Saudi Arabia Industrial Electrical Components Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

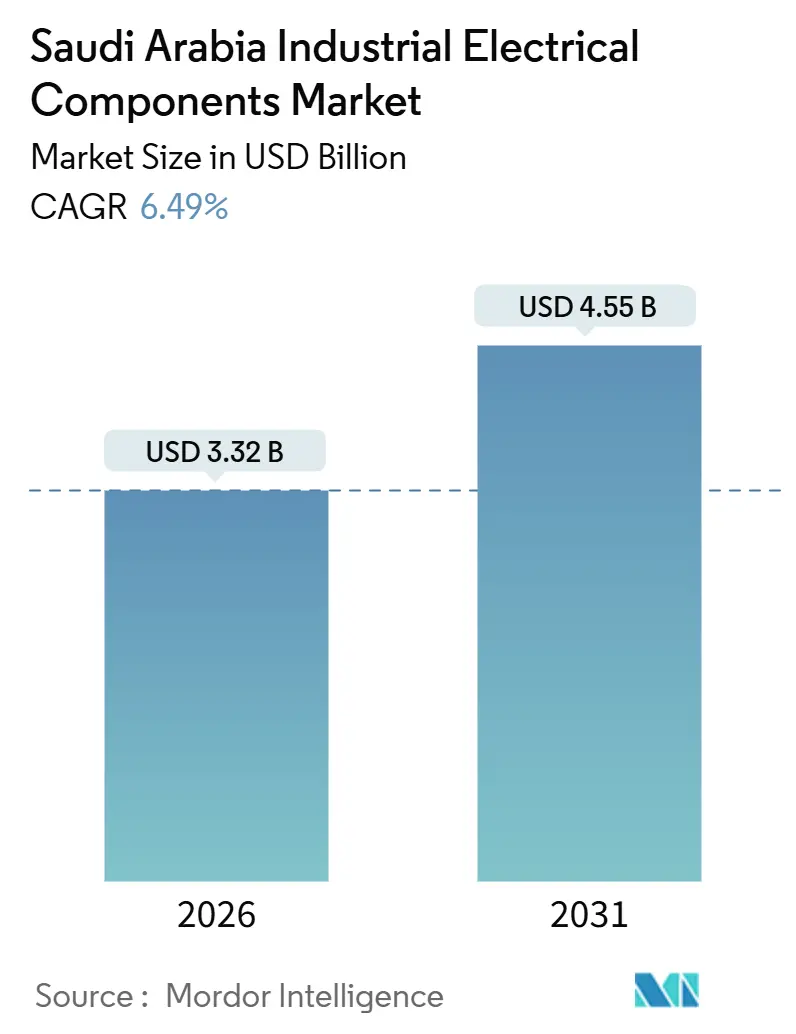

| Market Size (2026) | USD 3.32 Billion |

| Market Size (2031) | USD 4.55 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

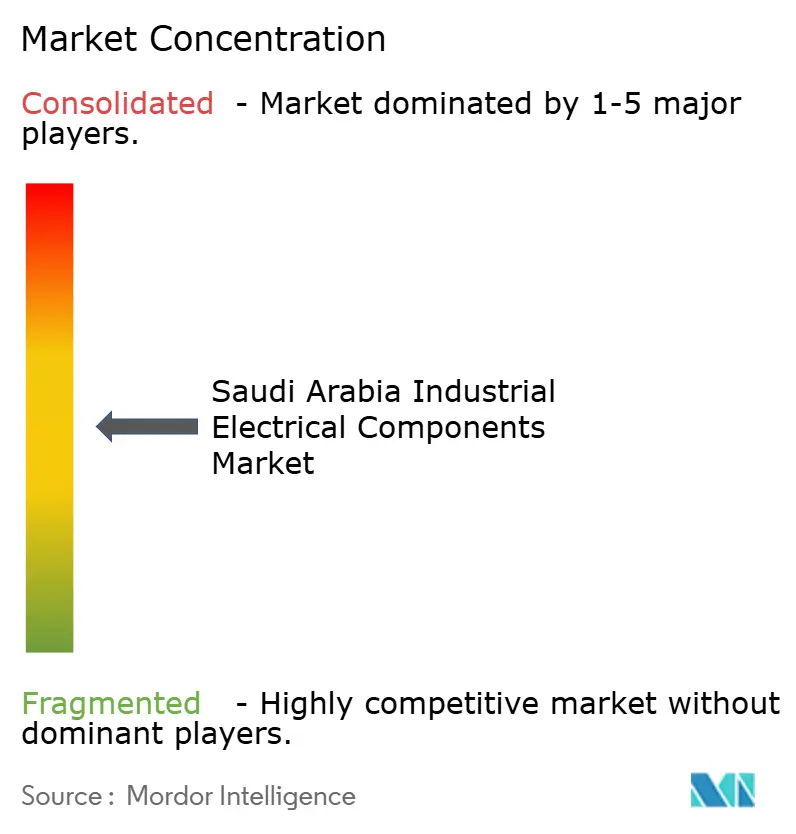

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Industrial Electrical Components Market Analysis by Mordor Intelligence

The Saudi Arabia Industrial Electrical Components Market size is estimated at USD 3.32 billion in 2026, and is expected to reach USD 4.55 billion by 2031, at a CAGR of 6.49% during the forecast period (2026-2031).

Vision 2030 megaprojects, grid-digitalization mandates, and sovereign manufacturing targets are lifting baseline demand, while data-center build-outs introduce new power-quality specifications that favor intelligent switchgear.[1]NEOM, “Vision 2030 Projects,” NEOM, neom.com Local content requirements under IKTVA are reshaping sourcing models as utilities ask for 70% Saudi value addition, creating room for regional fabricators to scale alongside multinationals. At the same time, the phased rollout of smart meters and substation automation is accelerating replacement cycles for legacy electromechanical devices.[2]Saudi Electricity Company, “Annual Report 2024,” Saudi Electricity Company, se.com.sa Supply-chain exposure to copper and grain-oriented steel remains the key cost headwind, but vertical integration moves such as Elsewedy Electric’s Yanbu copper-rod plant are mitigating price swings.

Key Report Takeaways

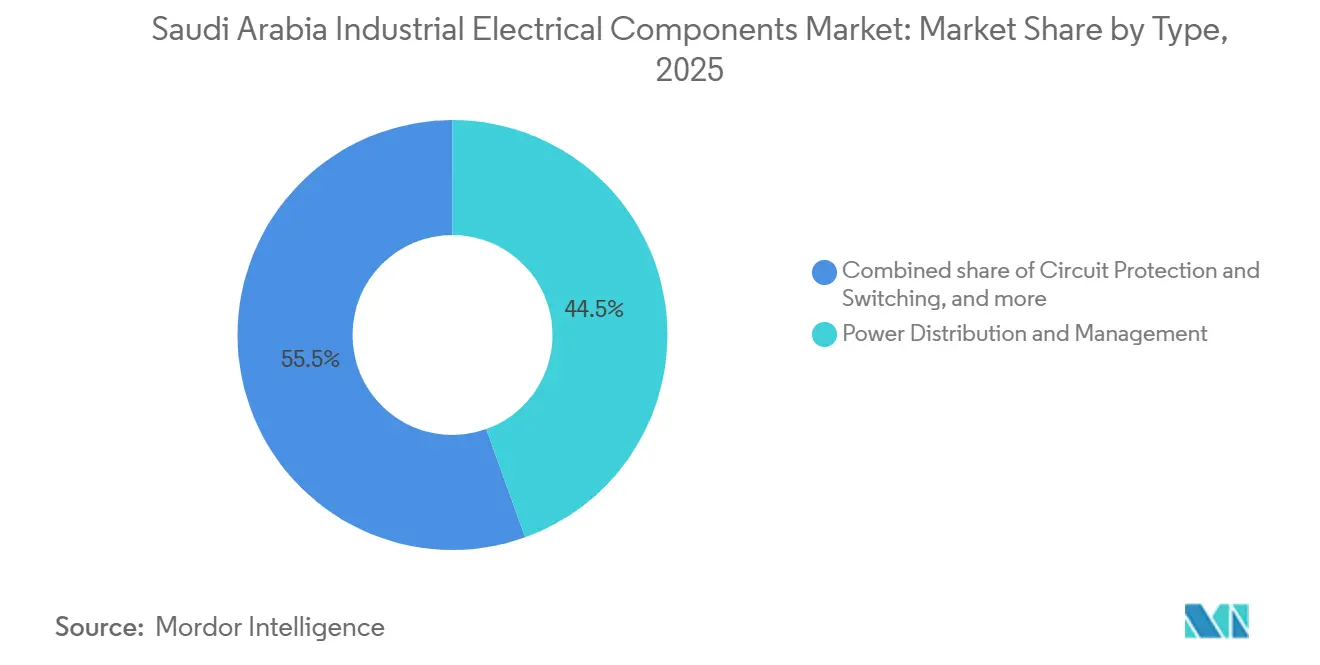

- By type, power distribution and management led with 44.5% revenue share in 2025, while circuit protection and switching is tracking a 7.6% CAGR to 2031.

- By voltage class, low-voltage equipment held 50.1% of 2025 demand, yet high and extra-high voltage gear is forecast to expand at an 8.1% CAGR through 2031.

- By installation environment, indoor deployments dominated with 79.9% share in 2025; outdoor equipment is advancing at a 7.7% CAGR through 2031.

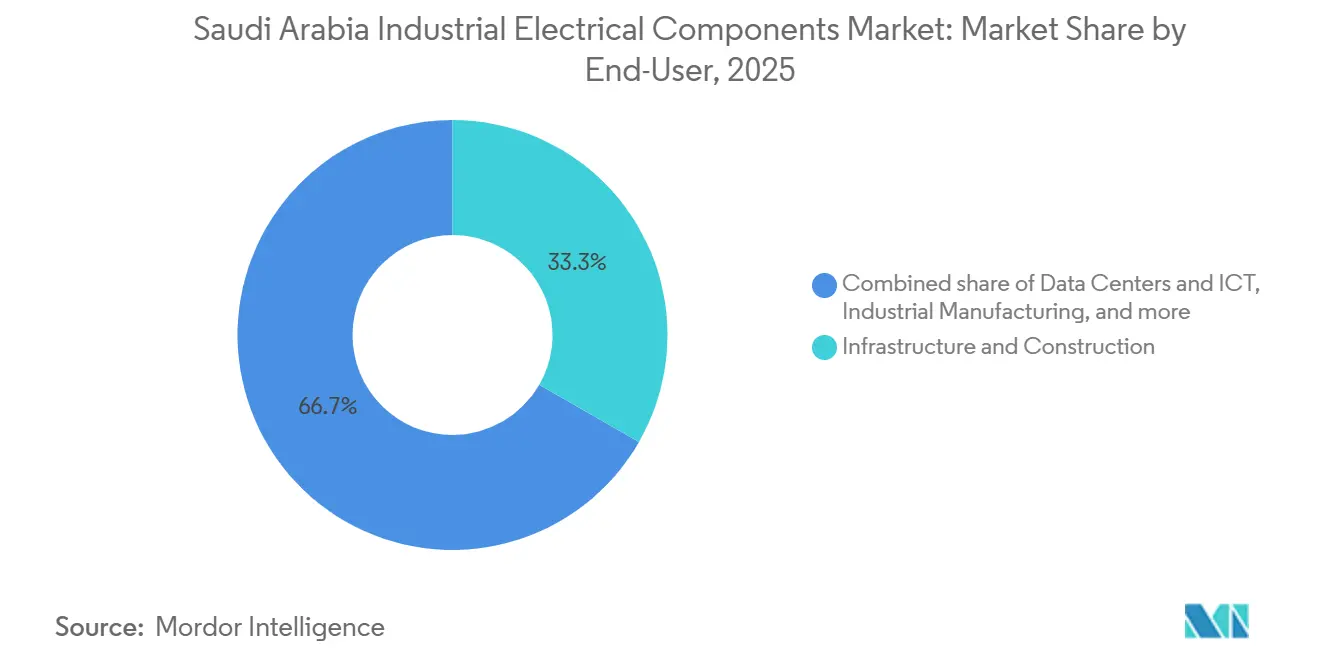

- By end-user, infrastructure and construction absorbed 33.3% of 2025 revenue, whereas data centers and ICT exhibit the fastest 9.5% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Saudi arabia representing one among them. The global report on industrial electrical component market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Saudi Arabia Industrial Electrical Components Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 mega-projects pipeline | 1.8% | National, concentrated in NEOM, Red Sea, Qiddiya, Diriyah Gate, with spillover to Tabuk and Western regions | Medium term (2–4 years) |

| Grid digitalization and smart-meter rollout by SEC | 1.5% | National, with early gains in Riyadh, Jeddah, Dammam metropolitan areas, expanding to 500 rural villages | Short term (≤ 2 years) |

| Data-center boom (hyperscale and colocation) | 1.4% | National, anchored in NEOM, Riyadh, Jeddah, with emerging clusters in Eastern Province | Medium term (2–4 years) |

| Hydrogen and green-ammonia export hubs | 1.2% | NEOM, Ras Al-Khair, Jubail Industrial City, with transmission infrastructure extending to Northern Borders | Long term (≥ 4 years) |

| In-Kingdom localization (IKTVA and Made-in-Saudi) push | 1.1% | National, with manufacturing clusters in Riyadh Industrial City, Yanbu, Jubail, Dammam Second Industrial City | Medium term (2–4 years) |

| Downstream petrochemical and midstream gas capacity build-out | 0.9% | Eastern Province (Jafurah, Jubail, Ras Al-Khair), with ancillary infrastructure in Northern and Central regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Mega-Projects Pipeline

The USD 500 billion NEOM program, The Line’s 170 km linear city, and Qiddiya’s entertainment cluster are staging multi-year procurement waves that reward vendors able to stock inventory in desert and coastal hubs.[3]NEOM, “Vision 2030 Projects,” NEOM, neom.com The Red Sea Project’s 400 MW solar array paired with 1.3 GWh storage, commissioned in 2024, highlights demand for bi-directional inverters and real-time grid-forming controls.[4]Red Sea Global, “Microgrid Commissioning,” Red Sea Global, redseaglobal.com Diriyah Gate is specifying single-IP building-automation backbones, accelerating uptake of Ethernet-enabled contactors and IoT sensors. Peak procurement impact arrives in 2027–2028 when civil works flip to fit-out phases, lifting the Saudi Arabian industrial electrical components market during those years. Automated cranes at the Port of NEOM, powered exclusively by renewables, eliminate diesel gensets and require redundant UPS systems, pushing suppliers toward modular architectures.

Grid Digitalization and Smart-Meter Rollout by SEC

Saudi Electricity Company installed 10 million smart meters by 2024 and targets 40% grid automation by 2025, driving rapid relay and SCADA upgrades. Capital outlays of SAR 60 billion in 2024 and SAR 47.4 billion in H1 2025 prioritized distribution automation and digital substations. Siemens’ SAR 2.3 billion award is bringing edge-computing substations that cut unplanned outages by 25%. ABB’s SAR 1.9 billion contract introduced modular protection relays that slash commissioning time by 30%. Short-term uplift ends once SEC meets its 2025 automation milestone, but the follow-on 70% coverage plan through 2030 keeps the Saudi Arabia industrial electrical components market on a steady replacement path.

Data-Center Boom

AWS’s USD 5.3 billion commitment, DataVolt’s USD 5 billion NEOM facility, and a wider USD 21 billion pipeline demand 99.999% uptime with N+2 redundancy. Each hyperscale hall consumes 20 – 50 MW, requiring harmonic-filtering switchgear and intelligent PDUs with per-outlet metering. Google and Microsoft are reviewing Riyadh and Jeddah colo options, spurring orders for liquid-cooled busbars that trim copper mass 40%. Medium-term demand peaks 2026–2028 as operators commission backup diesel generators and 15-minute ride-through battery storage, injecting further momentum into the Saudi Arabia industrial electrical components market. ENOWA is integrating 4 GW of renewables plus 2 GW electrolysis load, turning NEOM into a sandbox for synthetic inertia algorithms that will shape future data-center designs.

Hydrogen and Green-Ammonia Export Hubs

The 600-tonne-per-day NEOM Green Hydrogen plant coming online in 2026 pulls 2 GW of electrolysis load, specifying high-current rectifiers and explosion-proof enclosures. ACWA Power and Air Products are progressing additional projects that need medium-voltage drives for continuous-duty compressor trains. Electrolyzer stacks create a niche for DC switchgear and solid-state breakers rated at 10 kA without arcing. Long-term upside extends beyond 2031 as capacity scales toward 4 million tonnes of hydrogen, bolstering the Saudi Arabian industrial electrical components industry over the decade. Compliance with IECEx and ATEX rules narrows the supplier pool to firms with Zone 1 and Zone 2 product lines, solidifying pricing power.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (copper, steel) | -0.9% | Global, with acute impact on Saudi imports of transformers, cables, busbars, and switchgear enclosures | Short term (≤ 2 years) |

| Global supply-chain lead-time shocks | -0.7% | Global, affecting large power transformers, gas-insulated switchgear, with bottlenecks in GOES, bushings, tap-changers | Medium term (2–4 years) |

| MV-skills gap in installation and operations-and-maintenance | -0.6% | National, most acute in remote project sites (NEOM, Northern Borders, rural electrification zones) and specialized segments (BESS, HVDC) | Medium term (2–4 years) |

| SF₆-free standards obsoleting legacy inventory | -0.4% | National, with concentrated impact on utilities and industrial facilities holding SF₆-based switchgear inventory, aligned with EU phase-out timelines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Copper peaked at USD 10,845 per tonne in May 2024 before sliding 15%, compressing transformer and cable margins by up to 12 percentage points. Grain-oriented electrical steel doubled to USD 2,800 per tonne as Chinese mills diverted supply to EV motors, squeezing transformer-core producers. Elsewedy Electric’s vertical copper-rod line in Yanbu hedges costs, but smaller fabricators lacking integration are delaying expansions. Steel tariffs added 10–15% to enclosure and busbar pricing, prompting trials of aluminum alloys that face conductivity hurdles.

Global Supply-Chain Lead-Time Shocks

Delivery for large power transformers now runs 120 – 210 weeks, versus 52 – 78 weeks in 2020, as core steel, bushings, and tap-changers all suffer bottlenecks. SEC now pre-orders 132 kV and 380 kV units four years ahead, tying up USD 400 million in working capital and risking spec obsolescence. Gas-insulated switchgear faces SF₆ scarcity and higher-cost fluoronitrile substitutes. Hitachi Energy’s SAR 1.2 billion HVDC contract includes 18-month delivery clauses that force parallel civil works, lifting financing costs by 12%. Modular multi-unit transformer designs are emerging, but the footprint grows 20–25%, an awkward trade-off in dense urban substations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Transformers Anchor Revenue, Protection Devices Accelerate

Transformers and related power-distribution gear captured 44.5% of 2025 revenue as the SEC’s SAR 60 billion grid expansion and NEOM microgrids demanded large step-up units. Circuit protection and switching posted the quickest 7.6% CAGR thanks to IEC 61850 automation that bundles metering, communication, and cybersecurity in one device, trimming cabinet counts. The Saudi Arabia industrial electrical components market size for protection devices is forecast to climb steadily as distributed energy resources proliferate. Control and connectivity products benefit from Elsewedy Electric’s XLPE cable output, supplying The Line and Jafurah with 90 °C-rated conductors that withstand desert heat.

Variable-frequency drives and software-defined controllers are penetrating data centers and petrochemical plants, with Aramco’s Khurais field posting an 18% power drop after adopting IoT-enabled motor controllers. ABB’s digital substations eliminate 60% of copper cabling, allowing remote reconfiguration and lowering installation labor. Local transformer makers, Saudi Power Transformer Company and Electrical Industries Company, are adding capacity, yet imported grain-oriented steel keeps them reliant on foreign inputs, limiting their capture of the Saudi Arabia industrial electrical components market share in higher-margin protection devices.

By Voltage Class: Low Voltage Dominates, Transmission Infrastructure Surges

Low-voltage systems up to 1 kV held 50.1% of 2025 demand due to building automation, motor drives, and data-center PDUs. High and extra-high voltage gear above 40 kV is pacing an 8.1% CAGR as 27.3 GW of renewables come online and 800 km transmission corridors move power to Riyadh. The Saudi Arabia industrial electrical components market size for high voltage is expanding on the back of Hitachi Energy’s SAR 1.2 billion HVDC link, which cuts line losses by 30%.

Medium-voltage systems remain the workhorse of industrial plants, yet a skills gap persists: only 21% of TVTC electrical graduates enter field roles, delaying commissioning of 14 GWh of battery storage scheduled through 2027. Schneider Electric’s Wiser platform networks 50,000 devices per smart building, pushing low-voltage component demand. GE Vernova’s SF₆-free switchgear installed at NEOM reduces global-warming potential 99% but needs thicker insulation, raising enclosure costs. Lucy Switchgear’s ring-main units are chosen for Riyadh pilots, slicing customer-minutes-lost by 40%.

By Installation Environment: Indoor Facilities Lead, Outdoor Networks Expand

Indoor settings drove 79.9% of 2025 sales, reflecting data-center and manufacturing concentration within climate-controlled halls. Outdoor gear is still on a 7.7% CAGR as utilities stretch medium-voltage feeders into remote desert zones where ambient temperatures top 50 °C. The Saudi Arabia industrial electrical components industry is adopting IP65-rated inverters and UV-stabilized cables for the 400 MW Red Sea solar microgrid.

DataVolt’s 1.5 GW NEOM campus exemplifies indoor complexity, requiring raised-floor PDUs and liquid-cooled busbars that cut copper 40%. Outdoor deployments face salt fog and sand ingress, so META Switchgear and GEDAC Electric use silicone-rubber seals that triple maintenance intervals. Aramco’s Jafurah field adds explosion-proof starters for Zone 1 hazards. SEC’s rural electrification program demands pole-mounted transformers with lightning arresters, widening the customer base for outdoor-rated components.

By End-User: Infrastructure Leads, Data Centers Surge

Infrastructure and construction absorbed 33.3% of 2025 revenue as Vision 2030 megaprojects dominated tender books. Data centers and ICT, however, are riding a 9.5% CAGR fueled by AWS, DataVolt, and sovereign AI mandates, cementing future growth for the Saudi Arabia industrial electrical components market. Oil and gas remains a stable anchor with Aramco’s 2.2 TCF Jafurah program specifying hazardous-area gear.

Industrial manufacturing gains from IKTVA localization as transformer and cable assembly plants rise, though imported core steel and SF₆ still limit domestic value capture. Commercial and hospitality projects like Diriyah Gate favor silent amorphous-core transformers that cut no-load losses by 70%, meeting LEED noise limits. Sovereign AI and green-ammonia programs add specialized demand for 480 V DC distribution and high-current rectifiers, diversifying the customer portfolio.

Geography Analysis

Eastern Province, Riyadh, and Mecca regions together accounted for roughly 65% of 2025 demand as petrochemical clusters in Jubail and Yanbu, government construction in Riyadh, and religious-tourism infrastructure in Mecca drove procurement. NEOM’s Tabuk location is emerging as a fourth pole, securing 12% of incremental spend between 2026 and 2031 as The Line, the solar microgrid, and green-hydrogen facilities come online. The Eastern Province gains further impetus from Aramco’s Jafurah gas field, which specifies explosion-proof motor drives and hydrogen-resistant cables.

Riyadh’s data-center corridor, anchored by AWS, requires modular UPS systems and intelligent PDUs that allow per-rack metering. The Western Region, encompassing Jeddah, benefits from the Red Sea Project and Diriyah Gate, both of which adopt prefab wiring harnesses that cut labor by 30%. SEC’s rural electrification extends 33 kV lines to 500 villages, but transformer lead times of up to 210 weeks delay substation energization, revealing logistical bottlenecks.

The Northern Borders renewable hub added 9.2 GW of solar and wind in 2024 and has 27.3 GW under development, demanding HVDC links to southern load centers. SASO compliance remains mandatory, favoring firms with in-country testing facilities. Qiddiya’s theme-park systems require IP65 outdoor enclosures with stainless fasteners suited to 50 thunderstorm days per year, narrowing qualified suppliers.

Competitive Landscape

Global multinationals, ABB, Siemens, Schneider Electric, and Hitachi Energy, captured about 45% of 2025 revenue through large grid and megaproject orders, while local champions Al-Fanar, Electrical Industries Company, and Saudi Power Transformer Company leveraged IKTVA to secure roughly 30% in transformers, switchgear, and cables. The remaining 25% is split among regional specialists targeting hazardous-area enclosures, data-center PDUs, and building-automation components. Multinationals are embedding digital twins and predictive analytics into hardware packages, creating switching costs that elevate their stickiness with utilities.

Local fabricators are expanding assembly capacity ahead of the 70% localization deadline, but dependency on imported core steel and SF₆ limits full margin capture. Elsewedy Electric’s vertical copper integration and DataVolt’s adoption of 480 V DC corridors exemplify disruptive moves that realign technical standards. IEC 61850 adoption is squeezing single-function relay makers as utilities consolidate protection, metering, and cybersecurity into multifunction devices.

CG Power and Eaton gain share in medium-voltage soft starters by offering local warranties, yet their smaller installed base hinders bids for turnkey HV substations. White-space opportunities include SF₆-free switchgear, solid-state DC breakers, and modular transformers that halve delivery time. Suppliers with proven performance in 50 °C climates and Zone 1 hazards keep a defensible moat as Saudi buyers raise technical bars.

Saudi Arabia Industrial Electrical Components Industry Leaders

GEDAC Electric Company

TIEPCO

Al-Abdulkarim Holding (AKH) Co.

Saudi Power Transformer Company

Saudi Electric Supply Company Limited (SESCO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Amazon Web Services (AWS) and Saudi AI firm HUMAIN have announced an investment exceeding USD 5 billion to establish an AI Zone in Saudi Arabia.

- February 2025: DataVolt began building its USD 5 billion, 1.5 GW data-center campus in NEOM, specifying 480 V DC power distribution and liquid-cooled busbars that cut copper mass 40%

- March 2024: AWS has announced plans to invest over USD 5.3 billion to establish a new cloud region in Saudi Arabia by 2026. This initiative will include multiple data center Availability Zones, necessitating significant electrical industrial components such as power distribution systems, backup systems, cooling solutions, and switchgear.

Saudi Arabia Industrial Electrical Components Market Report Scope

The Industrial Electrical Component Market encompasses the production, distribution, and maintenance of electrical devices designed to control, protect, distribute, and monitor electrical power in industrial and commercial settings. These components play a critical role in ensuring the safe, reliable, and efficient operation of machinery, processes, and electrical systems.

The Saudi Arabia industrial electrical components market is segmented into type, voltage class, installation environment, end-user, and geography. By type, the market is segmented into circuit protection and switching, power distribution and management, control and connectivity, and other types. By voltage class, the market is divided into low voltage, medium voltage, and high/extra-high voltage. By installation environment, the market is divided into indoor and outdoor. By end-user, the market is divided into oil and gas, industrial manufacturing, infrastructure and construction, data centers and ICT, commercial and hospitality, and other end-users. The market forecasts are provided in terms of value (USD).

| Circuit Protection and Switching | Circuit Breakers |

| Switches | |

| Relays | |

| Contactors | |

| Fuses | |

| Power Distribution and Management | Transformers |

| Switchgear | |

| Control and Connectivity | Wires and Cables |

| Connectors | |

| Sensors and Actuators | |

| Other Types | Power Supplies |

| Motor Drives | |

| Controllers |

| Low Voltage (Up to 1 kV) |

| Medium Voltage (1 to 40 kV) |

| High/Extra-High Voltage (Above 40 kV) |

| Indoor |

| Outdoor |

| Oil and Gas |

| Industrial Manufacturing |

| Infrastructure and Construction |

| Data Centers and ICT |

| Commercial and Hospitality |

| Other End-Users |

| By Type | Circuit Protection and Switching | Circuit Breakers |

| Switches | ||

| Relays | ||

| Contactors | ||

| Fuses | ||

| Power Distribution and Management | Transformers | |

| Switchgear | ||

| Control and Connectivity | Wires and Cables | |

| Connectors | ||

| Sensors and Actuators | ||

| Other Types | Power Supplies | |

| Motor Drives | ||

| Controllers | ||

| By Voltage Class | Low Voltage (Up to 1 kV) | |

| Medium Voltage (1 to 40 kV) | ||

| High/Extra-High Voltage (Above 40 kV) | ||

| By Installation Environment | Indoor | |

| Outdoor | ||

| By End-User | Oil and Gas | |

| Industrial Manufacturing | ||

| Infrastructure and Construction | ||

| Data Centers and ICT | ||

| Commercial and Hospitality | ||

| Other End-Users | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia industrial electrical components market?

The market stands at USD 3.32 billion in 2026 and is projected to reach USD 4.55 billion by 2031.

Which segment is growing fastest within Saudi electrical components?

Data centers and ICT are expanding at a 9.5% CAGR through 2031 as hyperscale build-outs and sovereign AI programs accelerate power-infrastructure upgrades.

How will Vision 2030 projects influence component demand?

Megaprojects such as NEOM and the Red Sea drive multi-year procurement cycles, adding 1.8 percentage points to market CAGR by 2028.

What challenges do suppliers face in meeting Saudi demand?

Volatile copper and steel prices and transformer lead times of up to 210 weeks tighten margins and extend project schedules.

Why are data centers important to future growth?

Hyperscale investments exceeding USD 21 billion require high-reliability power gear, pushing the segment at a 9.5% CAGR.

How is localization changing the competitive landscape?

IKTVA rules that call for 70% local value by 2030 are prompting global firms to partner with Saudi fabricators and open assembly lines.

Page last updated on: