Shortenings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.42 Billion |

| Market Size (2031) | USD 7.34 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shortenings Market Analysis by Mordor Intelligence

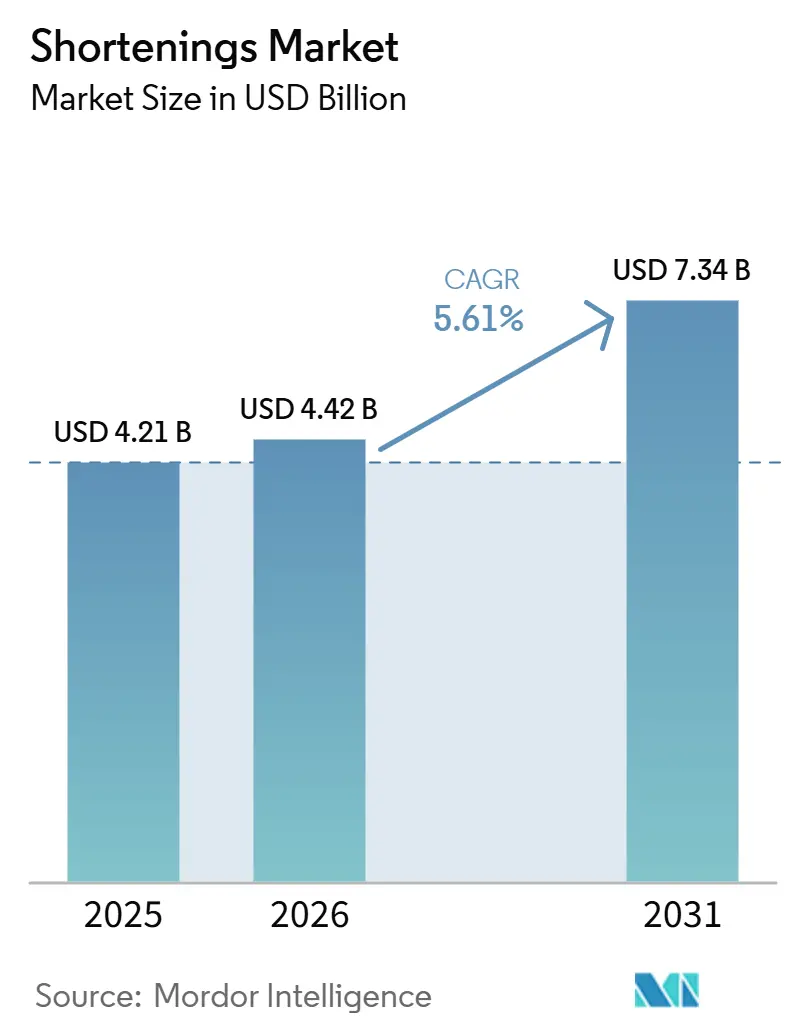

The shortenings market size was valued at USD 4.21 billion in 2025 and is estimated to grow from USD 4.42 billion in 2026 to reach USD 7.34 billion by 2031, at a CAGR of 5.61% during the forecast period (2026-2031). The shortenings market is being shaped by wider adoption of trans-free fat systems, continued reformulation of older hydrogenated fat portfolios, and stricter compliance expectations across industrial food production[1]Source: World Health Organization, “WHO Recognizes Four Countries with Life-Saving Trans Fat Elimination Policies,” WHO News, who.int. Demand is also benefiting from the expansion of frozen bakery supply chains, where precise shortening performance matters for layered texture, aeration, handling, and shelf life in large-scale production. Competitive conditions remain balanced between large integrated processors with refining depth and specialty suppliers that compete through formulation quality, technical support, and application-specific fats. The shortenings market is also seeing stronger opportunity in emerging bakery and foodservice systems, especially where organized retail, quick-service restaurant formats, and cold-chain distribution are scaling together. At the same time, palm-linked sourcing risk, certification pressure, and biofuel competition are making feedstock access a more important differentiator for producers with broad regional networks and alternative oil capabilities.

Key Report Takeaways

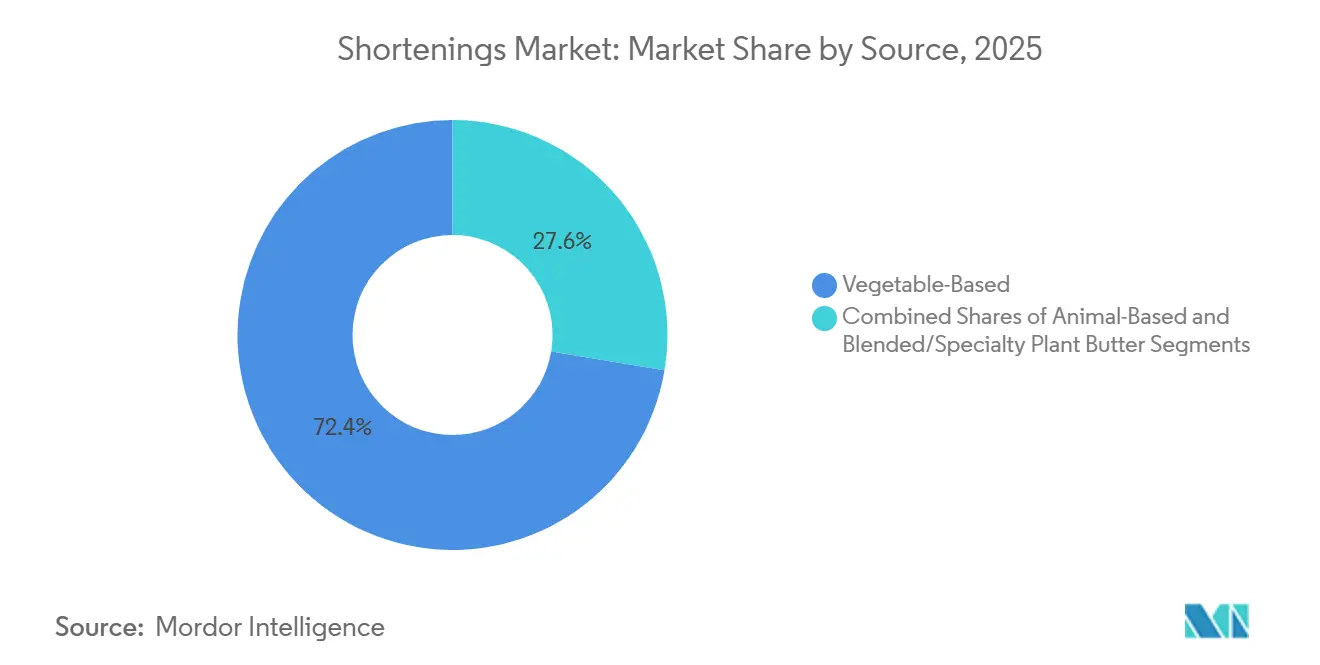

- By source, vegetable-based shortenings held 72.37% of the shortenings market share in 2025, while blended and specialty plant butters are projected to expand at a 7.12% CAGR through 2031.

- By form, Solid All-Purpose held 45.02% share in 2025, while Puff/Lamination recorded the highest projected CAGR at 6.78% through 2031.

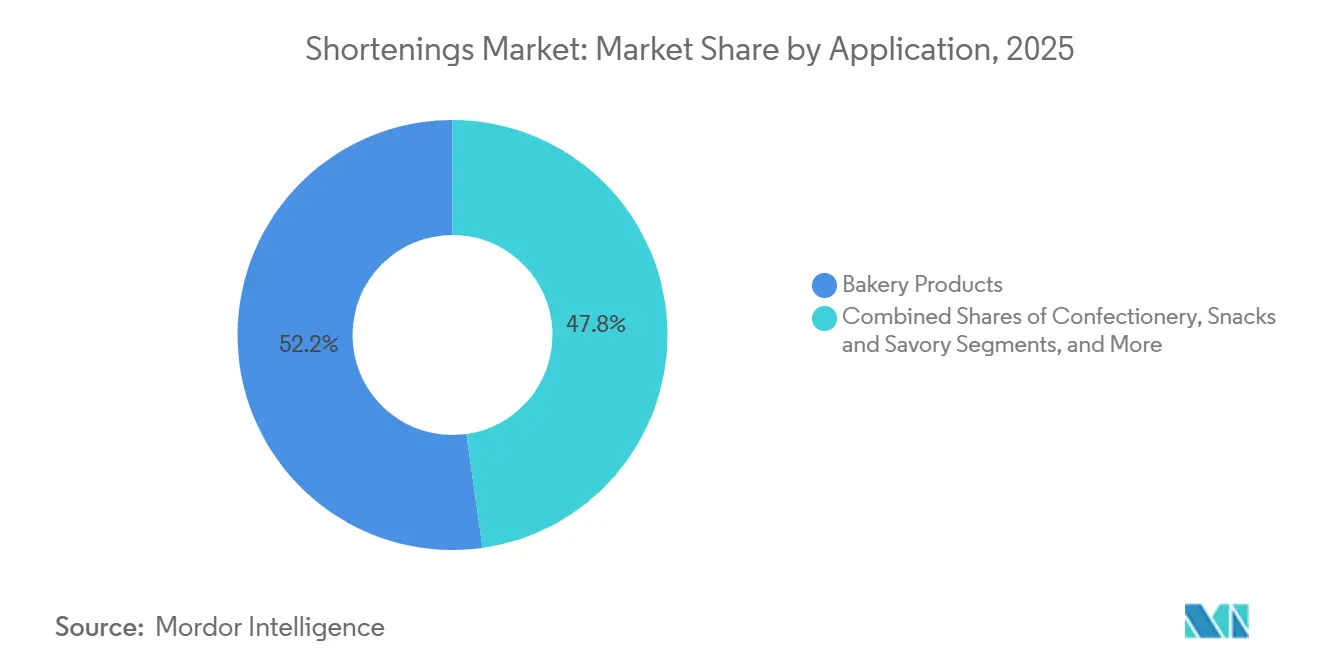

- By application, Bakery Products accounted for 52.23% of the shortenings market size in 2025, while Frozen Desserts and Ice Cream are advancing at a 7.32% CAGR through 2031.

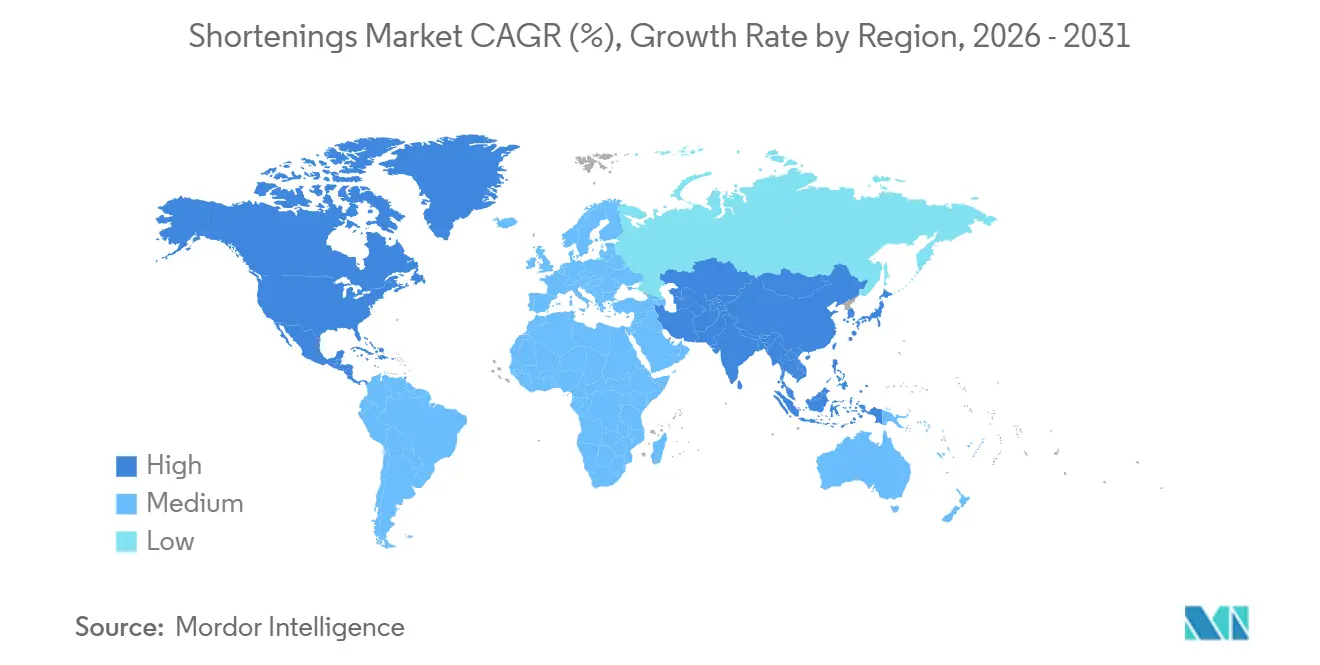

- By geography, Asia-Pacific held 35.25% of global revenue in 2025 and is also forecast to grow at the fastest regional CAGR of 6.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Shortenings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Clean-Label and Trans-Free Fats in Baking Industry | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Increasing Consumption of Confectionery Products | +0.8% | Global, led by Asia Pacific and Europe | Medium term (2-4 years) |

| Advancements in Specialty and Functional Shortenings | +0.7% | Global, led by North America and Europe, with expansion into Asia Pacific | Long term (≥ 4 years) |

| Surge in Demand for Plant-Based Shortenings | +0.9% | Global, led by North America and Europe, with fast Asia Pacific adoption | Medium term (2-4 years) |

| Expansion of Frozen Bakery and Ready-to-Bake Products | +0.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Rising Demand from Foodservice and QSR Sector | +0.5% | Global, with the fastest momentum in Asia Pacific and the Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Clean-Label and Trans-Free Fats in Baking Industry

The shift away from partially hydrogenated oils has become a compliance requirement across industrial baking and food processing. As of May 2025, nearly 60 countries had best-practice trans fat elimination policies in effect, covering 46% of the global population. WHO validation in 2024 for Denmark, Lithuania, Poland, Saudi Arabia, and Thailand, followed by Austria, Norway, Oman, and Singapore in 2025, showed that stricter regulation is spreading into a wider set of export and processing markets. This is raising the value of enzymatic interesterification, because it allows producers to reshape fatty acid profiles without hydrogenation and to supply trans-free functional fats with greater regulatory confidence[2]Source: American Oil Chemists' Society, “Enzymatic Interesterification,” AOCS Resource Centre, aocs.org. Producers that already operate these systems have a clearer advantage in pricing, technical positioning, and customer retention than smaller processors that still depend on older chemical routes. In the shortenings market, this shift is reinforcing barriers to entry and directing more compliant demand toward integrated multinational suppliers with stronger reformulation capabilities.

Surge in Demand for Plant-Based Shortenings

Plant-based shortenings are gaining traction across confectionery, bakery, and adjacent food applications, not only in products positioned for vegan claims. The sharp cocoa price pressure seen in 2024 pushed confectionery producers toward cocoa butter equivalents, cocoa butter replacers, and other specialty plant fat systems that remain commercially useful even after the immediate price shock. A 2025 peer-reviewed study in Foods showed that enzymatically interesterified plant-based shortening from Triadica sebifera oil achieved the β′ crystal form that supports smooth texture and consistent mouthfeel, while keeping trans-fatty acid levels below 0.1%. That matters because the shortenings market depends on fats that can meet performance expectations, not only label claims. Suppliers with upstream relationships in shea, coconut, and high-oleic sunflower are therefore better placed than those that rely mainly on standard commodity pools. This is helping the shortenings market move toward plant systems that deliver both formulation flexibility and stronger margin potential.

Expansion of Frozen Bakery and Ready-to-Bake Products

Frozen bakery remains one of the steadiest demand channels for high-performance shortenings because laminated doughs, filled pastries, and portioned cakes require fats that hold structure through freezing and baking. Puff and lamination systems need consistent crystallization behavior, plasticity, and solid fat content to deliver layered texture at industrial scale. A 2025 study in LWT - Food Science and Technology found that enzymatic interesterification of palm stearin and rice bran oil blends improved crystallization behavior and supported shortening performance for fast-frozen food applications. That technical requirement favors suppliers that can control formulation tightly and produce at repeatable quality levels. The growth of in-store bakery formats and ready-to-bake lines is also broadening the customer base beyond very large industrial contracts. In the shortenings market, this is increasing demand for specialty grades that can deliver bakery consistency across different production scales and handling conditions.

Rising Demand from Foodservice and QSR Sector

Quick-service restaurant chains remain a stable source of shortening demand because frying and baking operations depend on predictable fat behavior across large outlet networks. These customers value fry life, oil absorption control, crispness, and repeatable output more than simple headline input cost. Expansion in Southeast Asia and Latin America is widening the installed base of institutional demand as urban consumption patterns, delivery platforms, and organized restaurant formats continue to scale. Reformulated shortenings also fit with menu commitments around trans-fat-free positioning and broader brand standards on ingredient quality. That creates a commercial pull that supports higher-value shortening systems in bakery and frying uses. For the shortenings market, this channel provides a durable outlet where functionality and operational consistency often matter more than pure commodity pricing.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Preference for Healthier Fat Alternatives | -0.7% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Stringent Regulations on Trans Fats | -0.4% | Global, led by Europe and North America | Short term (≤ 2 years) |

| Sustainability Concerns Surrounding Palm Oil | -0.8% | Global, especially in palm-dependent Asia Pacific and European supply chains | Long term (≥ 4 years) |

| Supply Chain Disruptions for Edible Oils | -0.5% | Global, with South and Southeast Asia most exposed | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations on Trans Fats

Trans fat regulation supports demand for reformulated products, but it also raises the compliance burden for producers that need to rebuild processes and portfolios. WHO standards require countries to limit industrially produced trans-fatty acids to below 2g per 100g of total fat or to ban partially hydrogenated oils outright, and validation activity accelerated through 2024 and 2025. Producers that still operate older chemical interesterification lines face a difficult capital decision when customers begin to require cleaner, more defensible formulations. In several emerging markets, the new rules are reducing the competitiveness of local suppliers that were built around legacy commodity grades. This can shift volume toward imported compliant specialty fats even when end demand remains intact. In the shortenings market, the result is a tighter operating environment where compliance spending can compress margins before it fully translates into higher-value sales.

Sustainability Concerns Surrounding Palm Oil

Palm oil remains central to a large share of shortening production, but sustainability scrutiny is adding new cost and reputation risk to that dependence. Research published in Frontiers in Plant Science in 2026 noted that oil palm expansion into peatlands can release up to 120 tonnes of CO2-equivalent per hectare per year, which has intensified investor and buyer attention on palm-heavy supply chains. Certification systems such as RSPO, ISPO, and ISCC are becoming more important procurement filters, especially where customers expect traceability and deforestation-related assurance[3]Source: Roundtable on Sustainable Palm Oil, “From Boycotts to Inclusion, Is Sustainable Palm Oil Finally the Way Forward,” RSPO, rspo.org. At the same time, Indonesia's planned centralization of palm oil exports from September 2026 is adding uncertainty around trade routing, pricing visibility, and feedstock access for global buyers. These pressures are widening the gap between producers with certified alternative fat systems and those whose portfolios remain heavily exposed to palm fractions. Across the shortenings market, that dynamic is making sourcing resilience just as important as product functionality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Vegetable Fats Dominant, but Specialty Blends Claim the Growth Premium

Vegetable-based shortenings held 72.37% of the shortenings market share in 2025, supported by a strong cost-to-performance balance across bread, biscuits, cakes, fried snacks, and other high-volume food uses. Soybean oil, palm fractions, and canola remain the core feedstocks because they offer reliable functionality and broad industrial availability. The segment also benefits from better compatibility with trans-free formulation goals than older hydrogenated systems. High-oleic sunflower is gaining relevance in premium and clean-label products, and that shift is starting to lift average selling prices within vegetable-based portfolios. A 2025 study in Foods showed that enzymatically interesterified mustard oil and palm stearin blends could deliver shortening functionality with exclusive β′ crystallinity and no detectable trans fats, which supports continued movement away from animal-based options in specialty applications.

Animal-based shortenings such as lard, tallow, and dairy-derived formats still serve selected traditional foodservice and confectionery uses where specific mouthfeel and flavor remain important. Their role is narrower, however, because dietary preferences and labeling expectations continue to shift toward plant-derived systems. Blended and Specialty Plant Butters form the fastest-growing source segment, and the shortenings market size for this category is projected to expand at a 7.12% CAGR through 2031. Fuji Oil Group identified cocoa butter equivalents and compound chocolate as core growth engines in its vegetable fats business, with volume targeted to rise by 5-10% through equipment improvements in FY2026. This segment draws support from the same regulatory and sustainability trends that are changing the broader shortenings market, while also offering higher margin potential than standard commodity formats.

By Form: Solid All-Purpose Anchors Volume, Puff/Lamination Sets the Pace

Solid All-Purpose shortening commanded 45.02% of market volume in 2025, which reflects its broad usefulness across bread, donut frying, bakery mixes, and general commercial baking. This is still the most practical format for markets that are scaling standardized bakery manufacturing capacity and need dependable handling at competitive cost. It remains important in countries such as India, Vietnam, and Indonesia, where bulk formats support cost-efficient production across growing organized food channels. Cake and Icing grades keep a stable position because premium cake, decorated dessert, and patisserie formats still require consistent aeration and texture. Liquid and Frying products serve commercial frying demand, while Flaked and Dry grades remain tied to dry-mix systems and convenience-led foodservice uses.

Puff and Lamination shortenings are the fastest-growing form, and the shortenings market size for this segment is forecast to rise at a 6.78% CAGR from 2026 to 2031. Demand is being driven by frozen croissants, pastries, and laminated dough products supplied to quick-service restaurant chains and in-store bakery programs. These products require a tightly controlled plastic range and dependable solid fat content, which limits participation from producers that lack technical precision. A 2025 study in LWT - Food Science and Technology confirmed that enzymatic interesterification of palm stearin and rice bran oil blends improved the crystallization profile needed for fast-frozen food applications. In the shortenings market, that performance threshold is reinforcing the gap between specialty manufacturers and commodity suppliers.

By Application: Bakery Leads on Volume, Frozen Desserts on Growth Velocity

Bakery Products represented 52.23% of shortening consumption in 2025, giving this category the leading shortening market share across all major applications. Bread, cakes and pastries, cookies and biscuits, and donuts remain the largest combined users of functional fats because shortening supports crumb structure, aeration, tenderness, and shelf-life extension. Cakes and pastries carry the highest value per unit because they require high-ratio functionality and stable emulsification. Cookies and biscuits generate the highest absolute volume, especially across Asia Pacific where large bakery chains and multinational foodservice operators have expanded production. Confectionery also uses shortenings in compound coatings, cream fillings, and molded alternatives, while Snacks and Savory and Ready-to-Eat and Prepared Meals depend on frying stability, texture management, and freeze-thaw performance.

Frozen Desserts and Ice Cream record the fastest application-level growth, and the shortenings market size for this application is projected to advance at a 7.32% CAGR through 2031. Demand is rising as chilled and frozen dessert formats gain wider acceptance in Southeast Asia and the Middle East, where cold-chain systems are improving. This segment needs shortenings that can maintain structure through temperature variation and prevent bloom in compound-coated frozen novelties. The use case is also broadening as consumers shift toward smaller-portion indulgent products that still need stable fat systems to maintain mouthfeel and product quality. In the shortenings market, that makes frozen dessert applications an important outlet for suppliers investing in structured lipids with precise melting behavior.

Geography Analysis

Asia-Pacific accounted for 35.25% of global revenue in 2025, giving the region the leading shortenings market share worldwide. It is also the fastest-growing regional cluster, with the shortenings market size in Asia-Pacific projected to expand at a 6.65% CAGR through 2031. This position reflects the region's dual role as a major palm-based feedstock center and a rapidly industrializing bakery production base. China remains central because its industrial bakery system supports large-scale demand for functional fats across commercial baking and food processing. India, Vietnam, Indonesia, and Thailand are also becoming more important as quick-service restaurant expansion, organized retail bakery formats, and rising disposable incomes support higher institutional demand.

North America remains the second-largest regional market and continues to set the benchmark for trans-fat elimination and clean-label shortening formulation. The United States benefits from mature cold-chain infrastructure, large quick-service restaurant networks, and in-store bakery programs that create steady demand for Solid All-Purpose and Cake and Icing grades. Canada keeps a meaningful canola-based processing base through suppliers such as Richardson International and Stratas Foods, which supports a cleaner positioning against soybean and palm-derived alternatives. Europe presents a mixed pattern, with softer retail table spread demand in parts of Western Europe but continuing industrial bakery demand for laminated pastry and frozen baked goods. Procurement standards linked to traceability and certification are pushing European buyers toward RSPO-certified materials and alternative fat systems that can reduce palm exposure.

South America is centered on Brazil, where a growing packaged food base, an expanding quick-service restaurant sector, and soybean-linked refining support steady shortening demand. Argentina and Chile add demand from confectionery and packaged snacks, although input cost swings have affected operating margins for local processors. The Middle East and Africa are growing quickly after Asia Pacific, supported by GCC food processors, expanding packaged food demand in Nigeria and Egypt, and a halal-oriented shortening base that fits regional food standards. Turkey is also becoming more relevant for premium functional fats as suppliers target the country's large snack export base and wider processed food capacity.

Competitive Landscape

The shortenings market remains moderately concentrated, with a small group of vertically integrated companies shaping upstream oilseed processing, refining, and global logistics. Bunge, Wilmar, Cargill, and ADM hold structural advantages because they can link raw material access with formulation scale and distribution reach. A second tier that includes Fuji Oil, Vandemoortele, CSM Ingredients, and Kerry Group competes more on technical differentiation and application-specific performance. This creates a market where upstream scale matters, but so do specialized fat systems, customer support, and process know-how. The gap between broad commodity capability and higher-value formulation expertise is becoming more visible as compliance, traceability, and functional performance standards continue to rise.

Recent strategy has moved in two directions, with consolidation upstream and specialization downstream. Cargill announced a multi-million-dollar expansion of its Port Klang, Malaysia edible oil plant in March 2026, adding a new specialty fats line and placing its Lipid R&D center closer to customers in Asia-Pacific and Europe, the Middle East, and Africa. Vandemoortele signed an agreement in March 2025 to acquire Bunge's European Margarines and Spreads business, which strengthens its distribution reach and its position in plant-based fats across Europe. Fuji Oil Group reported that new specialty fat and compound chocolate production lines are commencing in Japan, Canada, Europe, and Australia during H2 FY2026, which supports wider specialty fats capacity within its network. Bunge's integration moves and planned refining additions also point to a stronger vertically integrated position across multi-oil processing and specialty ingredient supply.

Acquisition scope remains meaningful in Southeast Asia and South America, where smaller regional processors often lack the capital needed to move from chemical platforms to advanced enzymatic systems. That makes technical retrofits, licensing, and outright consolidation viable paths for larger companies with balance-sheet capacity. Innovation is also continuing at the process level, with new attention on faster and lower-enzyme-load batch interesterification routes that can improve economics for specialty fats. At the same time, RSPO, ISCC, and related sourcing frameworks are becoming harder procurement requirements in many business-to-business channels, which raises the barrier for non-certified suppliers. The shortenings market is therefore likely to reward companies that can combine feedstock security, certification depth, and technical performance with regional customer responsiveness.

Shortenings Industry Leaders

Cargill Inc.

AAK AB

Wilmar International

Stratas Foods LLC

Bunge Holdings S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Cargill announced a multi-million-dollar expansion of its edible oil plant in Port Klang, Malaysia, adding a new specialty fats production line, the first in Cargill's global edible oils network to deploy specialty fats processing technology.

- February 2025: Bunge and Viterra completed their merger to create a premier global agribusiness solutions company, enhancing capabilities in oilseed processing and specialty plant-based oils and fats with projected annual operational synergies of USD 250 million within three years

- October 2024: Stratas Foods agreed to acquire AAK Foodservice in Hillside, New Jersey for approximately USD 56.55 million, expanding manufacturing facilities from eight to nine locations in the US

Global Shortenings Market Report Scope

| Vegetable-based |

| Animal-based |

| Blended and Specialty Plant Butters |

| Solid All-Purpose |

| Cake and Icing |

| Puff / Lamination |

| Liquid / Frying |

| Flaked and Dry |

| Bakery Products | Bread |

| Cakes and Pastries | |

| Cookies and Biscuits | |

| Donuts and Muffins | |

| Confectionery | |

| Snacks & Savory | |

| Frozen Desserts & Ice Cream | |

| Ready-to-Eat & Prepared Meals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Vegetable-based | |

| Animal-based | ||

| Blended and Specialty Plant Butters | ||

| By Form | Solid All-Purpose | |

| Cake and Icing | ||

| Puff / Lamination | ||

| Liquid / Frying | ||

| Flaked and Dry | ||

| By Application | Bakery Products | Bread |

| Cakes and Pastries | ||

| Cookies and Biscuits | ||

| Donuts and Muffins | ||

| Confectionery | ||

| Snacks & Savory | ||

| Frozen Desserts & Ice Cream | ||

| Ready-to-Eat & Prepared Meals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the shortenings sector and where is it headed by 2031?

The shortenings market was valued at USD 4.21 billion in 2025, stands at USD 4.42 billion in 2026, and is forecast to reach USD 7.34 billion by 2031 at a 5.61% CAGR.

Which source category leads revenue and which one is growing the fastest?

Vegetable-based shortenings led with 72.37% share in 2025, while blended and specialty plant butters are projected to grow fastest at a 7.12% CAGR through 2031.

Which form type is most important for current demand?

Solid All-Purpose led with 45.02% of market volume in 2025 because it fits the widest range of bakery and frying applications.

Which region offers the strongest growth outlook?

Asia Pacific led with 35.25% of revenue in 2025 and is expected to grow fastest at a 6.65% CAGR through 2031 because it combines feedstock strength with fast bakery industrialization.

Page last updated on: