Saudi Arabia Entertainment And Amusement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

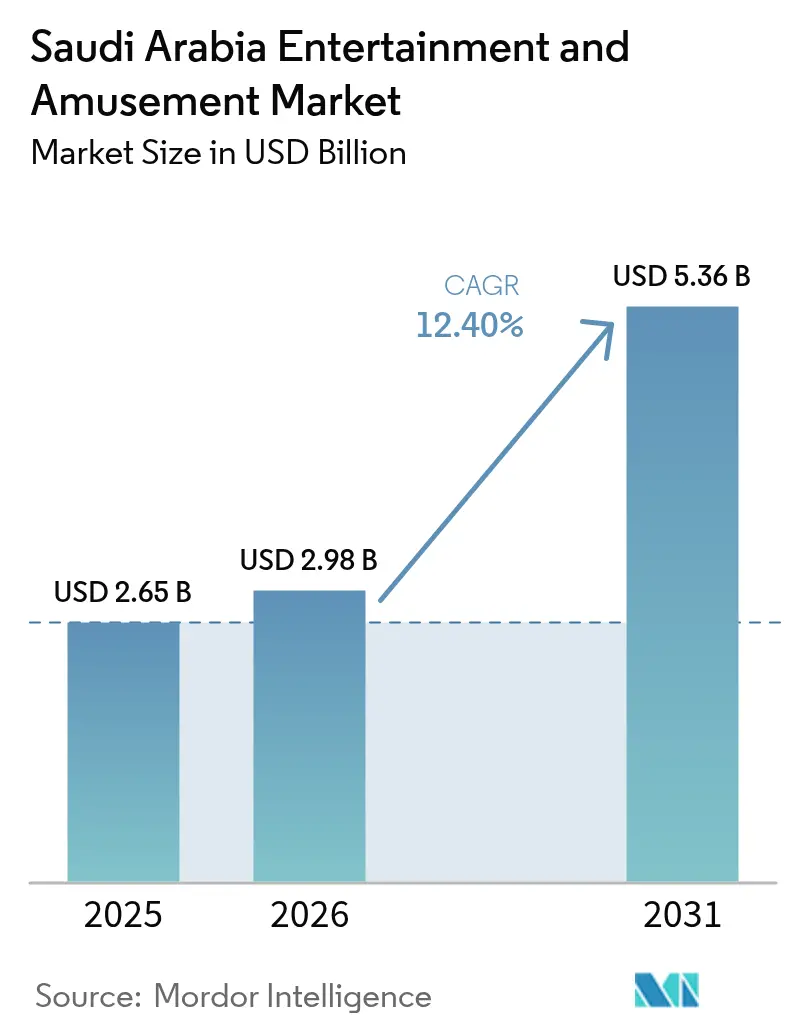

| Base Year Market Size (2025) | USD 2.65 Billion |

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 12.40% CAGR |

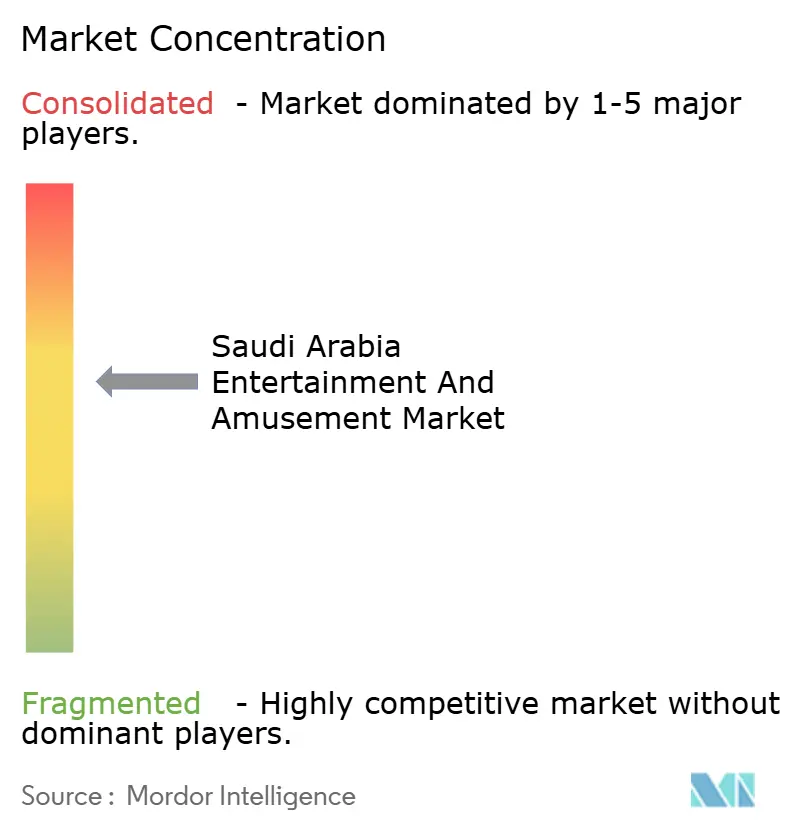

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Entertainment And Amusement Market Analysis by Mordor Intelligence

Saudi Arabia Entertainment And Amusement market size in 2026 is estimated at USD 2.98 billion, growing from 2025 value of USD 2.65 billion with 2031 projections showing USD 5.36 billion, growing at 12.4% CAGR over 2026-2031.

The acceleration reflects higher public-sector capital expenditures, a visible pivot toward leisure components inside mixed-use real-estate projects, and a steady normalization of family-oriented out-of-home leisure spending. Intensified PIF-backed funding into giga-projects, rapid rollout of mall-anchored family entertainment centers, and relaxed social norms that broaden mixed-gender visitation continue to push ticket volumes and per-capita spend upward. Domestic tourism campaigns under the “Saudi Summer” banner have lengthened the average stay of local travelers and have redirected weekend footfall toward purpose-built leisure hubs. Meanwhile, international pilgrims increasingly combine cultural excursions with heritage attractions, further lifting seasonal revenues during shoulder months. Competitive pricing by new-generation operators and bundled dining-plus-activity passes are also reshaping revenue mixes toward higher-margin premium experiences.

Key Report Takeaways

- By venue type, family entertainment centers led with 36.02% of the Saudi Arabia entertainment and amusement market share in 2025; mixed reality & VR arcades are projected to expand at a 18.5% CAGR through 2031.

- By revenue stream, ticket sales accounted for 50.10% of the Saudi Arabia entertainment and amusement market share in 2025; premium experiences are forecast to advance at a 20.1% CAGR to 2031.

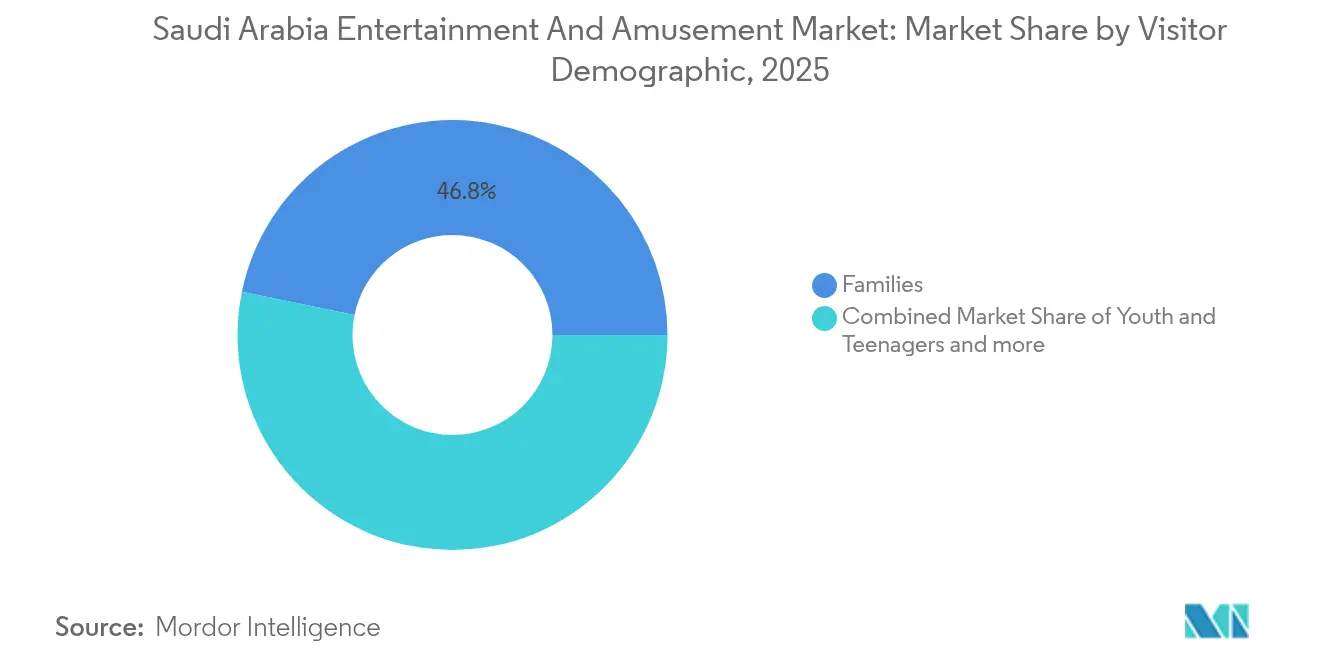

- By visitor demographic, families captured 46.78% of the Saudi Arabia entertainment and amusement market share in 2025, while youth & teenagers are on track for a 13.3% CAGR during the outlook period.

- By region, Riyadh captured 52.10% of the Saudi Arabia entertainment and amusement market share in 2025, while Eastern Province is on track for a 6.8% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Entertainment And Amusement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensified Vision 2030 CAPEX | +1.4% | Kingdom-wide, highest in Riyadh & Tabuk | Long term (≥ 4 years) |

| Growing domestic tourism ("Saudi Summer") | +1.1% | All provinces, strongest in coastal Asir | Medium term (2-4 years) |

| Mall-anchored FEC roll-outs | +0.9% | Top-tier retail corridors in Riyadh, Jeddah, and Dammam | Short term (≤ 2 years) |

| Relaxed social norms (female & family visitation) | +0.8% | Kingdom-wide | Short term (≤ 2 years) |

| Gaming and esports infrastructure development | +0.7% | Kingdom-wide, concentrated in Riyadh, NEOM, and Eastern Province | Medium term (2-4 years) |

| Gamified pilgrimage packages | +0.4% | Makkah & Madinah corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensified Vision 2030 CAPEX

Government entities channeled more than SAR 50 billion (USD 13.33 billion) into leisure infrastructure between 2024 and 2025, anchoring 21 Saudi Entertainment Ventures (SEVEN) destinations, the Qiddiya mega-theme-park cluster, and mixed-reality zones inside NEOM. The steady funding pipeline reduces developer risk perceptions, shortens payback periods, and attracts global IP partners to license ride technologies. Higher-quality supply, in turn, elevates domestic staycation retention and curbs outbound leisure leakage. The clear policy alignment with Vision 2030 tourism metrics has also accelerated municipal permit approvals in priority corridors. As phased openings ramp up, ticketing systems integrate dynamic pricing, ultimately widening both weekday utilization and off-peak yield[1]Source: Ministry of Investment Saudi Arabia, “Tourism, Culture & Entertainment,” investsaudi.sa..

Growing Domestic Tourism Under “Saudi Summer” Campaigns

The Ministry of Tourism reported a 17% year-on-year rise in intra-kingdom leisure trips in the 2025 summer window, propelled by bundled packages that pair hotel vouchers with attraction passes. Partnerships with regional airlines and ride-hailing platforms have trimmed average transport costs, making weekend getaways feasible for middle-income households. Event calendars now include co-branded concerts and culinary festivals that prolong visitor dwell times. During campaign periods, retail landlords witness an 11% increase in foot traffic, underscoring the harmonious relationship between entertainment anchors and discretionary shopping. Incremental demand stabilizes cash flows for operators that historically relied on peak religious seasons[2]Source: Ministry of Transport Saudi Arabia, “Sector Indicators,” mt.gov.sa..

Mall-Anchored FEC Roll-outs by Local Conglomerates

Retail REITs and hypermarket chains increasingly position family entertainment centers as core traffic drivers inside new-build malls. Medium-format indoor rides, redemption arcades, and kid-centric edutainment zones require lower land envelopes than full-scale theme parks, enabling faster payback. Operators such as Abdul Mohsen Al Hokair Group and Al Othaim Leisure & Tourism report double-digit revenue lifts when FECs launch adjacent to food courts. The clustering of leisure, cinema, and specialty dining promotes longer dwell times and cross-shop conversions. Importantly, the modular design allows periodic re-theming, meeting the Saudi adolescent audience’s appetite for novelty.

Relaxed Social Norms Spurring Female & Family Visitation

Regulatory reforms that have eased guardianship requirements and broadened permissible public activities for women have markedly shifted attendance patterns. Mixed-gender queuing and family-dedicated lanes now dominate weekend throughput at indoor amusement parks. Operators report a 22% rise in mother-initiated online bookings, supported by loyalty apps that reward repeat play sessions. The growth of female labor participation enlarges disposable incomes, thereby lifting per-capita spending on bundled food-and-play packages. Marketing narratives highlighting inclusive, culturally sensitive environments resonate strongly across social media channels, further normalizing leisure outings[3]Source: United Nations World Tourism Organization, “Saudi Heritage Tourism Update,” unwto.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High seasonality (Hajj & Umrah peaks) | −0.7% | Makkah, Madinah | Short term (≤ 2 years) |

| Fragmented municipal licensing | −0.6% | Secondary cities | Medium term (2-4 years) |

| Talent shortage in themed-entertainment engineering | −0.5% | Kingdom-wide | Long term (≥ 4 years) |

| Peripheral giga-project power deficits | −0.4% | NEOM, AMAALA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Seasonality During Hajj & Umrah Peaks

Visitor traffic surges sharply during pilgrimage seasons but drops in the intensely hot midsummer weeks. While cultural attractions near mosque precincts run at near-full capacity in Dhul-Hijjah, coastal water parks in Jeddah report utilization dips below 35% occupancy in the same window. Operators have begun to stagger new-ride debuts to coincide with lull periods and to introduce discounted shoulder-season combo passes. Even so, fixed operating costs for climate-controlled venues weigh on profit margins outside peak quarters. The seasonality issue reinforces the importance of dynamic staffing and energy-management systems.

Fragmented Licensing Across Municipalities

Entertainment developers often navigate overlapping city and provincial permitting frameworks that extend ground-breaking timelines by three to six months. Inconsistent safety-code interpretations across jurisdictions add design-revision costs and delay imported ride installations. Smaller domestic investors face higher compliance spending relative to cash flow, nudging them toward franchising instead of building original concepts. Recent moves to create a unified digital approval portal are still in pilot stages, leaving interim uncertainty for planned secondary-city FECs[4]Source: Vision 2030, “Municipal Licensing Reform Pilot,” vision2030.gov.sa..

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Venue Type: Family-oriented concepts drive volume while mixed-reality formats accelerate value

Family entertainment centers account for 36.02% of the Saudi Arabia entertainment and amusement market size in 2025, cementing their role as the default anchor inside new-generation malls. The packaged mix of mid-intensity rides, redemption arcades, and birthday-party rooms attracts multi-age groups and delivers predictable weekday school-trip demand. Ticket bundles commonly start at SAR 89 (USD 23.7) for two-hour passes, and operators upsell branded food combos that lift basket value. Competitive space is tightening as SEVEN alone lines up 21 branded destinations across tier-one and tier-two cities, often with long-term operating guarantees that ease landlord fears over vacancy risk.

Mixed reality and VR arcades, while currently below 5% share, showcase the fastest trajectory with a projected 18.5% CAGR through 2031. High-definition headsets, motion platforms, and esports clusters resonate with a digitally native youth cohort whose average disposable gaming budget has risen 14% year on year. Content localization—such as Arabic language storylines and regionally themed zombie shooters—enables deeper engagement. Premium private-pod rentals priced at SAR 150 (USD 40) per hour further elevate yield without expanding the physical footprint. The format’s modularity suits pop-up activations inside seasonal “Boulevard” events in Riyadh, ensuring national exposure before fixed-site rollouts.

By Revenue Stream: Ticket sales remain dominant, but premium add-ons reshape profitability

Ticket sales contributed 50.10% of Saudi Arabia entertainment and amusement market revenue in 2025, reflecting bundled admission models across most indoor venues. Dynamic pricing tools that adjust rates based on occupancy have improved weekday breakeven thresholds. Kiosks and mobile apps enable visitors to split payments across multiple cards, eliminating queue bottlenecks and increasing average transaction count per visit. In water parks, RFID wristbands streamline locker rentals and micro-transactions for food stalls, further enlarging the ticket-linked revenue bucket.

Premium experiences such as VIP queue-skipping passes, private cabanas, behind-the-scenes tours, and character dining will post a 20.1% CAGR between 2026 and 2031. Operators leverage scarcity to price VIP night parades at SAR 400 (USD 107) per head, with limited-edition merchandise bundles pushing total per-capita spend above SAR 600 (USD 160). The upsell is particularly effective in cultural attractions where heritage-focused augmented-reality overlays enrich storytelling for affluent domestic tourists. The margin differential between premium passes and base admissions exceeds 25 percentage points, driving net operating income without proportionate capital reinvestment.

By Visitor Demographic: Families dominate footfall; youth segments underpin growth

Families captured 46.78% of Saudi Arabia's entertainment and amusement market share in 2025, thanks to a mix of stroller-friendly layouts, prayer-room availability, and bundled dining upgrades aligned with multigenerational preferences. Multi-ticket packs that combine soft-play areas with gentle rides reduce per-guest costs and widen inclusion. Operators partner with educational agencies to integrate STEM-themed edutainment zones, reinforcing repeat visitation among school groups.

Youth and teenagers, projected to grow at a 13.3% CAGR, gravitate toward gamified experiences, esports tournaments, and social-shareable ride moments. Snackable content drop-ins—such as seasonal anime character crossovers—sustain interest and extend the marketing reach through user-generated content on TikTok and Snapchat. Loyalty schemes award in-app points redeemable for virtual items, knitting together physical attendance and online engagement.

Geography Analysis

The Saudi Arabia entertainment and amusement market demonstrates clear regional stratification in both supply density and spend profiles. Riyadh, with its cluster of newly opened Boulevard zones and high-end retail complexes, maintains the highest share at 52.10% of the Saudi Arabia entertainment and amusement market share in 2025 and records weekday average occupancy of 68% at FECs. Makkah Province aligns its attraction mix with pilgrimage cycles, drawing international visitor additions through themed heritage shows that resonate with faith-driven tourists. Eastern Province capitalizes on its coastal climate, anchoring water parks that engage youth segments seeking respite from inland heat, with a 6.8% CAGR of the Saudi Arabia entertainment and amusement market share during the outlook period.

Beyond the top three hubs, Asir and Qassim provinces experiment with indoor trampolines and boutique cultural centers that respect conservative social norms while catering to family day-trip demand. Tabuk’s NEOM corridor shifts the geographic narrative westward, promising a testbed for net-zero ride technologies and immersive holographic theater concepts. Supply pipelines in secondary cities increasingly track mall construction timelines; as new retail space comes online, developers lock in long-term leases with brand-managed leisure anchors, thereby minimizing dilution of ticket revenue per square meter.

Labor mobility within the kingdom supports staffing ramp-ups across regions, but talent concentration in Riyadh and Jeddah continues to widen unit-level productivity differentials. Energy-subsidy reforms prompt coastal operators to install solar parking canopies, shaving daytime peak power costs by up to 19%. Cross-province annual passes, valid across multiple brands, encourage repeat visitation and dilute region-specific seasonality effects. Strategic road-and-rail investments, such as the Riyadh–Jeddah high-speed rail link, promise to compress travel times and broaden the catchment areas of flagship parks.

Competitive Landscape

The competitive landscape leans toward a government-backed oligopoly, with leading players like Saudi Entertainment Ventures, Qiddiya Investment Company, Abdul Mohsen Al Hokair Group, Al Othaim Leisure & Tourism, and Sela dominating market revenues in 2024. SEVEN deploys a portfolio approach that targets white-space cities, signing multi-IP licensing deals with global brands to diversify ride refresh cycles. Qiddiya positions itself as a giga-park cluster, leveraging its Phase-1 Six Flags anchor to attract hospitality co-investors. Hokair exploits its legacy network of Sparky’s branded FECs across 90 locations, banking on operational know-how to negotiate favorable rent restructurings.

Private operators such as Fakieh Leisure & Entertainment concentrate on coastal Jeddah, bundling aquarium exhibits with outdoor ride zones to balance weather risk. Majid Al Futtaim Entertainment imports proven concepts like indoor ski slopes, adapting temperature-control systems for Riyadh’s climate profile. Global chains, including Merlin Entertainments, engage through JV structures that leave local real-estate risk with Saudi partners while contributing brand IP and operational standards.

Strategic moves in 2025 revolve around vertical integration and data analytics. SEVEN’s rollout of unified CRM platforms captures cross-park behavior, enabling variable pay-per-ride monetization models. Qiddiya fast-tracked an advanced ride-testing facility to localize maintenance expertise, reducing dependence on foreign engineers. Muvi Cinemas ventured into the esports arena development, cross-advertising events through its existing movie-goer base. Sela expanded seasonal festival musically themed zones, negotiating multi-year artist residencies that enhance merchandising margins. The market’s medium concentration score of 6 reflects a clustered top tier yet leaves room for specialized niche entrants in VR and live-performance segments.

Saudi Arabia Entertainment And Amusement Industry Leaders

Qiddiya Investment Company

Abdul Mohsen Al Hokair Group

Al Othaim Leisure & Tourism

Sela

Saudi Entertainment Ventures (SEVEN)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Esports World Cup 2025 entered the fourth week in August 2025 in Riyadh with over USD 60 million in total prize pools across multiple gaming titles, including chess (USD 1.5 million) and Mobile Legends like Bang Bang (USD 3 million), positioning Saudi Arabia as the global esports capital and demonstrating the Kingdom's commitment to gaming sector development.

- May 2025: Saudi Arabia launches a comprehensive summer program featuring over 550 tourism products and 150 family-focused offers across seven destinations, including the return of Jeddah Season and new Aseer Season, targeting record-breaking tourist numbers and domestic tourism growth.

- September 2024: Qiddiya Investment Company reiterated that Six Flags Qiddiya City, planned as the world’s largest Six Flags Park with 28 rides, remained on track for a late-2025 public opening; the SAR 30 billion (USD 8.00 billion) giga-project targets 17 million visitors annually by 2030

- July 2024: IMAX forged its first partnership with Saudi exhibitor Muvi Cinemas; four new IMAX auditoriums in Riyadh, Jeddah, Hofuf, and Dhahran were committed for delivery by year-end 2024, on top of 10 existing locations.

Saudi Arabia Entertainment And Amusement Market Report Scope

The entertainment and amusement market encompasses various industries that provide recreational activities and experiences, including theme parks, cinemas, live performances, gaming, and more.

Saudi Arabia's entertainment and amusement market is segmented by type of entertainment Destination (cinemas and theatres, amusement and theme parks, gardens and zoos, malls, gaming centers, and other entertainment destinations), the source of revenue (tickets, food & beverages, merchandise, advertising, and other sources of revenues), and by city (Riyadh, Jeddah, Makkah, Dammam, and Rest of Saudi Arabia).

The report offers market size and forecast values for the Saudi Arabia Entertainment and Amusement Market in USD million for the above segments.

| Theme Parks |

| Amusement Parks |

| Family Entertainment Centers (FECs) |

| Water Parks |

| Cultural / Heritage Attractions |

| Live Performance Venues |

| Mixed Reality & VR Arcades |

| Ticket Sales |

| Food & Beverage |

| Merchandise & Retail |

| Sponsorship & Advertising |

| Premium Experiences |

| Ancillary Services (parking, rentals) |

| Families |

| Youth & Teenagers |

| Tourists (International) |

| Corporate & Events |

| Children (<12 yrs) |

| Riyadh Province |

| Makkah Province |

| Eastern Province |

| Madinah Province |

| Asir Province |

| Qassim Province |

| Tabuk Province |

| Rest of Saudi Arabia |

| By Venue Type | Theme Parks |

| Amusement Parks | |

| Family Entertainment Centers (FECs) | |

| Water Parks | |

| Cultural / Heritage Attractions | |

| Live Performance Venues | |

| Mixed Reality & VR Arcades | |

| By Revenue Stream | Ticket Sales |

| Food & Beverage | |

| Merchandise & Retail | |

| Sponsorship & Advertising | |

| Premium Experiences | |

| Ancillary Services (parking, rentals) | |

| By Visitor Demographic | Families |

| Youth & Teenagers | |

| Tourists (International) | |

| Corporate & Events | |

| Children (<12 yrs) | |

| By Geography | Riyadh Province |

| Makkah Province | |

| Eastern Province | |

| Madinah Province | |

| Asir Province | |

| Qassim Province | |

| Tabuk Province | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

How large is the Saudi Arabia entertainment and amusement market in 2026?

The sector is valued at USD 2.98 billion in 2026, with a 12.4% CAGR outlook to 2031.

Which venue format is currently dominant?

Family entertainment centers lead, holding 36.02% of 2025 spending.

What is the fastest-growing revenue stream?

Premium experiences are projected to rise at a 20.1% CAGR between 2026 and 2031.

Which province offers the highest growth runway?

The NEOM Zone in Tabuk is set for a 15.5% CAGR through 2031.

How concentrated is the competitive landscape?

The combined share of the top five operators indicates moderate concentration.

Which demographic segment drives future ticket growth?

Youth and teenagers will post the quickest gains, advancing at a 13.3% CAGR.

Page last updated on: