Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

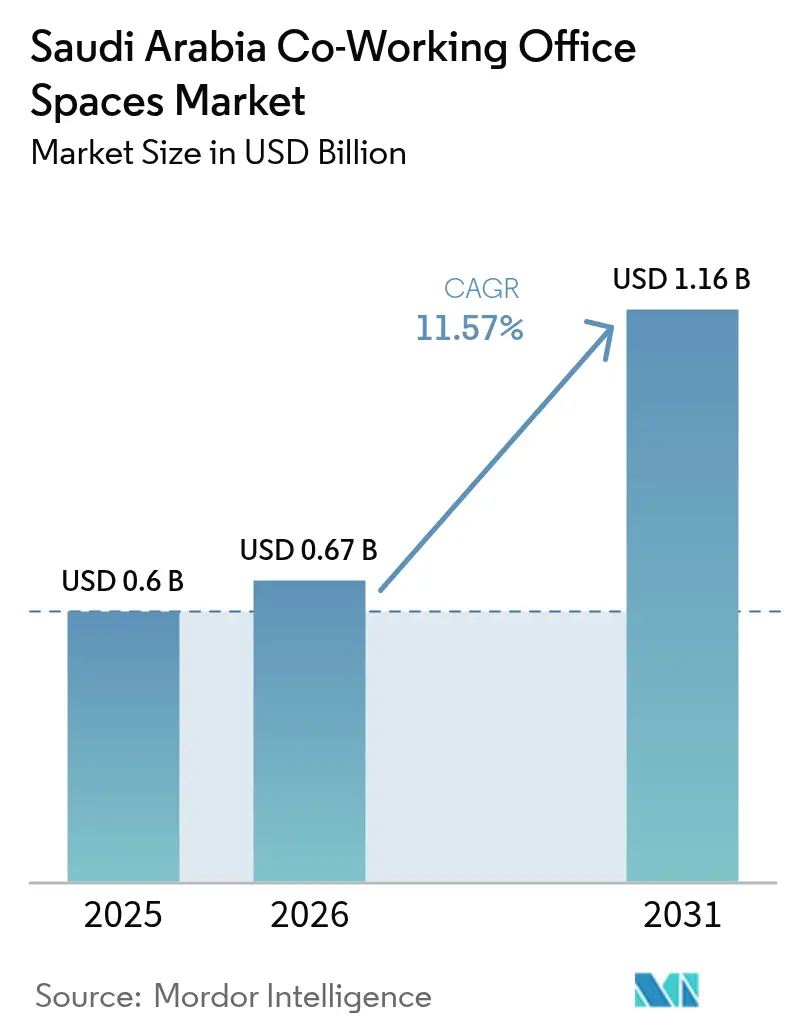

| Base Year Market Size (2025) | USD 0.60 Billion |

| Market Size (2026) | USD 0.67 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 11.57% CAGR |

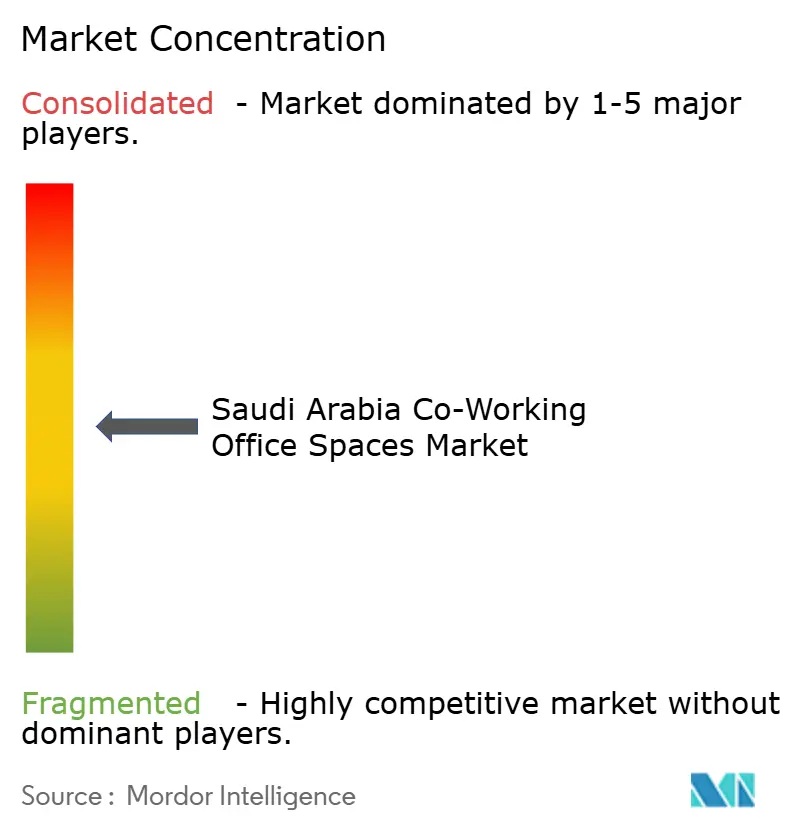

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Coworking Office Spaces Market Analysis by Mordor Intelligence

The Saudi Arabia Coworking Office Spaces Market size is expected to grow from USD 0.60 billion in 2025 to USD 0.67 billion in 2026 and is forecast to reach USD 1.16 billion by 2031 at 11.57% CAGR over 2026-2031. The momentum rests on Vision 2030’s push for economic diversification, a steadily widening base of small businesses, and the arrival of more than 500 foreign regional headquarters since 2021. A three-fold jump in licensed accelerators, incubators, and co-working sites to 273 by mid-2025 confirms strong policy alignment with flexible workspace demand. Corporations are embedding hybrid work policies that favor short, renewable commitments over long leases, while real-estate developers are integrating co-working floors into mixed-use projects to ensure steady traffic and yield. Rising venture funding volatility is nudging start-ups toward cost-efficient desks instead of private offices, and international operators are responding by pairing global standards with local cultural cues. Together, these shifts underpin a market where agility and community services increasingly outweigh sheer floorplate size.

Key Report Takeaways

- By size of facility, large sites led with 46.85% of the Saudi Arabia Coworking Office Spaces Market share in 2025. Medium facilities are projected to post the fastest 12.11% CAGR through 2031.

- By sector, information technology and IT-enabled services held 38.75% of the Saudi Arabia Coworking Office Spaces Market share in 2025. Banking, financial services, and insurance are slated to expand at a 12.42% CAGR up to 2031.

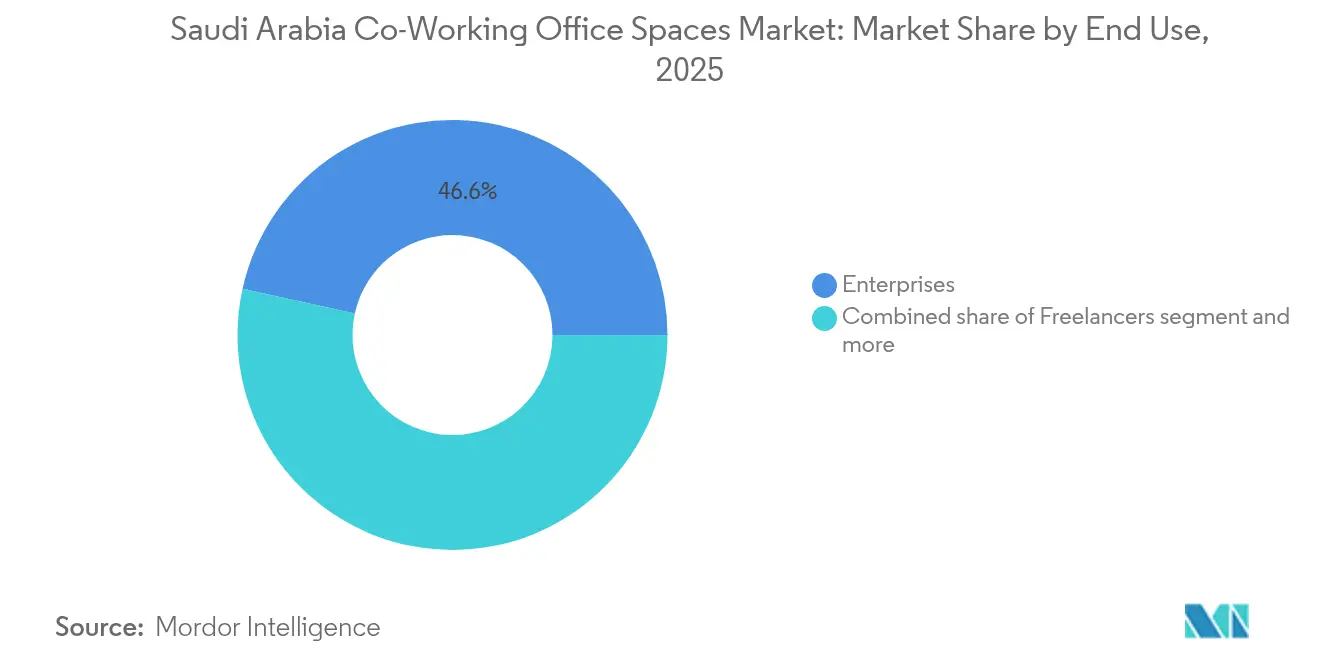

- By end user, enterprises accounted for 46.55% of the Saudi Arabia Coworking Office Spaces Market size in 2025. Freelancers are on track to climb at a 12.65% CAGR during the same period.

- By city, Riyadh captured 58.70% revenue share in 2025; the Dammam Metropolitan Area is forecast to progress at a 13.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Coworking Office Spaces Market Trends and Insights

Drivers Impact Analysis*

| Drivers | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 fostering entrepreneurship and SME ecosystems that drive co-working demand | +2.5% | National, with concentration in Riyadh, Jeddah, and NEOM | Medium term (2-4 years) |

| Adoption of hybrid work practices among corporates expanding flexible workspace needs | +1.8% | Riyadh and Jeddah primarily, expanding to DMA | Short term (≤ 2 years) |

| Government-backed free zones and innovation hubs creating demand for co-working clusters | +1.2% | NEOM, King Abdullah Economic City, and four new SEZs | Long term (≥ 4 years) |

| Rising demand for cost-effective and short-term office solutions among start-ups | +1.0% | National, with higher concentration in major cities | Short term (≤ 2 years) |

| Entry of international co-working operators in Riyadh and Jeddah expanding supply | +0.8% | Riyadh and Jeddah metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Entrepreneurship Agenda Expands SME Demand

Saudi Arabia’s Vision 2030 program has licensed 273 accelerators, incubators, and co-working sites by mid-2025, triple the pre-2020 count. SME numbers climbed to 1.24 million by mid-2023, while government-backed initiatives such as the Jada30 project support 245 enterprises and 60,000 beneficiaries, turning co-working hubs into business-enablement platforms rather than mere desk providers. The state’s pledge to raise SME GDP contribution ensures sustained workspace incentives, and operators that embed advisory, mentoring, and financing support into memberships are best placed to win recurring revenue. Consequently, the Saudi Arabia Coworking Office Spaces Market keeps deepening its linkage to the Kingdom’s diversified growth engines.

Hybrid Work Uptake Among Corporates

Corporate transformation programs show that 32% of change projects tie directly to Vision 2030 goals, with operational efficiency ranking high. A Gensler survey found employees allocate 28% of work time to tasks requiring focused solitude, underscoring a mismatch between existing layouts and evolving work modes. Over 500 multinationals now navigating Saudi regional-HQ rules are seeking flexible seat counts as they scale local teams. EY’s own 11,691 m² office in King Abdullah Financial District features booking apps, wellness pods, and on-demand collaboration rooms, exemplifying the hybrid blueprint. Such precedents validate flexible models and propel fresh demand in the Saudi Arabia Coworking Office Spaces Market[1]Eyad Al-Sayed, “EY Riyadh Wavespace Fact Sheet,” Ernst & Young MENA Disclosure, ey.com.

Government Free Zones and Innovation Hubs

Four new special economic zones—Riyadh, Jazan, Ras Al-Khair, and King Abdullah Economic City—offer 100% foreign ownership, customs waivers, and reduced taxes, stimulating location-agnostic entrepreneurship. NEOM alone attracted USD 10.6 billion commitments in 2023, including a USD 10 billion logistics joint venture with DSV that will require transient project offices. The Public Investment Fund has reclaimed the King Abdullah Financial District to accelerate roll-outs, and JPMorgan’s feasibility guidance confirms global investor interest. As policy packages remove red tape, co-working operators can embed in free-zone towers to serve cross-border teams, an angle expected to add structural lift to the Saudi Arabia Coworking Office Spaces Market[2]Ministry of Economy & Planning, “Special Economic Zones Framework 2025,” Government of Saudi Arabia, arabnews.com.

Entry of Global Co-Working Brands

Former WeWork founder Adam Neumann re-entered the field with a “conscious community” venture funded by more than USD 1 billion of Saudi capital in September 2024. IWG recorded GBP 3.3 billion (USD 4.1 billion) top-line in 2023, with 80% of new hubs in suburbs, mirroring the Kingdom’s multi-centered urban plan. Hospitality operators are fusing extended-stay rooms with shared offices to woo digital nomads, while developers such as Cenomi Centers channel USD 1.39 billion into Riyadh and Jeddah schemes that include plug-and-play desks. Best-in-class brands raise service expectations, introduce global tech stacks, and ultimately broaden the Saudi Arabia Coworking Office Spaces Market footprint beyond first movers[3]International Workplace Group, “2023 Annual Results Statement,” IWG Investor Centre, iwgplc.com.

Restraints Impact Analysis*

| Restraints | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural resistance to shared spaces among traditional corporates | -1.5% | National, with stronger impact in conservative regions | Medium term (2-4 years) |

| Economic volatility and oil price dependency affecting start-up funding and co-working occupancy | -1.2% | National, with higher impact on startup-dependent segments | Short term (≤ 2 years) |

| Limited supply of established operators beyond major cities | -1.0% | Rest of Saudi Arabia excluding Riyadh, Jeddah, DMA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cultural Resistance to Shared Space Norms

Long-standing preferences for hierarchical private offices slow the adoption of shared environments among family-owned conglomerates and public agencies. Gensler research highlights underperformance in collaboration zones, reflecting cultural unease with open layouts. Yet success stories such as Mustqr, a women-only hub in Dhahran now past its third anniversary, prove that culturally sensitive design can unlock new cohorts. International HQ mandates compel legacy firms to pilot flexible pods, and generational turnover is introducing executives educated abroad who favor communal energy. Even so, a measured shift is expected, tempering growth trajectories in the Saudi Arabia Coworking Office Spaces Market for the medium term.

Limited Operator Depth Outside Top Cities and Funding Volatility

Riyadh, Jeddah, and the Dammam Metropolitan Area dominate current supply, leaving secondary cities underserved despite Vision 2030 grants earmarked for provincial growth. Lower density and thinner tenant pipelines weigh on utilization economics, forcing providers to consider franchise, pop-up, or retail-hybrid formats for viability. Venture funding fell 70% in 2024, shrinking start-up occupancy budgets even as state programs pledged fresh stimulus. Operators that digitize access control, remote management, and dynamic pricing stand a better chance of penetrating frontier locales. Until scalable templates mature, geographic expansion of the Saudi Arabia Coworking Office Spaces Market will skew toward proven corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size & Scale of Facility: Medium Spaces Anchor Community-Centric Growth

Large facilities controlled 46.85% of the Saudi Arabia Coworking Office Spaces Market share in 2025, fueled by anchor-tenant demand in Riyadh’s central business districts. However, medium spaces are pacing ahead at a forecast 12.11% CAGR to 2031, signaling user preference for neighborhoods that deliver intimacy and purposeful networking. Operators report that 50-150-member hubs strike the right cost-to-service ratio, offering program rooms, mentor hours, and curated events without diluting community bonds. The Saudi Arabia Coworking Office Spaces Market size allocated to medium footprints is likely to accelerate as suburban transport links shorten commute times and remote workers seek third-place alternatives closer to home. Over the long haul, large flagship sites will remain relevant for multinational town-halls, yet replication economics favor the mid-tier template.

The expansion of women-only hubs and fintech-focused lofts underscores how medium settings accommodate specialized themes that large halls cannot easily segregate. Mustqr in Dhahran and comparable concepts in Jeddah leverage tailored fit-outs, privacy protocols, and targeted programming to appeal to distinct cohorts. This specialization trend helps operators lift retention rates and ancillary service revenues through event hosting and pay-per-use advisory pods. Parallel to IWG’s global suburb-first strategy, domestic players are eyeing mixed-use malls and transit-adjacent plots to scale medium centers cheaply, further embedding the segment within the broader Saudi Arabia Coworking Office Spaces Market.

By Sector: Financial Services Accelerate Digital Adoption

Information technology and IT-enabled services commanded 38.75% of the Saudi Arabia Coworking Office Spaces Market share in 2025, buttressed by coding bootcamps, SaaS start-ups, and cloud system integrators. Yet banking, financial services, and insurance (BFSI) verticals are on track for the quickest 12.42% CAGR through 2031 as regulators fast-track open-banking and crypto-asset frameworks. Financial institutions gravitate toward flexible hubs in King Abdullah Financial District to run project squads, vendor workshops, and regulatory sandboxes under one subscription. The Saudi Arabia Coworking Office Spaces Market size devoted to BFSI pods will likely broaden as Shariah-compliant fintech founders demand institutional-grade IT security within communal studios.

Business consulting and legal advisory teams form a stable mid-tier, benefiting from the entry of more than 500 foreign HQs needing local compliance counsel. Ancillary segments such as life sciences and clean-energy services also tap temporary rooms for M&A diligence and EPC bid reviews. As Vision 2030 broadens capital-market and insurance reforms, BFSI occupiers will increasingly value variable term commitments to align headcount with deal cycles, bolstering the resilience of the Saudi Arabia Coworking Office Spaces Market.

By End Use: Freelancers Catalyze Flexible Membership Models

Enterprises generated 46.55% of the Saudi Arabia Coworking Office Spaces Market size in 2025, thanks to hybrid seating policies, but freelancers are poised for the swiftest 12.65% CAGR out to 2031. Government platforms such as Qiwa simplify licensing and fee payment, encouraging professionals to swap payroll roles for project gigs. Operators now sell day passes, digital-only plans, and part-time bundles to match irregular usage patterns, an innovation critical for unlocking the next wave of penetration. The freelancer rise marks a cultural pivot toward self-employment that dovetails with Vision 2030’s job-creation narrative.

Start-ups remain a volatile but important slice, seeing occupancy ebb during the 2024 funding dip yet buoyed by USD 5 billion deal flow announced at Biban 24. Flexible interiors that switch swiftly from hot-desks to war-rooms help founders preserve cash while maintaining investor-ready professionalism. Enterprises, meanwhile, use satellite memberships to give remote staff secure drop-in options, cementing the full-stack appeal of the Saudi Arabia Coworking Office Spaces Market.

Geography Analysis

Riyadh held 58.70% of 2025 receipts and continues as the gravitational center for the Saudi Arabia Coworking Office Spaces Market. Flagship clusters in King Abdullah Financial District and Olaya benefit from proximity to regulators, sovereign funds, and regional HQs. EY’s state-of-the-art Riyadh Wavespace exemplifies how smart-building tech, wellness amenities, and hackathon zones merge in one lease, amplifying expectations for future supply. Tier-one operators layer community programming atop such infrastructure to capture sustained membership growth.

Jeddah serves as the Kingdom’s commercial gateway, with port, logistics, and tourism industries underpinning steady workspace needs. The USD 1.39 billion Jawharat Jeddah development brings co-working into a mall-office hybridity that is expected to lower member acquisition costs through shopper traffic synergies. Cultural fluidity and a high expatriate mix contribute to open-plan acceptance, while pilgrimage seasons create time-specific surges accommodated by flexible capacity algorithms.

The Dammam Metropolitan Area posts the fastest 13.02% CAGR forecast as logistics corridors with Bahrain deepen and energy diversification spawns supplier ecosystems. Women-only Dhahran facilities like Mustqr demonstrate receptiveness to thematic hubs beyond traditional business centers. Farther afield, Vision-related industrial parks in cities such as Hail start to seed demand, but limited operator presence and thinner talent pools temper expansion speed. Smart access control and remote concierge models could unlock these territories and expand the overall Saudi Arabia Coworking Office Spaces Market.

Competitive Landscape

The field is moderately fragmented, with international heavyweights WeWork’s new Saudi-backed offshoot and IWG’s Regus and Spaces brands anchoring premium supply in Riyadh and Jedda. Local specialists such as Mustqr build defensible moats by catering to cultural niches, including women-only lounges and Arabic-language mentoring. Developers increasingly choose management agreements with global brands for turn-key delivery, while others create proprietary labels to retain asset-level economics.

Technology is rising as the key differentiator. Operators deploy AI-based occupancy analytics, facial-recognition access, and blockchain-verified contracts to raise user confidence, especially among BFSI and legal tenants. Partner ecosystems with telecom and cloud providers enable bundled connectivity and cybersecurity, aligning with corporates’ hybrid mandates. Simultaneously, hospitality groups convert under-utilized hotel wings into subscription offices, injecting fresh competition into the Saudi Arabia Coworking Office Spaces Market.

White-space expansion hinges on cost-effective entry into secondary cities and free zones. Franchise-light models, revenue-share leases, and pop-up pods inside retail centers are under evaluation to sidestep high capital layouts. Operators possessing government connections and multilingual community teams possess an edge in navigating licensing and cultural integration, keeping the contest fluid yet disciplined.

Saudi Arabia Coworking Office Spaces Industry Leaders

Wework

Regus (IWG)

Servcorp

Spaces (IWG)

White Space

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: YOO and IWG unveil a global partnership to roll out club-style workplaces that fuse YOO’s design DNA with IWG’s flexible-platform playbook across five continents.

- September 2024: Adam Neumann launches a Saudi-funded “conscious community” real-estate start-up backed by over USD 1 billion from Affinity Partners.

- May 2024: Cenomi Centers confirms progress on the Jawharat Riyadh project, scheduled to open H2 2025 with integrated co-working floors and 300+ retail units.

- April 2024: Sahm Capital partners with Saudi Cloud Computing Company at LEAP 2024 to bolster digital financial services infrastructure that co-working tenants can tap.

Saudi Arabia Coworking Office Spaces Market Report Scope

Coworking is a business services provision model that involves individuals working independently or collaboratively in shared office spaces. This report offers a complete analysis of the Saudi Arabian Co-working Office Spaces Market, including a market overview, market size estimation for key segments and emerging trends by segments, and market dynamics. The report also offers the impact of COVID-19 on the market.

The Saudi Arabian Coworking Office Spaces Market is Segmented By End User (Personal User, Small Scale Company, Large Scale Company, and Other End Users), Type (Flexible Managed Office and Serviced Office), and Application (Information Technology (IT and ITES), Legal Services, BFSI (Banking, Financial Services, and Insurance), Consulting, and Other Services). The report offers market size and forecast for Saudi Arabia Co-working Office Spaces Market in value (USD billion) for all the above segments.

By Size & Scale of Facility

| Small |

| Medium |

| Large |

By Sector

| Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Service |

| Other Services (Retail, Lifesciences, Energy, Legal Services) |

By End Use

| Freelancers |

| Enterprises |

| Start Ups and Others |

By City

| Riyadh |

| Jeddah |

| DMA (Dammam metropolitan area) |

| Rest of Saudi Arabia |

| By Size & Scale of Facility | Small |

| Medium | |

| Large | |

| By Sector | Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Service | |

| Other Services (Retail, Lifesciences, Energy, Legal Services) | |

| By End Use | Freelancers |

| Enterprises | |

| Start Ups and Others | |

| By City | Riyadh |

| Jeddah | |

| DMA (Dammam metropolitan area) | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

How large is the Saudi Arabia Coworking Office Spaces Market in 2026?

The value stands at USD 0.67 billion and is on course toward USD 1.16 billion by 2031.

What is the expected growth rate for flexible workspace demand through 2031?

The market is forecast to advance at an 11.57% CAGR between 2026-2031 on the back of Vision 2030 reforms and hybrid work adoption.

Which city contributes the most revenue to co-working operators?

Riyadh leads with 58.70% share in 2025, thanks to its concentration of government entities and foreign regional headquarters.

Which end-user group is expected to surge the most?

Freelancers are estimated to grow at a 12.65% CAGR as digital platforms simplify independent contracting.

Page last updated on: