Saudi Arabia E-commerce Eyewear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

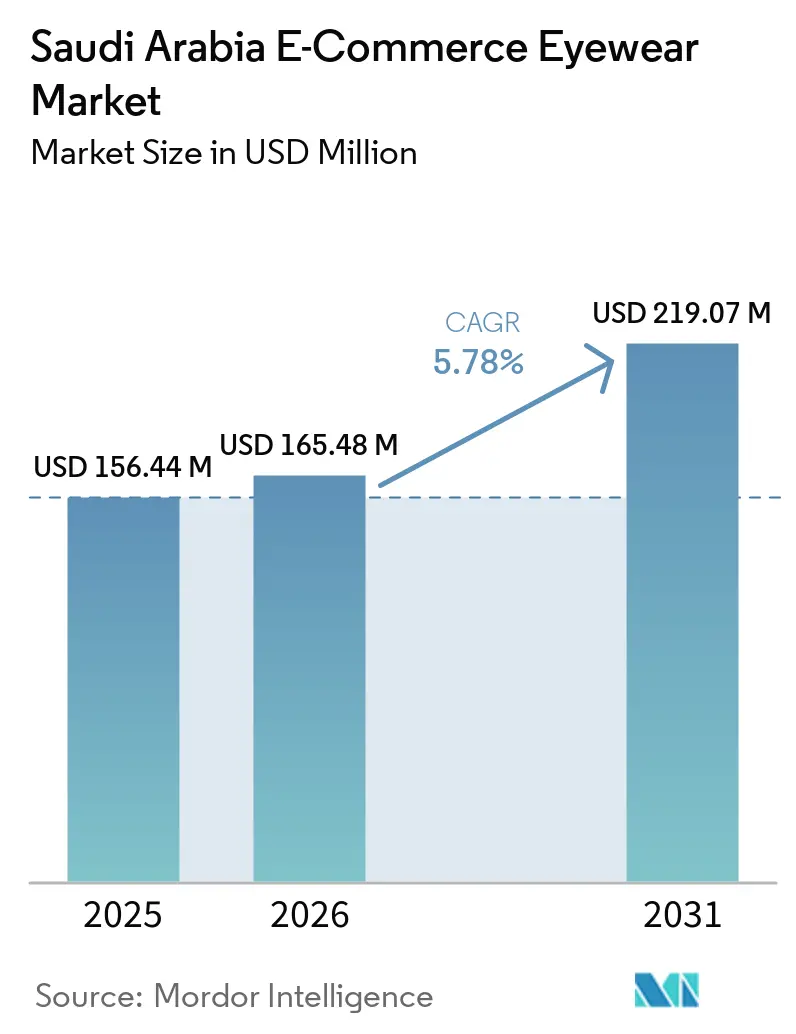

| Base Year Market Size (2025) | USD 156.44 Million |

| Market Size (2026) | USD 165.48 Million |

| Market Size (2031) | USD 219.07 Million |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia E-commerce Eyewear Market Analysis by Mordor Intelligence

The Saudi Arabia E-commerce Eyewear Market size was valued at USD 156.44 million in 2025 and estimated to grow from USD 165.48 million in 2026 to reach USD 219.07 million by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). The expansion of robust internet infrastructure, the deployment of 5G technology, and the increasing adoption of digital payment systems have established e-commerce platforms as critical channels for eyewear sales. Additionally, Saudi Arabia's Vision 2030 initiative continues to drive both local and international investments in the market. Spectacles remain the dominant product category, as they effectively combine medical functionality with fashion-forward appeal. However, contact lenses are experiencing the fastest growth in volume, fueled by the convenience they offer to working professionals. Urban consumers are increasingly favoring third-party marketplaces due to their extensive product variety, flexible payment options, and frequent promotional offers. At the same time, company-owned websites are gaining traction by offering advanced features such as virtual try-on tools and seamless prescription renewal services. While challenges such as counterfeit products and inefficiencies in last-mile delivery persist, the implementation of stricter intellectual property regulations and continuous improvements in logistics infrastructure are expected to mitigate these issues over the long term.

Key Report Takeaways

- By product type, spectacles captured 59.62% of the Saudi Arabia E-commerce Eyewear Market share in 2025, while contact lenses are forecast to expand at a 6.12% CAGR through 2031.

- By category, the mass segment held 68.32% revenue share of the Saudi Arabia E-commerce Eyewear Market in 2025; the premium segment is projected to advance at a 6.49% CAGR to 2031.

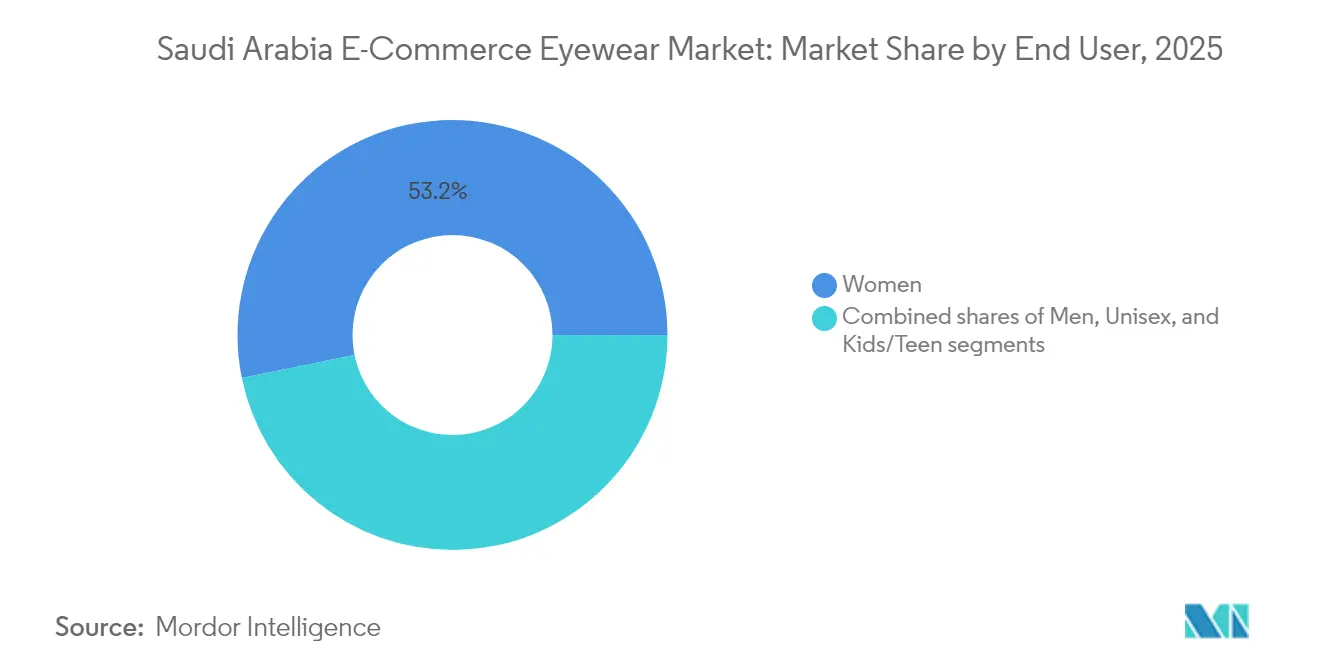

- By end user, women accounted for 53.21% of the Saudi Arabia E-commerce Eyewear Market in 2025 and the unisex segment records the highest projected CAGR at 6.92% through 2031.

- By platform type, third-party marketplaces dominated with 83.97% of the Saudi Arabia E-commerce Eyewear Market size in 2025 and are growing at a 7.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia E-commerce Eyewear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible and diverse payment options supports the market | +1.2% | National‐urban focus | Short term (≤ 2 years) |

| Promotion and discounts enticing consumer to make purchase | +0.8% | National‐mass segments | Short term (≤ 2 years) |

| Technological advancements drives the market | +1.5% | Early adopters in Riyadh and Jeddah | Medium term (2-4 years) |

| Influence of social media platforms and celebrity endorsements | +0.9% | Younger demographics | Medium term (2-4 years) |

| Rising internet penetration boosts e-commerce sales | +1.1% | Rural acceleration | Long term (≥ 4 years) |

| Growing awareness of eye health drives demand | +1.3% | Backed by national health programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Flexible and diverse payment options supports the market

Saudi Arabia's payment ecosystem is undergoing significant transformation, creating a conducive environment for the expansion of the e-commerce eyewear market by minimizing transaction barriers and fostering greater consumer confidence. A notable development in this regard is the Saudi Central Bank's collaboration with Google to introduce Google Pay by 2025. This initiative, which integrates with the national Mada network, represents a critical upgrade to the country's payment infrastructure, aimed at simplifying and enhancing the eyewear purchasing experience. Additionally, the increasing adoption of buy-now-pay-later services and digital wallets is particularly beneficial for eyewear transactions, as these purchases often involve higher price points and require extended decision-making periods. The modernization of payment systems is effectively addressing the traditional reliance on cash-based transactions, which has historically hindered the growth of the e-commerce eyewear market, especially for prescription products that necessitate thorough evaluation before purchase.

Technological advancements drives the market

Saudi Arabia's e-commerce eyewear market is witnessing a major overhaul, largely due to the adoption of augmented reality (AR) virtual try-on features and AI-driven recommendation systems. These tech advancements are not only reshaping what consumers expect but also how they shop. A pivotal moment in this evolution came in May 2025, when Google unveiled a USD 150 million investment, teaming up with Warby Parker to craft AI-enhanced glasses. This move underscores a broader industry pivot towards "smart" eyewear, merging traditional vision correction with cutting-edge digital features. Virtual try-on tech is already making waves, providing shoppers with a tailored and engaging buying journey. The blend of AR/VR with prescription eyewear offers brands a golden chance: to stand out by marrying crucial medical needs with the modern consumer's tech-savvy desires. Meanwhile, AI-driven insights from social media are spotlighting new trends, allowing brands to swiftly tweak their product lines and marketing strategies.

Growing awareness of eye health drives demand

The increasing reliance on remote work, e-commerce education, and social media has significantly contributed to the growing prevalence of digital eye strain (DES), particularly among younger populations. This condition has prompted consumers to actively seek solutions, such as blue light-blocking glasses and anti-glare lenses, through e-commerce platforms to mitigate symptoms like discomfort, dryness, and fatigue. Vision 2030 has allocated substantial financial resources to preventive healthcare initiatives, leading to improved early diagnosis rates for eye-related conditions. For example, the Seha Virtual Hospital has conducted over 1.6 million teleconsultations, many of which include eye screenings, effectively directing patients toward e-commerce eyewear purchases. Additionally, with life expectancy goals set at 80 years, there is an intensified focus on promoting long-term ocular health. Advanced AI-driven analytics are further enhancing the early detection of refractive errors, offering significant potential for improved eye care outcomes.

Influence of social media platforms and celebrity endorsements

Saudi Arabia's youthful demographic, with over 75% smartphone penetration, presents significant opportunities for social media-driven eyewear marketing through influencer collaborations and celebrity endorsements. In 2023, the Kingdom's digital economy was valued at over USD 40.94 billion[1]Source: International Trade Association, " Saudi Arabia Country Commercial Guide', www.trade.gov, highlighting the population's active use of digital platforms as primary channels for discovering fashion and health products. The cultural emphasis on personal appearance and brand awareness in Saudi society enhances the impact of social media marketing, particularly for eyewear, which holds both functional and fashion appeal. The rise of local digital influencers and the increasing adoption of global fashion trends via social media have created multiple engagement opportunities for eyewear brands. Additionally, internet usage for health-related information has grown, with influencers' websites playing a key role. For instance, in 2024, 25.4% of consumers aged 15-19 in Saudi Arabia used the internet for health-related information, according to the General Authority for Statistics (Saudi Arabia)[2]Source: General Authority for Statistics (Saudi Arabia), "Health Care Statistics", www.stat.gov.sa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit products limits the growth | −1.4% | Mostly on e-commerce marketplaces | Short term (≤ 2 years) |

| Logistical challenges in fulfillment and delivery | −0.9% | Remote regions | Medium term (2-4 years) |

| Lack of consumer awareness regarding e-commerce eyewear purchases | −0.7% | National | Medium term (2-4 years) |

| High dependence on imported eyewear products | −0.6% | National supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit products limits the growth

Unregulated third-party sellers on e-commerce platforms frequently distribute counterfeit branded eyewear. Customers, unaware of the deception, may receive inferior products, incorrect prescriptions, or, in severe cases, experience eye damage. Such incidents diminish trust in e-commerce shopping, prompting consumers to favor physical stores that ensure product authenticity. Brands leading in eyewear innovation, such as those producing AR smart glasses, AI-integrated lenses, and eco-friendly frames, face heightened risks of counterfeiting. These counterfeiters devalue genuine innovation and create challenges for authentic sellers in maintaining premium pricing. Unlicensed vendors circumvent the Medical Device Marketing Authorization, offering frames and lenses of questionable quality. The associated health risks include inaccurate prescriptions and potential allergic reactions. Although Saudi Arabia was removed from the USTR Priority Watch List in 2022, enforcement challenges persist. The Saudi government has made progress in intellectual property enforcement; however, the digital marketplace presents significant obstacles, with counterfeit products rapidly spreading across multiple platforms.

Logistical challenges in fulfillment and delivery

Saudi Arabia's vast geography and densely populated urban areas pose significant logistical challenges for eyewear deliveries, particularly for prescription products that require precise handling and timely distribution. Under its Vision 2030 initiative, the Kingdom has invested USD 18 billion in modernizing its logistics sector, focusing on infrastructure upgrades and digital integration to address these issues. However, the specialized requirements of eyewear products, such as prescription lenses and contact lenses, demand temperature-controlled storage and expedited delivery capabilities, which remain underdeveloped in several regions. Effective October 2024, a revised customs service fee structure introduced a 0.15% import fee, capped at SAR 500 for standard shipments and SAR 15 for e-commerce orders under SAR 1,000. These changes are likely to impact pricing strategies for imported eyewear products in the Kingdom.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spectacles Remain the Mainstay while Contacts Gain Pace

In 2025, spectacles led the Saudi Arabian e-commerce eyewear market, capturing 59.62% of the market share. Their ability to address both medical requirements and fashion preferences ensures they remain the primary revenue contributor. The demand for spectacles in Saudi Arabia has grown, supported by influencer-driven trends promoting the ownership of multiple frames for various occasions. Affordable polycarbonate lenses and lightweight titanium frames appeal particularly to students and first-time buyers. Additionally, the increasing adoption of blue-light filtering coatings highlights the influence of screen-intensive lifestyles on purchasing behavior.

Contact lenses are experiencing the fastest growth, with a projected CAGR of 6.12% through 2031. This growth is fueled by the rising participation of women in the workforce and an increasing interest in sports and outdoor activities. Digital health platforms now simplify the process by providing repeat prescriptions e-commerce, effectively eliminating traditional clinic delays. To address the Kingdom's dry climate, brands are emphasizing silicone-hydrogel materials, which enhance comfort and extend wear time. While sunglasses represent a smaller portion of the market, they maintain steady sales due to consistent demand for UV-blocking lenses driven by year-round sunshine. Prescription sunglasses, though a niche segment, combine medical correction with lifestyle attributes, signaling potential advancements toward smart-glasses in the future.

By Category: Mass Holds Volume, Premium Builds Margin

In 2025, the mass segment emerged as the leading category in the Saudi Arabian e-commerce eyewear market, accounting for a significant 68.32% share. This dominance was primarily attributed to the availability of an extensive assortment of products, attractive price promotions, and bundled lens packages that appealed to a broad consumer base. The frequent flash sales conducted by major e-commerce marketplaces further enhanced price transparency, fostering customer trust and encouraging repeat purchases. Additionally, a growing number of lower-income consumers increasingly preferred house brands, which provided affordable alternatives by replicating premium designs without compromising on style.

Premium frames are expected to grow at a 6.49% CAGR through 2031, fueled by demand from professionals and high-net-worth individuals seeking features such as lightweight acetates, proprietary hinge systems, and exclusive limited-edition collaborations. To support premium pricing, flagship stores of major global brands now offer personalized styling consultations and same-day lens edging services. Furthermore, smart eyewear prototypes currently in pilot testing are anticipated to launch within premium price categories. Over time, production scaling may result in certain SKUs transitioning from the premium segment to the mass market, enabling brands to sustain volume while optimizing their overall product mix.

By End User: Female Spend Leads, Unisex Designs Accelerate

In 2025, women contributed 53.21% of total revenue, driven by factors such as a strong interest in fashion discovery, active engagement in social commerce, and rising spending power, all of which align with eyewear upgrades. Female consumers show a preference for color-swapping lens options and frame embellishments that reflect seasonal fashion trends. Furthermore, loyalty programs offering birthday discounts and lens upgrade vouchers significantly enhance repeat purchases.

The unisex category, expanding at a 6.92% CAGR, benefits from streamlined designs and neutral color palettes that transcend traditional gender norms. Younger consumers increasingly favor minimalist metal frames and classic rectangular frames, which are worn interchangeably by men and women. Among male shoppers, the adoption of lighter materials and subtle brand detailing has driven an increase in average selling prices. Simultaneously, brands focusing on child-friendly hinges and stain-resistant coatings are targeting the Kingdom’s younger demographic, aiming to build early loyalty and secure long-term customer relationships.

By Platform Type: Third-Party Marketplaces Lead, Brand Sites Seek Differentiation

In 2025, Amazon KSA and Noon.com, two leading third-party portals, the third-party players captured a substantial 83.97% share of the Saudi Arabian e-commerce eyewear market and are growing at a 7.21% CAGR to 2031. This dominance is driven by their extensive product catalogs, nationwide delivery capabilities, and integrated wallet support. By utilizing deep retail data, these platforms effectively cross-sell accessories, such as lens cleaning kits, thereby increasing the overall basket value. However, their large scale also attracts parallel importers, which can undermine brand equity if not carefully managed.

To challenge this dominance, company-owned platforms are introducing advanced features, including virtual try-ons, lens thickness calculators, and streamlined insurance claim processes. By directing prescription orders to in-house labs, these platforms reduce delivery times, particularly for high-index or progressive lenses. Additionally, proprietary sites are better positioned to enforce compliance with Saudi Food and Drug Authority regulations, providing a competitive edge in regulated product categories. Subscription models for contact lenses and anti-blue-light filters are showing early potential in fostering stronger customer retention.

Geography Analysis

In Saudi Arabia, the e-commerce eyewear market demonstrates significant activity in Riyadh, Jeddah, and the Eastern Province. These regions benefit from a combination of higher disposable incomes, a well-established modern retail culture, and early adoption of 5G technology, making them key drivers of market growth. Urban consumers are more inclined to adopt fashion-forward eyewear trends and exhibit higher average spending per purchase compared to their rural counterparts. While the western provinces show a strong preference for European luxury eyewear brands, central regions prioritize durable and functional designs that cater to professional and academic needs.

Despite achieving an impressive 99% internet penetration rate, rural areas continue to face challenges related to last-mile delivery reliability and limited awareness of digital prescription services. However, government initiatives, such as the expansion of fiber-optic networks and the rollout of 77% 5G coverage, are progressively addressing these issues. Additionally, public healthcare facilities are incorporating tele-optometry tools, which direct patients to verified e-commerce platforms for eyewear purchases. A notable development in this regard is the Seha Virtual Hospital, which, by February 2025, will connect 224 physical hospitals. This initiative is expected to extend screening services to smaller towns, thereby facilitating e-commerce eyewear purchases once prescriptions are issued.

Emerging economic zones, including NEOM and Qiddiya, are attracting a growing population of young professionals who demand premium eyewear products and smart-wear integrations. These zones are creating localized demand clusters outside traditional urban centers. The surge in logistic registrations highlights the private sector's commitment to catering to these new demand nodes. Furthermore, companies are leveraging AI-driven marketing tools to segment audiences based on city and device type. This approach enables highly targeted promotions for specific frame styles and ensures delivery timelines align with regional consumer expectations, thereby enhancing customer satisfaction and market penetration.

Competitive Landscape

The Saudi Arabia E-commerce Eyewear Market is moderately fragmented due to the presence of local and international major players in the market, including Essilor-Luxottica SA, LVMH Moët Hennessy Louis Vuitton, Bausch + Lomb Corp., Alcon Inc., and Kering SA. Companies are striving for their market share, with mergers and acquisitions and expansion being the most adopted strategies, followed by partnerships and product innovation. Players operating in the e-commerce eyewear market in Saudi Arabia gained prominence due to the expansion of their distribution channels by establishing stores and warehouses at different locations across the country, which helps with easy and faster delivery.

Vertical integration consolidates lens supply, lab services, and retail operations under a unified framework, significantly enhancing bargaining power with insurers and e-commerce partners. Prominent regional players, such as MAGRABi, have achieved substantial growth by merging with Rivoli Vision, increasing their store count to over 290 locations and strengthening their dominance in mall-based optical retail spaces. Strategic funding has enabled Eyewear to integrate e-commerce and offline retail formats effectively, establishing compact stores that also function as fulfillment hubs. This approach has optimized logistics, reducing delivery times to less than 24 hours in key urban centers.

Technological advancements are driving innovation, with virtual try-on features, AI-powered customer support, and augmented reality (AR) sizing tools becoming central to platform enhancements. AI-integrated initiatives are poised to transform the e-commerce eyewear market in Saudi Arabia by combining wellness solutions with digital connectivity. Simultaneously, efforts to combat counterfeit products, achieve sustainability objectives, and implement recycled-acetate programs are emerging as critical factors in shaping brand reputation and differentiation.

Saudi Arabia E-commerce Eyewear Industry Leaders

-

EssilorLuxottica SA

-

LVMH Moët Hennessy Louis Vuitton

-

Kering SA

-

Alcon Inc.

-

Bausch + Lomb Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Johnson and Johnson has expanded its portfolio of presbyopia-correcting intraocular lenses (PC - IOL) with the roll-out of TECNIS Odyssey IOL. The new full visual range IOL offers high-quality and continuous vision with unmatched range.

- December 2024: EssilorLuxottica has acquired Espansione Group, a company specializing in non-invasive medical devices for ophthalmology, including Light Modulation, Low-level Light Therapy, and Intense Pulsed Light technology.

- May 2023: EssilorLuxottica and Chalhoub Group have formed a joint venture to advance direct eyewear retail in Saudi Arabia. This partnership aims to transform the eyewear market by integrating EssilorLuxottica's expertise in eyewear, innovative technology, and premium brands with Chalhoub Group's in-depth knowledge of regional consumer preferences and dedication to delivering experiences.

Saudi Arabia E-commerce Eyewear Market Report Scope

Eyewear is a product worn over the eyes for vision correction or protection. This can be purchased for a variety of reasons, including fashion or adornment, UV infrared ray protection, and so on. The Saudi Arabia E-commerce Eyewear Market studied is segmented by product category and end user. Based on product category, the market is segmented into spectacles, sunglasses, contact lenses, and other product types. Based on end users, the market is segmented into three categories: women, men, and unisex. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Spectacles |

| Sunglasses |

| Contact Lenses |

| Mass |

| Premium |

| Men |

| Women |

| Unisex |

| Kids/Teen |

| Third-Party Marketplace |

| Company-owned Platform |

| By Product Type | Spectacles |

| Sunglasses | |

| Contact Lenses | |

| By Category | Mass |

| Premium | |

| By End User | Men |

| Women | |

| Unisex | |

| Kids/Teen | |

| By Platform Type | Third-Party Marketplace |

| Company-owned Platform |

Key Questions Answered in the Report

What is the current value of the Saudi Arabian e-commerce eyewear market?

The market is valued at USD 165.48 million in 2026 and is forecast to hit USD 219.07 million by 2031.

Which product segment leads sales in Saudi Arabia?

Spectacles lead with 59.62% of the Saudi Arabia E-commerce Eyewear Market share while contact lenses are growing fastest at a 6.12% CAGR.

Why do third-party marketplaces dominate eyewear sales?

They offer large assortments, built-in payment options and nationwide logistics, which together captured 83.97% of 2025 revenue.

How is Vision 2030 influencing eyewear demand?

Vision 2030 invests in digital infrastructure, preventive healthcare and logistics upgrades, all of which raise awareness and convenience for e-commerce eyewear purchasing.

Page last updated on: