Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

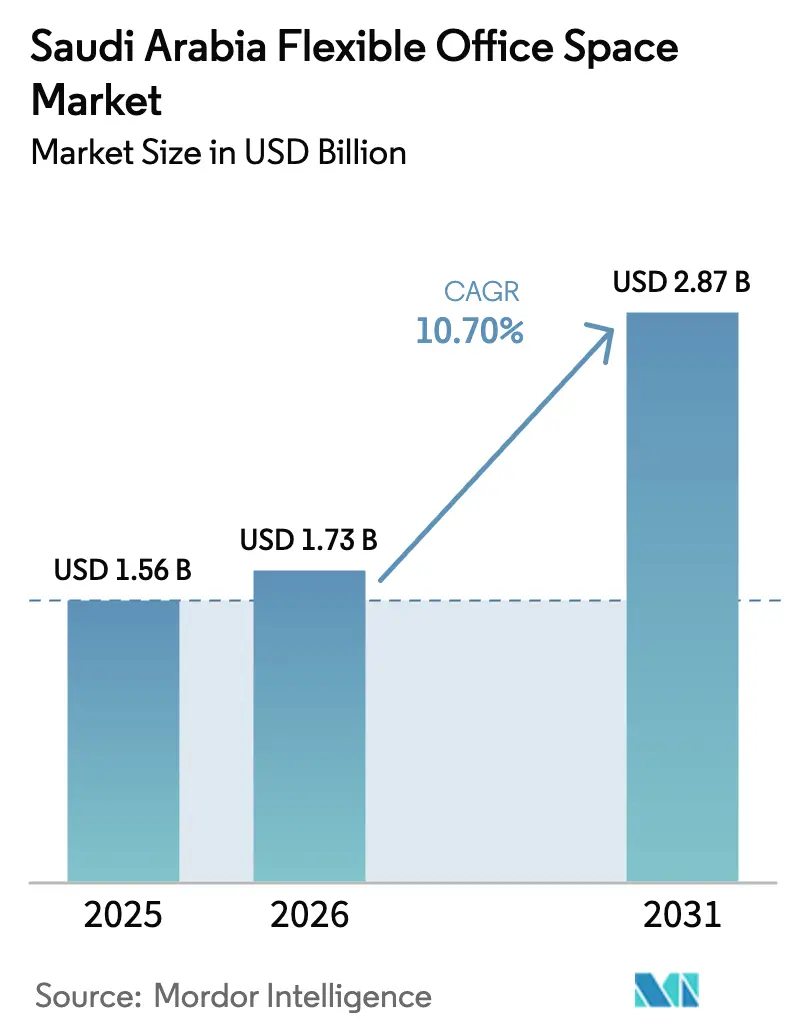

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 10.70% CAGR |

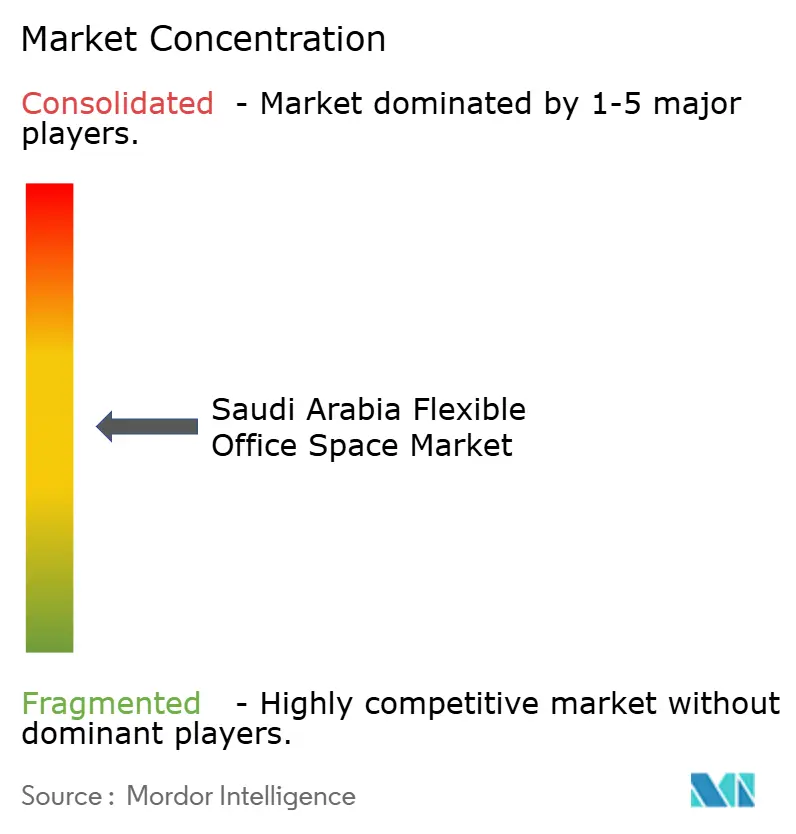

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Flexible Office Space Market Analysis by Mordor Intelligence

The Saudi Arabia flexible office market size was valued at USD 1.56 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 2.87 billion by 2031, at a CAGR of 10.70% during the forecast period (2026-2031). This surge links directly to Vision 2030, which is steering the economy away from hydrocarbons toward knowledge-based activity and fueling demand for agile workspace formats. Over 1.27 million SMEs were on the national register by year-end 2023, actively supported by 273 licensed incubators, accelerators, and co-working venues that anchor the entrepreneurial ecosystem. International firms relocating regional headquarters to Riyadh under new regulatory incentives, the USD 70 billion annual spending target of the Public Investment Fund, and a 15-point jump in female labor participation since 2018 are creating a structural pull for adaptive office solutions. At the same time, megaprojects such as NEOM, King Abdullah Financial District (KAFD), and multiple Special Economic Zones are embedding flexible office components into their master plans to satisfy globally mobile talent pools.

Key Report Takeaways

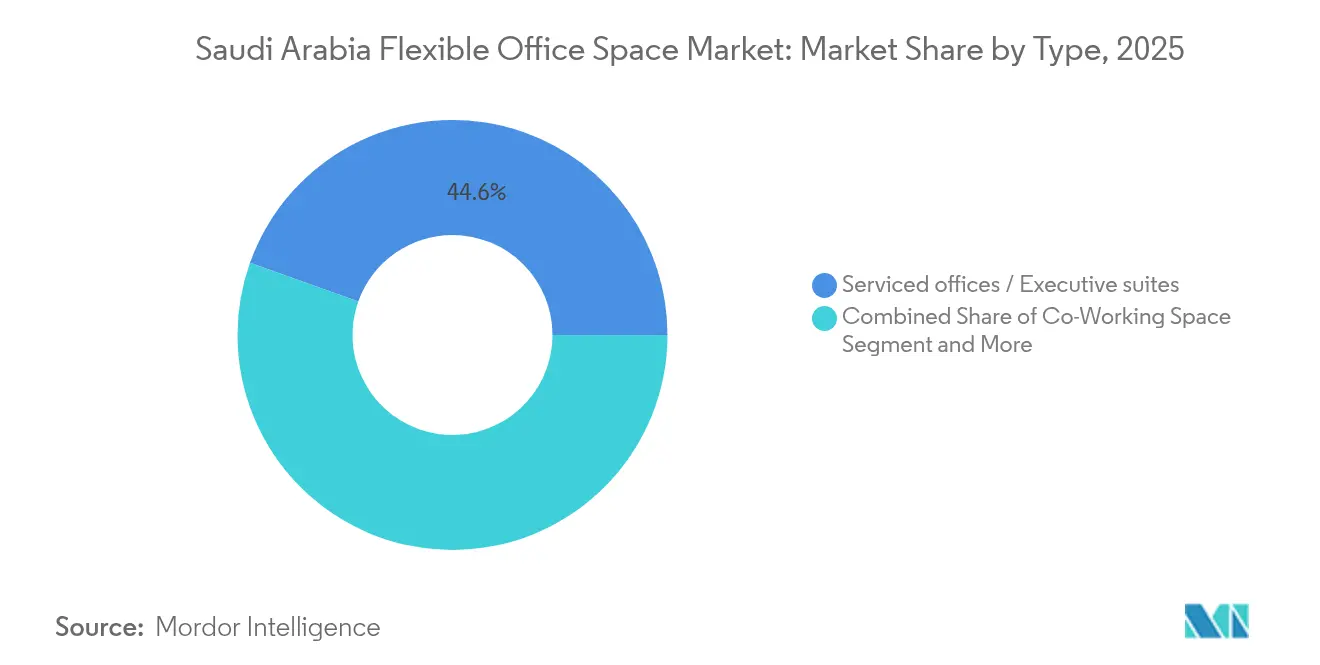

- By type, serviced offices commanded 44.55% of the flexible office market share in 2025, while co-working spaces are forecast to expand at an 11.54% CAGR through 2031.

- By sector, information technology & IT-enabled services held 40.45% share of the flexible office market size in 2025; the banking & financial services segment is projected to post the fastest 11.6% CAGR to 2031.

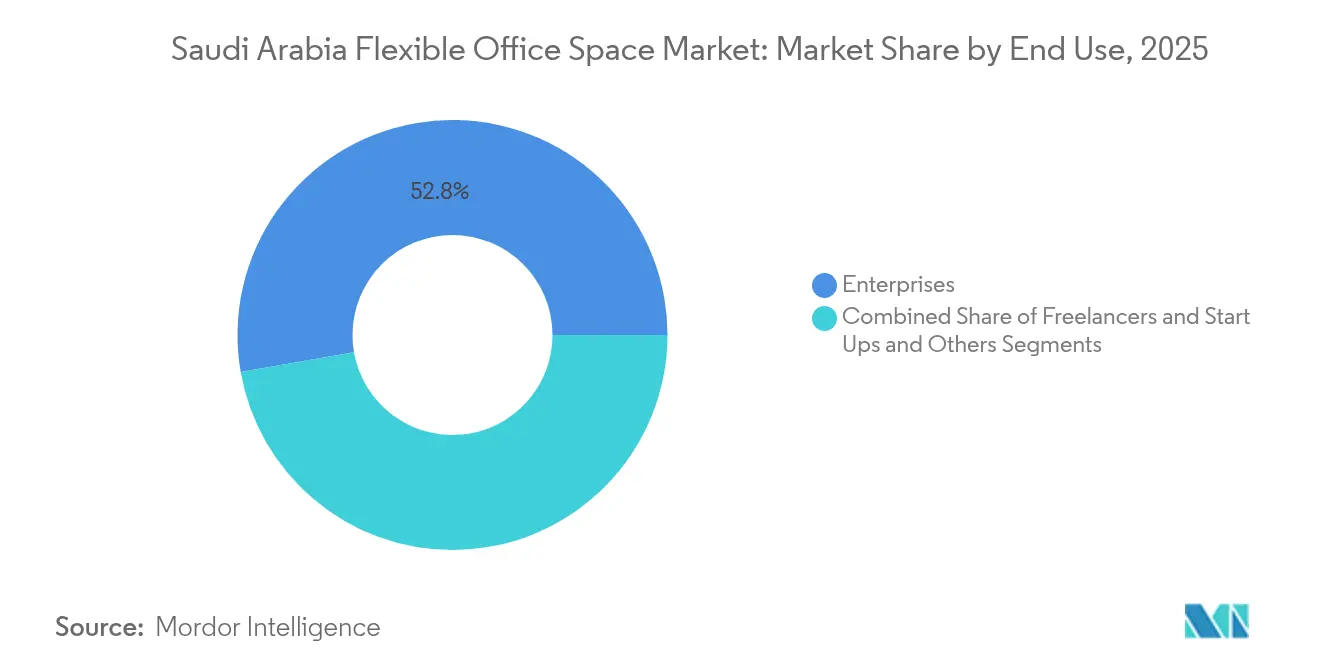

- By end use, enterprise tenants accounted for 52.75% of the flexible office market size in 2025, whereas startups are on track to advance at a 12.05% CAGR between 2026 and 2031.

- By key city, Riyadh led with an 81.60% flexible office market share in 2025, while Jeddah is poised for the strongest 12.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Flexible Office Space Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Entrepreneurship and SME growth under Vision 2030 fueling demand for co-working spaces | +3.2% | National (Riyadh, Jeddah, NEOM) | Long term (≥ 4 years) |

| Increased adoption of hybrid working models among corporates | +2.8% | Riyadh, Jeddah, expanding to DMA | Medium term (2-4 years) |

| Government-backed innovation hubs and free zones encouraging flexible workspace demand | +2.1% | NEOM, KAEC, KAFD, SEZs | Long term (≥ 4 years) |

| International operators entering Riyadh and Jeddah to meet rising premium demand | +1.7% | Riyadh & Jeddah metros | Short term (≤ 2 years) |

| Growing preference for cost-efficient, short-term leasing models among tenants | +1.2% | National business districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Entrepreneurship and SME growth under Vision 2030 fueling demand for co-working spaces

Saudi Arabia's entrepreneurial growth is transforming office space usage. In 2023, the number of SMEs exceeded 1.27 million, supported by initiatives such as Monsha'at, which operates 273 accelerators and incubators offering capacity-building programs, advisory services, and subsidized spaces. Startups increasingly prefer flexible pay-as-you-go models, enabling them to manage capital efficiently and adjust to workforce changes. Entrepreneurs in sectors like fintech, e-commerce, and creative media are opting for collaborative open spaces instead of traditional cellular office layouts. The Social Development Bank's "Jada30" program demonstrates government support by linking funding to accessible workspaces. As Vision 2030 aims to increase the private sector's GDP contribution from 40% to 65%, co-working spaces are becoming essential to support this economic growth[1]Economic Cities and Special Zones Authority, “SEZ Framework 2024,” eca.gov.sa.

Increased adoption of hybrid working models among corporates

The adoption of hybrid work models is transforming corporate strategies and reshaping office spaces. In a move echoing their pandemic-era trials, major enterprises are now solidifying remote and hub-and-spoke work policies. Banking, telecom, and energy giants are designating portions of their portfolios to distributed sites, enabling staff to work closer to home two to three days a week. A 2024 independent workplace survey highlights that employees dedicate about 28% of their office hours to individual tasks, benefiting from quiet zones. In contrast, collaborative efforts require flexible meeting suites equipped with advanced AV systems. This task-oriented strategy is prompting landlords to upgrade buildings with modular partitions, smart-booking apps, and acoustic pods. Cost optimization is another driving force: corporate occupiers are moving away from under-utilized traditional leases, yet maintaining prestigious addresses through flexible office agreements that adapt to real-time usage. As a result, operators offering networked footprints across multiple cities in Saudi Arabia are gaining a strategic edge.

Government-backed innovation hubs and free zones encouraging flexible workspace demand

Government-backed initiatives are playing a pivotal role in driving demand for flexible workspaces, fostering innovation and collaboration across various industries. In 2024, four new Special Economic Zones (SEZs) were launched, focusing on cloud computing, manufacturing, logistics, and maritime services. These zones offer enticing benefits like tax holidays, 100% foreign ownership, and streamlined permitting processes. Each SEZ is equipped with shared R&D labs and modular offices, allowing tenants to expand with ease. At NEOM’s Oxagon, a groundbreaking USD 5 billion deal with DataVolt is set to establish the world’s first net-zero AI factory, slated to commence operations by 2028. Such initiatives are attracting clusters of engineers, data scientists, and venture teams, all of whom seek nearby collaboration hubs. In the King Abdullah Financial District, 94 smart buildings, managed by IBM Maximo, oversee 100,000 assets. This management has not only achieved the prestigious LEED Platinum certification but also a remarkable 95% increase in service satisfaction. The fusion of green design ambitions with the adoption of Industry 4.0 is driving a surge in demand for technologically advanced flexible workspaces.

International operators entering Riyadh and Jeddah to meet rising premium demand

The demand for premium workspaces in Riyadh and Jeddah is driving international operators to expand their presence in Saudi Arabia. Global brands are rapidly entering the Kingdom, building on strong performances in other markets. In 2024, the International Workplace Group (IWG) achieved record revenue of USD 3.3 billion, utilizing a capital-light franchise model that aligns well with Saudi partners aiming to diversify their portfolios. Since 2021, the regional headquarters rule—offering foreign multinationals rent exemptions and expedited licensing—has attracted over 500 companies, including Adobe, Microsoft, and Amazon. These companies are not just seeking office spaces but also hotel-like amenities, strong ESG credentials, and seamless tech integration—standards already established by international operators globally. The growing venture capital inflows reflect confidence in the market's resilience. For instance, Flow, supported by USD 293 million in Saudi funding, highlights the local interest in prop-tech-driven workspace ventures. These developments are intensifying competition and raising service standards nationwide.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural resistance to shared working environments in certain segments | -1.8% | Traditional business districts in Riyadh, Jeddah, and conservative regions | Medium term (2-4 years) |

| Limited supply of high-quality flexible office operators outside major cities | -1.4% | DMA, Rest of Saudi Arabia, secondary cities | Short term (≤ 2 years) |

| Economic volatility impacting SME and start-up occupancy stability | -1.1% | National, with higher impact in emerging business districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cultural resistance to shared working environments in certain segments

Adapting to modern workspace trends requires addressing cultural and organizational challenges in Saudi Arabia. In Saudi Arabia, corporate hierarchy runs deep. Senior executives often opt for enclosed offices, a nod to their status and the privacy they cherish. Meanwhile, both government entities and family-owned conglomerates voice concerns over confidentiality when considering open-plan co-working spaces. Research highlights that for public-sector entities, shifting from traditional cellular layouts to collaborative hubs isn't just about design it's a delicate dance of change management. This involves staff workshops and pilot zones to demonstrate potential productivity boosts. However, societal dynamics are evolving. Female workforce participation surged from 20% in 2018 to over 35% in 2023, driving a demand for workspaces that prioritize inclusivity, featuring wellness rooms and gender-sensitive designs. Additionally, younger tech professionals, many of whom received training abroad, are embracing trends like hot-desking and communal amenities. This suggests that the cultural barriers in Saudi workspaces may soon diminish.

Limited supply of high-quality flexible office operators outside major cities

The availability of high-quality flexible office operators remains limited outside major cities in Saudi Arabia. Riyadh and Jeddah dominate the premium office landscape, yet the Dammam Metropolitan Area and other secondary cities fall short. These locales lack operators equipped with enterprise-grade IT infrastructure, concierge services, and ESG certifications. Government agencies, particularly those spearheading energy megaprojects, frequently lease entire floors, tightening the inventory for flexible providers. Despite a promising USD 1.5 trillion national construction pipeline set to unveil new mixed-use assets by 2030, many developers grapple with the nuances of managed office metrics. This learning curve spanning service-level agreements to dynamic pricing extends rollout timelines. Until either local or international brands invest in these smaller markets, occupiers will likely confront quality disparities, hindering wider adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serviced Offices Lead Premium Positioning

Serviced offices captured 44.55% of the flexible office market share in 2025, underscoring corporate preference for turnkey suites that combine privacy with hotel-style amenities. International relocatees drawn by the regional headquarters program gravitate toward these “ready-on-day-one” spaces to accelerate local integration. Operators typically bundle high-speed connectivity, meeting rooms, and multilingual reception services, thereby reducing onboarding friction for foreign executives. Yet momentum is tilting toward co-working formats, which post the segment-leading 11.54% CAGR to 2031 as startups and project teams favor collaborative communities. The hybrid sub-category, encompassing virtual offices and swing-space subscriptions, is emerging as a bridge product, letting firms split staff between core HQ floors and satellite nodes.

The co-working wave finds its strongest expression in fintech and creative media circles, where cross-pollination of ideas is a currency in itself. Membership models that allow “global roaming” among networks in Riyadh, Jeddah, and Dubai have become popular perks in expatriate remuneration packages. Meanwhile, serviced-office landlords are adding lounges and drop-in desks to retain relevance. Competitive intensity is especially high along Riyadh’s King Fahd Road, where more than a dozen branded hubs now vie for multinational tenants. As operators standardize biometric access, IoT-driven environmental controls, and ESG reporting dashboards, differentiation will hinge on community programming and partnerships with talent accelerators.

By Sector: Technology Drives Current Demand While Finance Accelerates

Information technology and IT-enabled services accounted for 40.45% of the flexible office market size in 2025, reflecting the nation’s rapid digital transformation agenda. Tech firms often require scalable environments with robust power redundancy, top-tier cybersecurity, and 24/7 access, features that are increasingly embedded in Grade-A co-working centers. Many of these companies also integrate lab-style project rooms outfitted with AR/VR testing rigs as part of their lease package. The banking and financial services sector, projected to record the fastest 11.6% CAGR to 2031, is gravitating to flexible offices as it pivots to venture-studio innovation and partnerships with fintech startups. In KAFD, global payment giant Visa debuted an innovation center in 2024 designed around modular collaboration zones that blur the lines between workspace and showroom.

Professional services, legal, strategic advisory, and accounting remain steady users because the mix of private suites and client-ready boardrooms aligns with confidentiality mandates. The “other services” bucket, covering life sciences, renewables, and culture & entertainment, is gaining ground as Vision 2030 diversifies GDP composition. Operators courting these niches invest in sector-specific infrastructure, such as wet labs for biotech or acoustically treated studios for digital media production. The sector landscape, therefore, mirrors wider economic diversification, making flexible office providers indirect beneficiaries of policy reform.

By End Use: Enterprises Dominate While Startups Drive Growth

Enterprises occupied 52.75% of the flexible office market size in 2025, attracted by professional ambience, rigorous compliance support, and service-level agreements that match global HQ standards. Large occupiers appreciate the ability to ring-fence contiguous suites within broader hubs, giving teams privacy while still granting access to shared amenity floors. The regional HQ regime further compels international companies to conduct board meetings physically in-country, boosting demand for premium conference facilities with advanced telepresence systems. Operators respond with “enterprise wings,” often branded under the tenant’s logo, marrying flexibility with corporate identity.

Startups, however, register the briskest 12.05% CAGR through 2031, spurred by the Kingdom’s rising venture-capital inflows that peaked at USD 1.33 billion in 2023. Accelerators embedded within flexible offices provide mentoring, investor pitch nights, and talent-matching services. Freelancers, though still a smaller slice, are growing as government promotion of the gig economy gains traction. Membership levels tailored for solo professionals day passes, weekend desks, or post-4 p.m. bundles are expanding to meet this audience. The varied end-user mix encourages operators to program diverse events ranging from coding hackathons to corporate wellness workshops, fostering cross-sector synergies.

Geography Analysis

Riyadh's dominant position arises from its blend of political clout, robust capital markets, and swift infrastructure development. The city's regional HQ mandate has lured numerous Fortune 500 companies, bolstered by incentives like multi-year rent holidays and expedited licensing. The recently inaugurated Boulevard Business Park, featuring an art walk and rooftop wellness amenities, underscores a shift towards experiential workplaces aimed at enhancing staff retention. KAFD's 94 interconnected towers highlight the benefits of smart-building technologies, reducing maintenance costs and boosting tenant satisfaction. Collectively, these factors cement Riyadh's status as the hub for premium flexible office demand.

Jeddah, historically a commercial and port city, is leveraging its legacy for a modern resurgence. Developments along the Corniche not only elevate the city's lifestyle but also align with Red Sea tourism goals, aiming for 100 million visitors annually by 2030. Al-Khabeer Capital's Elite Commercial Center, situated near King Abdulaziz International Airport, underscores the correlation between enhanced connectivity and rising office values. Compared to its counterparts, Jeddah's cultural openness fosters quicker acceptance of shared workspaces, especially among design, advertising, and media sectors. Capitalizing on the city's laid-back business culture, flexible office operators are integrating hospitality elements, from seaside cafés to sunset networking decks.

The Dammam Metropolitan Area, serving as the gateway to the Eastern Province's energy sector, faces a structural undersupply in office spaces, particularly in the premium flexible segment. While industrial tenants, especially those in oilfield services, emphasize compliance and security with specialized facilities, escalating rents hint at potential for operators eyeing upscale conversions or new developments. Beyond the "big three" cities, Saudi Arabia's Vision 2030 is steering focus towards secondary cities, bolstered by rail connections, digital infrastructure, and educational centers. NEOM stands out as a pioneering vision, aiming for a circular economy where innovations like autonomous pods and solar canopies reshape commuting and workspaces. As these regions evolve, flexible office providers adept in off-grid power and modular systems are poised to seize the first-mover advantage.

Competitive Landscape

The Saudi flexible office market sits at a midpoint between fragmentation and consolidation. International Workplace Group leverages global scale to secure enterprise contracts and seed capital-light franchises, adding depth to both downtown Riyadh and Jeddah waterfront districts. Local brand Medad Offices courts government agencies through Arabic-first service desks and Sharia-compliant contract structures, while Vibes positions community-centric hubs near universities to capture Gen-Z entrepreneurs. Real-estate developers behind mixed-use mega-projects are carving out in-house operating units, blurring landlord-operator lines and pressuring independent providers to sharpen their value proposition.

Technology integration is now a primary battleground. Operators deploy AI-driven occupancy analytics and app-based seat reservations to offer usage-based pricing that aligns with corporate ESG reporting. IBM’s Maximo blueprint at KAFD sets a benchmark many newer hubs emulate, including digital twins for predictive maintenance. Sustainability credentials carry equal weight; LEED Gold or better serves as a baseline for premium-tier tenants. Providers that can quantify energy savings and wellness metrics in real time secure longer renewal cycles and command price premiums.

Sector specialization is emerging as the next differentiator. AstroLabs collaborates with venture capital funds to host founder academies and demo days, ensuring a pipeline of tech clients. Hospitality-anchored groups such as Kerten Hospitality combine boutique hotels with co-working floors, capturing remote professionals seeking seamless live-work packages. Meanwhile, landlord consortiums in Dammam and Tabuk explore co-lab models targeting renewable-energy engineers. The market’s evolving shape suggests a gradual power shift toward hybrid platforms that weave workspace, community, and lifestyle into one subscription[3]Visa, “KAFD Innovation Center Press Release,” kafd.sa.

Saudi Arabia Flexible Office Space Industry Leaders

IWG (Regus, Spaces)

Servcorp

CBRE (Hana)

AstroLabs

Tools & Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: NEOM and DataVolt signed a USD 5 billion investment agreement to develop the region's first net-zero AI factory, expected to be operational by 2028, creating demand for specialized flexible workspace solutions supporting AI and technology companies.

- November 2024: Adam Neumann's Flow venture secured USD 293 million in Saudi real estate investment, focusing on housing development that appeals to both foreign workers and young Saudis, reflecting changing social norms toward apartment living.

- October 2024: CEVA Logistics signed a joint venture agreement with Almajdouie Logistics to enhance integrated logistics solutions across energy, automotive, and e-commerce sectors, creating a workforce of around 2,000 employees requiring flexible workspace solutions.

- October 2024: Visa opened a new innovation center and office in King Abdullah Financial District to enhance digital payments growth, demonstrating continued attraction of KAFD as a premium business destination.

Saudi Arabia Flexible Office Space Market Report Scope

Flexible workspace is also known as shared office space or flex space. This type of office space is fitted with basic equipment, like phone lines, desks, and chairs, a setup that allows employees who normally work from home or telecommute to have a physical office for a few hours every week or every month. Furthermore, this report offers a complete analysis of the Flexible Office Market in Saudi Arabia, including a market overview, market size estimation for key segments, emerging trends by segments, and market dynamics.

Saudi Arabia's flexible office space market is segmented by type (private offices, co-working space, and virtual offices), by end user (IT and Telecommunications, media and entertainment, retail and consumer goods, and other end users), and by city (Riyadh, Dammam, Jeddah, and Rest of Saudi Arabia). The report offers the market size in value terms in (USD) for all the above mentioned segments.

By Type

| Co-Working Space |

| Serviced offices / Executive suites |

| Others (Hybrid, Virtual Office) |

By Sector

| Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Service |

| Other Services (Retail, Lifesciences, Energy, Legal Services) |

By End Use

| Freelancers |

| Enterprises |

| Start Ups and Others |

By Key City

| Riyadh |

| Jeddah |

| DMA (Dammam metropolitan area) |

| Rest of Saudi Arabia |

| By Type | Co-Working Space |

| Serviced offices / Executive suites | |

| Others (Hybrid, Virtual Office) | |

| By Sector | Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Service | |

| Other Services (Retail, Lifesciences, Energy, Legal Services) | |

| By End Use | Freelancers |

| Enterprises | |

| Start Ups and Others | |

| By Key City | Riyadh |

| Jeddah | |

| DMA (Dammam metropolitan area) | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

How big is the flexible office market in Saudi Arabia in 2026?

The flexible office market size stands at USD 1.73 billion in 2026 and is tracking toward USD 2.87 billion by 2031 at a 10.70% CAGR.

Which city leads demand for flexible offices?

Riyadh holds 81.60% share thanks to ministry clusters, sovereign funds, and mega mixed-use developments.

What segment is expanding the quickest?

Co-working spaces post the highest 11.54% CAGR as startups and project teams seek collaborative environments.

Why are global operators entering Saudi Arabia?

A regional HQ mandate, tax incentives, and a robust SME pipeline make the market attractive for premium flexible workspace providers.

What challenges could restrain growth?

Cultural preference for private offices and limited premium supply outside Riyadh and Jeddah pose short-term hurdles.

How is Vision 2030 influencing workspace trends?

The drive toward economic diversification and digital transformation is accelerating demand for technology-rich, scalable workspace solutions.

Page last updated on: