Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.87 Billion |

| Market Size (2026) | USD 4.04 Billion |

| Market Size (2031) | USD 4.99 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Interior Design Market Analysis by Mordor Intelligence

Saudi Arabia interior design market size in 2026 is estimated at USD 4.04 billion, growing from 2025 value of USD 3.87 billion with 2031 projections showing USD 4.99 billion, growing at 4.32% CAGR over 2026-2031. The robust trajectory is underpinned by Vision 2030’s giga-project pipeline, a record hotel room pipeline of 362,000 keys, and sustained growth in retail and upmarket residential renovations. Hospitality developers front-load procurement to meet luxury standards, while retail landlords champion immersive “experience economy” concepts that elevate interior complexity and fee potential. Mortgage reforms widen the addressable homeowner base, and digital design tools such as BIM and VR compress lead times, enabling firms with strong adoption to capture large multi-site contracts. Meanwhile, import cost volatility and skilled labor shortages remain headwinds that favor financially resilient, tech-forward design studios.

Key Report Takeaways

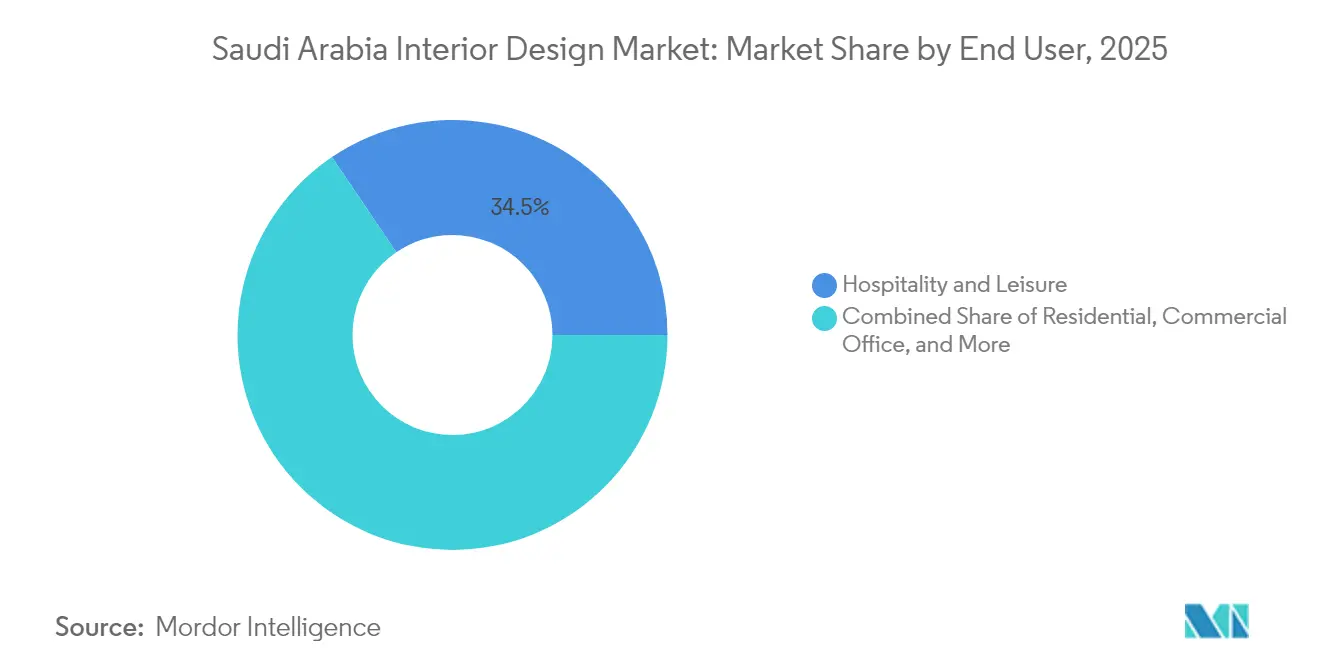

- By end user, Hospitality and Leisure led with 34.48% revenue share in 2025, while Retail and F&B is expanding at a 4.76% CAGR through 2031.

- By project type, New Build captured 60.78% share of the Saudi Arabia interior design market size in 2025, whereas Renovation and Remodel is projected to increase at a 4.94% CAGR to 2031.

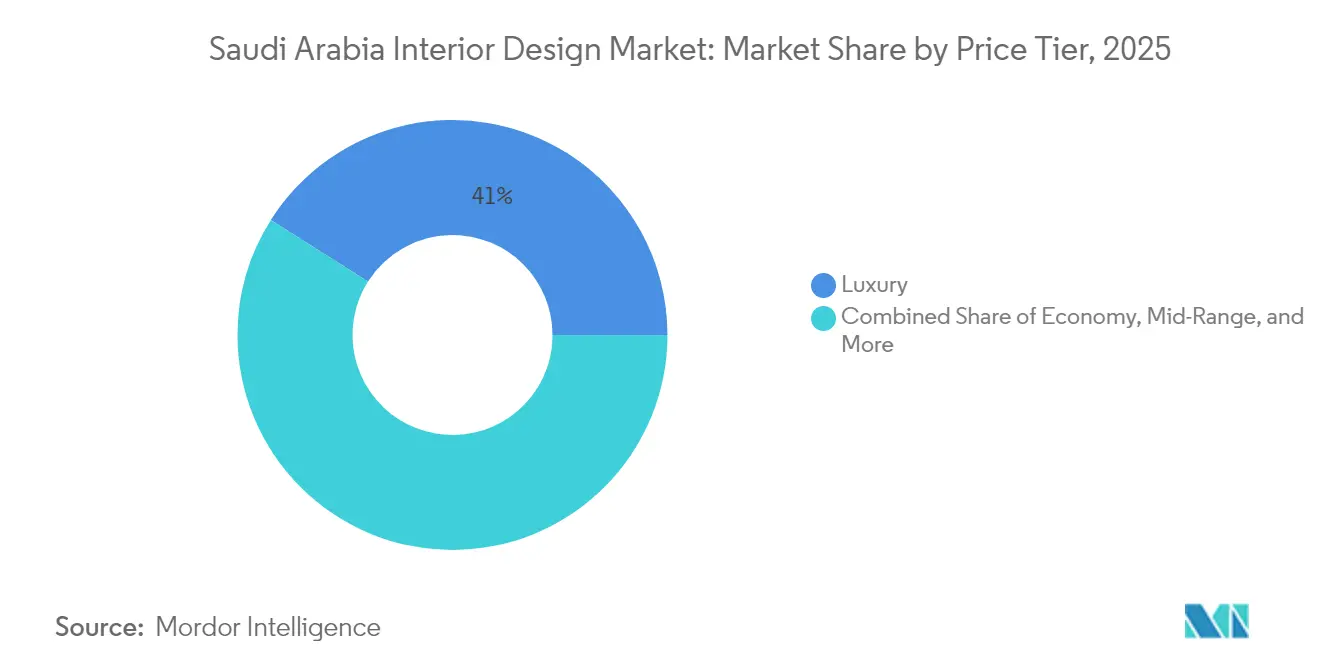

- By price tier, Luxury commanded 41.02% of the Saudi Arabia interior design market share in 2025, and Ultra-Luxury is forecast to grow the fastest at 5.56% through 2031.

- By geography, Riyadh Metropolitan accounted for 37.76% activity in 2025, yet the Medina and North-West NEOM corridor is advancing at a 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Interior Design Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga-project pipeline accelerates commercial & hospitality interiors | +1.8% | National, with concentration in NEOM corridor, Riyadh, Red Sea | Long term (≥ 4 years) |

| Record hotel pipeline (~320k rooms by 2030) boosting FF&E demand | +1.2% | National, with emphasis on Riyadh Metropolitan, Makkah Province | Medium term (2-4 years) |

| Retail "experience economy" driving mall & F&B fit-outs | +0.8% | Riyadh Metropolitan, Eastern Province, Makkah Province | Short term (≤ 2 years) |

| Residential mortgage reforms unlocking mid-/high-end home renovations | +0.6% | National, with early gains in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Localization mandates spurring growth of Saudi fit-out contractors | +0.4% | National | Long term (≥ 4 years) |

| Digital design tools (BIM, VR) shortening lead-times & winning clients | + 0.3% | National, with early adoption in major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 giga-project pipeline accelerates commercial and hospitality interiors

Vision 2030 allocates about USD 1.6 trillion to construction, catalyzing unprecedented demand for large-format interior scopes in resorts, cultural venues, and mixed-use districts[1]Timber Design & Technology, “Vision 2030 Boosts Construction Demand,” timberdesignandtechnology.com.. NEOM’s USD 5 billion DataVolt AI factory and Samsung C&T’s SAR 1.3 billion automation spending illustrate the blend of advanced manufacturing with premium finishes[2]EqualOcean, “Samsung C&T Invests SAR 1.3 Billion in NEOM Automation,” equalocean.com. Red Sea Global’s 12 eco-luxury resorts, all running on renewable power, oblige designers to integrate net-zero solutions without sacrificing five-star aesthetics. King Salman Park’s 400,000 m² Royal Arts Complex plus 16 hotels extend interior opportunities well into the next decade. Together, these projects let firms scale specialized teams in ultra-luxury hospitality, themed entertainment, and regenerative design.

Record hotel pipeline boosting FF&E demand

The country’s 362,000-room target by 2030 represents USD 110 billion in capital outlays and a corresponding surge in furniture, fixtures, and equipment orders. Four Seasons will operate five Saudi properties, including AMAALA’s 220-key wellness resort with 26 branded residences, reinforcing the premium orientation. Geographic clustering in Riyadh and the emerging NEOM corridor allows procurement hubs to streamline logistics across simultaneous projects. AMAALA Phase One alone adds 2,000 keys across 12 resorts, underpinning high-volume fit-out contracts that reward firms adept at value engineering luxury specifications. Compliance with SBC 601 energy-conservation rules further differentiates design studios that can integrate efficient MEP solutions without compromising guest experience.

Retail “experience economy” driving mall and F&B fit-outs

The Avenues Riyadh’s USD 1.2 billion immersive mall prototype signals the pivot from commodity retail toward experiential destinations that merge dining, entertainment, and culture. Developers commission extensive wayfinding, interactive media walls, and flexible zones that evolve with fast-changing consumer behavior. Downtown Design Riyadh, debuting in May 2025, positions the Kingdom as a sourcing hub for premium interior products by connecting global brands with local projects. Retail interiors command SAR 13,000-19,000 per m² for upscale restaurants, preserving design firm margins even amid material cost inflation. The segment’s 4.98% CAGR hinges on younger consumers’ appetite for social, Instagrammable spaces that fuse technology, storytelling, and hospitality-grade finishes.

Residential mortgage reforms unlocking mid- and high-end renovations

Mortgage lending reached SAR 10.06 billion in November 2024, with apartment financing up 60.6% year-on-year, expanding the pool of renovation clients. Subsidized loans at 3.5-4.5% interest and 90% loan-to-value ratios aim for 70% national homeownership by 2030. Luxury villa prices at SAR 7,500-10,000 per m² in prime Riyadh districts provide generous interior budgets, especially as developers pass 70-80% of construction cost increases to buyers. Foreign ownership reforms widen demand further, drawing capital from the wider GCC and Europe into prestige neighborhoods. Concentrated price appreciation in North Riyadh promotes neighborhood-focused design studios that optimize sourcing and workforce deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labour shortages in advanced interior trades & software | -0.9% | National, with acute impact in Riyadh, NEOM corridor | Medium term (2-4 years) |

| Payment-cycle delays on public/mega projects | -0.7% | National, with concentration on giga-projects | Short term (≤ 2 years) |

| Import-dependent premium material costs & FX volatility | -0.5% | National | Medium term (2-4 years) |

| Stringent Saudization quotas raising operating cost base | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled labor shortages in advanced interior trades and software

Thirty percent Saudization quotas for engineering firms took effect in July 2024, intensifying the hunt for locally qualified talent[3]Cercli, “Saudization Rules for Engineering Firms,” cercli.com. . Employers now incur training-plan obligations regardless of size, per the 2025 Labor Law amendments, elevating compliance overheads[4]Clyde & Co, “2025 Saudi Labor Law Amendments,” clydeco.com. BIM and VR adoption give digitally fluent firms like Nesma Group a competitive edge via clash-free coordination and modular fabrication. Conversely, studios lacking digital depth face project delays, cost overruns, and reduced qualification scores on giga-project tenders. Visa caps for foreign specialists compound the bottleneck in artisanal trades critical to ultra-luxury fit outs.

Payment-cycle delays on public and mega projects

About 31.6% of Saudi construction jobs encountered payment disputes in 2024, hampering contractor cash flow. NEOM has documented lags in reimbursements to suppliers, while the Civil Code’s bar on interest precludes compensation for late payment. A peer-reviewed MDPI study validated payment delay as a systemic risk to schedule adherence and firm solvency. Interior design firms must finance sizable up-front commitments for materials and specialist labor before milestone billing. As a result, capital-strong enterprises gain share, and niche boutiques increasingly partner with or are acquired by larger groups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Hospitality Dominance Drives Premium Positioning

Hospitality and Leisure controlled 34.48% of the Saudi Arabia interior design market in 2025, mirroring the Kingdom’s tourism diversification thrust. Five-star operators such as Four Seasons, Mandarin Oriental, and Rosewood line up to anchor giga-projects, locking in multi-property design frameworks that span guestrooms, branded residences, and holistic wellness centers. Retail and F&B, scaling at a 4.76% CAGR, benefits from mall developers’ focus on immersive dining districts that blur the boundary between gastronomy and entertainment. Commercial offices follow Vision 2030’s financial-services ambitions, while healthcare interiors track demographic growth and medical tourism inflows. Industrial, logistics, and educational facilities under the “Others” cluster advance modernization mandates, offering stable, specification-led workstreams.

Design firms specializing in hospitality secure deeper vendor discounts and standardized FF&E packages that accelerate delivery across multi-phase programs. Retail fit-out specialists co-create wayfinding and experiential touchpoints with international lifestyle brands seeking regional traction. Corporate occupiers add collaborative hubs that reflect hybrid-work preferences, prompting demand for acoustic zoning, modular furniture, and biophilic accents. Healthcare interiors pivot toward patient-centric layouts that combine infection control protocols with hotel-like amenities to attract overseas clientele. Industrial and educational projects adopt durable, low-maintenance materials, generating predictable, volume-based orders that balance portfolios heavy on ultra-luxury hospitality.

By Project Type: New Build Leadership with Renovation Acceleration

New Build accounted for 60.78% of the Saudi Arabia interior design market in 2025, fueled by giga-projects such as NEOM, Red Sea Global, and Qiddiya. These master-planned clusters compress decades of construction into bold timelines, making end-to-end design-build partnerships more common. Massive square-footage demands let interior firms secure bulk procurement, optimize logistics, and experiment with modular assemblies that mitigate site constraints. Nevertheless, Renovation and Remodel, while smaller today, will rise at a 4.94% CAGR, sustained by mortgage lending booms, foreign ownership relaxation, and escalating asset repositioning among aging commercial properties. The renovation share also benefits from SBC convergence updates that trigger retrofits for energy efficiency, accessibility, and smart-building readiness.

Renovation contractors excel in phasing work around occupied premises, leveraging night shifts and prefabricated elements to limit downtime. Developers allocate retrofit budgets to refresh public areas, introduce digital check-in kiosks, and expand co-working lounges that monetize underutilized space. High-net-worth homeowners invest in extension kitchens, spa bathrooms, and walk-in wardrobes that raise property valuations. Commercial landlords refurbish to win ESG-conscious tenants, prioritizing LED lighting, low-VOC materials, and sensor-driven HVAC controls. The duality of green-field grandeur and brown-field agility positions diversified design houses to smooth revenue cycles across interest-rate swings.

By Price Tier: Luxury Leadership with Ultra-Luxury Emergence

Luxury interiors held 41.02% share in 2025, reflecting both local buying power and the country’s status as a high-profile visitor destination. finishes include imported marbles, bespoke bronze fixtures, and artisan woodwork that push project budgets well above regional averages. Ultra-Luxury, forecast to climb 5.56% yearly, targets UHNW clients via NEOM’s Magna and Sindalah enclaves, AMAALA’s wellness retreats, and repurposed royal palaces. Economy and Mid-Range tiers serve middle-class housing expansion, factory-built hotels, and public-sector facilities that prioritize durability over opulence. The price-tier split lets firms recalibrate resource allocation, from cost-engineered modular rooms to one-off couture suites clad in hand-tooled Saudi stucco.

Ultra-Luxury mandates hospitality suites with dedicated spa circuits, panoramic glass elevators, and immersive art installations driven by advanced projection mapping. Luxury remains a volume driver in airport hotels, branded residences, and corporate headquarters that broadcast status without straying into extravagance. Mid-Range projects leverage global standard-brand prototypes adapted to local cultural cues, offering steady pipelines ideal for mid-cap contractors. Economy interiors maximize off-site fabrication to reduce on-site labor, making them attractive for speed-to-market strategies in secondary cities. Material sourcing strategies bifurcate: local content rules lift domestic quarry output for stone, while ultra-luxury owners still import rare Italian Calacatta and French Lapis Lazuli slabs.

Geography Analysis

Riyadh Metropolitan registered 37.76% share of the Saudi Arabia interior design market in 2025, energized by SAR 75 billion of infrastructure outlays tied to EXPO 2030. King Salman Park’s green heart hosts 16 hotels, galleries, and an opera house, cementing long-term cultural demand. The capital’s luxury home segment grew 10.7% in 2024, spurring boutique studios to establish micro-offices in North Riyadh for faster site supervision. King Salman International Airport’s USD 7.2 billion expansion aims for 120 million annual passengers, triggering terminal interior redesigns aligned with seamless biometric travel. Large mixed-use schemes such as Diriyah Gate’s heritage precinct require meticulous integration of Najdi motifs into modern hospitality settings.

Makkah Province, encompassing Jeddah and Mecca, rides a dual engine of religious tourism and Red Sea leisure developments. Jeddah Tower’s resumed works involve SR 712 million of fresh structural investment, reviving super-tall interior packages for observation decks and VIP lounges. The Islamic Arts Biennale 2025 showcased date-palm-based modular musallas, signaling potential for sustainable regional materials in mainstream interiors. Coastal resorts see demand for coral-inspired palettes that respect environmental guidelines while captivating affluent divers and yachting enthusiasts. Logistics-centric Dammam accelerates industrial office fit-outs alongside staff accommodations that comply with enhanced worker welfare norms.

Medina and the North-West NEOM corridor represent the fastest-growing cluster at 5.12% CAGR, amplified by the USD 5 billion DataVolt facility and Samsung C&T’s automation hub. NEOM’s Shebara resort features floating villas with transparent under-sea observation decks, pushing designers to merge marine-grade engineering with five-star luxury. Aquellum’s inverted skyscraper concept adds subterranean yacht berths and sky-bridge retail arcades, spawning novel lighting and ventilation solutions. Medina’s heritage redevelopment aligns with faith-based tourism, requiring respectful restoration that blends Islamic calligraphy with smart-building controls for crowd management. Southern Asir’s “Summer Tourism” program and Northern Tabuk’s coastal projects extend interior demand into emerging micro-markets.

Regulatory Landscape

Saudi Arabia interior design and fit-out activity is shaped by product compliance and import controls overseen by the Saudi Standards, Metrology and Quality Organization (SASO). Furniture and related interior products commonly route through the SALEEM Saudi Product Safety Programme using the SABER electronic conformity platform, where importers obtain a Product Certificate of Conformity (PCoC) and Shipment Certificate of Conformity (SCoC) for regulated items. Labeling expectations, including Arabic labeling, and test-based requirements for items such as upholstered products create a compliance gate that affects specification choices, approved supplier lists, and procurement lead times for hospitality and retail projects.

On cross-border movement, the Zakat, Tax and Customs Authority (ZATCA) administers customs processes and tariffs, including the GCC move to an integrated 12-digit HS-based customs tariff system effective January 1, 2025, which raises the need for accurate classification of FF&E. Import documentation is increasingly digitized in the clearance workflows, and Saudi ports introduced a palletization requirement for containerized imports effective May 8, 2025, affecting packaging, consolidation, and site delivery planning for bulky furniture and finishing materials. Sector development and professional direction also link to government bodies such as the Architecture and Design Commission under the Ministry of Culture, which supports broader architecture and interior design through sector programs and initiatives.

Value Chain Analysis

The value chain starts with client-side demand from hospitality developers, retail landlords, residential owners, and government-linked entities, followed by concept design, design development, and design management services, then detailed coordination for MEP, life-safety, and code compliance. Delivery typically moves into tendering and subcontractor selection (fit-out contractors, joinery, MEP specialists, lighting, AV, and façade interface trades), then procurement of FF&E and finishing materials, manufacturing or fabrication (local joinery workshops and regional suppliers alongside imports), installation, commissioning, and handover. Digital workflows such as BIM and project permitting systems are increasingly embedded upstream, reducing revision cycles and supporting multi-site rollouts.

Sourcing and logistics are the most cost- and schedule-sensitive part of the chain because premium finishes and branded FF&E depend on imports. SASO conformity steps via SABER, ZATCA tariff classification, and port handling requirements directly influence timelines. Localization and procurement policy also shape channel choices, including public procurement local-content requirements that encourage local manufacturing, assembly, or partnering with Saudi fit-out contractors. Industrial financing and capacity programs support domestic furniture and wood products expansion, while residential pipeline visibility through national housing programs and platforms helps suppliers and design-build firms align procurement hubs, warehousing, and installation sequencing across multiple developments.

Competitive Landscape

International studios such as HKS, Foster + Partners, and Wilson Associates compete alongside domestic champions like Dar Al Riyadh and Godwin Austen Johnson, creating a moderately fragmented Saudi Arabia interior design market. Firms differentiate through mastery of Saudi building codes, track record on giga-projects, and the ability to absorb lengthy payment cycles without compromising quality. Digital design leadership matters; Nesma Group’s BIM-enabled modular MEP contributes to clash-free installs that shave weeks off schedules. Sustainability credentials also command premiums, as Red Sea Global mandates LEED Gold or above for hospitality interiors. Meanwhile, Saudization quotas reshape human-capital strategies, encouraging joint ventures that pair overseas design intellect with on-ground Saudi execution.

Cash-rich conglomerates increasingly acquire boutique studios to secure niche skills in ultra-luxury, wellness, or cultural restoration. Foreign brands partner with local fit-out contractors to navigate procurement regulations and Arabic documentation requirements. Procurement consortia improve foreign-exchange hedging for imported premium materials, mitigating cost spikes that climbed 6-8% annually between 2024 and 2025. Value-chain integration, from concept design through furniture manufacturing—emerges as a hedge against supply uncertainty, illustrated by Al-Mismari Group’s new Riyadh joinery plant. Overall, scale, technology, and regulatory fluency outrank lowest-price bids as decisive factors in tender awards.

White-space opportunities surface in retrofitting heritage sites for boutique hospitality, embedding biophilic elements in high-rise offices, and deploying circular-economy materials such as recycled aluminum partitions. ESG-savvy institutional investors seek design partners that can quantify embodied carbon savings and track material provenance. The rise of branded residences tied to hotel operators blurs the residential-hospitality boundary, deepening integration of concierge-style amenity interiors into private units. Payment-risk management remains vital; larger entities negotiate milestone-based advances or micro-certifications to sustain cash flow. Market share is expected to tilt toward firms that marry cultural authenticity with modern efficiency across the next investment cycle.

Saudi Arabia Interior Design Industry Leaders

Dar Al Riyadh

Havelock One Interiors

Depa Interiors Saudi

AMAQ Interiors

A&T Group Interiors

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace centers on aligning interior design services with Saudi Arabia's large construction and housing delivery cadence, while reducing delivery risk from imported FF&E. The Housing Program and related residential build-out create recurring demand for standardized, repeatable interior packages (mid-range to luxury) that can be rolled out across clusters. Off-plan unit launches through platforms such as Sakani also increase the need for fast-turn, specification-driven fit-out options and homeowner upgrade programs. Construction momentum in 2026 is supported by the Alrajhi Capital Saudi Construction Index reaching 56.3 in June 2026, which sustains active bidding environments for interior scopes across residential and infrastructure-linked projects.

A second opportunity area is supply chain localization and industrialized fit-out, driven by local-content mandates, customs and conformity requirements, and schedule pressure on mega and mixed-use developments. Corporate investment provides a concrete anchor, with Emirates Stallions Group (via Vision Furniture & Decoration Factory) securing a 16-year agreement for 13,000 sqm of warehouse space in Saudi Arabia (May 2025), reflecting a strategy to expand localized production and staging to shorten lead times for furniture and interior packages. Government-backed industrial positioning also supports higher-value offerings, including smart, automated manufacturing and modular interior components, evidenced by the Ministry of Industry and Mineral Resources awarding "Factory of Future" status to Saudi Emaar Furniture & Design. Domestic manufacturers such as Qnadeel Furniture highlight local capacity for doors, wall panels, and institutional furniture that can be specified into government and large private programs.

Recent Industry Developments

- April 2026: Depa PLC reported receiving rights issue proceeds following regulatory admission, aligning with growth initiatives across its regional interior solutions operations, including activity tied to Saudi Arabia. Additional capital supports working-capital needs and capacity planning for long-cycle projects where materials and specialist labor must be financed ahead of milestone payments. The move coincides with a market environment where balance-sheet strength informs prequalification and delivery reliability on mega-project programs.

- May 2025: Emirates Stallions Group via Vision Furniture & Decoration Factory secured a 16-year agreement for 13,000 sqm of warehouse space in Saudi Arabia, underscoring investment in localized production and staging that can shorten lead times for furniture and interior packages. The arrangement signals continued localization of the interior supply chain to support large-scale residential and mixed-use developments.

- June 2024: Dar Al Riyadh was awarded a design services contract by the Royal Commission for Jubail and Yanbu, expanding its involvement in government-led development workstreams. The contract supports sustained demand for Saudi code-fluent design management and coordination capabilities across multiple assets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers paid interior design services delivered within Saudi Arabia for indoor environments, where design work supports function, safety needs, and the look and feel of spaces.

Scope exclusions: We exclude furniture and decor product sales, construction contracting, and pure architectural design fees when they are not part of a defined interior design service engagement.

Segmentation Overview

- By End User

- Residential

- Commercial Office

- Hospitality and Leisure

- Retail and F&B

- Healthcare

- Others (Industrial & Logistics, Education etc.)

- By Project Type

- New Build

- Renovation / Remodel

- By Price Tier

- Economy

- Mid-Range

- Luxury

- Ultra-Luxury

- By Region

- Riyadh Metropolitan

- Makkah Province (incl. Jeddah, Mecca)

- Eastern Province

- Medina and North-West (NEOM corridor)

- Southern Region (Asir)

- Northern and Central Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the starting structure for demand and to anchor assumptions that can be checked later. We mainly relied on public and official sources such as Saudi Arabia's General Authority for Statistics, the Ministry of Municipal and Rural Affairs and Housing, the Saudi Central Bank, and Customs or trade statistics for imported interior materials that influence renovation activity.

To keep the model grounded, we also referenced construction and real estate project announcements from government programs, plus standards and guidance that affect interior specifications (for example, Saudi Building Code related releases). Alongside these, we reviewed company annual reports, investor presentations, and reputable press coverage for signals on project pipeline, pricing changes, and hiring. Paid subscriptions were used only where needed for company financials and intelligence, news and financials, import export shipment-level checks, and patent databases for tracking design and materials activity. The sources listed here are illustrative, and many other public documents were also used for cross-checking and clarification.

Primary Interviews and Surveys

Primary work focused on validating how design fees are priced and how project volumes are shifting across residential and commercial interiors in Saudi Arabia. We spoke with a mix of design firms, fit-out ecosystem participants, project consultants, and buyer-side stakeholders, and the discussion was used to test utilization, typical project cycles, and how regional demand differs across the Kingdom.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 19% | |

| Mid tier: 44% | Functional/Unit leaders: 32% | |

| Smaller Players: 19% | Managers: 49% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool built from Saudi construction and real estate activity, which is then translated into interior design service spend using penetration and fee-rate assumptions by end-use. The totals are subsequently corroborated with selective bottom-up approximations, where sampled project counts and typical design fee ranges are applied to validate the overall value and adjust outliers.

Key inputs used in the model include non-residential project pipeline intensity (hospitality, offices, healthcare, and education), residential unit delivery and renovation propensity, average design fee as a percent of interior budgets, price tier mix shifts, and regional concentration of projects (for example, higher activity in large metro areas). When interview feedback showed that project awards were being delayed or phased, the volume assumptions were softened and then rechecked against broader construction signals.

For forecasting, scenario analysis is used so that demand can be flexed based on how quickly major developments move from planning to execution and how pricing changes with labor and materials conditions. Where bottom-up checks had gaps, we filled them using conservative ranges for fee rates and project frequency, and then kept the final total within the limits suggested by independent indicators and expert feedback.

Data Validation & Update Cycle

Validation is done through a set of stepwise checks before values are finalized. Outputs are compared against independent signals such as construction spending direction, project award momentum, and reported revenue trends for relevant service providers, and then any large variances are reviewed and corrected with documented assumption changes.

A second analyst review is completed to test math logic, year-to-year continuity, and reasonableness of pricing and volume movement. If new information creates a material change in project flow or fee behavior, respondents are re-contacted to confirm the direction and size of the shift. Reports are refreshed annually, and interim updates are made when major events meaningfully impact demand, after which a fresh final pass is completed right before delivery.

Mordor Intelligence's Saudi Arabia Interior Design Market Size Measured Against Other Published Estimates

Published market values for Saudi Arabia interior design often differ because firms do not measure the same thing, even if the title looks identical. The gaps typically come from what is counted as a service, which year is treated as the base, and how project timing and pricing are converted into a single USD value.

Some external estimates broaden the scope by mixing interior design fees with interior fit-out execution and related product spending. For Mordor Intelligence, only interior design service revenue delivered in Saudi Arabia is counted, and adjacent contracting and product sales are left out so the value stays tied to service activity.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.87 B (2025) | |

| Regional Consultancy A | USD 4.09 B (2024) | Uses a different base year and appears to blend design with a wider set of interior project spending, which can lift the reported value when fit-out and furnishings are implicitly included. |

| Industry Publisher B | USD 4.10 B (2025) | Leans on aggressive project ramp-up assumptions and a faster price progression, and the estimate is less transparent on how delayed or phased developments are treated in annual spend. |

The table shows that year selection and what sits inside the scope explain most of the spread in values. When service-only revenue is isolated and then checked against project activity and realistic fee ranges, the result is easier to trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the Saudi Arabia interior design market in 2031?

Forecasts indicate the market will reach USD 4.99 billion by 2031, reflecting a 4.32% CAGR from 2026 levels.

Which end-user segment currently contributes the most revenue?

Hospitality and Leisure contributes the largest share at 34.48%, bolstered by the record hotel pipeline.

Where is the fastest regional growth expected?

The Medina and North-West NEOM corridor shows the quickest expansion, with a projected 5.12% CAGR through 2031.

How are Saudization quotas affecting design firms?

Quotas mandate 30% Saudi staff in engineering teams, raising recruitment costs and accelerating investment in training programs.

What are the main restraints on market growth?

Skilled labor shortages and payment-cycle delays on public mega-projects exert the strongest downward pressure on the sector’s CAGR.

Which price tier is expanding most rapidly?

The Ultra-Luxury tier is growing at 5.56% annually as giga-projects target ultra-high-net-worth visitors and residents.

Page last updated on: