Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

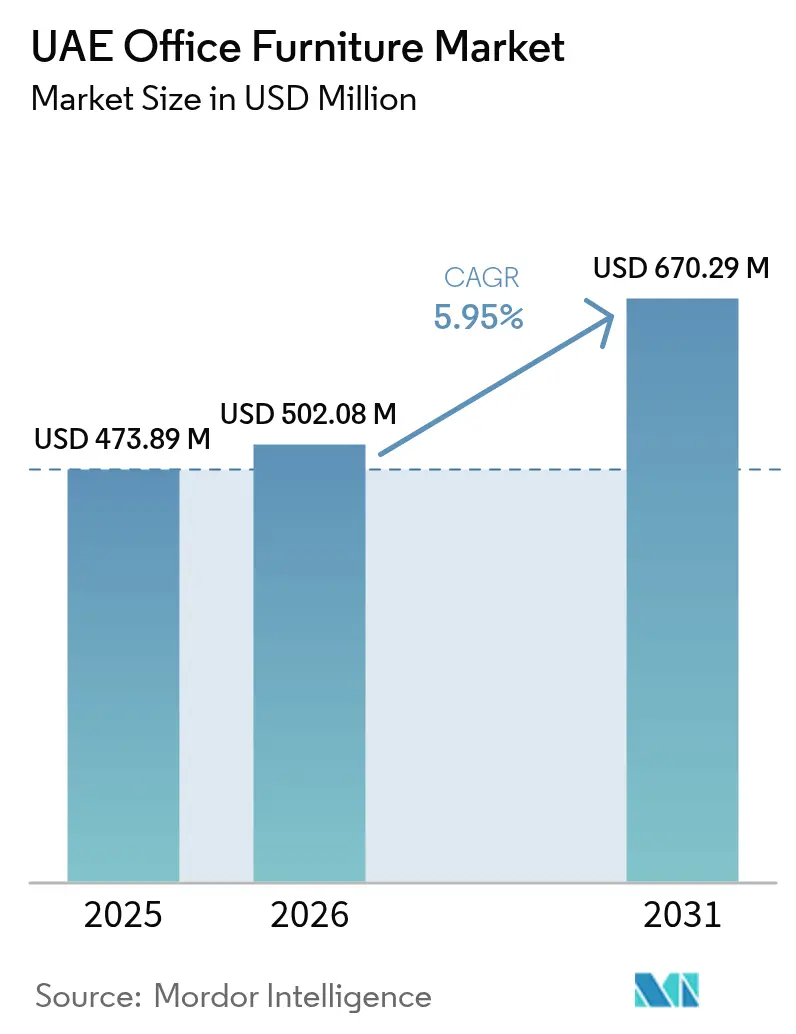

| Base Year Market Size (2025) | USD 473.89 Million |

| Market Size (2026) | USD 502.08 Million |

| Market Size (2031) | USD 670.29 Million |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

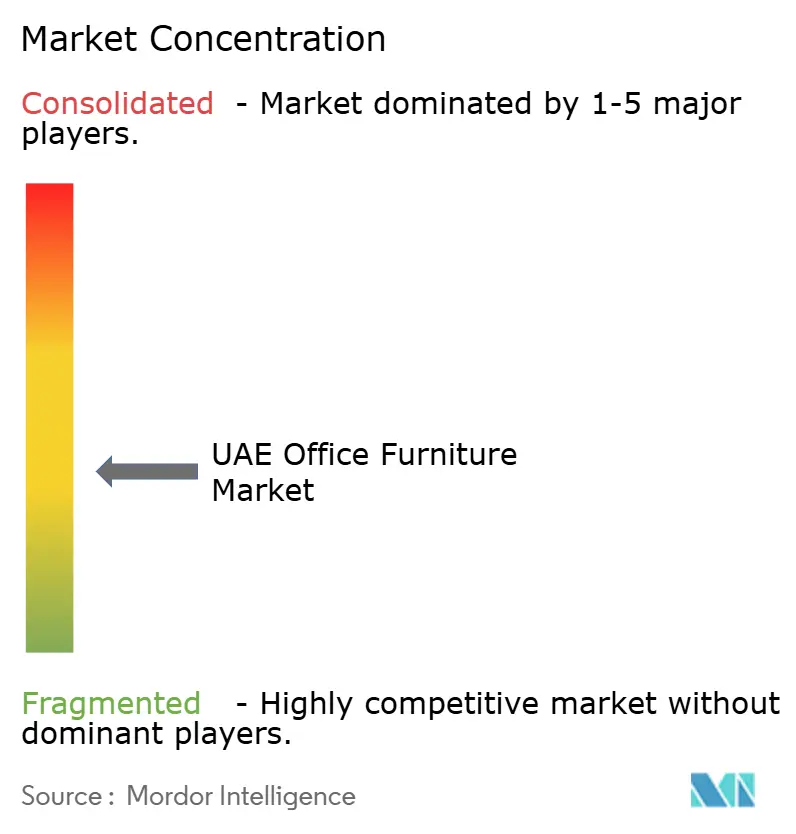

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Office Furniture Market Analysis by Mordor Intelligence

The UAE office furniture market size is expected to grow from USD 473.89 million in 2025 to USD 502.08 million in 2026 and is forecast to reach USD 670.29 million by 2031 at 5.95% CAGR over 2026-2031. Government-funded commercial real-estate programs, mandatory workplace-wellness rules, and hybrid work adoption by multinationals relocating to Dubai and Abu Dhabi continue to stimulate bulk procurement. “Made-in-UAE” quotas reward domestic content and have prompted several global brands to open assembly lines in Dubai Industrial City. Free-zone tax holidays aimed at green manufacturing lower entry barriers for sustainable production, while the rebound in tourism and retail extends demand beyond traditional corporate offices. Premium specifications remain the norm for new headquarters where furniture doubles as a talent-attraction tool. At the same time, co-working operators prefer modular, reconfigurable systems that maximize revenue per square meter and shorten payback periods.

Key Report Takeaways

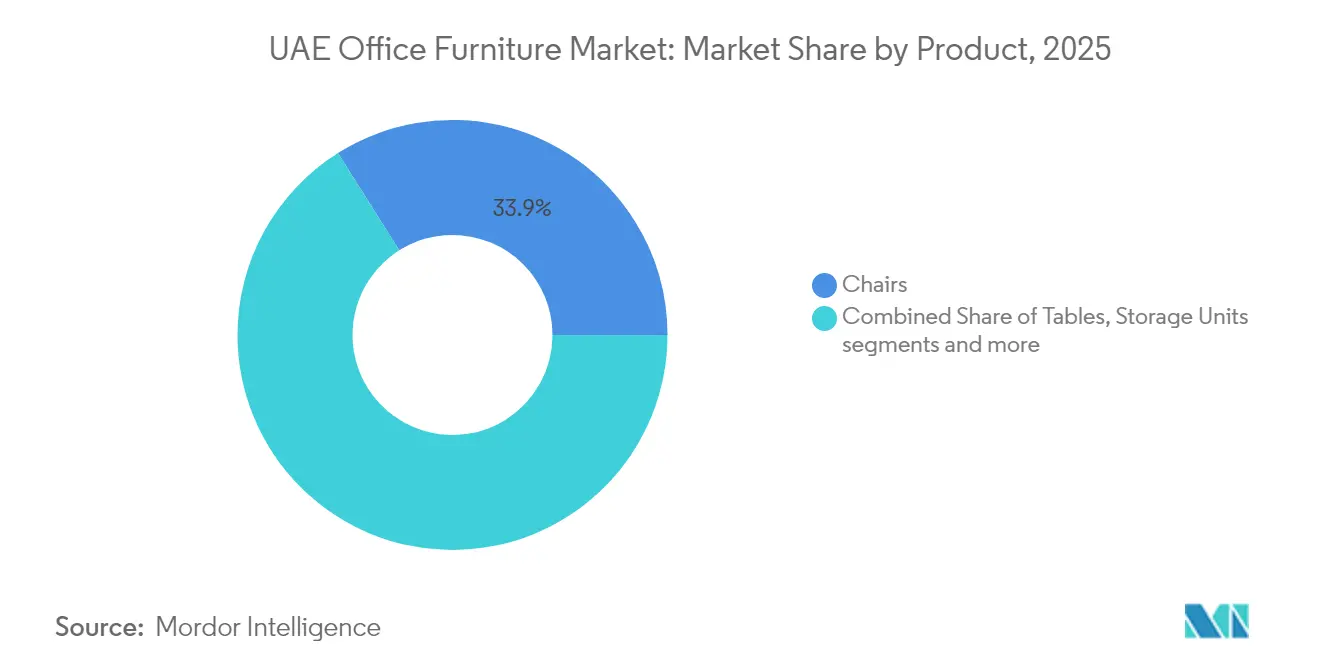

- By product, chairs accounted for 33.94% of the UAE office furniture market share in 2025, while booths and dividers exhibit the highest projected CAGR at 6.05% through 2031.

- By material, wood led with 44.78% revenue share in 2025; plastic and polymer products are forecast to expand at a 6.18% CAGR to 2031.

- By price range, the mid-range tier held 43.21% of the UAE office furniture market size in 2025; the premium segment is advancing at a 6.28% CAGR between 2026-2031.

- By end-user, corporate offices captured 47.35% share of the UAE office furniture market size in 2025, while hospitality and retail back-office demand is growing at a 6.61% CAGR to 2031.

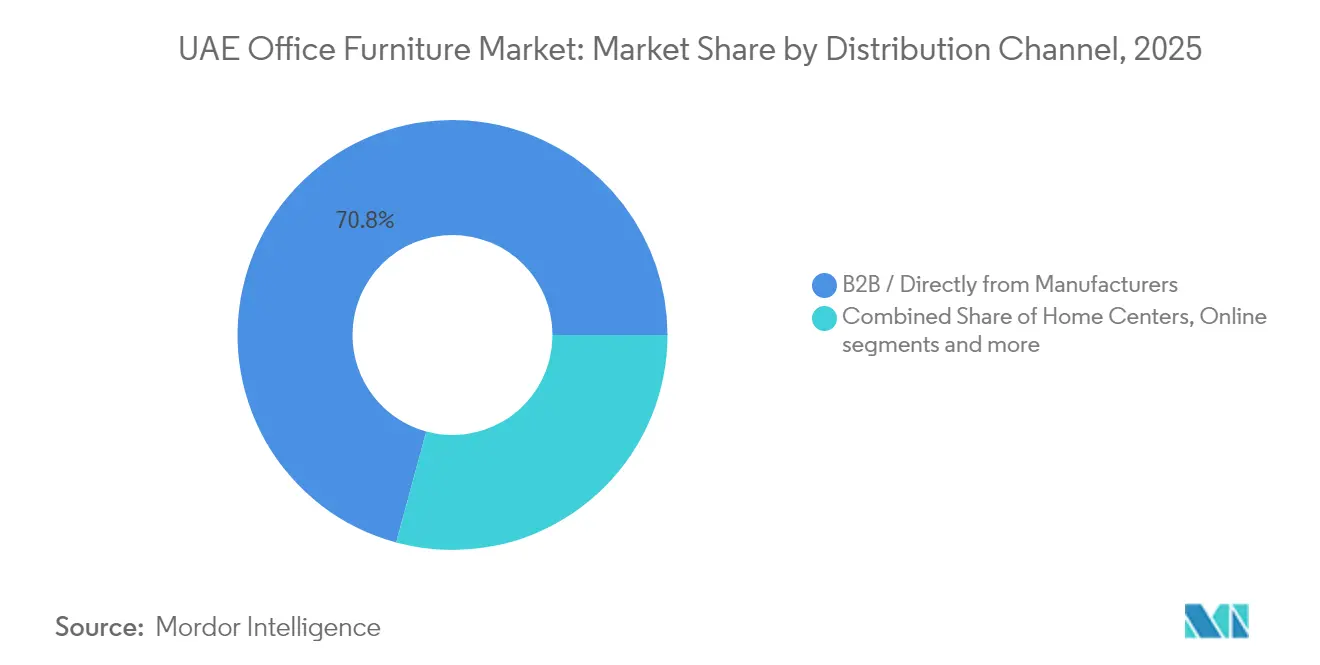

- By distribution channel, B2B direct sales held 70.78% of the UAE office furniture market share in 2025, while the same channel is projected to post the highest CAGR at 6.55% through 2031.

- By geography, Dubai commanded 41.25% revenue share in 2025; Abu Dhabi is projected to post the fastest regional CAGR at 8.12% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led commercial real-estate expansion | +1.2% | Dubai, Abu Dhabi, and spillover to Sharjah | Medium term (2-4 years) |

| Surge in co-working and flexible workspace operators | +0.8% | Dubai, Abu Dhabi, and early gains in Sharjah | Short term (≤ 2 years) |

| Mandatory workplace-wellness and ergonomics standards | +0.7% | All emirates | Long term (≥ 4 years) |

| Hybrid-office fit-outs for relocated global teams | +0.9% | Dubai, Abu Dhabi, and secondary markets are emerging | Medium term (2-4 years) |

| “Made-in-UAE” procurement quotas in federal entities | +0.6% | National, government districts | Long term (≥ 4 years) |

| Free-zone tax incentives for sustainable furniture lines | +0.5% | Dubai, Abu Dhabi, and Sharjah free zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Led Commercial Real-Estate Expansion Plans

Dubai’s 2040 Urban Master Plan and Abu Dhabi’s Economic Vision 2030 continue to announce clusters of Grade A towers, innovation parks, and government hubs that require fully furnished interiors at handover. Occupancy levels top 85%, forcing developers to fast-track new projects and pre-order furniture to avoid delays when tenants sign leases[1]Ministry of Foreign Affairs, “UAE Non-Oil Foreign Trade Hits All-Time High,” mofa.gov.ae. Procurement managers demand turnkey packages that cover workstations, collaborative zones, and reception areas, and often insist on a single point of accountability for supply, installation, and post-handover warranty. Federal ministries relocating to purpose-built campuses issue standardized bills of material, thereby amplifying volume per order and favouring vendors with automated production lines. Private enterprises moving into these districts mimic ministry standards to maintain design cohesion, effectively cascading identical specifications across multiple projects. The magnitude of these contracts pushes suppliers to invest in local warehousing and lean logistics so that partial shipments dock precisely with construction timelines. Such scale effects strengthen the UAE office furniture market by creating predictable, project-based sales pipelines that span two to four years.

Surge in Co-Working and Flexible Workspace Operators

Flexible space operators have grown from niche players to anchor tenants, absorbing entire floors in premium towers. Their business model revolves around high seat-density layouts that must be reconfigured nightly to suit hot-desking, events, and short-term incubator programs. Consequently, buyers prioritize modular desks with clip-on power rails, stackable stools, and wheeled acoustic partitions that can convert an open hall into private pods in minutes. Furniture-as-a-service contracts dominate transactions, locking suppliers into multi-year relationships that cover maintenance, swap-outs, and refurbishments. Brand identity is critical; operators commission signature upholstery colors and custom wood grains that match their digital-first aesthetics, giving domestic upholsterers and laminators new project streams. Rapid expansion into secondary locations across Sharjah has further widened geographic penetration for the UAE office furniture market. Importantly, the recurring revenue from monthly rental fees stabilizes demand during periods when conventional corporate fit-outs slow.

Mandatory Workplace-Wellness and Ergonomics Standards

The Ministry of Human Resources and Emiratization now treats ergonomic compliance as an enforceable obligation. Inspectors evaluate seat-height adjustability, lumbar curvature, and permissible monitor angles during routine audits. Corporate risk managers view non-compliance as both a reputational hazard and a liability exposure under ISO 45001 frameworks, prompting procurement teams to request third-party certification from furniture suppliers. Ergonomics also intersects with employee-well-being programs that track absenteeism linked to musculoskeletal disorders; boards increasingly allocate capital to preventive furniture upgrades rather than healthcare premiums. Sales cycles elongate because buyers demand digital mock-ups and test samples for user feedback, yet order sizes grow because organizations standardize across multiple sites once a chair or desk model passes pilot trials. Training modules that teach employees to set up workstations correctly have become bundled with large contracts, creating cross-selling opportunities for service-oriented vendors. Over time, ergonomic awareness elevates baseline expectations and cements premium features—synchro-tilt mechanisms, 4-D armrests, anti-fatigue edges—as non-negotiable elements in the UAE office furniture market.

Hybrid-Office Fit-Outs for Relocated Global Teams

Multinationals consolidating Gulf operations into Dubai and Abu Dhabi now treat office design as an integration exercise between physical space and virtual collaboration. Desks embed wireless chargers, occupancy sensors, and retractable power modules so teams can plug in anywhere. Meeting rooms are scaled down into huddle pods equipped with 360-degree cameras and sound-masking panels that enable hybrid presentations without acoustic echo. The brief increasingly calls for activity-based zones—focus booths, social lounges, and maker labs—each furnished with distinct densities and lighting levels. Procurement heads push vendors to deliver “ecosystem” solutions with matching finishes across workstations, soft seating, and storage, simplifying asset tracking and refurb cycles. Corporate sustainability rhetoric translates into a preference for FSC-certified wood, water-based lacquers, and upholstery derived from recycled PET bottles. Combined, these criteria elevate ticket values and reinforce the UAE office furniture market as a test-bed for integrated, tech-centric interiors that global headquarters later replicate elsewhere.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-driven raw material supply volatility | –0.4% | Nationwide, manufacturing hubs | Short term (≤ 2 years) |

| Fluctuating timber and metal prices | –0.3% | Nationwide | Short term (≤ 2 years) |

| Rising popularity of furniture leasing models | –0.2% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Poor recycling infrastructure is inflating disposal costs | –0.2% | National, urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import-Driven Raw Material Supply Volatility

UAE factories depend on MDF from Thailand, steel tubing from China, and specialty laminates from Italy. Any disruption—port congestion, Red Sea route security alerts, or container shortages—ripples across production schedules because local buffer stocks seldom cover more than six weeks[2]General Administration of Abu Dhabi Customs, “Foreign Trade Statistics,” adcustoms.gov.ae. To hedge, manufacturers place forward contracts and diversify supplier lists, but smaller firms lack the purchasing power to lock in favorable terms. Opportunistic spot-market buys sometimes lead to mismatched veneer shades or inconsistent board densities, triggering rework once batches reach final assembly. Delivery delays cascade into construction sites where furniture installation sits on the critical path before handover. Clients penalize late deliveries, eroding already thin margins. Consequently, the UAE office furniture market must internalize the true cost of global logistics volatility when projecting profit forecasts.

Fluctuating Timber and Metal Prices

European oak and beech prices respond to climate-induced forest restrictions and energy-driven kiln-drying costs[3]World Bank, “United Arab Emirates Furniture Parts Imports,” wits.worldbank.org. Steel spot rates swing with Chinese capacity curbs and iron-ore tariffs, making quotations valid for mere days. Large government tenders, however, freeze prices for up to three years, forcing vendors to absorb inflation spikes. Currency hedging offers partial relief, yet forward contracts can backfire if markets plunge, leaving firms with above-market raw-material inventories. Design engineers try swapping solid wood for engineered veneer and steel for powder-coated aluminum, but specification approvals add administrative overhead. Until commodity futures stabilize, cost unpredictability remains a nagging restraint in the UAE office furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Chairs Maintain Dominance While Dividers Drive Innovation

Chairs generated 33.94% of the UAE office furniture market size in 2025, driven by mandatory ergonomic audits that force enterprises to replace legacy seating. Frequent user contact accelerates wear on casters, gas lifts, and upholstery, prompting refurb or replacement every 5-7 years—well ahead of tables or storage cycles. Meeting and guest chairs expand briskly as corporates shift from fixed conference rooms to agile collaboration zones requiring diverse seating postures. Task-chair specifications now include mesh backs for breathability, weight-sensitive synchro-tilt, and headrests adaptable for VR headset compatibility. These evolving requirements align with health-and-safety checklists, reinforcing demand for premium manufacturers that document test results and global warranty coverage.

Meanwhile, booths and dividers are on an upward trajectory, projected to grow at a 6.05% CAGR through 2031. Soft-lined acoustic pods help employees conduct video calls without distracting open-office neighbors, meeting hybrid work etiquette benchmarks. Movable dividers with writable glass surfaces turn empty corridors into impromptu scrum zones, underpinning the UAE office furniture market’s pivot to activity-based layouts. Although the unit count per project is lower than chairs, average selling prices are higher, lifting revenue share over time. Importantly, booths incorporate embedded ventilation fans and LED task lighting, forging cross-sector partnerships between furniture makers and HVAC or IoT suppliers for integrated control panels.

By Material: Wood Leadership Faces Plastic Innovation Challenge

Wood held 44.78% of the UAE office furniture market share in 2025 because natural veneers convey status and align with regional aesthetics rooted in hospitality culture. Executive suites still favor walnut credenzas and solid-oak meeting tables that project permanence. Yet procurement teams also cite sustainability; FSC-certified timber commands premiums as boards showcase eco-labels during ESG presentations. Local joineries import finger-jointed panels from Italy but increasingly explore African plantation teak processed in Ras Al Khaimah to reduce freight miles.

Plastic and polymer products grow at a 6.18% CAGR by leveraging low weight, recyclability, and freedom of form. High-pressure polypropylene shells survive outdoor balconies where smokers retreat, while glass-fiber-reinforced composites enable stool bases that look like metal but cost half as much. Designers mold cable channels and USB ports directly into polymer desk modesty panels, slashing assembly steps. The “other materials” category combines bamboo cores with aluminum skins or basalt-fiber rods, showing how hybrid innovation erodes singular-material dominance. This expanding choice palette broadens the appeal of the UAE office furniture market among architects seeking differentiating textures.

By Price Range: Premium Segment Accelerates Through Corporate Demand

Mid-range lines represented 43.21% of the UAE office furniture market share in 2025, balancing performance and cost for federal ministries and mid-cap firms. Vendors in this tier deliver warranty periods of five years, fabric choices in corporate colors, and modular add-ons like monitor arms at modest surcharges. Clients appreciate predictable lead times, usually six weeks, making this range a default for projects under tight fit-out schedules.

Premium furniture, however, records the fastest 6.28% CAGR. Multinationals ask for antimicrobial nanocoating, leather sourced under animal-welfare audits, and cast-zinc hardware with artisanal polish. Vendor proposals include carbon-footprint dashboards mapping cradle-to-grave emissions, resonating with board-level ESG narratives. Installation crews laser-level desks within ±1 mm tolerances, reflecting service quality expectations at this price point. The prestige factor filters down to regional family offices emulating Fortune 500 aesthetics, broadening premium adoption across the UAE office furniture market.

By End-User: Corporate Dominance Meets Hospitality Growth

Corporate offices captured 47.35% of the UAE office furniture market size in 2025, thanks to ongoing expansions by banks, consultancies, and tech giants in the Dubai International Financial Centre and Abu Dhabi Global Market. These tenants commission workplace strategy consultants to blueprint layouts, generating precise furniture schedules that drive bulk orders. Government agencies, while classified separately, often piggyback on corporate design language, further boosting contract volumes for standardized workstations and storage.

Hospitality and retail back-office environments deliver a 6.61% CAGR as the UAE welcomes rising tourist arrivals. Hotels invest in employee experience—dedicated social rooms, ergonomic concierge desks, and training centers—mirroring guest-facing opulence behind the scenes. Retailers, juggling omnichannel logistics, retrofit stock rooms into inventory command centers equipped with height-adjustable workbenches and ESD-safe chairs for electronics. Education and healthcare maintain steady procurement, but hospitality’s seasonal refurbishment cycles inject fresh dynamism into the UAE office furniture market, encouraging manufacturers to offer quick-ship SKUs aligned with renovation windows.

By Distribution Channel: Direct Sales Dominate Project-Based Market

B2B direct sales claimed 70.78% revenue share because mega-projects value single-source accountability for design, supply, and installation. Factory account managers embed with general contractors, attending weekly site meetings to coordinate ceiling clearances, floor cores, and delivery elevators. In-house CAD teams adjust panel heights based on live MEP changes, an iterative collaboration impossible via retail channels. Direct deals often bundle extended warranties, user training, and asset-management software, positioning manufacturers as lifecycle partners.

Retail and e-commerce serve SMEs and replacement buyers who need fewer than 20 seats. Home-improvement chains stock task chairs and flat-pack desks optimized for self-assembly, while online platforms attract start-ups with flash promotions and buy-now-pay-later options. Specialty showrooms feature experience zones where executives test high-end chairs alongside VR mock-ups of proposed offices. Although retail revenue is smaller, its high transaction frequency provides real-time data on emerging style preferences, informing future mass-production runs across the UAE office furniture market.

Geography Analysis

Dubai maintained 41.25% share in 2025 by virtue of its diverse economic base that spans finance, media, and e-commerce. The emirate’s tight vacancy rates, especially for Grade A stock in DIFC and Business Bay, compel tenants to maximize worker density without sacrificing comfort. Furniture suppliers respond with narrow-footprint workstations and shared sit-stand benches that squeeze more seats into the same footprint. Dubai’s trade and logistics infrastructure also serves as a re-export hub, so warehouses stock extra inventory that can redeploy to regional Gulf projects, reinforcing economies of scale for the UAE office furniture market.

Abu Dhabi posts an 8.12% forecast CAGR on the back of megaprojects like Al Maryah Island South and ADQ’s new headquarters cluster. Sovereign entities demand iconic lobbies featuring marble reception desks capped with bespoke lighting, providing showcase opportunities for local craftsmen. Sustainability regulations tied to Estidama Pearl Ratings nudge project teams toward low-VOC lacquers and recycled aluminum frames. As ministries centralize into smart campuses, they adopt asset-tracking software linked to RFID tags embedded in furniture, opening ancillary service revenue for vendors.

Sharjah and the northern emirates emerge as cost-efficient alternatives for manufacturers seeking lower industrial land leases. Free-zone incentives in Hamriyah Port attract containerized shipments of knock-down kits that local factories assemble for nearby projects. Universities in Sharjah’s education district procure collaborative lecture hall seating and 24/7 library desks, spreading demand across academic calendars. Ras Al Khaimah’s hospitality boom, fueled by beachfront resorts, orders back-office furniture with moisture-resistant surfaces suited to marine air. Collectively, these regions diversify the customer mix within the UAE office furniture market and reduce reliance on the Dubai-Abu Dhabi corridor.

Regulatory Landscape

Market access for office furniture and related components is shaped by the Ministry of Industry and Advanced Technology (MoIAT) through the UAE Conformity Assessment System. Regulated product categories require Certificates of Conformity and supporting test reports from accredited laboratories for clearance and sale. Import processes also rely on standard trade documentation (commercial invoice, certificate of origin, packing list, and bill of entry), and shipment processing can be accelerated or delayed depending on whether products need MoIAT product status statements for customs shipments.

On the border and local-market side, the Federal Authority for Identity, Citizenship, Customs and Port Security (ICP) operates the centralized customs tariff system used to confirm HS codes, duty treatment, and any restrictions, with a typical UAE customs duty rate of 5% of CIF for most imported goods. Within Dubai, Dubai Municipality, via its Certification and Quality Control of Products Section, enforces product conformity practices that influence specifications and supplier selection for projects that require documented safety and quality compliance.

Value Chain Analysis

The UAE office furniture value chain begins with imported inputs, notably MDF, steel tubing, and specialty laminates, and moves through local cutting, fabrication, finishing, and assembly before delivery to project sites. Manufacturing clusters around logistics-linked industrial zones such as Jebel Ali Free Zone (JAFZA), Dubai industrial areas (e.g., Al Quoz), and Sharjah free zones, where proximity to ports and warehousing supports bulk, time-bound fit-out schedules and helps mitigate the short buffer-stock reality typical in the segment.

Value capture increasingly shifts toward vertically integrated players that bundle space planning, engineering, manufacturing, and in-house installation to manage site changes and accelerate handover readiness. Compliance and licensing requirements under MoIAT, including industrial regulation frameworks such as Federal Decree-Law No. 25/2022, reinforce the role of standardized specifications and documented quality systems. In parallel, corporate and government buyers frequently request recognized benchmarks such as ISO and BIFMA-aligned performance evidence, pushing suppliers to invest in CNC-enabled production, automated finishing, and reliable last-mile installation capabilities.

Competitive Landscape

Competition remains moderate, with a stable core of domestic manufacturers complemented by design-driven multinationals. Local pioneers such as BAFCO and Highmoon leverage short lead times, extensive showroom footprints, and a nuanced grasp of Arabic-English bilingual documentation, securing an inside track on federal tenders that require Arabic catalogues and onsite Arabic-speaking project managers. Their fabricated-to-order approach allows last-minute dimension tweaks when MEP reroutes appear during fit-out.

Global powerhouses—Herman Miller, Steelcase, and Haworth—capitalize on long-standing R&D pipelines that feed patent-protected ergonomic mechanisms and durable surface materials. They cultivate deep relationships with architecture and design firms, often participating in early conceptual workshops to lock specs before projects hit the tender stage. These brands differentiate through global warranty reciprocity, enabling multinationals to service assets purchased in the UAE at offices worldwide, an assurance local brands cannot yet match.

An emerging cadre of niche specialists focuses on technology integration and circular-economy services. Start-ups retrofit legacy desks with IoT sensors that track real-time utilization, selling data dashboards that help facilities teams right-size footprints. Others run refurbishment hubs where worn chairs are stripped, powder-coated, and re-upholstered for a second lease cycle, offering companies ESG credits against waste-reduction targets. Together, these innovators force incumbents to refine after-sales propositions, tilting the UAE office furniture market toward holistic workspace-as-a-service solutions rather than pure product sales.

UAE Office Furniture Industry Leaders

Bafco

Herman Miller

Steelcase

Highmoon Furniture

IKEA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Local capacity additions and industrial-zone commitments are creating room for suppliers that can deliver customized, fast-turnaround project packages aligned with procurement localization priorities. A clear proof point is Zarberg’s December 2025 announcement to invest over AED 120 million in a new furniture manufacturing facility at DP World’s National Industries Park in Dubai, with a Phase 1 footprint of 18,000 sqm within a planned 65,000 sqm development. Such investments strengthen the addressable opportunity for UAE-based assembly and finishing, particularly for mid-range to premium corporate fit-outs that demand consistent lead times and documented compliance.

Demand visibility also improves where the commercial pipeline is measurable: Dubai off-plan office sales reached Dh 13.1 billion in H1 2026, exceeding the combined value of transactions from 2019 through 2025, which expands the pool of properties progressing toward interior fit-out scopes. In parallel, emirate-level industrial programs broaden end-user coverage beyond corporate offices, illustrated by RAKEZ signing an agreement in May 2026 with Magrabi Retail Group to set up a Store Manufacturing Centre for furniture and store fit-outs with capacity to service up to 140 stores annually. This supports opportunities for modular systems, standardized rollout packages, and after-sales refurbishment and maintenance models that suit multi-site operators.

Recent Industry Developments

- May 2026: Ras Al Khaimah Economic Zone (RAKEZ) signed an agreement with Magrabi Retail Group to establish a Store Manufacturing Centre focused on furniture and store fit-outs, designed to service up to 140 stores annually. The agreement formalizes a repeatable, multi-site rollout pipeline that favors standardized product platforms and dependable local production and installation capacity.

- December 2025: Zarberg announced an investment of over AED 120 million in a new furniture manufacturing facility at DP World’s National Industries Park (NIP) in Dubai, with Phase 1 spanning 18,000 sqm within a planned 65,000 sqm site. The project strengthens the local supply base for customized and higher-spec interior packages, helping reduce lead-time exposure tied to imported finished goods.

- June 2024: The Federal Authority for Identity, Citizenship, Customs and Port Security (ICP) continued expanding use of its centralized customs tariff system to standardize HS-code based duty and restriction checks across importers. For office furniture buyers and distributors, improved tariff classification workflows reduce clearance friction and support tighter project scheduling for direct-to-site deliveries.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of office furniture sold in the UAE for workplace use, across common items like seating, desks, tables, and storage, and counted in current US dollars for the time period studied.

Scope exclusions: We exclude office supplies and consumables, and we also exclude building fit-out services such as interior contracting and civil works.

Segmentation Overview

- By Product

- Chairs

- Employee Chairs

- Meeting Chairs

- Guest Chairs

- Tables

- Conference Tables

- Desks

- Other Tables

- Storage Units

- Filing Cabinets

- Bookcases & Shelving

- Sofas / Soft Seating

- Booths & Office Dividers

- Other Office Furniture (Stools, Reception, Accessories)

- Chairs

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-range

- Premium

- By End-user

- Corporate Offices

- Healthcare Offices

- Educational Institutions

- Government & Public Offices

- Hospitality & Retail Back-office

- Others

- By Distribution Channel

- B2C / Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B / Direct from Manufacturers

- B2C / Retail

- By Geography

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a fact base on demand drivers and the supply chain so we can size the market with a clear logic. For the UAE, we leaned on public sources such as UAE Federal Competitiveness and Statistics Centre releases, Dubai Statistics Center tables, UAE Central Bank economic indicators, and UAE Ministry of Economy publications on business activity and trade.

To cross-check category direction, we also reviewed customs and trade signals where product coding is available, plus relevant standards and circulars from UAE authorities, and academic or peer-reviewed work on workplace ergonomics and fit-outs in the region. Company annual reports, investor presentations, and reputable press were used to understand pricing moves, project timing, and channel shifts. Where needed, we referenced paid subscriptions for company financials and intelligence, patent look-ups, and import-export shipment level context to check whether the market mix was moving toward higher value seating and modular workstations. These sources are illustrative, and many other public documents and databases were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions, especially around average selling prices, typical discounting in project sales, and how demand splits between new office builds and refurbishment cycles. We spoke with a mix of manufacturers, distributors, retailers, workplace designers, and large buyer groups across the UAE so we could validate channel mix and project conversion timing. Inputs were also checked across the main emirates to avoid over-weighting activity from one office hub when estimating the national total.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | |

| Mid tier: 48% | Functional/Unit leaders: 41% | |

| Smaller Players: 15% | Managers: 47% |

Market-Sizing & Forecasting

Our sizing uses a top-down and bottom-up approach, where UAE office build activity, business formation, and refurbishment intensity are first translated into a furniture demand pool, and then the totals are tested using selective supplier and channel roll-ups. In practice, the model starts from demand-side indicators like office space additions and fit-out cycles, and then it is adjusted using pricing and mix checks from trade and channel feedback.

Key inputs include commercial real estate pipeline and occupancy signals, import and re-export patterns for furniture categories, channel mix between project sales and retail, average selling price bands by major product groups (seating, desks, storage), and the share of modular workstations in new projects. These variables matter because shifts in project-led demand or a move toward ergonomic seating can change value even when unit volumes remain stable.

For forecasting, scenario analysis is used with a base case built from macro indicators and construction outlook, and then it is refined using what respondents expect on tender flow, lead times, and price revisions. When bottom-up checks are incomplete for smaller local players, gaps are handled by using observed distributor coverage, typical assortment breadth, and a conservative uplift factor that is rechecked during validation.

Data Validation & Update Cycle

Validation is done through triangulation across three layers, desk indicators, primary feedback, and internal model checks on unit economics so we can spot values that do not match real purchasing behavior. If the implied pricing, growth rate, or channel shares drift outside what is seen in interviews or public signals, the assumptions are reopened and the calculation steps are reworked before sign-off.

A second analyst review is used to challenge the scope boundary, currency handling, and any sudden jumps by year that look inconsistent with project cycles. The report is refreshed annually, and interim updates are triggered when material events occur such as sharp currency moves, large policy changes, or major shifts in construction timing. Before delivery, we run a fresh pass on key inputs so clients receive the most current view available.

Mordor Intelligence's UAE Office Furniture Market Estimate Compared With Other Published Estimates

Published market values for UAE office furniture can vary because each source may choose a different timing for currency conversion, a different way to treat price discounting in project sales, and a different rule for what counts as office furniture versus adjacent fit-out spending. When these choices are combined with different base years, the market size can look meaningfully higher or lower even if everyone is looking at the same country.

In our work, estimates are kept stable by refreshing average selling prices and mix assumptions on a planned cadence, and then rechecking the results against trade signals and channel feedback before numbers are finalized, which is a discipline applied in the model by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 473.89 M (2025) | |

| Industry Consultancy A | USD 450.00 M (2024) | Uses a different base year and appears to rely more on historical value with a lighter stated treatment of annual price progression and discounting in contract projects, which can compress the market value versus a refreshed ASP build. |

| Press Release B | USD 316.63 M (2024) | Likely applies a narrower product boundary and more conservative pricing assumptions, and the public note gives limited detail on validation checks across channels, which can reduce the estimated value in a project-heavy market. |

Taken together, the spread mainly reflects base-year selection and how pricing and project discounting are translated into value. By keeping the steps visible, linking demand to real office activity, and re-validating the price mix assumptions through repeated checks, the final number stays traceable to inputs that can be revisited and updated in a consistent way.

Key Questions Answered in the Report

How large is the UAE office furniture market in 2026?

The UAE office furniture market size stands at USD 502.08 million in 2026 and is set to grow at a 5.95% CAGR to 2031.

Which product category leads sales in the UAE?

Chairs remain in the top-selling category, generating 33.94% of total revenue in 2025 due to ergonomic mandates and frequent replacement cycles.

Why is premium furniture demand accelerating?

Multinationals favor high-specification, sustainable furniture aligned with global workplace standards, driving the premium tier at a 6.28% CAGR.

What makes Abu Dhabi the fastest-growing regional market?

Aggressive infrastructure development, smart-campus projects, and sustainability regulations produce an 8.12% CAGR for Abu Dhabi through 2031.

How do “Made-in-UAE” quotas affect suppliers?

Federal In-Country Value rules push contracts toward manufacturers with local production, encouraging global brands to establish UAE assembly partnerships.

What impact do leasing models have on the sector?

Furniture-as-a-service extends product life, reduces new unit sales, but opens recurring revenue streams tied to maintenance and refurbishment.

Page last updated on: