Privileged Access Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

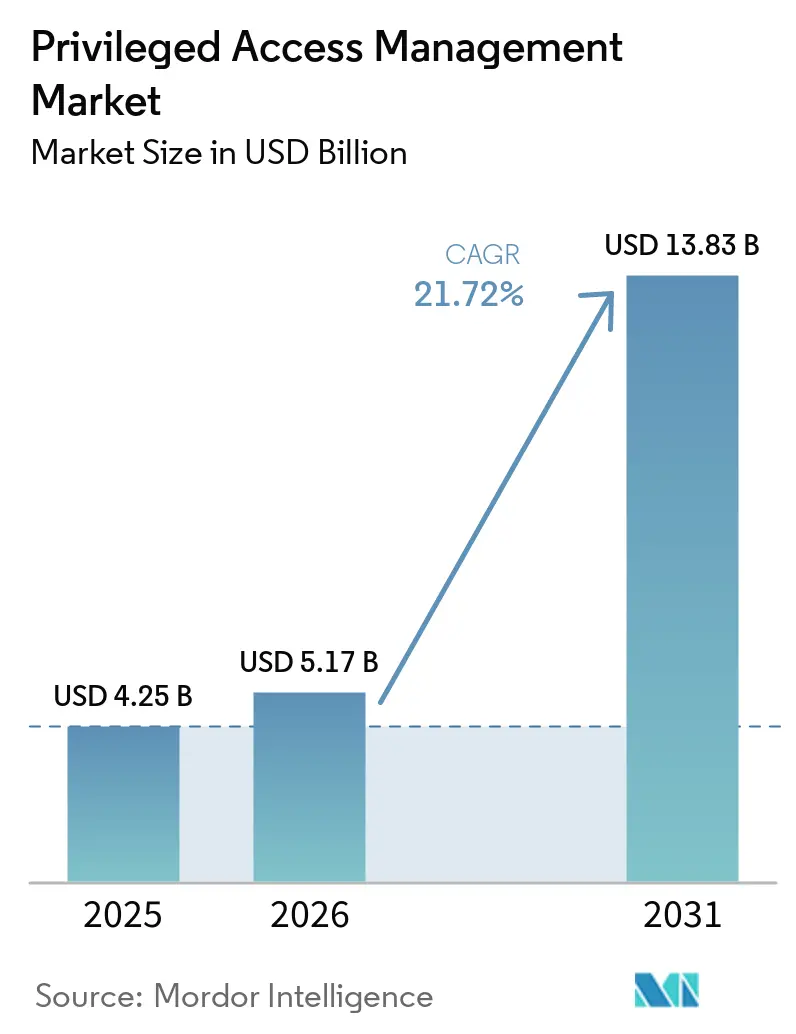

| Market Size (2026) | USD 5.17 Billion |

| Market Size (2031) | USD 13.83 Billion |

| Growth Rate (2026 - 2031) | 21.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Privileged Access Management Market Analysis by Mordor Intelligence

The Privileged Access Management Market size is expected to increase from USD 4.25 billion in 2025 to USD 5.17 billion in 2026 and reach USD 13.83 billion by 2031, growing at a CAGR of 21.72% over 2026-2031.

Demand accelerates as machine identities now outnumber human identities by 40:1, forcing enterprises to automate credential vaulting, extend controls to non-human accounts, and embed zero-trust policies across hybrid estates. Implementation urgency also rises because insurers increasingly require PAM controls before underwriting cyber-risk policies, and post-quantum cryptography migration compels organisations to modernise vaulting algorithms well before 2030. Vendors that combine vaulting, session monitoring, and entitlement governance inside a single platform gain a competitive advantage as buyers gravitate toward unified identity security architectures that reduce integration overhead and accelerate time to value.

Key Report Takeaways

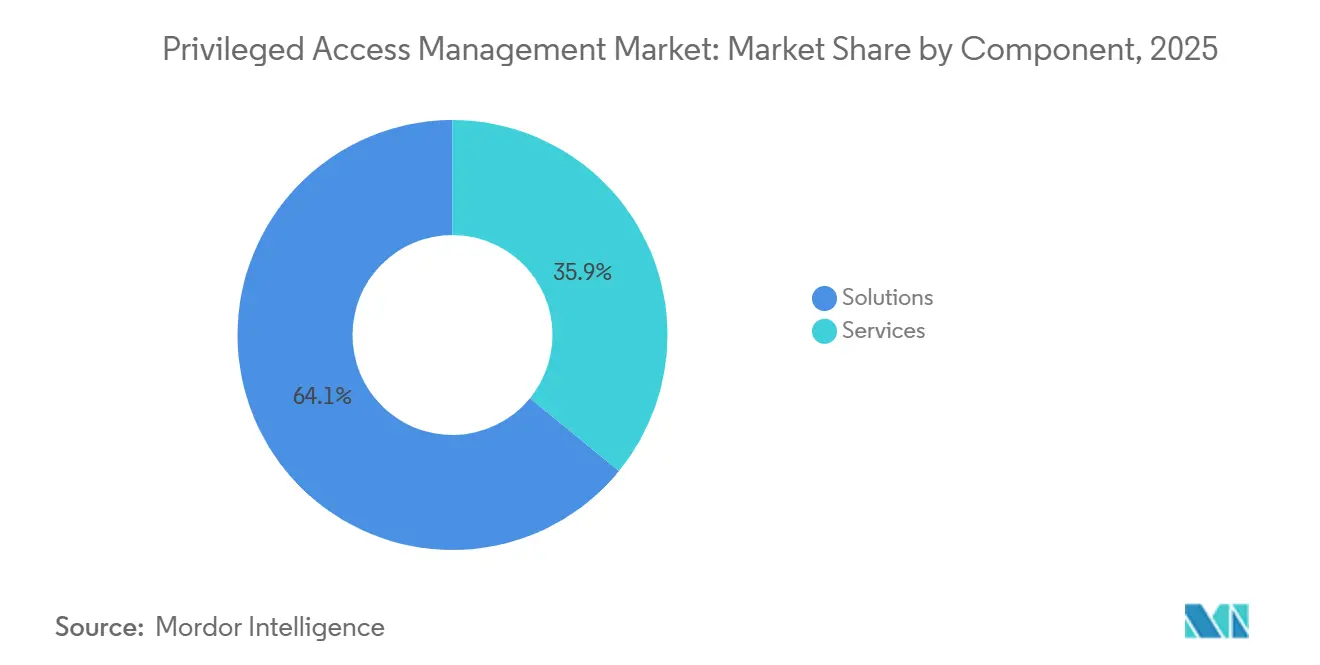

- By component, solutions led with 64.10% of privileged access management market share in 2025; services are projected to record the fastest 24.40% CAGR through 2031.

- By deployment mode, cloud deployments commanded a 57.05% share of the privileged access management market size in 2025, while hybrid deployments are forecast to expand at a 24.10% CAGR to 2031.

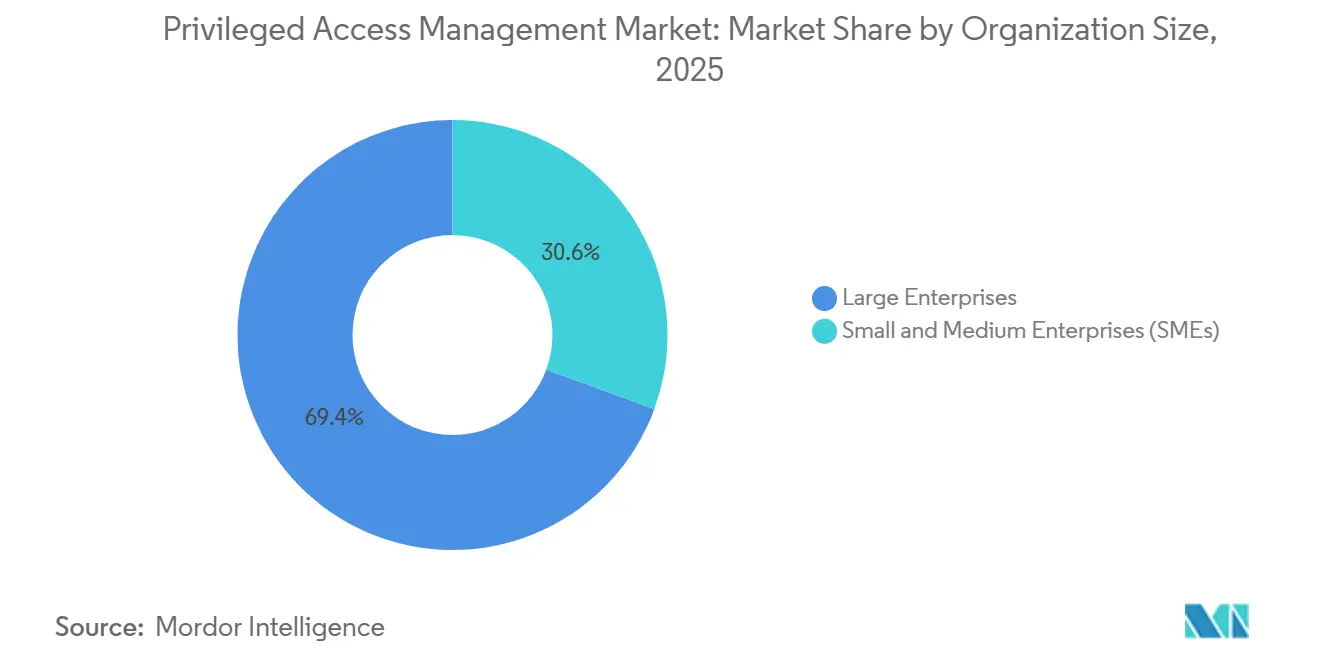

- By organization size, large enterprises held 69.40% privileged access management market share in 2025; small and medium enterprises are expected to advance at a 24.70% CAGR through 2031.

- By end-user industry, BFSI captured 28.30% revenue share in 2025, whereas healthcare is projected to expand at a 23.20% CAGR between 2026 and 2031.

- By type of access control, endpoint privilege management accounted for 37.80% of the privileged access management market size in 2025; cloud and SaaS privilege management is poised to grow at a 23.90% CAGR in the forecast period.

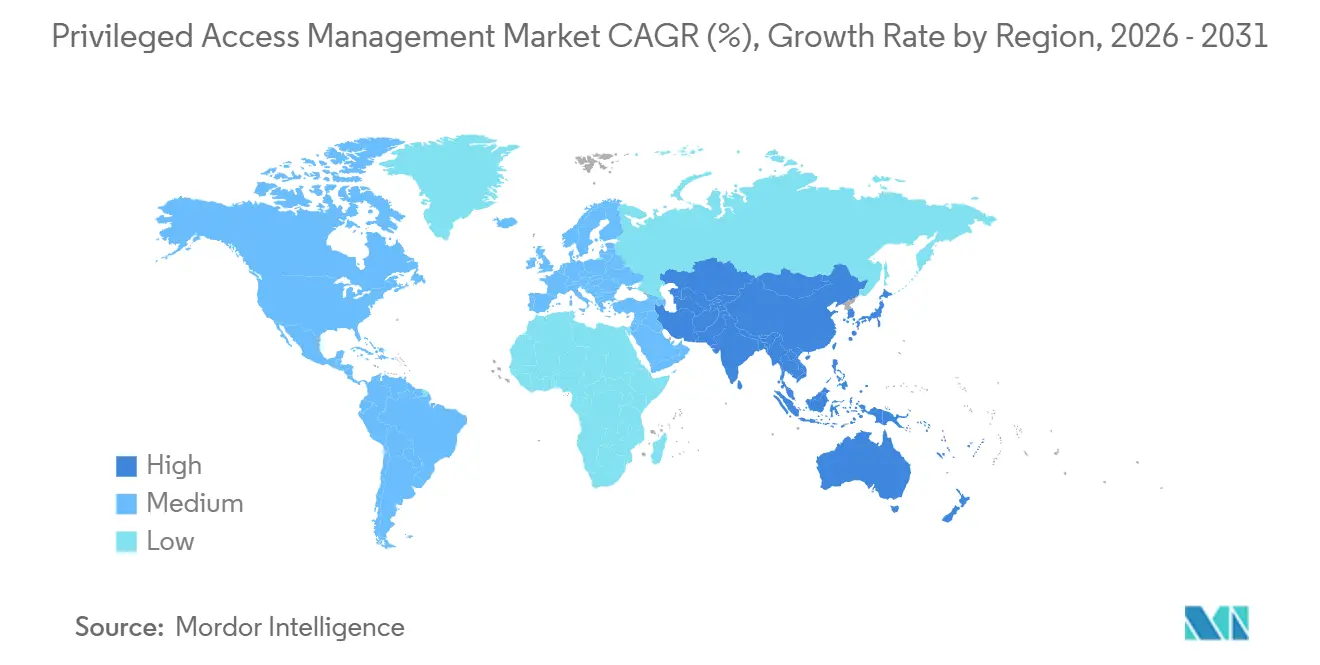

- By geography, North America led with 38.10% share of the market in 2025, while Asia-Pacific is projected to register the fastest 23.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Privileged Access Management Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid proliferation of machine identities and secrets management complexity | +4.2% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Zero-trust architectures accelerating privileged session isolation | +3.8% | North America and Europe core, expanding to APAC | Medium term (2-4 years) |

| Cloud-native PAM demand from DevSecOps tool-chain integration | +3.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| AI-driven attack surface discovery boosting PAM adoption in OT and IoT | +2.9% | Global, with early adoption in manufacturing-heavy regions | Long term (≥ 4 years) |

| Stringent cyber-insurance underwriting requirements | +2.7% | North America and Europe primarily | Short term (≤ 2 years) |

| Post-quantum crypto transition pressure on credential vaulting | +2.1% | Global, with government and defense sectors leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of Machine Identities and Secrets Management Complexity

Organisations running microservices, containers, and event-driven architectures now generate thousands of short-lived service accounts every day, creating a credential-sprawl problem that legacy vaults cannot absorb. CyberArk observes ratios of 40 machine identities for every human identity, and 87% of enterprises admit to storing secrets in multiple, unmanaged locations. [1]CyberArk, “You've Got Privileged Access Management… But Can You Keep Secrets Secure?” CYBERARK.COM Vendor roadmaps respond with automated discovery, rotation, and behavioural analytics tuned to non-human accounts, a capability highlighted by Saviynt’s research that calls for machine-identity-specific lifecycle policies.

Zero-Trust Architectures Accelerating Privileged Session Isolation

Government frameworks such as the United States Department of Defense Zero Trust Execution Roadmap require privileged access management controls by FY 2027, confirming that just-in-time provisioning and continuous session validation are mandatory inside zero-trust blueprints. [2]Department of Defense, “Zero Trust Capability Execution Roadmap,” DODCIO.DEFENSE.GOV Enterprises in finance and healthcare mirror these mandates, causing PAM vendors to integrate with identity federations, micro-segmentation gateways, and behavioural risk engines that revoke privileges when contextual risk rises.

Cloud-Native PAM Demand from DevSecOps Tool-Chain Integration

Continuous integration and continuous deployment pipelines break when manual credential approvals impede release velocity. Cloud-native PAM products expose API-first architectures that inject secrets just-in-time, enabling fully automated deployment workflows. Case studies at P0 show enterprises reducing deployment times by bypassing VPN-centric workflows and adopting ephemeral SSH certificates that expire within minutes. As 89% of enterprises follow multi-cloud strategies, end users demand platform-agnostic controls spanning AWS, Azure, and GCP.

AI-Driven Attack-Surface Discovery Boosting PAM Adoption in OT and IoT

Machine-learning scanners from industrial cyber-security providers such as Armis detect hidden privileged accounts inside SCADA controllers and PLCs that previously fell outside IT’s visibility perimeter. As IT and OT networks converge, manufacturers and utilities must extend PAM to production lines, prompting vendors to harden gateways for latency-sensitive, occasionally air-gapped environments. Palo Alto Networks demonstrates how AI algorithms classify device roles and recommend least-privilege policies inside industrial zones.

Restraints Impact Analysis of Privileged Access Management Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills scarcity for PAM deployment and lifecycle governance | -2.8% | Global, most acute in APAC and emerging markets | Medium term (2-4 years) |

| Brownfield integration complexity across hybrid legacy estates | -2.3% | North America and Europe, where legacy infrastructure dominates | Short term (≤ 2 years) |

| Shadow-IT proliferation undermining policy enforcement | -1.9% | Global, with higher impact in decentralized organizations | Medium term (2-4 years) |

| High TCO for SMEs amid subscription sprawl | -1.6% | Global, particularly affecting emerging markets and cost-sensitive sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skills Scarcity for PAM Deployment and Lifecycle Governance

Identity-security programmes demand expertise across cryptography, directory services, and API integration—skills in chronic short supply worldwide. Enterprises often discover that staff versed in traditional identity governance struggle to operate cloud-native analytics modules that rely on machine-learning models. Large banks and healthcare networks offset the gap through long-term managed service contracts, while many SMEs postpone projects until external consultants become available. Vendor response includes low-code policy builders and prescriptive deployment templates that reduce configuration time but cannot fully eliminate the need for skilled practitioners.

Brownfield Integration Complexity Across Hybrid Legacy Estates

Mainframes, Unix clusters, and bespoke OT controllers seldom expose modern API hooks, forcing IT teams to script custom connectors that inflate project timelines and budgets. ForgeRock and SSH Communications Security highlight coexistence toolkits that allow password-based legacy access and certificate-based modern access under one pane of glass. However, every additional connector raises the attack surface and complicates audit workflows, tempering the overall privileged access management market CAGR by 2.3 percentage points according to Mordor Intelligence modelling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Privileged Access Management Market Segment Analysis

By Component:

Solutions Dominate Through Platform ConsolidationThe solutions category dominated the privileged access management market, accounting for 64.10% revenue share in 2025, while the services category is projected to grow at 24.40% CAGR through 2031. Platform consolidation remains the primary buying criterion as enterprises favour unified vaulting, session isolation, and entitlement analytics delivered within a single console. The privileged access management market size for solutions reached USD 2.72 billion in 2025 and is forecast to exceed USD 8.2 billion by 2031, whereas services will climb from USD 1.53 billion to USD 5.65 billion during the same horizon. CyberArk’s USD 1.54 billion acquisition of Venafi illustrates a vendor playbook that merges machine-identity management with human-privilege workflows. Buyers cite lower integration costs and faster audit readiness as decisive factors when selecting all-in-one platforms over point products.

Services growth is propelled by three factors: a chronic shortage of identity-security experts, rising complexity in hybrid estates, and the shift toward outcome-based managed services that bundle tool licensing with 24×7 monitoring. Managed service providers advertise predictable subscription pricing that aligns with OpEx-oriented security budgets, particularly among SMEs. Continuous advisory services also help enterprises keep pace with quarterly compliance updates and emerging post-quantum cryptography guidelines, allowing service partners to maintain double-digit expansion throughout the decade.

By Deployment Mode:

Hybrid Models Address Legacy Integration ChallengesCloud deployments captured 57.05% of privileged access management market share in 2025, reflecting buyer preference for SaaS-delivered vaults and policy engines that avoid on-premises hardware. The privileged access management market size for cloud deployments reached USD 2.42 billion in 2025, with a projected USD 7.75 billion valuation by 2031. Hybrid implementations, however, post the fastest 24.10% CAGR as enterprises bridge on-premises mainframes and air-gapped OT networks with cloud control planes. SSH Communications Security’s PrivX offers side-by-side password vaulting and certificate-based brokerage, enabling phased migration without downtime.

Persistent regulatory requirements in defence, utilities, and payment processing keep on-premises deployments relevant, especially where data sovereignty statutes forbid external key stores. Vendors mitigate migration risk through containerised vault appliances that run inside private clouds yet replicate metadata to SaaS analytics clusters, offering a compromise between local control and cloud-scale insights. Over the forecast period, hybrid adoption will outpace pure cloud in verticals with significant legacy footprints, while green-field digital natives will remain fully SaaS.

By Organization Size:

SME Adoption Accelerates Through Insurance MandatesLarge enterprises controlled 69.40% of the privileged access management market share in 2025, due to compliance budgets and dedicated security operations teams. Yet, small and medium enterprises will expand at a 24.70% CAGR as cyber-insurance mandates push them toward privileged access tooling that was once considered optional overhead. The privileged access management market size for SMEs was USD 1.3 billion in 2025 and is forecast to surpass USD 4.85 billion by 2031. Delinea case studies indicate that retailers and equipment-leasing firms deployed PAM chiefly to satisfy policy terms, unlocking premium reductions of up to 18%.

Cloud-delivered vaults with per-user pricing appeal to SMEs by removing infrastructure costs and reducing administrative burden. Vendors also simplify user interfaces, ship pre-built policy templates, and embed self-service onboarding wizards to shorten deployment cycles from months to weeks. As insurers raise the bar annually, SMEs are expected to maintain double-digit spending momentum well into the next decade, contributing meaningfully to overall market acceleration.

By End-User Industry:

Healthcare Surge Driven by Regulatory ComplianceBFSI led the privileged access management market with 28.30% revenue share in 2025, propelled by stringent data-protection laws and real-time payment platforms that demand traceable administrator actions. Healthcare, however, will compound at 23.20% CAGR after a surge of ransomware attacks exposed gaps in hospital network defences. The privileged access management market size attributed to healthcare stood at USD 645 million in 2025 and will grow beyond USD 2.28 billion by 2031. Electronic health record mandates, connected medical devices, and HIPAA extension clauses now explicitly reference least-privilege and session monitoring controls.

Energy, manufacturing, and telecom sectors maintain steady adoption because OT networks and 5G core nodes face credential-based sabotage risks. Government agencies accelerate funding to comply with zero-trust deadlines, generating a healthy pipeline for vendors equipped with FedRAMP and ISO certifications. Retail and e-commerce buyers adopt PAM to secure payment systems and supply-chain integration APIs, though growth in those verticals trails regulated industries where penalties for non-compliance are immediate and severe.

By Type of Access Control:

Cloud and SaaS Management Leads InnovationEndpoint privilege management remained the largest sub-segment in 2025 at 37.80% market share, driven by operating-system hardening and the need to remove local administrator rights in dispersed workforces. The fastest trajectory belongs to cloud and SaaS privilege management, at 23.90% CAGR, as enterprises wrestle with hundreds of platform-specific admin portals and granularity differences between AWS IAM, Google Cloud IAM, and Microsoft Entra Permissions Management. Application-to-application password management and shared administrative account vaulting uphold consistent demand, though innovation focus clearly tilts toward cloud entitlement governance and least-privilege automation frameworks.

Cloud-native sub-platforms increasingly integrate policy-as-code modules that map Terraform or CloudFormation state files to privilege templates, allowing DevOps teams to verify compliance in pre-production pipelines. Vendors insert just-in-time brokering layers that issue short-lived tokens rather than long-standing keys, minimising blast radius in the event of compromise. This technical pivot fuels segment growth and underpins the broader transition toward zero-standing privilege architectures.

Geography Analysis

North America Privileged Access Management Market

North America retained 38.10% privileged access management market share in 2025, reflecting regulatory impetus from federal zero-trust mandates and high breach-cost awareness. The United States Treasury’s crackdown on ransomware-facilitated money laundering compels banks and insurers to treat privileged access as a control of first resort. Canada follows similar patterns through updated PIPEDA guidelines, while Mexico’s financial authorities impose vaulting requirements on cross-border payment service providers. Market incumbents maintain extensive partner ecosystems, enabling rapid scaling of managed PAM consumption models.

APAC Privileged Access Management Market

Asia-Pacific will rise at a 23.60% CAGR through 2031, the fastest worldwide trajectory. Singapore’s Monetary Authority guidelines require privileged access controls across banking infrastructures, setting a benchmark that ripples across ASEAN member states. Japan’s mature cyber-security culture drives platform refresh cycles; Zoho Japan secured 46.2% shipment share in 2023 via its Password Manager Pro offering, while NTT TechnoCross captured consecutive industry awards for domestic PAM leadership. Growth in China and India stems from smart-manufacturing programmes and data-localisation statutes that require strong audit trails for administrator actions.

Europe Privileged Access Management Market

Europe notes steady adoption due to GDPR and the EU Network and Information Security Directive that penalise inadequate privileged-account protection. Germany and the United Kingdom head regional spending because automotive, financial, and telecom operators face explicit privileged-access clauses within national security legislation. The UK Telecommunications Security Act obliges carriers to implement privileged session controls before 2024 network upgrades, reinforcing the solution priority. Southern Europe and the Nordics exhibit emerging demand, spurred by government digital-transformation funds and heightened ransomware exposure in healthcare systems.

MEA Privileged Access Management Market

Middle East and Africa display nascent yet accelerating demand, driven by oil-and-gas OT modernisation, sovereign cloud rollouts, and national-level cyber-security strategies. Gulf Cooperation Council banks and utilities increasingly require PAM certification in tender documents, pushing international vendors to establish local data centres and Arabic language support. South Africa and Kenya lead sub-Saharan adoption because of mobile-money ecosystem growth that raises credential-abuse risks.

Competitive Landscape

The privileged access management industry shows moderate consolidation as market leaders acquire adjacent technologies to create end-to-end identity security platforms. The CyberArk portfolio now spans human, machine, and AI identities after buying Venafi for USD 1.54 billion in 2024 and Zilla Security for USD 175 million in 2025. BeyondTrust exceeded USD 400 million annual recurring revenue in 2025 by cross-selling least-privilege features into its endpoint protection base and purchasing Entitle to fortify cloud entitlements. [4]BeyondTrust, “Beyond Momentum,” BEYONDTRUST.COM Delinea broadened capabilities through strategic purchases of Authomize and Fastpath, signalling a pivot toward unified identity threat detection.

Market entrants such as Entitle, P0, and JumpCloud challenge incumbents by focusing on narrow pain points—cloud permissions governance, just-in-time SSH brokering, or zero-infrastructure VPN-less access. Incumbents respond with API-first, micro-services architectures and AI-driven anomaly detection modules. Differentiation shifts from password vaulting to contextual risk scoring, post-quantum readiness, and developer-friendly integration kits.

Pricing models trend toward usage-based subscriptions and managed service bundles, reflecting customer demand for predictable OpEx over CapEx. Vendors that build strong partner ecosystems—in particular, MSSPs and cloud service providers—gain reach into SME segments and regulated verticals that prefer one-stop identity security contracting.

Privileged Access Management Industry Leaders

CyberArk Software Ltd.

BeyondTrust Corporation

Delinea Inc.

One Identity LLC

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Privileged Access Management Market Companies Covered in this Report

- CyberArk Software Ltd.

- BeyondTrust Corporation

- Delinea Inc.

- One Identity LLC

- IBM Corporation

- Broadcom Inc.

- ARCON TechSolutions Pvt. Ltd.

- WALLIX Group SA

- Micro Focus International plc

- ManageEngine – Zoho Corporation Pvt. Ltd.

- Hitachi ID Systems Inc.

- Senhasegura – MT4 Tecnologia Ltda.

- Keeper Security Inc.

- Thales Group (Gemalto NV)

- Fudo Security Sp. z o.o.

- Ekran System Inc.

- Saviynt Inc.

- Ericom Software Ltd.

- Quest Software Inc.

- Bravura Security Inc.

Recent Industry Developments in Privileged Access Management Market

- July 2025: CyberArk introduced expanded controls for AI and machine identities, broadening its platform reach beyond traditional human administrator accounts.

- June 2025: BeyondTrust surpassed USD 400 million ARR and acquired Entitle to deepen cloud permissions automation.

- May 2025: JumpCloud acquired VaultOne, embedding PAM and secure browsing to eliminate VPN complexity.

- April 2025: CyberArk completed the USD 175 million purchase of Zilla Security, integrating AI-assisted access reviews into its identity platform.

- March 2025: Delinea closed deals for Authomize and Fastpath, accelerating its move toward consolidated identity security.

- February 2025: BeyondTrust appointed Janine Seebeck as CEO, reinforcing a strategy that pivots from traditional PAM to broader identity threat detection.

- December 2024: ARCON integrated its PAM platform with Oracle Access Governance, underscoring ecosystem openness.

Global Privileged Access Management Market Report Scope

Segmentation Overview

| Solutions |

| Services |

| On-premises |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| IT and Telecom |

| Government and Public Sector |

| Healthcare |

| Retail and E-commerce |

| Manufacturing |

| Energy and Utilities |

| Other End-user Industries |

| Shared/Privileged Account Management |

| Application to Application Password Management (AAPM) |

| Endpoint Privilege Management (EPM) |

| Cloud and SaaS Privilege Management |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | On-premises | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Government and Public Sector | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Other End-user Industries | |||

| By Type of Access Control | Shared/Privileged Account Management | ||

| Application to Application Password Management (AAPM) | |||

| Endpoint Privilege Management (EPM) | |||

| Cloud and SaaS Privilege Management | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the privileged access management market?

The privileged access management market is expanding because machine identities now outnumber human identities by 40:1, insurers require PAM for cyber-risk coverage, and zero-trust mandates demand continuous session isolation.

How large is the privileged access management market today and what is its expected size by 2031?

The privileged access management market size reached USD 5.17 billion in 2026 and is projected to hit USD 13.83 billion by 2031, reflecting a 21.72% CAGR.

Which segment is growing the fastest within the privileged access management market?

Cloud and SaaS privilege management is the fastest-growing segment at 23.90% CAGR because enterprises need granular entitlement control across multi-cloud estates.

Why are small and medium enterprises adopting PAM solutions at higher rates?

SMEs face cyber-insurance underwriting rules that make PAM a prerequisite for policy approval, and cloud-delivered PAM services align with their budget and staffing constraints

Which region is expected to lead growth through 2031?

Asia-Pacific is forecast to record the highest 23.60% CAGR, bolstered by regulatory mandates in Singapore and accelerated digitisation in Japan, India, and China.

How are vendors preparing for post-quantum threats?

Vendors are integrating quantum-resistant algorithms into credential vaults and blocking unsanctioned ciphers, as illustrated by Palo Alto Networks’ 2024 update.

Page last updated on: