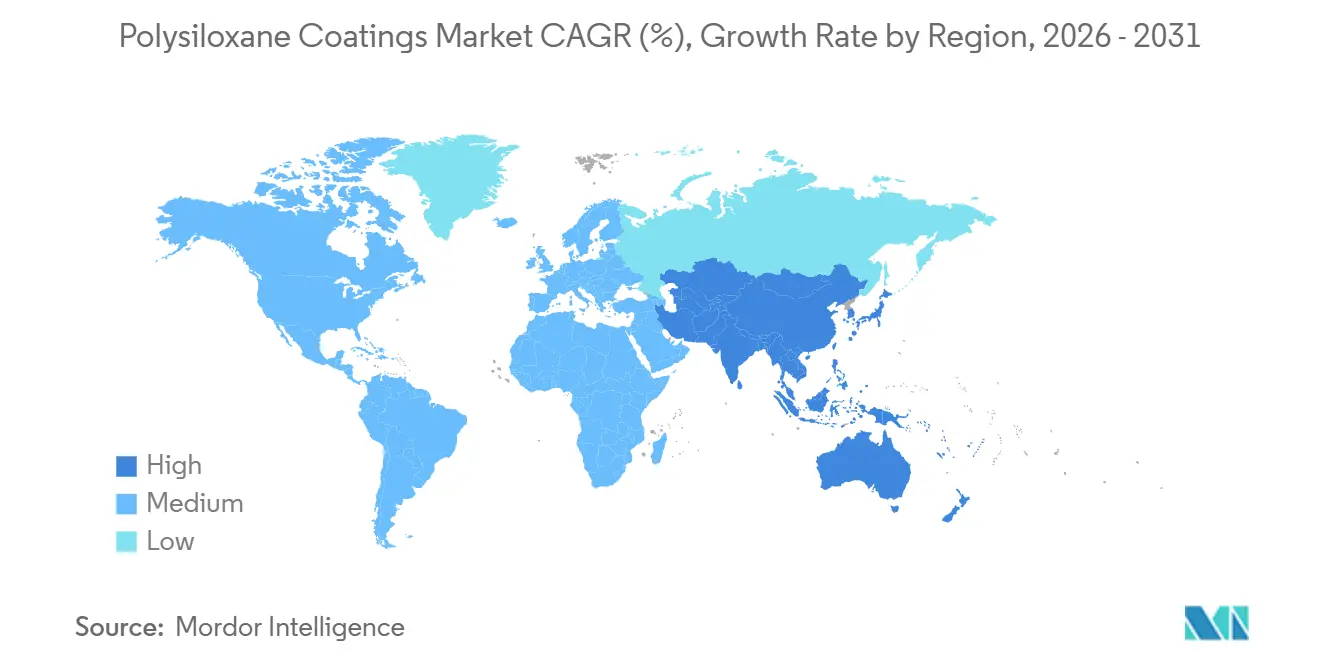

- By geography, Asia-Pacific captured 55.22% of the polysiloxane coatings market share in 2025 and is projected to grow at a 6.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polysiloxane Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising oil-and-gas CAPEX for corrosive offshore and shale assets | +1.2% | Global, with concentration in North America (Gulf of Mexico, Permian Basin), Middle-East (Saudi Arabia, UAE), and Asia-Pacific (offshore China, Malaysia) | Medium term (2-4 years) |

| Public-private megaproject pipelines in Asia and Africa | +0.9% | Asia-Pacific (China, ASEAN), Middle-East and Africa (Nigeria, Uganda, Tanzania, Morocco) | Long term (≥ 4 years) |

| Shift toward ultra-high-solid hybrid systems (≤100 g VOC/L) | +0.8% | Global, with early adoption in EU and North America driven by EPA and REACH compliance | Short term (≤ 2 years) |

| Modular floating wind-tower fabrication yards expansion | +0.7% | Europe (Poland, France, Scotland, Spain), Asia-Pacific (South Korea, China) | Medium term (2-4 years) |

| LNG carrier new-build spree under IMO GHG targets | +1.3% | Global, led by Asia-Pacific (South Korea, China shipyards) and Middle-East (Qatar orders) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Oil-and-Gas CAPEX for Corrosive Offshore and Shale Assets

Chevron’s 2026 capital plan, allocating USD 18-19 billion, designates USD 7 billion for offshore projects and USD 6 billion for shale operations. This investment drives demand for polysiloxane topcoats capable of withstanding hydrogen sulfide, salt spray, and cyclic heat on production modules. Murphy Oil’s USD 1.2-1.3 billion program highlights a trend toward life-extension projects over decommissioning, sustaining the need for retrofitting. Offshore operators prefer epoxy-polysiloxane film builds certified to ISO 12944 C5-M, as their siloxane-enriched surfaces repel chloride ions. Shale producers prioritize abrasion resistance for sand-handling equipment, valuing the hardness of polysiloxane hybrids. These differing performance requirements are steering acrylic-polysiloxane hybrids into midstream structures, where UV stability is more critical than immersion resistance.

Public-Private Megaproject Pipelines in Asia and Africa

Uganda’s USD 5 billion East African Crude Oil Pipeline, now 75% complete, is designed to operate at 50 °C, necessitating polysiloxane topcoats that can endure heat and humidity. Nigeria’s USD 24.6 billion Gas Revolution Industrial Park and the proposed USD 20-25 billion Atlantic Africa Pipeline present opportunities for large-diameter siloxane-capped systems resistant to solar exposure. Similarly, South-East Asian projects, such as Malaysia’s USD 34.56 billion Maharani Freeport and Thailand’s USD 29 billion Land Bridge, require durable coatings for jetty piles and storage tanks. Supply chains that integrate local blending with imported resin packages reduce freight costs and enhance bidding flexibility. Consequently, project-driven demand spikes benefit suppliers with regional manufacturing capabilities.

Shift Toward Ultra-High-Solid Hybrid Systems (≤ 100 g VOC/L)

The European Industrial Emissions Directive, which limits VOC levels to 100 g/L, is accelerating the adoption of high-solids epoxy-polysiloxane and acrylic-polysiloxane systems[1]European Environment Agency, “Industrial Emissions Directive,” eea.europa.eu. Colorado’s updated AIM rule mirrors this limit in North America. Suppliers have replaced aromatic solvents with reactive diluents that cure within the polymer network, maintaining film integrity while adhering to VOC regulations. In 2025, Arkema introduced waterborne one-component PVDF-acrylic hybrids, demonstrating that solvent-free platforms can achieve near-fluoropolymer durability at a lower cost. Contractors benefit from reduced odor and faster turnaround times in confined tank interiors, lowering respiratory protection expenses.

Modular Floating Wind-Tower Fabrication Yards Expansion

Companies such as Windar, BW Ideol, and Siemens Gamesa have established coastal yards to pre-assemble wind-tower sections before deployment, reducing construction timelines and favoring coatings that cure at ambient to 40 °C. Acrylic-polysiloxane hybrids meet these requirements while maintaining flexibility to accommodate tower oscillation. Projects by Vestas and Mingyang in Poland and Scotland underscore demand in cooler climates, where traditional epoxy-polysiloxanes require elevated-temperature bake cycles. Automated blast-and-coat lines now apply polysiloxane topcoats in a single 150-200 micron pass, reducing labor costs. As Northern Europe expands its Wind Turbine Installation Vessel (WTIV) fleets, suppliers securing yard approvals are positioned to increase volumes ahead of broader market growth for polysiloxane coatings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening rules on cyclic siloxane by-products (D4, D5) | -0.6% | EU (REACH Regulation 2024/1328), with spillover to North America and Asia-Pacific export markets | Short term (≤ 2 years) |

| Edge-defect failures under high-temperature cycling | -0.3% | Global, particularly in power generation (boiler stacks, turbine housings) and petrochemical sectors | Medium term (2-4 years) |

| Fluoropolymer top-coat substitution threat | -0.4% | North America and EU, where specifiers prioritize 20+ year service life over initial cost | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Rules on Cyclic Siloxane By-Products (D4, D5)

Regulation 2024/1328 limits D4 content to 0.5% and D5/D6 content to 0.3% in marine and protective coatings, effective from June 6, 2026[2]European Commission, “Regulation 2024/1328 on Cyclic Siloxanes,” eur-lex.europa.eu. This compels formulators to use higher-cost linear siloxanes and certify low-cycle content through third-party testing. Asian exporters face a choice between reformulating products or redirecting volumes to less-regulated markets, disrupting economies of scale. While the regulation acknowledges offshore performance needs, ongoing NGO pressure sustains regulatory risks, delaying long-term R&D investments. California’s Safer Consumer Products list, which flags D4 and D5, signals potential U.S. action that could further increase compliance costs. Suppliers with advanced waterborne chemistries are better positioned to adapt to future restrictions.

Edge-Defect Failures Under High-Temperature Cycling

Polysiloxane coatings applied to sharp edges and welds can crack under thermal cycling between ambient and 150-250 °C, as observed in boiler and reactor applications. The thermal-expansion mismatch between the siloxane surface layer and the epoxy or acrylic backbone concentrates stress at points where film thickness tapers. Stripe-coating with epoxy-phenolic primers mitigates this risk but increases labor and staging costs, reducing polysiloxane’s efficiency advantage. Experimental siloxane-branched polyurethane dispersions offer greater flexibility but lack hardness, limiting their commercial viability. Some specifiers are shifting to fluoropolymer or ceramic-filled epoxies for high-temperature zones, restricting polysiloxane adoption in power equipment applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Hybrids Gain on Epoxy Dominance

Epoxy-polysiloxane hybrids accounted for 39.12% of 2025 revenue, driven by their immersion resistance and cathodic-disbondment properties, which are critical for subsea pipelines. Acrylic-polysiloxane hybrids are expected to grow at a 5.71% CAGR through 2031, the highest among resin types, as renewable energy structures increasingly prioritize their UV stability and ambient curing capabilities. Patent filings from Chugoku Marine Paints and research initiatives by Anhui Jianzhu University highlight the growing intellectual property focus on acrylic-based formulations. Polyester-modified variants are addressing cold-climate requirements in regions such as Canada and Nordic countries. Meanwhile, experimental chemistries, including polysilazane-crosslinked acrylics, remain in pilot stages but reflect the ongoing innovation shaping the polysiloxane coatings market.

Regulatory pressures are influencing demand trends. High-solids formulations favor epoxy hybrids, as reactive diluents help maintain viscosity without increasing VOC levels. Acrylic hybrids are particularly effective in single-pass applications of 150-200 microns on floating wind foundations, reducing labor requirements by up to 20% compared to traditional three-coat epoxy systems. With Europe enforcing a 0.1% limit on cyclic siloxanes in consumer products, formulators are transitioning to acrylic and polyester matrices to minimize cyclic residuals. Suppliers offering both resin types are well-positioned to meet the dual demands of marine retrofitting and the growing renewable energy sector, ensuring sustained growth in the polysiloxane coatings market.

By End-user Industry: Marine Industry Drives Growth

The marine industry accounted for 57.31% of 2025 sales and is expected to grow at a 6.12% CAGR through 2031. This growth is supported by QatarEnergy’s 128-carrier LNG fleet expansion and the global shift of container fleets toward LNG or methanol propulsion. Protective coatings represent the remaining market share, with revenue distributed across oil and gas, power generation, and infrastructure sectors. ISO 12944 C5-M standards ensure polysiloxane coatings are integral to hulls, decks, and superstructures, particularly for cryogenic cargo containment applications.

In protective applications, oil and gas capital expenditures drive the use of epoxy hybrids on subsea risers and topsides, while power plants favor acrylic hybrids for turbine housings and stacks exposed to temperature fluctuations. Infrastructure demand remains steady but fragmented, with municipal water tanks, bridges, and treatment plants requiring NSF or AWWA approvals. Polysiloxanes excel in these applications due to their superior gloss and color retention. Competitive differentiation often hinges on technical service capabilities, such as field training for applicators and on-site performance validation, rather than resin cost. This combination of high-volume shipyard projects and specification-driven infrastructure recoating supports consistent growth in the polysiloxane coatings market.

Geography Analysis

The Asia-Pacific region accounted for 55.22% of the revenue in 2025 and is projected to grow at the fastest CAGR of 6.63% through 2031. Growth is driven by South Korea’s USD 5.7 billion wind-installation vessel backlog, China’s 18-vessel LNG award, and ASEAN infrastructure megaprojects. Local blending partnerships help offset freight costs, maintaining margins despite aggressive price competition. Regulatory diversity, such as GB/T standards in China versus ISO adoption in Singapore, allows non-compliant VOC or siloxane formulations to persist in some markets, sustaining low-price segments. India’s refinery expansions and offshore projects in the Krishna-Godavari basin are creating additional demand for polysiloxane topcoats certified to NORSOK M-501. In Japan, demand is focused on maintenance recoats for aging infrastructure rather than new projects, emphasizing products with high service life.

In North America, Chevron’s USD 7 billion offshore budget and Murphy Oil’s USD 1.2-1.3 billion allocation are driving demand in the Gulf of Mexico, while shale plays prioritize abrasion-resistant polysiloxane coatings. California AIM regulations and EPA HAP limits are encouraging the adoption of high-solids and waterborne chemistries. Sherwin-Williams’ USD 1.9 billion acquisition of Sika’s North American industrial coatings arm highlights deeper vertical integration across primer, topcoat, and concrete-repair lines. Additionally, Mexico’s cross-border pipelines connecting Permian gas to Pacific LNG terminals are adding midstream demand, which relies on U.S. specification approvals.

In Europe, offshore wind yards in France, Spain, and Scotland are driving demand for acrylic hybrids with ambient cure and flexibility. Regulation 2024/1328’s siloxane cap is increasing reformulation costs but provides protection for European producers against low-compliance imports. Nordic markets prioritize coatings that cure at 5-10 °C, positioning polyester-modified polysiloxanes favorably. Germany’s chemical and inland shipping sectors continue to sustain protective coating volumes, while the UK’s North Sea decommissioning activities are creating opportunities for fast-cure topcoats that minimize platform downtime.

South America, along with the Middle-East and Africa, contributed the remaining market share. Brazil’s pre-salt developments and hydroelectric upgrades generate irregular but high-tonnage orders for polysiloxanes when approved. In the Middle-East and Africa, projects such as Saudi Arabia’s NEOM, Uganda’s EACOP, and Nigeria’s gas corridor are driving demand for C5-M grade topcoats, often specifying multinational brands to meet lender audit requirements. However, currency fluctuations and tender budgets limit the uptake of premium products, allowing locally blended epoxies to compete on price. Together, these regions provide geographic diversification for the polysiloxane coatings market, mitigating risks associated with reliance on a single growth hub.

Competitive Landscape

The polysiloxane coatings market remains moderately concentrated, with Akzo Nobel, PPG Industries, Hempel, Jotun, and The Sherwin-Williams Company collectively accounting for 64% of the revenue in 2025. These companies leverage global raw-material contracts and multi-continent manufacturing facilities to maintain their positions in LNG new-builds and offshore wind structures. Akzo Nobel reported Q3 2024 sales of EUR 2.64 billion, driven by marine projects utilizing high-solids powder primers. PPG’s Q3 2024 net sales of USD 4.6 billion reflect strong performance in aerospace and protective coatings, which support R&D investments in waterborne polysiloxanes.

Consolidation continues to shape the market. Sherwin-Williams’ USD 1.9 billion acquisition of Sika’s North American industrial coatings arm integrates flooring, grouts, and concrete repair into a broader protective coatings portfolio, enhancing cross-selling opportunities during refinery turnarounds. Hempel’s launch of Hempadur Avantguard 750 offers a 20-year offshore lifespan with reduced recoat intervals, addressing lifecycle cost concerns critical to asset owners. Tnemec, with a turnover of USD 200-225 million, exemplifies niche specialization through acquisitions of Tex-Cote, ProPolymer, and Epoxytec, focusing on potable-water tanks, CUI mitigation, and polymer concrete linings, supported by robust technical field services.

Regional competitors include Tianjin Jinhai and Yung Chi Paint in China, Asian Paints in India, and KISHO Corporation in Japan. These companies leverage proximity to shipyards and lower labor costs, often pricing their products 15-25% below multinational competitors. Innovation opportunities are emerging in waterborne acrylic-polysiloxane dispersions for renewable energy equipment, where UV stability and under-film corrosion resistance are prioritized over immersion performance. Success through 2031 will depend on early compliance with EU siloxane caps and the rapid scaling of waterborne platforms, determining which suppliers capture the next wave of growth in the polysiloxane coatings market.

Polysiloxane Coatings Industry Leaders

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

Hempel A/S

Jotun

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Researchers in China developed a new class of hydrogen-terminated hyperbranched polysiloxanes to improve the performance of silicone-based release coatings. This advancement supported the polysiloxanes coatings market by addressing challenges in anti-sticking systems, which are critical for various industrial applications.

- February 2025: Wacker Chemie AG introduced SILRES HP 2000 LV, a low-viscosity silicone resin hardener designed for high-solids epoxy-polysiloxane coatings. By reducing volatile compounds to less than 0.1%, it supported polysiloxanes coatings market by enhancing sustainability and safety standards.

Global Polysiloxane Coatings Market Report Scope

Polysiloxane coatings are high-performance protective coatings that are siloxane hybrids formulated with an organic resin such as an epoxy or acrylate system. These coatings are known for their excellent durability, weather resistance, and unique properties that make them suitable for different industries, such as oil and gas, power, infrastructure, and others.

The Polysiloxane Coatings Market is segmented by resin type, end-user industry, and geography. By resin type, the market is segmented into epoxy-polysiloxane hybrids, acrylic-polysiloxane hybrids, polyester-modified polysiloxane, and other resin types. By end-user industry, the market is segmented into marine, protective, and other end-user industries. The protective industry is further segmented into oil and gas, power, and infrastructure. The report also covers the market size and forecasts for polysiloxane coatings in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Epoxy-Polysiloxane Hybrids |

| Acrylic-Polysiloxane Hybrids |

| Polyester-Modified Polysiloxane |

| Other Resin Types |

| Marine | |

| Protective | Oil and Gas |

| Power | |

| Infrastructure | |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Epoxy-Polysiloxane Hybrids | |

| Acrylic-Polysiloxane Hybrids | ||

| Polyester-Modified Polysiloxane | ||

| Other Resin Types | ||

| By End-user Industry | Marine | |

| Protective | Oil and Gas | |

| Power | ||

| Infrastructure | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the polysiloxane coatings market?

The polysiloxane coatings market stands at USD 1.01 billion and is forecast to reach USD 1.31 billion by 2031 at a 5.34% CAGR from 2026 to 2031.

Which resin type is expanding the most through 2031?

Acrylic-polysiloxane hybrids are projected to grow at a 5.71% CAGR through 2031, benefiting from ambient-temperature cure and UV stability demanded by offshore wind towers.

Why are marine specifications important for suppliers?

The marine segment already represents 57.31% of 2025 revenue and requires 15-year dry-dock intervals, securing recurring high-value orders for compliant coatings.

What regulation will most affect formulation in Europe?

Regulation 2024/1328 caps cyclic siloxanes in marine and protective coatings from June 2026, forcing reformulation or supply-chain realignment for non-compliant producers.

Page last updated on: