Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.04 Billion |

| Market Size (2026) | USD 6.27 Billion |

| Market Size (2031) | USD 7.58 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

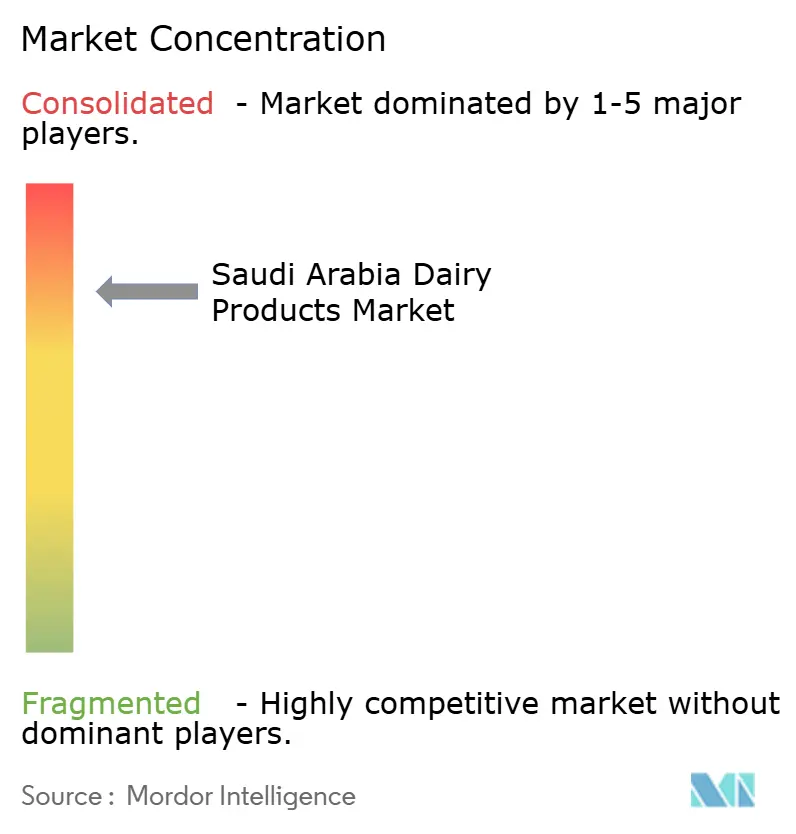

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Dairy Products Market Analysis by Mordor Intelligence

The Saudi Arabia dairy products market size is expected to grow from USD 6.04 billion in 2025 to USD 6.27 billion in 2026 and is forecast to reach USD 7.58 billion by 2031 at 3.85% CAGR over 2026-2031. This growth aligns with the Kingdom's Vision 2030 food-security agenda, which has shifted the nation from being a net importer to a net exporter by enhancing domestic production self-sufficiency. Significant investments, including Almarai's SAR 18 billion five-year expansion and the development of cluster farms in Al-Kharj, are driving capacity growth while reducing per-unit logistics costs. Rapid urbanization, population growth, and rising disposable incomes are increasing per-capita dairy consumption, particularly in functional, fortified, and convenient formats. As consumers increasingly associate dairy with benefits such as calcium, protein, and gut health, demand for fortified, probiotic, and low-fat dairy products is rising. Additionally, advancements in cold storage and transport technologies are ensuring product freshness and reliable supplies, even in challenging climates. The modernization of retail, growth of e-commerce, and a strong cold-chain infrastructure are enhancing product accessibility and shelf life. This not only supports premium market positioning but also strengthens cross-border exports to neighboring Gulf Cooperation Council (GCC) countries.

Key Report Takeaways

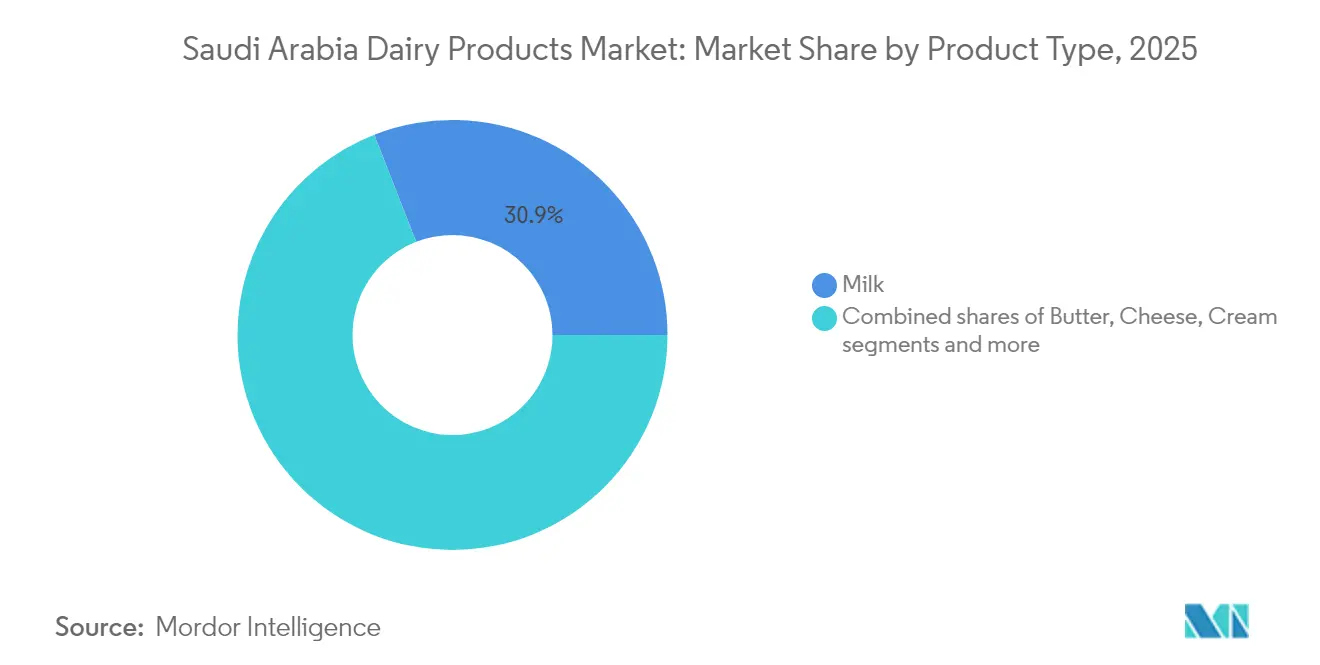

- By product type, milk led the Saudi Arabia dairy products market with a 30.92% revenue share in 2025; butter is on track to post the fastest growth of 4.77% CAGR through 2031.

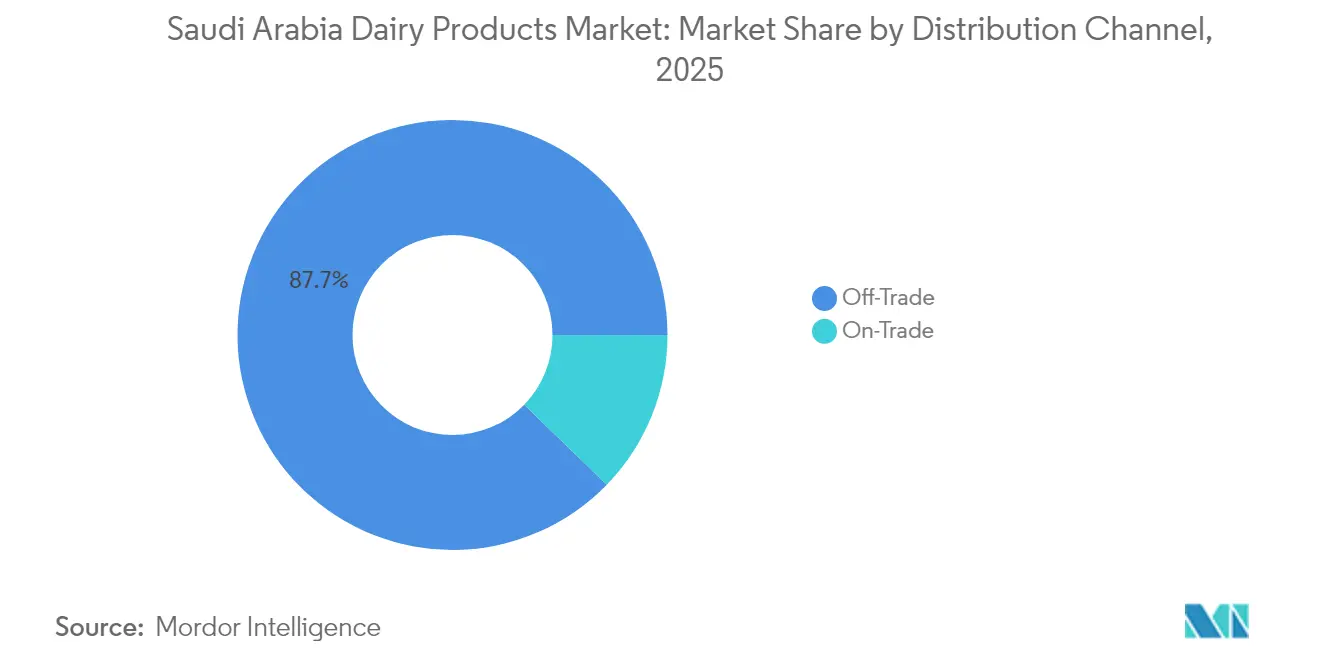

- By distribution channel, off-trade captured 87.74% of the Saudi Arabian dairy products market share in 2025, whereas on-trade is projected to expand at a 5.19% CAGR to 2031.

- By geography, the Eastern Region accounted for 32.28% of the Saudi Arabian dairy products market in 2025, while the Western Region is advancing at a 4.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Dairy Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer interest in convenience and ready-to-eat dairy products | +0.8% | National, with early gains in Riyadh, Jeddah, Dammam | Short term (≤ 2 years) |

| Rapid growth of modern grocery retail and cold-chain logistics | +0.6% | Western and Eastern regions primarily | Medium term (2-4 years) |

| Rising demand for functional/fortified dairy (probiotics, lactose-free) | +0.5% | Urban centers nationwide | Long term (≥ 4 years) |

| Expansion of school milk and nutrition programmes | +0.4% | National coverage | Medium term (2-4 years) |

| Government-led health and wellness campaigns | +0.3% | National | Long term (≥ 4 years) |

| Diversification of flavor, format, and health benefit claims | +0.2% | Major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising consumer interest in convenience and ready-to-eat dairy products

With the acceleration of urban lifestyles, consumers are increasingly opting for quick and reliable dairy options, driving demand for conveniently packaged, ready-to-eat (RTE) dairy products. These include single-serve yogurts, yogurt drinks, cheese snacks, pre-cut cheese portions, and ready-to-use dairy desserts. Urbanization in Saudi Arabia has significantly influenced consumption patterns. In 2023, 84.95% of the population resided in urban areas, according to the World Bank[1]Source: World Bank, "World Development Indicators", worldbank.org, highlighting the role of working professionals and dual-income households in boosting demand for grab-and-go dairy products. The convenience segment is experiencing robust growth, with products like flavored milk, yogurt cups, and cheese snacks recording double-digit sales increases. This trend is particularly prominent among individuals under 25, who value portability and on-the-go consumption. As Saudi Arabia's Vision 2030 drives economic diversification, resulting in longer commutes and busier lifestyles, convenience is becoming a lasting driver in the dairy market rather than a temporary shift in preferences.

Rapid growth of modern grocery retail and cold-chain logistics

Saudi Arabia's retail sector has undergone significant transformation, leading to the establishment of a highly advanced cold-chain infrastructure that facilitates the nationwide distribution of premium dairy products. Hypermarkets and supermarkets now play a pivotal role in driving dairy sales, contributing substantially to the overall market. Prominent retailers such as Carrefour and LuLu have integrated IoT-enabled temperature monitoring systems, which ensure the preservation of product quality and integrity throughout the supply chain, from the farm to the retail shelf. Additionally, the rapid growth of e-commerce platforms, including global players like Amazon Fresh and various local applications, has further accelerated the development of cold-chain logistics. This growth has heightened the demand for specialized refrigerated vehicles to ensure efficient and reliable last-mile delivery. Investments in this infrastructure not only provide a competitive edge for established market players but also support the positioning of premium dairy products and enhance regional export opportunities to neighboring GCC markets.

Rising demand for functional / fortified dairy

As consumers increasingly prioritize digestive health, lactose intolerance management, and nutritional benefits, the demand for products such as probiotic yogurts and lactose-free milk continues to grow significantly. These products are widely regarded as healthier alternatives, offering benefits like improved gut health, enhanced immunity, and superior nutritional value compared to traditional dairy options. In Saudi Arabia, rising health awareness has transformed functional dairy from a niche category into a mainstream market segment. Government-driven health campaigns have played a pivotal role in validating probiotic claims, while the SFDA's streamlined approval process for functional foods has accelerated the introduction of innovative formulations to the market. Local producers are actively collaborating with international enzyme manufacturers to create culturally relevant flavors and formats that cater to local preferences. For instance, Al Safi Danone offers an Arabic coffee-flavored probiotic drink, which successfully combines traditional tastes with modern health benefits. Additionally, policies under Saudi Vision 2030 emphasize the importance of promoting healthier food options alongside ensuring food security, thereby fostering increased investments in the functional dairy sector.

Expansion of school milk and nutrition programmes

The Ministry of Education in Saudi Arabia reported that its nationwide school nutrition initiative, which serves 5.2 million students across 35,000 schools, has created a reliable institutional demand valued at approximately USD 400 million annually in 2024[2]Source: Ministry of Education in Saudi Arabia, "Data and Statistics", moe.gov.sa. This program is designed to address childhood malnutrition by mandating the daily provision of milk to students. Additionally, it supports local dairy producers through preferential procurement policies, ensuring that domestic suppliers benefit from the initiative. The program has evolved to include not only standard milk but also fortified variants enriched with essential nutrients such as calcium, vitamin D, and iron. These fortified options aim to address specific nutritional deficiencies identified in national health surveys, thereby improving the overall health outcomes of students. Regional disparities in the implementation of the program have opened up opportunities for local suppliers to participate. For instance, NADEC has secured multi-year contracts to supply milk in the northern provinces, while Almarai has established a dominant presence in the central and western regions. The program's success has sparked discussions about its potential expansion to include universities and government institutions. If implemented, this expansion could significantly increase the institutional market size, potentially doubling its current value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water scarcity and high feed-import costs | -0.9% | National, acute in central regions | Long term (≥ 4 years) |

| Growing preference for plant-based alternatives | -0.4% | Urban centers, particularly Western region | Medium term (2-4 years) |

| Retail listing fees and price-promotion race squeezing producer margins | -0.3% | National retail networks | Short term (≤ 2 years) |

| Rising geopolitical freight risk on imported dairy inputs | -0.2% | National, affecting import-dependent producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water scarcity and high feed-import costs

Saudi Arabia's arid climate and limited renewable water resources create significant cost pressures, posing challenges to the scalability of its dairy production. On average, dairy farming in the country consumes approximately 1,000 liters of water to produce a single liter of milk. This water usage is notably higher than the global benchmark of 700 liters, primarily due to the cooling requirements necessitated by the region's extreme temperatures. To mitigate these challenges, leading dairy producers are increasingly investing in advanced water recycling technologies and precision irrigation systems. For example, Almarai, a key player in the market, has implemented state-of-the-art treatment facilities, achieving an impressive 56% water recycling rate. Furthermore, the Saudi government has taken proactive steps to conserve water resources by phasing out wheat production and redirecting agricultural support toward cultivating more water-efficient crops. Despite these initiatives, dairy farming remains vulnerable to potential water allocation restrictions in the future. Such restrictions could hinder herd expansion, elevate operational costs, and pose additional challenges to the industry's growth and long-term sustainability.

Growing preference for plant-based alternatives

Urban consumers, particularly health-conscious millennials and expatriates, are driving a significant and transformative shift toward plant-based dairy alternatives. This change is reflected in the increasing popularity of products such as oat milk, almond milk, and soy-based beverages across major metropolitan areas. International brands, including Oatly and Alpro, have strategically penetrated these markets by partnering with local distributors, ensuring their products are accessible to a broader consumer base. At the same time, regional manufacturers are innovating by developing culturally adapted formulations that incorporate locally favored ingredients like dates and nuts, effectively catering to diverse consumer preferences. This trend is most pronounced in premium retail channels and coffee shops, where plant-based options are not only widely available but also command a significant price premium over traditional dairy products. In response to this growing demand, traditional dairy producers are implementing diversification strategies. Many have launched their own plant-based product lines, aiming to capture a share of this expanding market segment while simultaneously safeguarding their core dairy business from potential market share erosion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Maintains Dominance Despite Premium Diversification

Milk captures a 30.92% share of the market in 2025, reflecting its deep-rooted cultural importance and its role as a staple in daily consumption across households. This segment benefits significantly from government-led nutrition programs aimed at promoting healthy dietary habits. Additionally, milk's traditional integration into key cultural practices, such as its use in Arabic coffee and its presence in Ramadan iftar meals, further reinforces its prominence. Fresh milk remains the leading choice within the segment; however, flavored milk options, particularly chocolate and strawberry, have experienced a notable rise in demand among younger consumers. These flavored variants are positioned as premium products, commanding a 25% higher price compared to plain milk.

Butter stands out as the fastest-growing segment, achieving a 4.77% CAGR through 2031, driven by the growth of the bakery industry and the increasing adoption of Western diets. Vision 2030's tourism initiatives have further boosted demand for international cuisines and baking ingredients. Cheese follows closely, with processed cheese dominating food service applications, while natural cheese gains traction in retail due to its premium positioning. Yogurt emerges as a hub of innovation, with probiotic and Greek-style variants capturing market share from traditional formats. Dairy desserts, including ice cream, experience seasonal demand fluctuations but maintain steady growth through premiumization and flavor localization strategies that incorporate traditional Middle Eastern ingredients like rosewater and pistachio.

By Distribution Channel: Off-Trade Dominance Faces On-Trade Disruption

Off-trade channels hold an 87.74% market share in 2025, highlighting Saudi Arabia's retail-focused consumption patterns and widespread supermarket presence. Hypermarkets and supermarkets significantly contribute to this segment, leveraging advanced cold-chain systems and diverse product offerings to meet consumer preferences. Convenience stores benefit from extended operating hours and their proximity to residential areas, while online retail experiences rapid growth, driven by an increasing number of internet users, same-day delivery options, and subscription services for dairy essentials. According to the Saudi Press Agency, mobile phones were used for 98.9% of internet browsing in Saudi Arabia in 2024.

On-trade channels, despite accounting for only 12.26% of the market share, demonstrate the highest growth potential, with a projected CAGR of 5.19% through 2031. This growth reflects the expansion of Saudi Arabia's hospitality sector, characterized by increasing hotel occupancy and a rise in restaurant establishments. Large-scale projects like NEOM and the Red Sea developments are driving foodservice demand, while shifting social dynamics are encouraging younger demographics to dine out more frequently. The growing coffee culture, marked by the proliferation of specialty cafes, is boosting the consumption of premium dairy products in lattes, cappuccinos, and artisanal beverages. Additionally, food delivery platforms such as HungerStation and Jahez are extending the reach of on-trade channels, enabling restaurants to serve a broader customer base and increasing the demand for dairy ingredients in prepared foods and desserts.

Geography Analysis

The Eastern Region holds a 32.28% market share in 2025, benefiting from its proximity to major dairy production hubs and a robust cold-chain network. The Al-Kharj dairy cluster, a key asset in this region, hosts Almarai's largest processing facilities and automated distribution centers with an annual capacity of 2.5 billion kilograms. The region's industrial base, coupled with a diverse expatriate workforce, ensures consistent demand for various dairy products. Additionally, its port access facilitates the seamless import of specialized ingredients and packaging materials. Dammam's development as a logistics hub further enhances distribution efficiency, enabling cost-effective supply to nearby provinces and GCC export markets.

The Western Region is expected to achieve the highest growth, with a projected CAGR of 4.94% through 2031. Jeddah's role as a commercial gateway and the ongoing development of the Red Sea economic zone are key growth drivers. Religious tourism, particularly the influx of Hajj and Umrah pilgrims, generates seasonal demand spikes that require adaptable supply chain solutions. The NEOM megacity project, anticipated to house 1 million residents, presents a significant opportunity for establishing a comprehensive dairy supply network. Retail modernization in the Western Region surpasses national averages, with international chains like Carrefour and LuLu expanding rapidly to cater to affluent urban populations. Additionally, the region's proximity to African markets positions it as a strategic export hub for dairy products targeting emerging economies across the Red Sea corridor.

The Northern and Central regions benefit from Riyadh's position as the political and economic capital. The concentration of government institutions and corporate headquarters in this area drives substantial purchasing power. Vision 2030 initiatives, such as King Salman Park and Diriyah Gate, are attracting international businesses and expatriate families with premium dairy preferences. Meanwhile, the Southern Region, although holding a smaller market share, is experiencing steady growth driven by agricultural development programs and trade with Yemen. Planned infrastructure investments are set to enhance connectivity to Jordan and Iraq, positioning the region as a gateway to broader Middle Eastern markets. Additionally, the SFDA's regional inspection centers ensure consistent quality standards across all regions, supporting inter-regional trade and export readiness.

Competitive Landscape

The Saudi Arabian dairy products market is highly concentrated, with the top three players accounting for a significant portion of the market share. This dominance creates significant entry barriers while enabling considerable economies of scale. Almarai leads the market through vertical integration, covering dairy farming, processing, distribution, and retail partnerships. This position is further supported by SAR 18 billion in investment commitments extending through 2028. Competition has shifted focus from pricing to innovation and premium positioning, with companies heavily investing in product development, advanced packaging technologies, and digital transformation. Smaller regional players, such as Al Rawabi and Bateel Dairy, compete by targeting niche markets with specialized products catering to specific consumer needs or geographic areas.

Major players in the market include Almarai Company, Arla Foods AmbA, Danone SA, Saudia Dairy and Foodstuff Company (SADAFCO), and The National Agricultural Development Company (NADEC). The Saudi Arabian dairy market features a mix of domestic and international companies employing various strategic initiatives. Firms are prioritizing product innovation, focusing on clean-label products, organic options, and functional dairy offerings to align with changing consumer preferences. Digital transformation is a key driver of operational excellence. Companies are also expanding production capacities by building new facilities, modernizing existing ones, and strengthening distribution networks to enhance market penetration and product accessibility.

Technology adoption has become a critical competitive advantage. Leading companies are implementing AI-driven supply chain optimization, automated quality control systems, and IoT-enabled cold-chain monitoring. Opportunities exist in organic dairy, camel milk products, and functional foods designed for specific health conditions such as diabetes and lactose intolerance. The growth of direct-to-consumer channels and subscription models presents opportunities for new entrants, while established players benefit from compliance with SFDA standards and strong quality management systems. Strategic collaborations with international technology providers and ingredient suppliers are driving rapid innovation. For example, Al Safi Danone leverages its parent company’s expertise to introduce advanced fermentation technologies and probiotic formulations tailored to local preferences.

Saudi Arabia Dairy Products Industry Leaders

-

Almarai Company

-

Arla Foods AmbA

-

Danone SA

-

Saudia Dairy and Foodstuff Company (SADAFCO)

-

The National Agricultural Development Company (NADEC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sawani, backed by the Public Investment Fund and owner of the NOUG brand, collaborated with GEA, a German specialist in modern milking systems, to establish its model farm. This cutting-edge facility produces 500,000 liters of camel milk monthly.

- January 2025: Almarai, the largest dairy producer in Saudi Arabia, is poised for substantial growth, unveiled a USD 4.8 billion investment as part of its new five-year strategic blueprint. This move underscores Almarai's dedication to bolstering Saudi Arabia's Vision 2030 ambition: attaining food self-sufficiency and curbing the nation's import dependencies.

- November 2024: Savola Group has announced the distribution of a 34.52% stake in Almarai to its shareholders, a transaction valued at SAR 12.8 billion, signifying a major ownership restructuring in the Kingdom's largest dairy company.

- January 2024: SADAFCO has launched a new distribution depot in Makkah, boasting an annual capacity of 50,000 tonnes. This move not only caters to the surging demand from religious tourism but also streamlines supplies to retailers in the western region. The state-of-the-art facility features cutting-edge cold-chain technology and automated inventory management systems.

Saudi Arabia Dairy Products Market Report Scope

Butter, Cheese, Cream, Dairy Desserts, Milk, Sour Milk Drinks, Yogurt are covered as segments by Category. Off-Trade, On-Trade are covered as segments by Distribution Channel.

By Product Type

| Butter | ||

| Cheese | Natural Cheese | Cheddar |

| Cottage | ||

| Ricotta | ||

| Parmesan | ||

| Others | ||

| Processed Cheese | ||

| Cream | Fresh Cream | |

| Cooking Cream | ||

| Whippng Cream | ||

| Others (Clottted, Sour Cream) | ||

| Dairy Desserts | Ice Cream | |

| Cheesecakes | ||

| Frozen Desserts | ||

| Others (Puddings/desserts, trifles, fools) | ||

| Milk | Condensed milk | |

| Flavored Milk | ||

| Fresh Milk | ||

| UHT Milk (Ultra-high temperature milk) | ||

| Powdered Milk | ||

| Yogurt | Drinkable | |

| Spoonable | ||

| Sour Milk Drinks | ||

By Distribution Channel

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others (Warehouse clubs, gas stations, etc.) |

| By Product Type | Butter | ||

| Cheese | Natural Cheese | Cheddar | |

| Cottage | |||

| Ricotta | |||

| Parmesan | |||

| Others | |||

| Processed Cheese | |||

| Cream | Fresh Cream | ||

| Cooking Cream | |||

| Whippng Cream | |||

| Others (Clottted, Sour Cream) | |||

| Dairy Desserts | Ice Cream | ||

| Cheesecakes | |||

| Frozen Desserts | |||

| Others (Puddings/desserts, trifles, fools) | |||

| Milk | Condensed milk | ||

| Flavored Milk | |||

| Fresh Milk | |||

| UHT Milk (Ultra-high temperature milk) | |||

| Powdered Milk | |||

| Yogurt | Drinkable | ||

| Spoonable | |||

| Sour Milk Drinks | |||

| By Distribution Channel | On-trade | ||

| Off-trade | Convenience Stores | ||

| Specialist Retailers | |||

| Supermarkets and Hypermarkets | |||

| On-line Retail | |||

| Others (Warehouse clubs, gas stations, etc.) | |||

Market Definition

- Butter - Butter is a yellow-to-white solid emulsion of fat globules, water, and inorganic salts produced by churning the cream from cows’ milk

- Dairy - Dairy product include milk and any of the foods made from milk, including butter, cheese, ice cream, yogurt, and condensed and dried milk.

- Frozen Desserts - Frozen dairy dessert means and includes products containing milk or cream and other ingredients which are frozen or semi-frozen prior to consumption, such as ice milk or sherbet, including frozen dairy desserts for special dietary purposes, and sorbet

- Sour Milk Drinks - Sour milk is thick, curdled milk, with a sour taste, obtained from the fermentation of milk. Sour milk drinks such as kefir, laban, buttermilk have been considered in the study

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms