Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.14 Billion |

| Market Size (2031) | USD 30.12 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Induction Motor Market Analysis by Mordor Intelligence

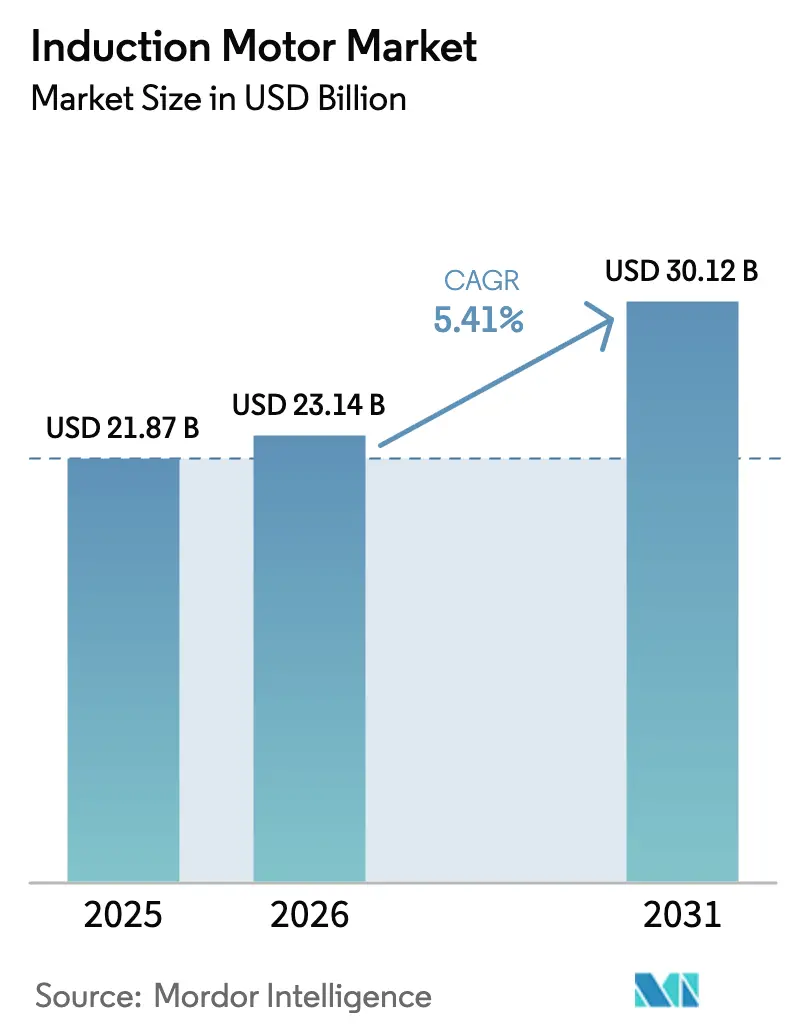

The Induction Motor Market size is expected to increase from USD 21.87 billion in 2025 to USD 23.14 billion in 2026 and reach USD 30.12 billion by 2031, growing at a CAGR of 5.41% over 2026-2031.

Demand is shaped by energy-efficiency mandates across major economies, accelerating adoption of variable frequency drives in pumps, fans, and compressors, and a gradual pivot to magnet-free designs that sidestep rare-earth risk. Competitive strategies focus on IE4 and IE5 portfolios, digital service layers, and inverter-duty enhancements that close the gap with premium-magnet machines at lower lifecycle cost. Data-center cooling, water and wastewater infrastructure, and semiconductor fab construction provide a steady pull for three-phase, VFD-paired systems that deliver energy savings at part load. The Asia-Pacific region remains the core manufacturing and consumption base, with an improving PMI profile and continued fab starts that sustain new installations and retrofits.[1]U.S. Department of Energy, “Energy Conservation Standards for Fans and Blowers,” Federal Register.

Key Report Takeaways

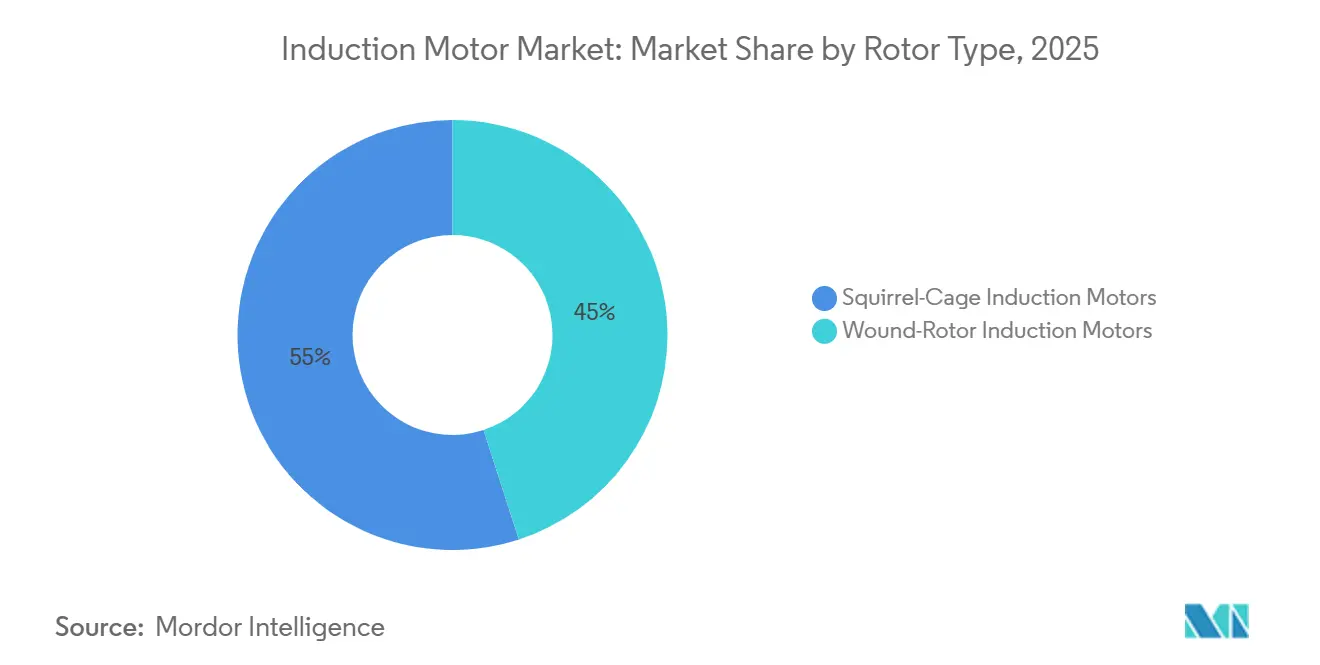

- By rotor type, squirrel-cage induction motors led with 55% revenue share in 2025 and are projected to expand at a 7.34% CAGR through 2031.

- By phase, single-phase held a 53% share in 2025, while the three-phase segment is forecast to grow at a 6.76% CAGR through 2031.

- By efficiency class, IE2 accounted for a 61.32% share in 2025, while IE4 is expected to grow at a 5.71% CAGR through 2031.

- By application, pumps accounted for a 35.67% share of the induction motors market size in 2025, and compressors recorded the highest projected CAGR at 7.32% through 2031.

- By end-user industry, manufacturing accounted for 68.02% of the base in 2025, while commercial buildings are projected to expand at an 8.50% CAGR through 2031.

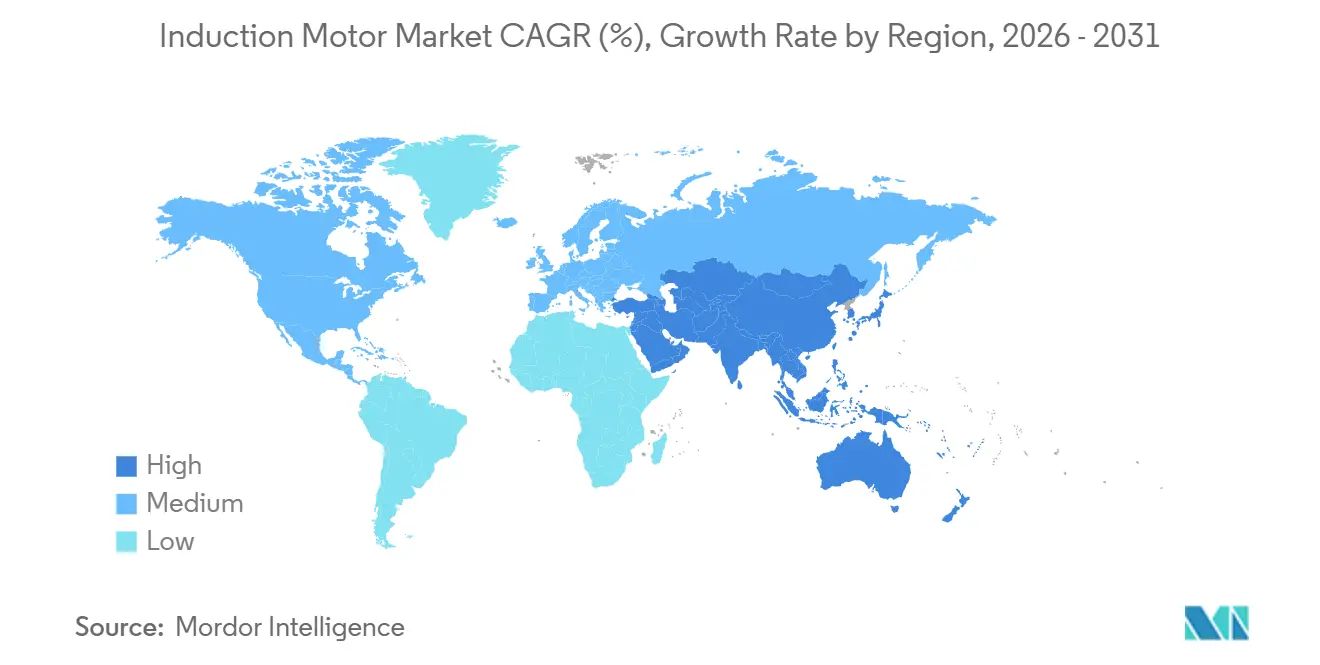

- By geography, the Asia-Pacific region captured 62% of the induction motors market share in 2025 and is projected to advance at a 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Induction Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Energy-Efficient Motor Standards | +1.8% | Global, strong in EU, China, United States | Short term (≤ 2 years) |

| Acceleration of Industrial Automation and Process Optimization Programs | +2.1% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of Water and Wastewater Infrastructure | +1.5% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Manufacturing Capacity Additions and Supply Chain Reconfiguration | +1.3% | Asia-Pacific, nearshoring to Mexico | Medium term (2-4 years) |

| Magnet-Free Design Preference in High-Power Drives | +0.7% | Global, strong in EU, United States, Japan | Long term (≥ 4 years) |

| Advances in Copper-Rotor and Inverter-Duty Designs | +0.4% | Global, premium-tier in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Energy-Efficient Motor Standards in Industrial Systems

Industrial motor systems account for a significant share of electricity use, making energy-efficiency policies the single strongest lever for performance upgrades and retrofit cycles. The European Union’s Ecodesign framework set IE4 as the minimum for 75–200 kW three-phase motors from mid-2023. Meanwhile, the United States finalized fan and blower standards in January 2024, which promote variable speed and high-efficiency motor-drive pairings across commercial and industrial air systems. China’s GB 18613-2020 has moved the baseline to IE3 for motors with a capacity of 0.75–375 kW, narrowing regional gaps and creating a scale for premium-efficiency designs. UN-led model regulations, published in 2025, provide a template for countries to accelerate adoption, with differentiated pathways for markets at varying levels of enforcement readiness. These rules shift purchase criteria toward lifecycle performance, which supports upgrades to IE3 and IE4 motors and broader deployment of VFDs in pumps and fans. Harmonized test protocols from IEC and national bodies reduce technical ambiguity and help the induction motors market capture savings from standardized compliance. [2]International Energy Agency, “Energy Efficiency 2025,” IEA, iea.org.

Acceleration of Industrial Automation and Process Optimization Programs

Factory modernization and digital operations are increasing demand for integrated motor-drive packages that operate efficiently at variable load. Variable frequency drives reduce energy consumption in variable torque applications and are central to modernization programs in HVAC, water pumping, and materials handling. Design standards for fans and blowers in the United States embed variable speed as a pathway to compliance, which filters through to motor selection and control strategies in new and retrofit projects. OEMs have updated drive platforms to support higher axis counts, tighter safety functions, and simpler integration, which lowers total cost of ownership for large-scale automation deployments. When paired with three-phase induction motors, drives improve part-load efficiency and reduce mechanical stress, extending service life in high-duty cycles. These dynamics continue to support the induction motors market as industrial users prioritize energy and uptime gains.

Expansion of Water and Wastewater Infrastructure Requiring Pumping Capacity

Urbanization and water security programs are driving large centrifugal-pump installations that rely on three-phase motors and speed control. Desalination strategies in the Middle East are shifting toward reverse osmosis, which lowers specific energy consumption and encourages rightsizing of motor-drive systems. Energy recovery devices in modern plants further optimize pump duty points, yet total motor capacity still rises as output scales. Utilities and industrial users also pursue ISO 50001-aligned savings and reliability targets, which align with premium-efficiency motors and VFDs in new and retrofit pumping stations. In Asia-Pacific, municipal treatment and irrigation systems contribute to sustained demand for robust, standards-compliant motor platforms. These project pipelines reinforce the induction motors market for medium-voltage and low-voltage systems tied to critical water infrastructure.

Manufacturing Capacity Additions in Asia-Pacific and Supply Chain Reconfiguration

Semiconductor fab construction plans indicate new cleanroom HVAC, process pump, and handling-system demand that depends on reliable induction motors paired with precision drives. Asia-Pacific accounts for most planned fab starts in the current cycle, while nearshoring creates incremental motor demand in Mexico and the broader North America supply chain. Automotive assembly and electrification investments across Southeast Asia add multi-decade conveyor and paint-shop motor requirements anchored to high-uptime duty. Large greenfield plants for EVs and batteries rely on standardized three-phase motor families that simplify maintenance across lines. These shifts concentrate procurement cycles and after-sales opportunities for OEMs able to deliver IE3 and IE4 performance at scale. As these factories come online, the induction motors market benefits from broader installed bases in both continuous process and discrete manufacturing.

Magnet-Free Design Preference Amid Rare-Earth Supply Risk in High-Power Drives

Policy and supply chain uncertainty around rare-earth magnets are reinforcing interest in magnet-free designs for efficiency upgrades and new installations. Synchronous reluctance motors provide high efficiency without neodymium or dysprosium and achieve strong loss reductions compared with IE3 induction motors when controlled by matched drives. Industrial users value the combination of premium performance and insulation from rare-earth sourcing volatility, which supports magnet-free portfolios in medium-power ranges. OEMs have introduced IE5 and IE6 roadmaps using reluctance-based designs to future-proof compliance without frame-size compromises. In heavy-duty pumps and fans, inverter-duty induction motors with copper rotors narrow the efficiency gap while retaining robustness and simplicity in the installed base. These choices sustain the induction motors market through product strategies that prioritize material risk management and lifecycle performance.

Advances in Cast-Copper Rotor and Inverter-Duty Designs Improving Efficiency

Copper-rotor technology reduces rotor losses and helps induction motors approach IE4 targets while preserving familiar installation practices. Inverter-duty windings, improved insulation, and bearings designed for variable speed extend reliability under PWM waveforms and high switching frequencies. Standardization of drive-motor efficiency measurement enables users to compare combined system performance and justify upgrades against energy and maintenance savings. Product platforms now cover common frame sizes with factory-rated constant torque and variable torque ranges, which eases retrofit planning in pumps and fans. High-quality laminations and optimized slot designs reduce core losses and temperature rise, allowing compact frames that meet new efficiency thresholds. These engineering gains underpin the induction motors market as industrial customers align compliance and cost objectives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Permanent-Magnet and Synchronous-Reluctance Alternatives | -0.8% | Global, strongest in premium automotive and robotics | Short term (≤ 2 years) |

| Upfront Price Premium of Premium-Efficiency Motors and VFD Retrofits | -0.6% | Price-sensitive regions across Asia and Latin America | Short term (≤ 2 years) |

| Volatility in Copper and Aluminum Prices | -0.6% | Global, more acute in EU and North America | Short term (≤ 2 years) |

| EC Fan Adoption in Buildings | -0.3% | North America and Europe commercial-residential HVAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Permanent-Magnet and Synchronous-Reluctance Motor Alternatives

Permanent-magnet machines hold an efficiency edge in many duty cycles, and recent rules for fans and blowers acknowledge electronically commutated designs as the top-tier benchmark in air-moving equipment. Synchronous reluctance motors achieve IE5-class performance without magnets and are being positioned as lower-risk, high-efficiency options when paired with matched drives. These alternatives can divert premium-efficiency demand in segments that prioritize peak performance and compact form factors. That said, they require variable speed control and cannot operate direct-on-line, which preserves the role of induction motors in fixed-speed and rugged environments. Magnet supply concentration and price swings remain a concern for permanent-magnet designs, which keeps magnet-free approaches attractive on total cost and risk grounds. OEM roadmaps and product launches reflect this balance as companies hedge portfolios across induction, SynRM, and PM lines to meet diverse user needs.

Volatility in Copper and Aluminum Prices Pressuring Motor BOM Costs

Copper and aluminum input costs surged sharply in late 2025, posing a challenge to pass-through strategies and bidding discipline for motor suppliers. Higher copper prices increase winding and rotor-bar costs, while aluminum volatility affects die-cast rotors and housings. Some manufacturers are responding by integrating vertically in wire and component supply to stabilize availability and margin structure. Portfolio optimization efforts that prioritize higher-margin motors and generators also help mitigate the impact of commodity price fluctuations. In markets with low electricity tariffs, longer payback periods can slow upgrade decisions for IE4-class induction motors and drive retrofits. These headwinds can compress margins for mid-tier suppliers that lack hedging programs, underscoring the need for effective cost control and supply chain resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rotor Type: Squirrel-Cage Dominance Reinforced by Reliability and Inverter-Duty Evolution

Squirrel-cage induction motors held 55% of the induction motors market share in 2025 and are forecast to grow at a 7.34% CAGR through 2031. This leadership rests on brushless rotor construction, robust die-cast bars and end rings, and low maintenance in harsh duty cycles. As compliance moved to IE3 and IE4 across regions, inverter-duty induction motors with optimized windings, bearings, and insulation became a standard pairing with modern drives. Copper-rotor variants have reduced rotor losses, enabling efficiency gains without rare-earth magnets, supporting adoption in premium tiers. IEC test and efficiency classification frameworks provide comparative benchmarks across sinusoidal and VFD-fed conditions, helping procurement teams evaluate lifecycle savings. The induction motors market continues to see specification preferences for rugged squirrel-cage designs in pumps, fans, conveyors, and general-purpose drives in industry.

Wound-rotor designs remain in niche roles that require external rotor resistance for precise torque profiles, including large hoists and slurry pumps. VFD-driven squirrel-cage alternatives have displaced wound-rotor options in many cases by offering dynamic control without brushes or slip rings. This shift reduces maintenance and extends service life, which influences long-term cost decisions for operators. As OEMs extend copper-rotor availability to larger frames, the installed base will shift toward more efficient induction platforms at similar footprint. IE3 and IE4 rules for previously exempt motor categories, such as brake motors and explosion-proof units, are pulling the rest of the base toward premium tiers. These technical and regulatory trends support share stability for squirrel-cage configurations in the induction motors market.[3]Oriental Motor Europe, “Overview of Laws, Regulations and Standards in Each Country,” Oriental Motor.

By Phase: Three-Phase Ascendancy Driven by Torque Density and Automation Integration

Single-phase motors held 53% share in 2025, centered in residential and fractional-HP uses, while three-phase motors are forecast to expand at a 6.76% CAGR through 2031. Three-phase machines deliver higher torque density, smoother operation, and better power factor, which makes them the default choice in industrial and commercial installations. Variable speed drives allow precise control of flow and pressure, which unlocks energy savings in variable torque loads like pumps and fans. The move toward premium efficiency standards in both the European Union and China incentivizes three-phase upgrades in commercial HVAC and light industrial settings. In many retrofits, swapping to three-phase motors with VFDs improves part-load performance and reduces mechanical wear. These dynamics reinforce adoption of three-phase architectures in the induction motors market as automation and energy efficiency become core design goals.

Industrial distribution standards favor three-phase power at 400 V, 460 V, or 575 V, which simplifies motor selection for larger loads. Modular product families with multiple pole configurations and frame sizes support drop-in replacements that minimize downtime. Digital nameplates and integrated feedback via single-cable technologies make commissioning faster with modern controls. Predictive monitoring tools built into drives and gateways rely on stable three-phase waveforms for accurate diagnostics, which complements reliability goals. As commercial buildings and factories standardize on three-phase motors with VFDs, operators benefit from unified maintenance practices. The induction motors market reflects these preferences with broader catalog coverage and inverter-duty ratings across common size ranges.

By Efficiency Class: IE4 Super Premium Ascendancy and IE5 Commercial Emergence

IE2 motors accounted for 61.32% share in 2025, reflecting markets at different stages of policy enforcement and update cycles. IE4 motors are forecast to grow at 5.71% CAGR through 2031, supported by rules that require higher minimums in larger kW bands and by fan-blower standards that push system-level efficiency. High-performance induction motors that use cast-copper rotors, premium laminations, and optimized slots reduce losses, and this enables IE4 compliance with familiar form factors. Synchronous reluctance portfolios marketed as IE5 offer significant loss reductions without magnets when paired with matched drives, which supports future-proofing of installations. For motor-drive packages in pumps and fans, system-level measurement is becoming the reference, which drives focus on the combined efficiency curve. These shifts reinforce the induction motors market as a leading pathway to cost-effective compliance in many duty cycles.

IE5-class offerings are expanding via magnet-free designs from leading OEMs, and these catalogs now cover more common frame sizes. While IE5 is not universally mandated, buyers that plan long service lives are beginning to anchor specifications around these levels for key processes. For high duty-factor pumps or fans, the combination of motor and VFD at IE4-or-better performance can bring material energy savings at part load. As testing norms converge, operators gain transparency on payback from motor-only and drive-integrated upgrades. This clarity encourages portfolio optimization even in cost-sensitive regions as electricity tariffs rise or incentive programs scale. These conditions underpin steady upgrades that lift the induction motors market toward higher-efficiency tiers.

By Application: Compressor Growth Outpaces Pumps as HVAC and Industrial Compression Intensify

Pumps retained the largest application share at 35.67% in 2025 within the induction motors market size. Compressors are projected to grow at 7.32% CAGR through 2031, driven by HVAC retrofits, refrigeration chains, and compressed-air system optimization. Variable speed control replaces load-unload cycling and delivers energy savings at the duty points where most systems operate. Fan and blower standards in the United States introduce compliance incentives that tie directly to variable speed and higher motor efficiency. As building codes tighten and data-center cooling grows, designers specify three-phase VFD-paired motors that align airflow to real-time loads. These practices increase the installed base for inverter-duty motors in both new builds and upgrades.

Fans and blowers compose a large third application that benefits from the same system-level improvements. Conveyor and materials handling demand constant torque values and robust construction, which favors induction motors with enhanced bearings and insulation. Commercial HVAC solutions increasingly shift to electronically commutated fans in smaller units, but induction motors remain standard in larger chillers and air handlers. Elevators and cranes remain specialized with high starting torque requirements that induction motors meet with proper control and braking options. Across these applications, lifecycle cost and uptime dominate decisions, which supports premium-efficiency induction platforms. This balance continues to direct volume and design choices in the induction motors market.

By End-User Industry: Manufacturing Supremacy and Commercial Buildings’ Data-Center Surge

Manufacturing held 68.02% of the base in 2025, reflecting heavy reliance on motor-driven systems across process and discrete operations. Commercial buildings are projected to expand at an 8.50% CAGR through 2031 as data-center construction and tight building codes steer upgrades. In factories, the combination of IE3 or IE4 motors with modern drives boosts efficiency and simplifies predictive maintenance programs. In buildings, chillers and air systems are the focus, where variable speed becomes a design norm to meet energy limits. The resulting purchasing decisions favor standard three-phase motors with inverter-duty ratings and premium insulation systems. This pattern strengthens the induction motors market in both industrial and commercial verticals.

Energy-intensive verticals such as petrochemicals, power generation, mining, and metals specify higher protection classes and certifications that lead to long-cycle purchases. Explosion-proof and medium-voltage offerings from leading OEMs align with these requirements and benefit from stricter global standards. Water and wastewater utilities support sustained demand for replacements and expansions that target energy-intensity reductions. Data-center growth adds high-value orders for hermetic motors and precision motion solutions, with OEM capacity investments timed to this trend. Suppliers with strong service capabilities and digital monitoring platforms extend revenue beyond hardware in these end users. These dynamics keep the induction motors industry central to efficiency and reliability programs across sectors.

Geography Analysis

The Asia-Pacific region held a 62% share in 2025 and is projected to grow at a 6.98% CAGR through 2031, as production depth and end-use demand reinforce each other in the region. Fabs, automotive assembly, and export-oriented manufacturing anchor multi-year procurement pipelines for motors and drives. Regional policy alignment with IE3 and above also supports the adoption of premium efficiency in larger frame sizes. Major coastal markets prioritize water treatment and high-efficiency HVAC, resulting in a steady order flow for three-phase, VFD-optimized systems. With more fab projects scheduled through the current cycle, cleanroom HVAC, pumps, and handling systems remain a reliable pull. These factors support the induction motor market as a critical supplier to APAC industrial development.

North America maintains an 18–20% range of global activity as a mature base that emphasizes retrofit quality and lifecycle services. The United States rulemaking for fans and blowers formalizes variable speed as a compliance pathway and strengthens the business case for high-efficiency motors and drives. Nearshoring has increased demand for motors in Mexican plants serving automotive and electronics supply chains. Data-center construction continues to drive orders for high-efficiency HVAC motors and precision systems that operate within strict uptime targets. OEMs invest in U.S. capacity, including new assembly and testing lines that are aligned with advanced HVAC and motion products. These actions strengthen the induction motors market as energy standards and infrastructure investments guide spending priorities.

Europe’s share is 15–17% and is shaped by strict Ecodesign requirements and premium application demand in hazardous areas, offshore, and heavy industry. IE4 mandates in the 75–200 kW range, along with IE3 coverage across broader bands, continue to encourage users to move to higher tiers. OEMs have expanded European capacity for explosion-proof motors that meet IECEx and ATEX certifications. The region’s focus on energy efficiency makes IE4 and integrated drive solutions attractive in pumps and fans. These drivers sustain the induction motors market across EU industries that demand consistent compliance and traceable performance. Investments in regional production and service capabilities support fast turnaround for complex projects.

Competitive Landscape

Global competition exhibits moderate concentration, with established OEMs maintaining a clear presence across premium ranges. ABB reported healthy Motion revenues with orders concentrated in HVAC for commercial buildings, water and wastewater, oil and gas, and rail. WEG's advanced capacity expansions and vertical integration initiatives stabilize key inputs and improve service coverage in Europe and the Americas. Nidec’s medium-term plan focuses on optimizing its portfolio and achieving operating margin goals, which support capital allocation toward generators, industrial motors, and energy systems. Chinese manufacturers have increased IE3-plus output at aggressive price points, which raises competition in cost-sensitive segments. These developments shape pricing, product mix, and service models in the induction motors market.

Strategy execution encompasses capacity investments, mergers and acquisitions, and product roadmap milestones aligned with IE5 and magnet-free platforms. ABB and its peers have expanded SynRM portfolios with IE5-level loss reductions, targeting applications that require high efficiency without the use of magnets. Nidec introduced reluctance-assisted offerings that achieve IE5 benchmarks and are marketed in conjunction with HVAC and compressor solutions. Regal Rexnord secured sizable data-center orders and invested in a new assembly footprint to meet demand for hermetic motors and precision systems. WEG announced investments to expand the production of explosion-proof and high-efficiency motors in Europe, addressing hazardous-area demand. These moves strengthen competitive positioning through technology differentiation and proximity to growth markets.

Competitive dynamics are also shaped by the harmonization of standards and testing, which enables clearer value comparisons and more accurate assessments. As rules emphasize system-level performance, the ability to deliver integrated motor-drive packages with validated curves is a differentiator. Digital condition monitoring and predictive analytics remain a key focus for OEMs seeking to extend their service offerings and ensure uptime. Supply chain resilience actions, including wire manufacturing and regional expansions, aim to stabilize lead times and costs. These transitions reward players with strong engineering depth and global service reach. They also keep the induction motors market aligned with energy, reliability, and digitalization priorities across end users.

Induction Motor Industry Leaders

Siemens AG

Rockwell Automation Inc.

ABB Ltd.

WEG S.A.

Nidec Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Siemens and Nvidia unveiled the Industrial AI Operating System at CES 2026, combining digital twins, IIoT, and AI-driven quality assurance to enable autonomous, adaptive factory operations. Siemens’ Erlangen Electronics Factory is positioned as a flagship for fully AI-driven manufacturing, with embedded motor-condition analytics.

- October 2025: Nidec acquired Chinese scroll-compressor manufacturer Xecom to expand HVAC and refrigeration motor portfolios and to secure vertical integration for heat-pump applications targeting data-center chillers and commercial buildings.

- July 2025: TECO Group acquired EVK Motor to strengthen electric-axle capabilities for commercial vehicles in Europe and North America, and scaled direct-drive systems for buses and trucks with production in India.

- April 2025: Wolong Electric and Zhongchu Guoneng unveiled ChuLong 105, a 105 MW 2-pole high-speed motor for compressed air energy storage systems, achieving 98.8% efficiency and 35-micron vibration metrics.

Global Induction Motor Market Report Scope

An induction motor is an AC electric motor that generates torque through the interaction between a fluctuating magnetic field produced in the stator and the current induced in the rotor's coils. This type of motor is widely utilized in various machinery due to its superior power and environmentally friendly characteristics compared to traditional motors available in the market.

The study tracks the revenue accrued through the sale of induction motors by various players in the global market. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The Induction Motors Market Report is Segmented by Rotor Type (Squirrel-Cage Induction Motors, and More), Phase (Single-Phase Induction Motors, Three-Phase Induction Motors), Efficiency Class (IE1 Standard Efficiency, and More), Application (Pumps, Fans and Blowers, and More), End-User Industry (Manufacturing, Oil and Gas and Chemicals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Rotor Type

| Squirrel-Cage Induction Motors |

| Wound-Rotor Induction Motors |

By Phase

| Single-Phase Induction Motors |

| Three-Phase Induction Motors |

By Efficiency Class

| IE1 Standard Efficiency Induction Motors |

| IE2 High Efficiency Induction Motors |

| IE3 Premium Efficiency Induction Motors |

| IE4 Super Premium Efficiency Induction Motors |

| IE5 Ultra Premium Efficiency Induction Motors |

By Application

| Pumps |

| Fans and Blowers |

| Compressors |

| Conveyors and Material Handling |

| Elevators and Cranes |

| HVAC Equipment |

| Other Applications |

By End-User Industry

| Manufacturing |

| Oil and Gas and Chemicals |

| Power Generation and Utilities |

| Water and Wastewater |

| Mining and Metals |

| Commercial and Buildings |

| Transportation |

| Residential |

| Other End-User Industry |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Rotor Type | Squirrel-Cage Induction Motors | |

| Wound-Rotor Induction Motors | ||

| By Phase | Single-Phase Induction Motors | |

| Three-Phase Induction Motors | ||

| By Efficiency Class | IE1 Standard Efficiency Induction Motors | |

| IE2 High Efficiency Induction Motors | ||

| IE3 Premium Efficiency Induction Motors | ||

| IE4 Super Premium Efficiency Induction Motors | ||

| IE5 Ultra Premium Efficiency Induction Motors | ||

| By Application | Pumps | |

| Fans and Blowers | ||

| Compressors | ||

| Conveyors and Material Handling | ||

| Elevators and Cranes | ||

| HVAC Equipment | ||

| Other Applications | ||

| By End-User Industry | Manufacturing | |

| Oil and Gas and Chemicals | ||

| Power Generation and Utilities | ||

| Water and Wastewater | ||

| Mining and Metals | ||

| Commercial and Buildings | ||

| Transportation | ||

| Residential | ||

| Other End-User Industry | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the induction motors market?

The induction motors market has a market size of USD 23.14 billion in 2026 and is projected to reach USD 30.12 billion by 2031 at a 5.41% CAGR.

Which segments are leading and growing the fastest within this space?

Pumps held the largest application share at 35.67% in 2025 and compressors are projected to grow the fastest at 7.32% CAGR through 2031, while squirrel-cage motors led rotor type with 55% share and are projected at 7.34% CAGR.

How are regulations influencing adoption of high-efficiency motors and drives?

EU Ecodesign rules, China's IE3 baseline, and the U.S. fan and blower standards push IE3-IE4 motors and variable speed control, which accelerates premium-efficiency upgrades across pumps and fans.

What is driving three-phase motor adoption over single-phase units?

Three-phase motors deliver better torque density and power factor, and when paired with VFDs they improve part-load efficiency, which aligns with automation and building code requirements for energy savings.

Which regions will account for most of the new demand?

Asia-Pacific leads with 62% share in 2025 and a projected 6.98% CAGR to 2031, supported by semiconductor fabs, automotive assembly, and infrastructure programs across water and HVAC.

What technologies are shaping competitive strategies among leading suppliers?

IE4 and IE5 roadmaps using copper rotors and magnet-free SynRM designs, expansion of inverter-duty portfolios, and digital monitoring and service models are central to differentiation and growth.

Page last updated on: