Shale Shakers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shale Shakers Market Analysis by Mordor Intelligence

The Shale Shakers Market size is projected to be USD 2.19 billion in 2025, USD 2.32 billion in 2026, and reach USD 3.01 billion by 2031, growing at a CAGR of 5.36% from 2026 to 2031. Measured growth sits on top of a structural change in solids-control economics. Operators are consolidating multi-stage separation into high-capacity units that handle a 40% productivity gain in North American shale drilling. This shift enables producers to sustain output with 518 rigs while Haynesville gas-directed activity has reached 64 rigs in early 2026, the highest since 2022. Triple-deck configurations that replace three machines now cut waste volumes by up to 80% in Midland and Piceance field trials. Regulatory pressure under OSPAR conventions and Colorado Rule 423 is accelerating the move toward electrically driven, variable-frequency-drive (VFD) systems that deliver 20% power savings and a quieter deck.

Key Report Takeaways

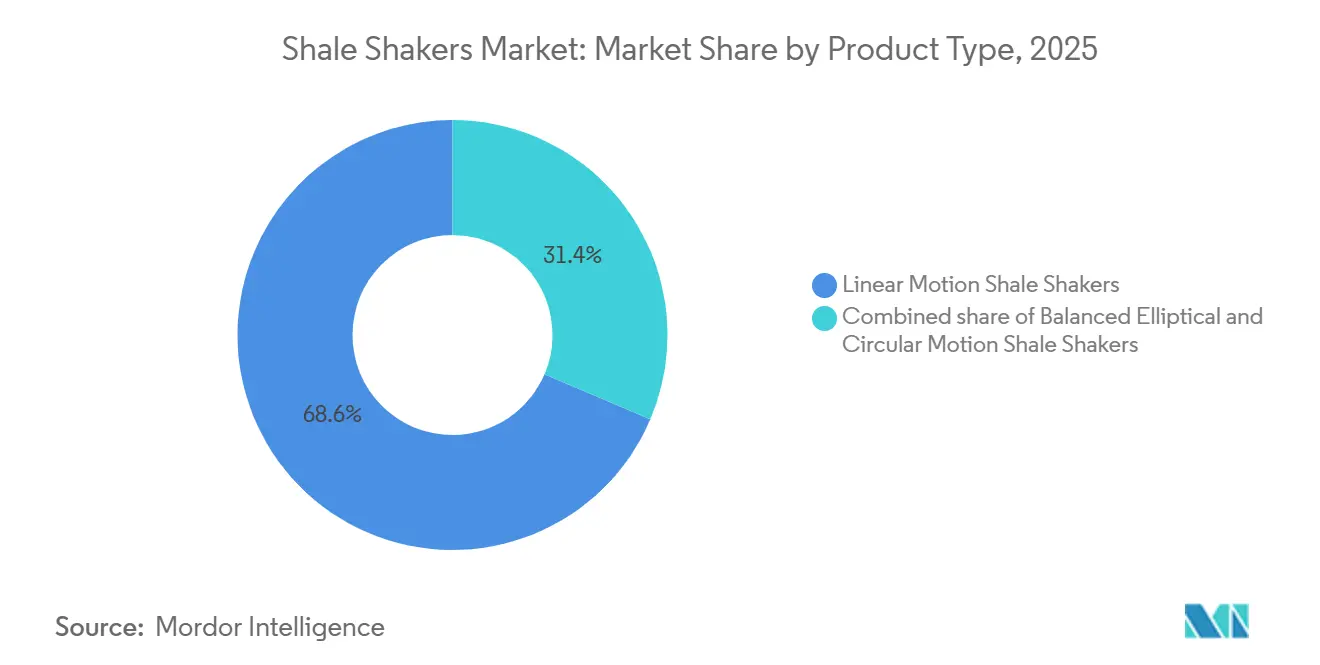

- By product type, linear-motion units led with 68.6% revenue share in 2025, while balanced elliptical motion is projected to register a 5.6% CAGR through 2031.

- By technology, single-deck units accounted for 54.2% of installations in 2025; triple-deck systems are forecast to expand at a 6.3% CAGR to 2031.

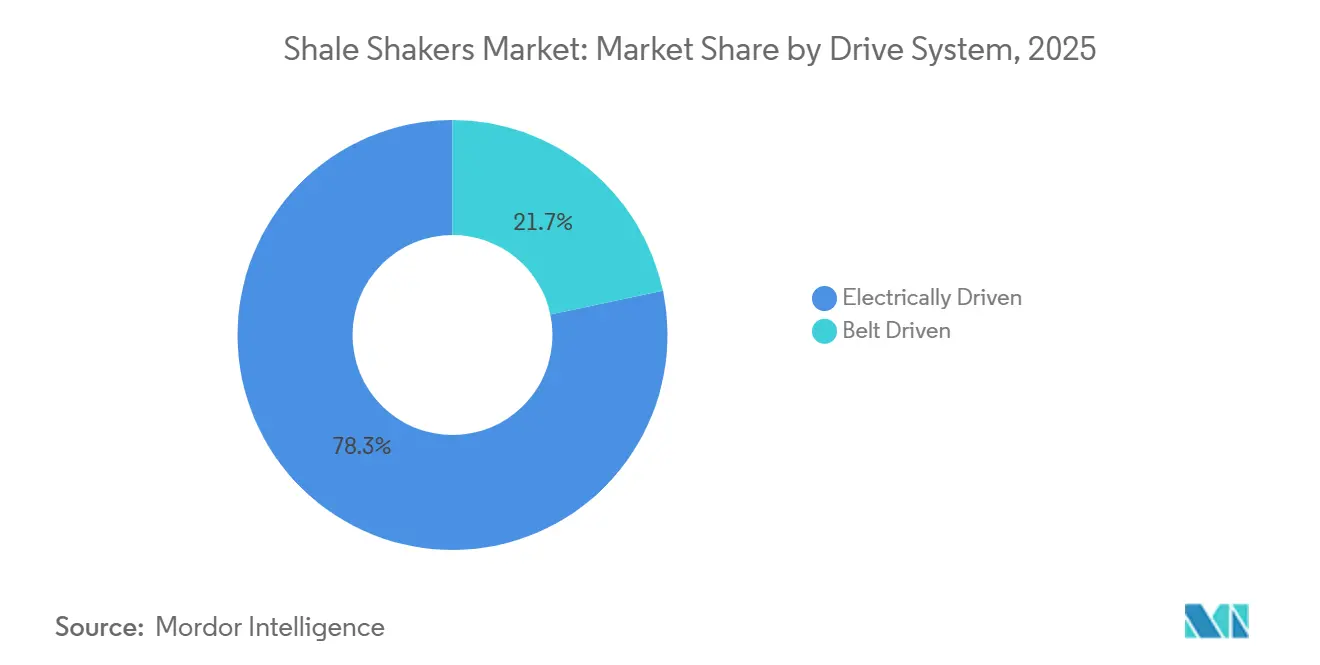

- By drive system, electrically driven configurations captured 78.3% of 2025 installations and are advancing at a 5.8% CAGR through 2031.

- By installation, newly installed captured 65.5% of 2025 installations and are advancing at a 6.0% CAGR through 2031.

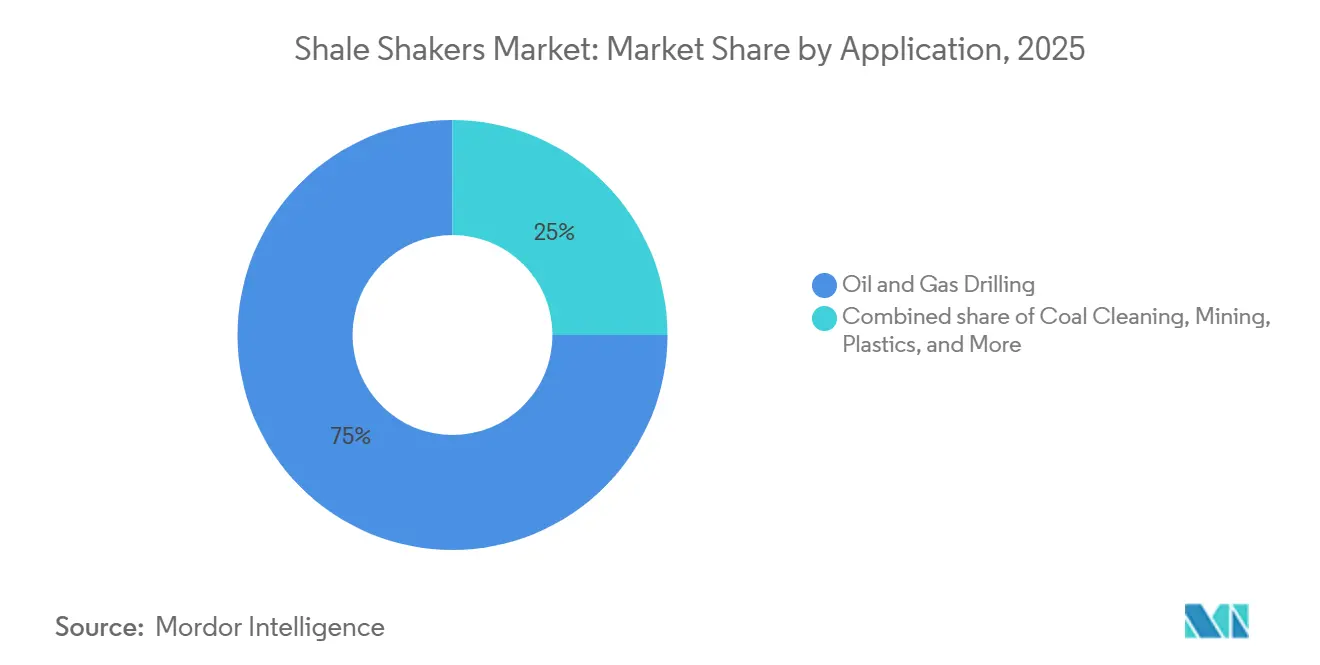

- By application, oil and gas drilling held 75.0% of 2025 revenue and is growing at a 6.1% CAGR, outpacing coal cleaning and mining.

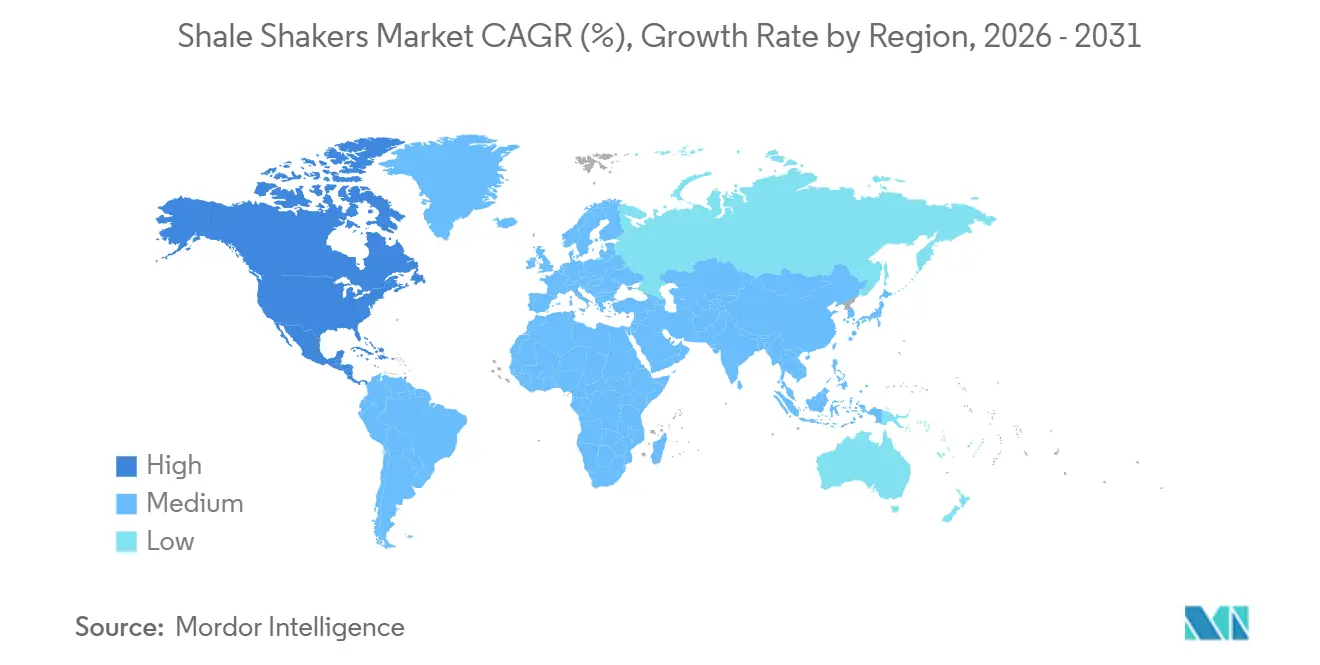

- By geography, North America commanded 40.1% revenue share in 2025; the area is expected to post the fastest 6.2% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Shale Shakers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging horizontal and directional shale drilling activity | +1.5% | North America, with spillover to Middle East unconventional plays and Argentina Vaca Muerta | Medium term (2-4 years) |

| Rising offshore ultra-deepwater wells with high-G mud programs | +0.8% | Global, concentrated in Gulf of Mexico, Brazil pre-salt, West Africa, and Abu Dhabi offshore fields | Long term (≥ 4 years) |

| Stringent cuttings-discharge regulations (e.g., North Sea OSPAR) | +1.2% | Europe (North Sea), North America (Colorado, Alberta), Asia-Pacific coastal zones | Short term (≤ 2 years) |

| Rig digital-twin adoption enabling predictive shaker maintenance | +0.6% | North America and Middle East, with early uptake in Canada and UAE | Medium term (2-4 years) |

| Adoption of autonomous g-force control to optimize ROP | +0.4% | North America shale plays, expanding to Middle East high-specification rigs | Medium term (2-4 years) |

| Lithium-rich geothermal wells requiring ultra-fine cuttings control | +0.3% | North America (Nevada, California), with potential expansion to Chile and Argentina lithium triangle | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Horizontal and Directional Shale Drilling Activity

Haynesville gas-directed drilling touched 64 rigs in February 2026 as LNG export expansions and data-center power demand boosted gas targets by 1.2 billion cubic feet per day for 2026 and 1.6 billion cubic feet per day for 2027 [1]U.S. Energy Information Administration, “Drilling Productivity Report,” eia.gov. Each horizontal well generates up to 2,000 barrels of drilling fluid that must pass across shale shakers before reuse. Longer laterals averaging 10,000-12,000 feet raise solids loading by 40%, forcing operators to shift from single-deck to triple-deck equipment to maintain 800 gallons-per-minute circulation. U.S. pad-drilling expertise is migrating to Argentina’s Vaca Muerta and Saudi Arabia’s Jafurah, where portable high-throughput decks process 28 liters per second at 7.5 G-force. Autonomous g-force control that modulates vibration amplitude based on downhole telemetry is reducing screen blinding by 20% and extending mesh life to 55 hours, lowering consumable cost by USD 8,000 per well. The confluence of higher well counts, longer laterals, and automation adds 1.5 % to the CAGR.

Rising Offshore Ultra-Deepwater Wells With High-G Mud Programs

Chevron’s Anchor project came on-stream in 2024 at 20,000 psi wellhead pressure, relying on synthetic-based muds that impose 6.5 G loads on decks [2]Chevron Corporation, “Anchor Field Fact Sheet,” chevron.com. Conventional linear-motion units struggle to remove sub-10-micron barite without losing fluid, prompting uptake of balanced elliptical shakers that safeguard 200-mesh screens while achieving 80% solids removal. ADNOC Drilling ordered two jack-up rigs and three island rigs in 2025, all specified with AI-enabled triple-deck shakers designed for 18-pound-per-gallon mud. Arabian Drilling reactivated three rigs the same year, each fitted with triple-deck units to handle high-pressure reservoirs. Growing deepwater campaigns in Brazil and West Africa will translate this practice globally, contributing 0.8 % to long-term growth.

Stringent Cuttings-Discharge Regulations

OSPAR Decision 2000/3 bans the discharge of oil-contaminated cuttings in the North Sea, compelling zero-discharge shaker cascades that achieve residual oil below 1% by weight [3]OSPAR Commission, “OSPAR Decision 2000/3,” ospar.org. Enhanced Drilling’s closed-loop platform, deployed on Norwegian rigs, integrates vacuum dewatering to meet the rule. Colorado Rule 423, effective 2024, caps nighttime noise at 50 dBA within 2,000 feet of homes; electrically driven shakers with acoustic enclosures meet the standard at an added USD 25,000 per unit [4]Colorado Oil and Gas Conservation Commission, “Rule 423 Noise Requirements,” cogcc.state.co.us. Alberta Directive 038 mandates continuous sound monitoring inside 1.5 kilometers of residences, accelerating retrofits of belt-driven units with VFD motors that operate 10 decibels quieter. Such mandates add 1.2 % to forecast growth as operators pre-empt compliance risk.

Rig Digital-Twin Adoption Enabling Predictive Shaker Maintenance

Precision Drilling implemented digital twins fleet-wide in 2025, using sensor streams on vibration amplitude, motor current, and differential pressure to forecast bearing failure 72 hours in advance. The program cut unplanned downtime by 30% and lifted bearing life to 1,600 hours. Schlumberger’s DELFI environment lets remote engineers fine-tune G-force and mesh size without on-site staff. ADNOC’s island rigs require AI-enabled solids control, reflecting regional appetite for 10% price premiums when predictive maintenance shrinks non-productive time. The digital-twin vector delivers 0.6 % of CAGR gain, with the greatest effect in the next four years as WITSML 2.1 data standards improve cross-vendor integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility curbing new rig CAPEX | -0.9% | Global, most acute in North America shale plays and price-sensitive independents | Short term (≤ 2 years) |

| High ownership cost vs. shaker-less vacuum filtration alternatives | -0.5% | North America and Europe, limited adoption in Asia-Pacific due to capital constraints | Medium term (2-4 years) |

| API compliant mesh supply bottlenecks due to rare-earth alloys | -0.3% | Global, with acute pressure in North America and Middle East high-specification applications | Short term (≤ 2 years) |

| ESG scrutiny on vibration-induced deck noise at well sites | -0.2% | North America (Colorado, Alberta, British Columbia), Europe (North Sea), expanding to urban drilling zones globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Curbing New Rig CAPEX

West Texas Intermediate averaged USD 62 per barrel in early 2026, prompting North American independents to trim drilling budgets and rely on 40% productivity gains to meet output targets. Fewer greenfield rigs translate to lower demand for newly installed shakers, even though retrofit work partially offsets the dip. Operators defer purchases until sustained prices climb above USD 70, creating a 0.9 percentage-point drag on CAGR through 2028.

High Ownership Cost Versus Shaker-Less Vacuum Filtration Alternatives

Vacuum systems eliminate screens and cut noise by 20 decibels, attractive in urban settings, yet they cost USD 600,000 versus USD 250,000 for a triple-deck shaker and sacrifice 30% liquid recovery. Hybrid approaches that pair shakers for bulk removal with vacuum stages for polishing are gaining ground, limiting wholesale substitution but still subtracting 0.5 % from forecast growth in capital-constrained North American and European plays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Linear Motion Maintains Throughput Leadership

Linear-motion designs generated 68.6% of 2025 revenue and will grow at 5.6% annually through 2031. The segment benefits from aggressive unidirectional vibration of 0.25 inches at up to 4 G that propels sticky Haynesville gumbo across the screen. Field trials showed that NOV's Brandt Alpha line delivered 37% waste reduction and saved USD 45,000 per pad in the Midland Basin. Balanced elliptical motion is favored offshore to protect fine screens against 6.5 G mud programs. Circular designs persist in coal cleaning where simplicity matters.

The shale shakers market for linear-motion units is projected to grow steadily through 2031, driven by their extensive use in conventional drilling and high-volume solids control operations. The introduction of autonomous G-force control systems is increasing screen life from approximately 40 hours to around 55 hours, enabling operators to lower consumable costs by nearly USD 8,000 per well. Adherence to API RP 13C standards at D100 cut points of 75–150 microns continues to enhance procurement preferences in Middle Eastern drilling projects, solidifying the segment's strong role in overall shale shaker demand.

By Technology: Triple-Deck Adoption Replaces Multi-Stage Trains

Single-deck units remained most numerous in 2025, with 54.2% installs due to low upfront cost. Triple-deck platforms, however, post the fastest 6.3% CAGR because they integrate coarse, intermediate, and fine screening inside one frame, erasing the need for separate desanders and desilters.Brightway's design trims footprint by 40% and halves rig-up time.

Triple-deck shale shaker systems are projected to experience significant growth through 2031, driven by operators' focus on adhering to stringent North Sea zero-discharge regulations, which mandate residual oil content below 1%. The integration of digital-twin sensors across multiple decks enhances operational data collection, facilitating machine-learning-based predictions of bearing wear and improving overall equipment uptime. While single-deck units remain prevalent in coal and mining applications, triple-deck configurations are increasingly favored for high-specification drilling rigs in North America.

By Drive System: Electric VFD Establishes Dominance

Electrically powered shakers equipped with VFDs held 78.3% of 2025 installs and will rise at a 5.8% CAGR. Real-time speed control swings G-force from 3.5 to 7.5 without shaft changes, cutting diesel use by 6 gallons per hour on land rigs. Permanent-magnet AC motors improve efficiency by 5% in 120°F Abu Dhabi conditions.

Electric-drive shale shakers are increasingly being adopted as operators focus on reducing noise emissions, enhancing energy efficiency, and lowering maintenance needs. Regulatory standards, including Alberta Directive 038 and Colorado Rule 423, are driving the adoption of variable frequency drive (VFD)-equipped systems, which operate approximately 10 decibels quieter than traditional belt-driven units. However, belt-driven shale shakers remain in use for specific offshore applications, where their straightforward mechanical design provides better resistance to salt-spray corrosion and reduces the likelihood of power-electronics failures.

By Installation: Newbuild Preference Amid Fleet Modernization

Newly installed equipment accounted for 65.5% of 2025 demand and should advance at 6.0% yearly as Middle Eastern national oil companies invest in high-spec rigs. ADNOC’s USD 1.15 billion jack-up order specifies turnkey triple-deck shakers bundled with three-year maintenance.

Retrofitted units still form 34.5% of volume and give operators a hedge when WTI prices linger near USD 62. A USD 150,000 upgrade that swaps single-deck for dual-deck hardware supplies 40% extra throughput and elongates rig life by seven years. Digital-twin analytics help target retrofits during scheduled downtime, trimming non-productive hours by 25%.

By Application: Oil and Gas Drilling Commands Premium Demand

Oil and gas drilling generated 75% of 2025 revenue and is forecast to grow at 6.1% through 2031. Ultra-deepwater projects such as Chevron’s Anchor require balanced elliptical units with 200-mesh screens to manage 20,000 psi wells. Onshore, each Haynesville horizontal well sends up to 2,000 barrels of fluid through shakers before reuse.

Coal cleaning and mining applications are experiencing relatively slower growth. However, Chinese OEMs continue to supply low-cost, API-compliant shakers for large-scale coal washing operations. In contrast, niche geothermal-lithium projects in Nevada and California are increasingly utilizing triple-deck shaker designs with D100 cut points below 75 microns to ensure brine purity for ion-exchange lithium extraction. Broader adoption of these technologies could contribute to further growth in the shale shakers market.

Geography Analysis

North America controlled 40.1% of the shale shakers market revenue in 2025 and is projected to grow at 6.2% annually to 2031. Haynesville rig counts rose to 64 by February 2026, and Permian totals held near 255 even during price softness. Comstock Resources plans 43 Haynesville wells in 2026, each specifying high-throughput triple-deck units. Tightening Colorado and Alberta noise codes are driving VFD retrofits that align with digital-twin uptime programs at Precision Drilling, reducing downtime by 30%.

The Middle East shows the strongest spending momentum. ADNOC placed more than USD 1.9 billion in rig orders during 2025 that mandate AI-enabled solids control, while Saudi operators keep capacity at 13 million barrels per day. Triple-deck shakers with PMAC motors and API RP 13C mesh are now standard in new Saudi and UAE fleets. Europe’s North Sea, constrained by OSPAR zero-discharge rules, adopts closed-loop systems with vacuum dewatering; residual oil levels under 1% are now routine on Norwegian Continental Shelf wells.

Asia-Pacific’s growth is steadier. Chinese coal washing maintains demand for cost-focused shakers from GN Solids Control, yet national renewable targets temper long-term volumes. India’s deeper Krishna-Godavari wells require higher throughput, but overall rig counts keep the region at one-third the North American size. South America, led by Brazil's pre-salt and Argentina's shale, is adopting North American pad-drilling methods that rely on portable equipment rated 28 liters per second at 7.5 G, although currency risks delay some orders.

Competitive Landscape

The Shale Shakers Market is semi-consolidated. Derrick’s Hyperpool GT lifted capacity 22% and saved USD 360,000 per pad in the DJ Basin, while NOV’s Alpha reduced waste 37% in Midland operations. Chinese manufacturers GN Solids Control, KOSUN, and Aipu are expanding in Asia-Pacific coal and mining by pricing 25% below Western OEMs with API-compliant mesh.

Technology leadership is the main battleground. Schlumberger’s autonomous G-force algorithm extends screen life to 55 hours, helping justify the 10% premium ADNOC paid for AI-enabled rigs. Enhanced Drilling carved a North Sea niche by integrating vacuum dewatering to meet OSPAR’s 1% oil-on-cuttings ceiling without auxiliary equipment. Smaller firms such as Elgin Separation and KEMTRON target retrofit kits that convert single-deck units to dual decks for one-third the cost of a new triple-deck system, appealing to operators cautious about capital outlay under USD 65 oil.

Digital-service bundles strengthen incumbents. Derrick and NOV offer three-year maintenance with predictive analytics, while Schlumberger ties shaker telemetry into its DELFI cloud to optimize downhole rate of penetration. Cost-focused challengers counter with rapid delivery and localized support. Lithium-rich geothermal wells in Nevada create a white space that none fully own; capturing that niche will depend on achieving sub-75-micron D100 cut points without screen loss, an area where the next technology leap is expected.

Shale Shakers Industry Leaders

Derrick Equipment Company

NOV – BRANDT (National Oilwell Varco)

Schlumberger NV

Halliburton Company

GN Solids Control

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Baker Hughes introduced the Kantori™ autonomous well construction solution, which incorporates AI, real-time analytics, and automated drilling workflows. Although not a shale shaker product, this platform facilitates the digitalization of drilling operations, driving demand for connected solids-control equipment.

- December 2024: Major Drilling USA demonstrated new robotic rod handler and drill analytics technology to senior mining executives, showcasing automation capabilities that could influence drilling equipment design requirements, including solids control systems.

- August 2024: Epiroc released the Simba SM60 S production drilling rig featuring breakthrough technology for smaller drift applications, incorporating advanced rod handling systems that save over 20 seconds per rod compared to previous models.

- July 2024: Caterpillar, Thiess, and WesTrac celebrated a milestone with three fully autonomous surface drills surpassing 1 million meters drilled at Mt. Arthur South coal mine, demonstrating the viability of autonomous drilling operations that influence equipment design requirements, including solids control systems.

Global Shale Shakers Market Report Scope

Shale shakers are essential equipment in drilling operations, utilizing vibrating screens to separate solid cuttings from drilling mud. This process ensures fluid quality, enhances drilling efficiency, minimizes waste, and reduces operational costs by allowing the reuse of drilling fluids.

The global shale shakers market is segmented by product type, technology, drive system, installation, application, and geography. By product type, the market is segmented into linear motion, balanced elliptical motion, and circular motion shale shakers. By technology, the market is segmented into single-deck, double-deck, and triple-deck systems. By drive system, the market is segmented into electrically driven and belt-driven shale shakers. By installation, the market is segmented into newly installed and retrofitted units. By application, the market is segmented into coal cleaning, oil and gas drilling, mining, chemical and petrochemical, plastics, and other industrial applications. The report also covers market size and forecasts for the global shale shakers market across major countries in key regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, market sizing and forecasts have been provided based on value (USD).

| Linear Motion Shale Shakers |

| Balanced Elliptical Motion Shale Shakers |

| Circular Motion Shale Shakers |

| Single Deck |

| Double Deck |

| Triple Deck |

| Electrically Driven |

| Belt Driven |

| Newly Installed |

| Retrofitted |

| Coal Cleaning |

| Oil and Gas Drilling |

| Mining |

| Chemical and Petrochemical |

| Plastics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Linear Motion Shale Shakers | |

| Balanced Elliptical Motion Shale Shakers | ||

| Circular Motion Shale Shakers | ||

| By Technology | Single Deck | |

| Double Deck | ||

| Triple Deck | ||

| By Drive System | Electrically Driven | |

| Belt Driven | ||

| By Installation | Newly Installed | |

| Retrofitted | ||

| By Application | Coal Cleaning | |

| Oil and Gas Drilling | ||

| Mining | ||

| Chemical and Petrochemical | ||

| Plastics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the shale shakers market?

The shale shakers market size stands at USD 2.32 billion in 2026 and is projected to reach USD 3.01 billion by 2031.

How fast is demand for shale shakers expected to grow?

Global revenue is forecast to rise at a 5.36% CAGR between 2026 and 2031, driven by higher-spec horizontal and deepwater drilling.

Which product type holds the largest share?

Linear-motion shakers led with 68.6% of 2025 revenue and continue to dominate sticky-solids handling.

Why are triple-deck shakers gaining popularity?

Triple-deck systems consolidate coarse, intermediate, and fine screening in one frame, cutting footprint 40% and meeting zero-discharge rules.

What regions are expanding fastest?

North America posts the highest 6.2% CAGR thanks to Haynesville gas drilling and stringent noise regulations that favor VFD retrofits.

Page last updated on: