Semiconductor Memory for Automotive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

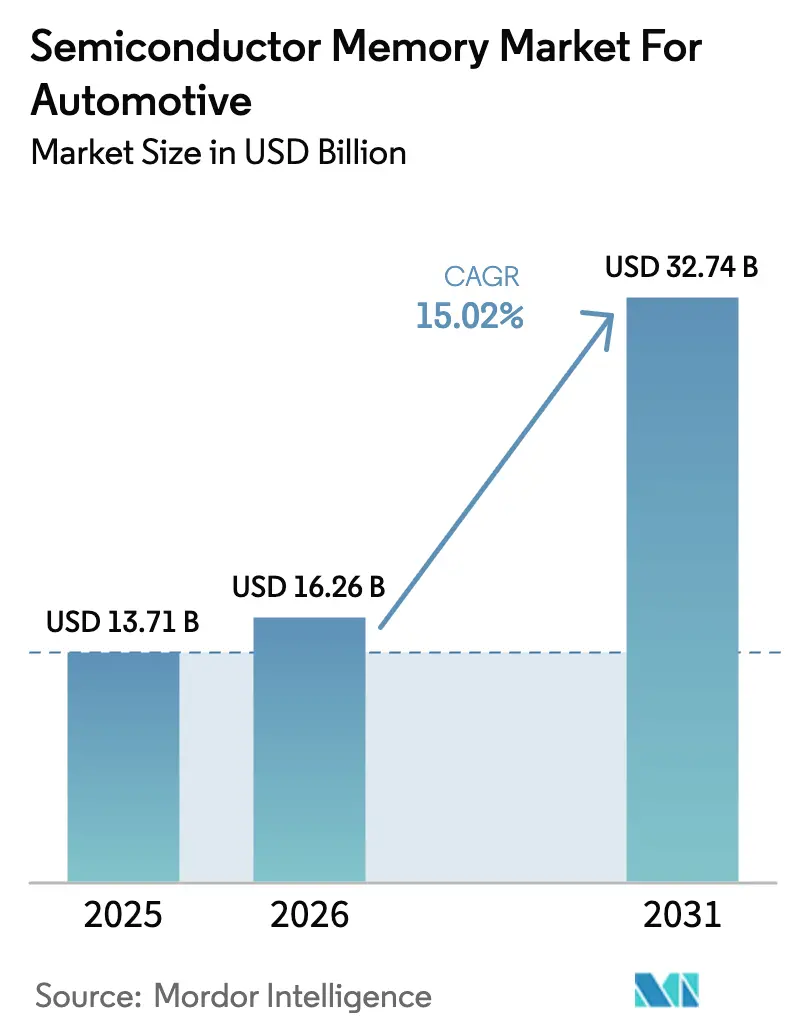

| Market Size (2026) | USD 16.26 Billion |

| Market Size (2031) | USD 32.74 Billion |

| Growth Rate (2026 - 2031) | 15.02% CAGR |

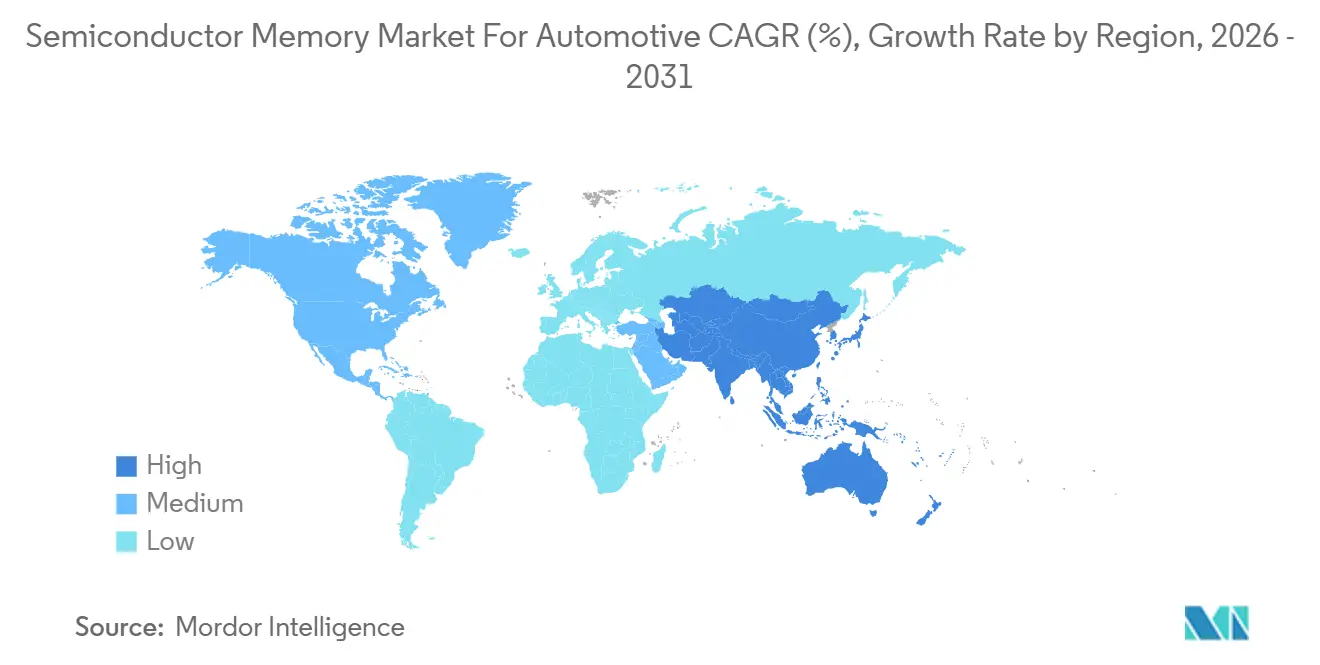

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Semiconductor Memory for Automotive Market Analysis by Mordor Intelligence

The semiconductor memory market size for automotive market size was valued at USD 13.71 billion in 2025 and estimated to grow from USD 16.26 billion in 2026 to reach USD 32.74 billion by 2031, at a CAGR of 15.02% during the forecast period (2026-2031). Rising adoption of software-defined vehicles, tighter cybersecurity rules, and the migration to centralized electrical-electronic architectures are pushing memory pools beyond 64 gigabytes per vehicle. Automakers are standardizing on LPDDR5 DRAM and UFS-based 3D NAND to stage frequent over-the-air updates, while domain controllers for Level 3 automation are provisioning 10-gigabyte model weights for transformer networks. Supply-side programs such as the CHIPS and Science Act in the United States and the European Chips Act are catalyzing regional production, although Asia-Pacific remains the revenue anchor given its electric-vehicle manufacturing scale. Premium pricing for automotive-grade parts persists because extended temperature grades, error-correction, and ISO 26262 qualification add cost yet deliver reliability demanded by original-equipment manufacturers.

Key Report Takeaways

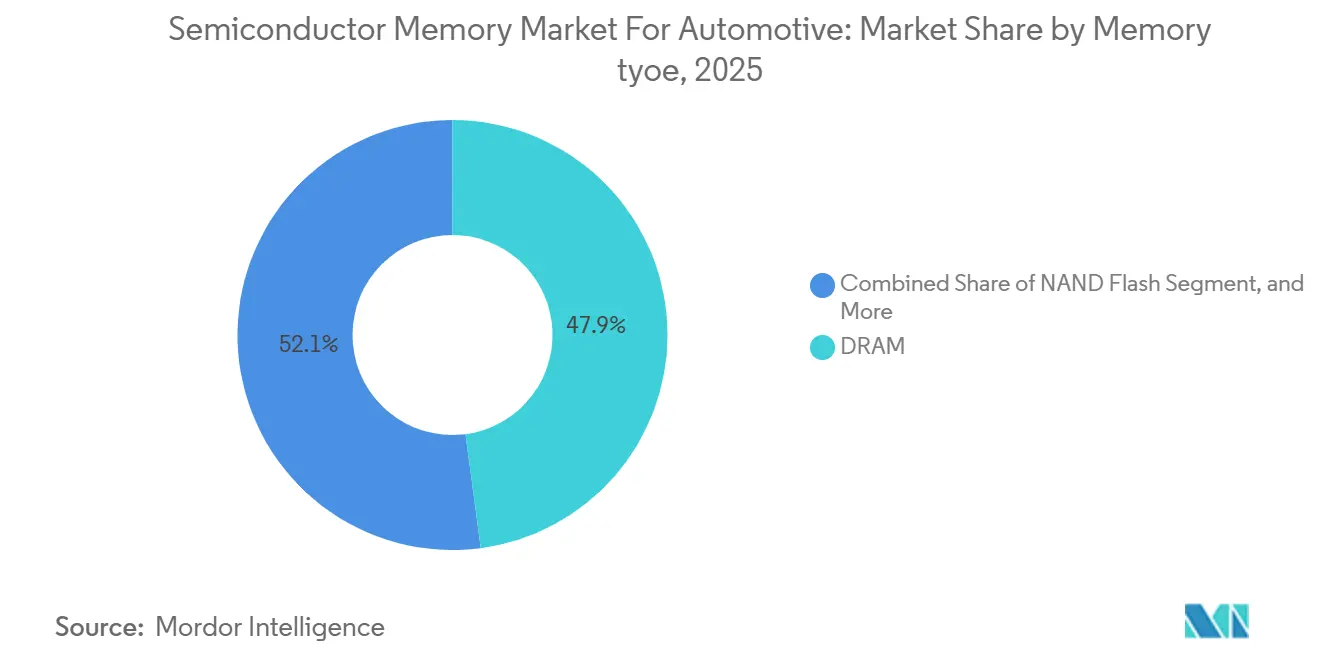

- By memory type, DRAM led with 47.91% of semiconductor memory market share in 2025, while NAND flash is projected to advance at a 15.08% CAGR through 2031.

- By application, the digital cockpit commanded 38.48% of revenue in 2025, whereas ADAS and automated driving is set to grow at a 15.17% CAGR to 2031.

- By vehicle type, passenger cars held 62.72% of volume in 2025, and electric passenger cars are forecast to expand at a 15.22% CAGR during 2026-2031.

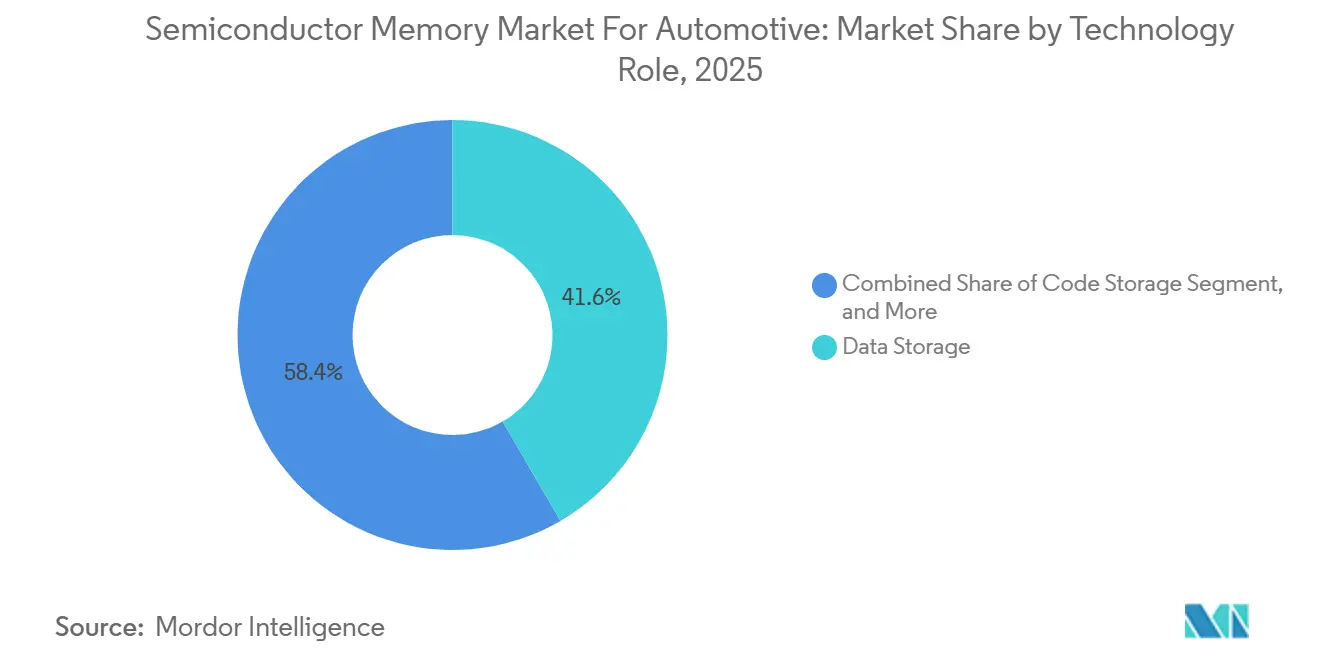

- By technology role, data storage dominated with 41.63% share in 2025 and is pacing a 15.11% CAGR, outstripping all other roles over the forecast horizon.

- By memory density, 128-512 Mb devices captured 46.62% share in 2025, whereas the 512 Mb-1 Gb tier is poised for the fastest 15.26% CAGR.

- By geography, Asia-Pacific secured 49.94% of revenue in 2025 and is positioned for a 15.34% CAGR, the highest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Semiconductor Memory for Automotive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Software-Defined Vehicle Adoption Accelerating Memory Capacity Requirements | +3.2% | Global, early adoption in North America and China | Medium term (2-4 years) |

| Centralized and Zonal E-E Architectures Expanding In-Vehicle Memory Pools | +2.8% | Global, led by European OEMs and Chinese NEV makers | Medium term (2-4 years) |

| Emergence of On-Package High-Bandwidth Memory for AI Domain Controllers | +2.4% | North America and Asia-Pacific, early-stage deployment | Long term (≥ 4 years) |

| Rapid Decline in Automotive-Qualified 3D NAND Cost per GB | +2.1% | Global, supply concentrated in Asia-Pacific | Short term (≤ 2 years) |

| High-Frequency OTA Update Cycles Requiring Larger Persistent Storage | +1.9% | North America and Europe, regulatory-driven in China | Short term (≤ 2 years) |

| Regulatory Push for In-Vehicle ML-Model Data Retention | +1.8% | Europe, North America, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Software-Defined Vehicle Adoption Accelerating Memory Capacity Requirements

Automakers are collapsing as many as 100 electronic control units into fewer than ten domain controllers, each with up to 32 GB of DRAM and 512 GB of NAND to host containerized software stacks. Tesla’s Hardware 4 platform already ships with 64 GB of LPDDR5 DRAM and 256 GB of UFS 3.1 storage, giving it headroom for real-time sensor fusion and full-self-driving inference.[1]Tesla, “Q2 2024 Investor Update,” ir.tesla.com General Motors’ Ultifi architecture standardizes on a 48 GB working-memory floor so that new features can be downloaded without hardware changes. Because memory is locked at design-in, demand persists even when vehicle output softens, anchoring a structural growth baseline. This dynamic is especially relevant for subscription-based functions that monetize incremental software, turning memory into a revenue-enabling asset rather than a pure cost item.

Centralized and Zonal E-E Architectures Expanding In-Vehicle Memory Pools

Zonal gateways aggregate sensor data by physical region, shedding wiring mass while concentrating compute and storage. Volkswagen’s E3 2.0 platform installs four 8 GB LPDDR5 gateways plus a central 64 GB compute node, shifting purchasing toward high-density devices.[2]Volkswagen AG, “Annual Report 2024,” volkswagenag.com Bosch calculates that memory content rises by USD 120-180 per vehicle under zonal designs, split roughly 60-40 between DRAM and NAND. Chinese brands over-specify capacity by 20-30% to future-proof against software bloat and comply with data-localization rules, creating an outsized pull for domestic DRAM and NAND suppliers.

Emergence of On-Package High-Bandwidth Memory for AI Domain Controllers

High-bandwidth memory (HBM) stacks bonded on silicon interposers are entering automotive roadmaps to meet the 1 TB-per-second throughput that Level 4 inference accelerators demand. SK hynix sampled 16 GB HBM3E in late 2025, reporting double-digit design wins with robo-taxi platforms.[3]SK hynix, “Develops First HBM3E 12Hi,” news.skhynix.com Packaging DRAM and NAND together trims board area, shaves latency, and simplifies thermal management compared with discrete components, giving tier-one suppliers a differentiated module for centralized AI compute nodes.

Rapid Decline in Automotive-Qualified 3D NAND Cost per GB

Average selling prices for 128-layer TLC NAND in automotive grades slid 18% in 2025, reaching USD 0.08 per GB. Kioxia’s BiCS8 node secured AEC-Q100 Grade 2 clearance, enabling 512 GB automotive SSDs priced below USD 50, a milestone that puts high-definition map caching in mainstream vehicles. Lower costs accelerate migration from eMMC to UFS interfaces, collapsing update times and smoothing user experience, although episodic factory incidents remind buyers that supply shocks can still spike contract pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Automotive Silicon Supply Chain | -1.4% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| High ASP Premium vs Consumer-Grade Memory | -1.1% | Global, cost-sensitive in emerging markets | Medium term (2-4 years) |

| Functional-Safety Certification Lead-Times | -0.9% | Global, regulatory compliance in Europe and North America | Medium term (2-4 years) |

| Thermal-Management Barriers in High-Density Modules | -0.7% | Global, acute in hot-climate regions and EVs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Automotive Silicon Supply Chain

A December 2025 fire at Western Digital’s Yokkaichi facility, which supplies 15% of global automotive-grade NAND, stretched lead times from 12 to 26 weeks and forced luxury OEMs to pay 30% air-freight premiums. Concentration is structural: Samsung, SK hynix, and Micron deliver more than 90% of automotive DRAM, with most fabs located in seismically active East Asia. Export controls on advanced tooling restrict expansion by Chinese contenders, capping alternate sources and keeping buffer-stock strategies expensive.

High ASP Premium vs Consumer-Grade Memory

Automotive LPDDR5 sold for USD 8.50 per GB in early 2026 versus USD 5.20 for smartphone-grade equivalents, reflecting extended temperature, longer test cycles, and ISO 26262 documentation overhead. Emerging MRAM carries an even steeper mark-up at USD 2.50 per Mb, thirty times the cost of NOR flash, limiting uptake to airbags and stability control where zero-latency and infinite endurance are mission-critical. For cost-sensitive markets in India and Southeast Asia, this premium constrains memory footprints to 32 GB DRAM and 128 GB NAND, delaying full software-defined functionality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Type: DRAM Retains Leadership While NAND Flash Rises Fast

The Semiconductor Memory for Automotive Market market size for DRAM equated to 47.91% of 2025 revenue, cementing its place as the workhorse for real-time compute. Advancing camera counts and higher-resolution displays keep DRAM density growth on track, while LPDDR5T delivers 9.6 Gb s⁻¹ throughput to meet multi-camera surround-view latency budgets. The semiconductor memory market size for NAND flash is accelerating, helped by 128-layer devices that slash cost-per-bit and make 512 GB UFS common even in mid-segment vehicles.

NAND flash, although smaller in 2025 share, posts the highest 15.08% CAGR as over-the-air update staging, event-data recording, and high-definition map caching proliferate. UFS 4.0 samples from Kioxia and Western Digital deliver 4 GB s⁻¹ sequential reads, cutting 10 GB update installs from 45 minutes to 12 minutes. DRAM meanwhile migrates from quad-channel LPDDR4X toward dual-channel LPDDR5 configurations, saving board real estate and power. MRAM, though only 3% of revenue, finds traction where unlimited endurance and instant-on boot justify price premiums, such as battery-management systems in electric vehicles.

By Application: Digital Cockpit Dominates as ADAS Drives Growth

Digital-cockpit systems consumed 38.48% of 2025 spending, reflecting multiple displays, voice assistants, and app-store ecosystems that require 24 GB of DRAM and 256 GB of NAND in premium trims. Memory density per seat continues to climb as augmented-reality overlays and 8K graphics permeate mid-range models, reinforcing DRAM’s hold on bandwidth-hungry rendering pipelines.

ADAS and automated driving, expanding at a 15.17% CAGR, is the fastest-growing slice of the Semiconductor Memory for Automotive Market . Level 3 pilots log lidar point clouds at 4-8 GB s⁻¹, demanding vast DRAM buffers and 512 GB-class NVMe SSDs for map storage. The segment benefits from transformer-based perception stacks whose model weights alone exceed 10 GB, ensuring a durable lift in working-memory demand. As regulatory bodies mandate 30 seconds of pre-crash data capture, persistent storage footprints widen, further buoying NAND shipments.

By Vehicle Type: Passenger Cars Lead While Electric Variants Accelerate

Passenger cars held 62.72% of shipments in 2025, driven by mainstream adoption of software-centric architectures. Electric passenger cars, however, register the sharpest 15.22% CAGR, spurred by battery-management systems that archive cell telemetry at kilohertz rates and rely on 4-8 GB NAND partitions for lifetime logs.

Light commercial vehicles post steady growth as fleet operators outfit vans with telematics gateways that preload route and manifest data, uplifting average persistent storage to 128 GB. Heavy trucks add 256 GB NAND to meet electronic logging mandates and platooning analytics, which collect ADAS traces for compliance audits. The Semiconductor Memory for Automotive Market thus captures incremental volume from every segment shift toward electrification and autonomy.

By Technology Role: Data Storage Commands the Largest Slice

Data storage accounted for 41.63% share in 2025 and is on a 15.11% CAGR trajectory as automakers cache maps, logs, and multiple software images on board. Code storage followed at 28%, benefiting from a migration to microservices that triples firmware size compared with monolithic builds. Working memory, representing 24%, grows as sensor fusion and AI inference workloads scale.

Unified memory architectures that co-package DRAM and NAND are emerging to collapse latency and cut power, a path championed by SK hynix for 2026 AI domain controllers. This trend blurs role boundaries, yet the semiconductor memory market share for data storage remains anchored because over-the-air cycles and regulatory retention rules bulk up non-volatile capacity at a faster clip than code or working memory needs.

By Memory Density: Mid-Range Capacities Dominate, High-Density Modules Surge

Devices in the 128-512 Mb class delivered 46.62% of 2025 revenue, serving clusters, body controllers, and gateways. The 512 Mb-1 Gb tier, however, is the growth leader at a 15.26% CAGR as zonal controllers specify single UFS modules that replace multi-chip arrays.

Above-1 Gb devices, while only 22% of revenue, gain momentum from ADAS platforms using 64 GB LPDDR5 and 512 GB NVMe configurations. As densities rise, component count drops, simplifying boards and improving reliability.

Geography Analysis

Asia-Pacific commanded 49.94% of 2025 sales and is on course for a 15.34% CAGR, fueled by China’s 9.2 million electric-vehicle output and data-localization mandates that require 16-32 GB of additional NAND per car. Domestic suppliers YMTC and CXMT leverage policy support to displace imports, although export controls cap their global reach. Japan and South Korea add momentum through vertically integrated champions Samsung, SK hynix, and Kioxia, while India grows from a smaller base, balancing cost constraints against rising ADAS penetration.

North America held 28% of global revenue in 2025 and grows at 15.1% CAGR on the back of USD 39 billion CHIPS incentives that drew Micron’s USD 20 billion New York fab commitment. Proposed NHTSA rules oblige Level 3 vehicles to store 30 seconds of sensor history, adding 8-16 GB of write-once memory per unit. Mexico strengthens regional supply resilience by assembling modules in Guadalajara, where Kingston and Transcend run new lines.

Europe captured an 18% stake in 2025 and expands at 14.6% CAGR, limited by supply concentration and slower electrification than China. The European Chips Act earmarks EUR 43 billion (USD 48.59 billion) for semiconductor projects, including Infineon’s EUR 5 billion (USD 5.65 billion) Dresden expansion that will supply embedded MRAM from 2027. Germany leads with centralized architectures in premium marques, while Eastern Europe posts the fastest sub-regional growth as Bosch and Continental integrate memory into zonal gateways built locally.

Competitive Landscape

The Semiconductor Memory for Automotive Market is moderately concentrated, with Samsung Electronics, Micron Technology, and SK hynix capturing 72% of DRAM and 58% of NAND revenue in 2025. These firms differentiate through rapid node migration, advanced packaging, and ISO 26262 roadmaps. Samsung mass-produced 10.7 Gb s-¹ LPDDR5T in December 2025 for Hyundai’s Genesis GV90, leveraging temperature-grade leadership. Micron secures multi-year supply deals with General Motors, pairing LPDDR5 and UFS 3.1 to halve installation times under the Ultifi platform.

SK hynix positions high-bandwidth memory as a leapfrog technology, sampling 16 GB HBM3E for AI domain controllers that need 1 TB s-¹ throughput. Outside the big three, Everspin dominates automotive MRAM with a 65% share, winning sockets in safety controllers where instant-on boot eliminates secondary storage. Chinese entrants YMTC and CXMT undercut pricing by up to 20%, but limited automotive qualification and export controls temper their penetration.

Tier-one suppliers are co-developing memory-centric modules to secure design wins. Renesas and NXP announced a zonal-gateway reference board that integrates 64 GB LPDDR5 and 256 GB UFS 3.1 for Ethernet backbones, targeting 2027 launches. Infineon embeds MRAM into its AURIX TC4x microcontrollers, removing external EEPROM and shaving USD 3 per ECU while maintaining data integrity during voltage droops. Competitive dynamics therefore hinge on balancing premium pricing for stringent grades against cost-reduction imperatives in mass-volume segments.

Semiconductor Memory for Automotive Industry Leaders

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

SK hynix Inc.

Kioxia Holdings Corp.

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SK hynix began mass production of automotive-grade HBM3E 12-high stack memory delivering 1.15 TB s-¹ bandwidth for Level 4 AI controllers.

- January 2026: Micron and General Motors signed a multi-year deal to supply LPDDR5 DRAM and UFS 3.1 storage for the Ultifi platform, aiming to cut software installation time by 50%.

- December 2025: Samsung commenced volume output of LPDDR5T DRAM at 10.7 Gb s-¹, shipping first to Hyundai’s Genesis GV90 electric SUV.

- November 2025: Infineon expanded its Dresden fab with a EUR 2 billion (USD 2.26 billion) investment to produce embedded MRAM from 2027 onward.

Global Semiconductor Memory for Automotive Market Report Scope

Semiconductor memory for automotive refers to specialized electronic memory chips used in vehicles to store and process data required for vehicle operation, safety, infotainment, and advanced driver-assistance systems (ADAS). Unlike standard consumer memory, automotive memory is engineered to withstand extreme temperatures, vibration, electrical noise, and long product lifecycles typical of vehicles.

The Semiconductor Memory for Automotive Market Report is Segmented by Technology Role (Code Storage, Working Memory, Data Storage, Other Roles), Memory Type (DRAM, NAND Flash, NOR Flash, MRAM and Emerging NVM), Application (ADAS and Automated Driving, Digital Cockpit, Powertrain, Chassis and Safety, Body and Comfort, Vehicle Networking, Battery Management System), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Buses and Coaches, Off-Highway Vehicles), Memory Density (Below 128 Mb, 128-512 Mb, 512 Mb-1 Gb, Above 1 Gb), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| DRAM |

| NAND Flash |

| NOR Flash |

| MRAM and Emerging NVM |

| ADAS and Automated Driving |

| Digital Cockpit |

| Powertrain |

| Chassis and Safety |

| Body and Comfort |

| Vehicle Networking |

| Battery Management System |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Buses and Coaches |

| Off-Highway Vehicles |

| Code Storage |

| Working Memory |

| Data Storage |

| Other Roles (Boot, Logs) |

| Below 128 Mb |

| 128 - 512 Mb |

| 512 Mb - 1 Gb |

| Above 1 Gb |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Memory Type | DRAM | |

| NAND Flash | ||

| NOR Flash | ||

| MRAM and Emerging NVM | ||

| By Application | ADAS and Automated Driving | |

| Digital Cockpit | ||

| Powertrain | ||

| Chassis and Safety | ||

| Body and Comfort | ||

| Vehicle Networking | ||

| Battery Management System | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| Off-Highway Vehicles | ||

| By Technology Role | Code Storage | |

| Working Memory | ||

| Data Storage | ||

| Other Roles (Boot, Logs) | ||

| By Memory Density | Below 128 Mb | |

| 128 - 512 Mb | ||

| 512 Mb - 1 Gb | ||

| Above 1 Gb | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected revenue for automotive semiconductor memory in 2031?

The market is forecast to reach USD 32.74 billion by 2031.

Which memory type is expected to grow the fastest through 2031?

NAND flash shows the highest 15.08% CAGR as persistent-storage needs for updates and map caching soar.

Why does Asia-Pacific dominate automotive memory demand?

China’s electric-vehicle scale and data-localization rules drive nearly half of global revenue, with regional suppliers capturing incremental share.

How are over-the-air updates influencing memory configurations?

Monthly security patches and feature releases require at least 128 GB dedicated NAND for staging, verification, and rollback, enlarging per-car storage footprints.

What makes automotive-grade memory more expensive than consumer parts?

Extended temperature tolerances, longer qualification cycles, and ISO 26262 functional-safety compliance raise testing costs, adding a 40-60% ASP premium.

Which companies lead in emerging MRAM adoption?

Everspin commands roughly 65% of automotive MRAM revenue by targeting safety-critical controllers that need instant-on and infinite endurance.

Page last updated on: