Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.06 Billion |

| Market Size (2026) | USD 16.43 Billion |

| Market Size (2031) | USD 18.43 Billion |

| Growth Rate (2026 - 2031) | 2.32% CAGR |

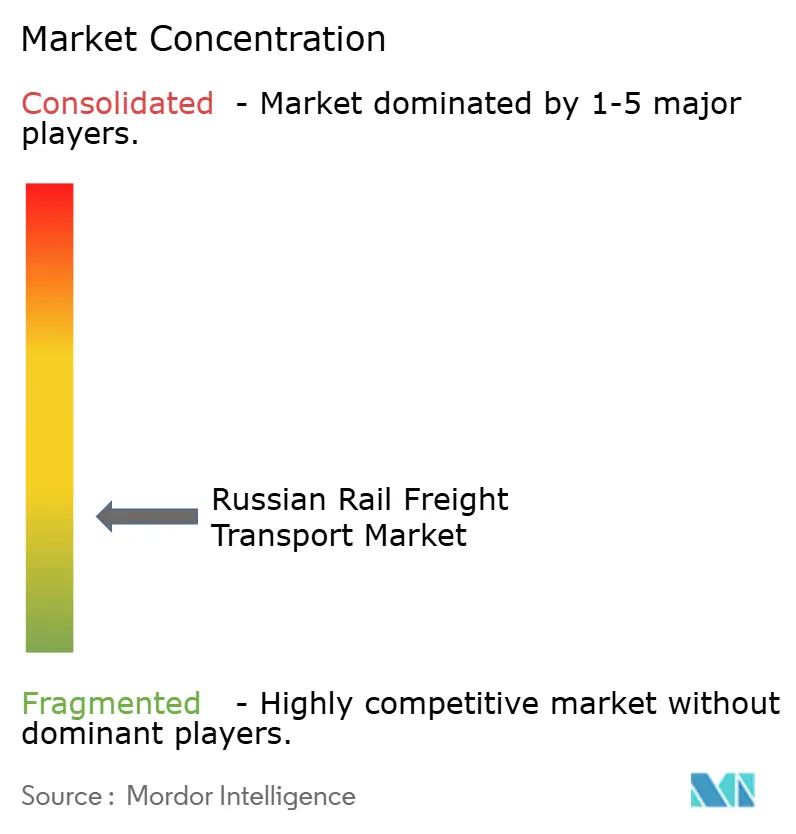

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Rail Freight Transport Market Analysis by Mordor Intelligence

Russia Rail Freight Transport Market size in 2026 is estimated at USD 16.43 billion, growing from 2025 value of USD 16.06 billion with 2031 projections showing USD 18.43 billion, growing at 2.32% CAGR over 2026-2031.

A decisive shift toward Asia-facing routes is reshaping traffic flows, even as Western sanctions squeeze access to modern locomotives and slow capacity gains. Heavy government investment amounting to 2.7 trillion rubles (USD 30.0 billion) is concentrated on the Trans-Siberian and Baikal-Amur corridors, underpinning long-haul bulk exports and providing a safety valve for rising container demand. Digital scheduling platforms are steadily reducing empty-run kilometers, signaling that data-driven reliability, not fleet size alone, will determine future competitive positioning. Bulk commodities still anchor revenues, yet faster growth in containerised and value-added services suggests the market is quietly diversifying its earnings base without abandoning its traditional strengths.

Key Report Takeaways

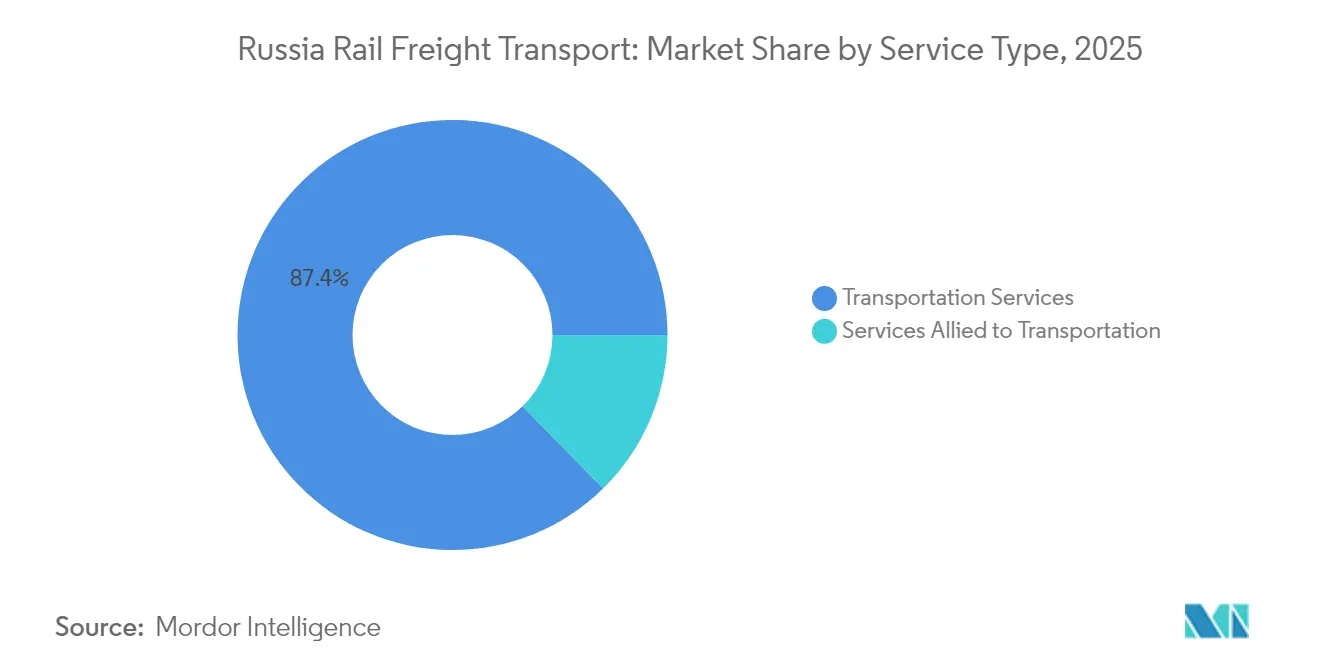

- By service type, Transportation captured 87.35 % of the Russia Rail Freight Transport market share in 2025, while the Russia Rail Freight Transport market size for Services Allied to Transportation is projected to grow at a 6.23 % CAGR through 2031.

- By cargo type, Dry Bulk accounted for 57.10 % of the Russia Rail Freight Transport market share in 2025, and the Russia Rail Freight Transport market size for Containerised/Intermodal services is forecast to expand at an 7.88 % CAGR to 2031.

- By end-user industry, Mining & Minerals held 35.45 % of the Russia Rail Freight Transport market share in 2025, whereas the Russia Rail Freight Transport market size tied to Retail & FMCG is expected to advance at a 9.18 % CAGR between 2026-2031.

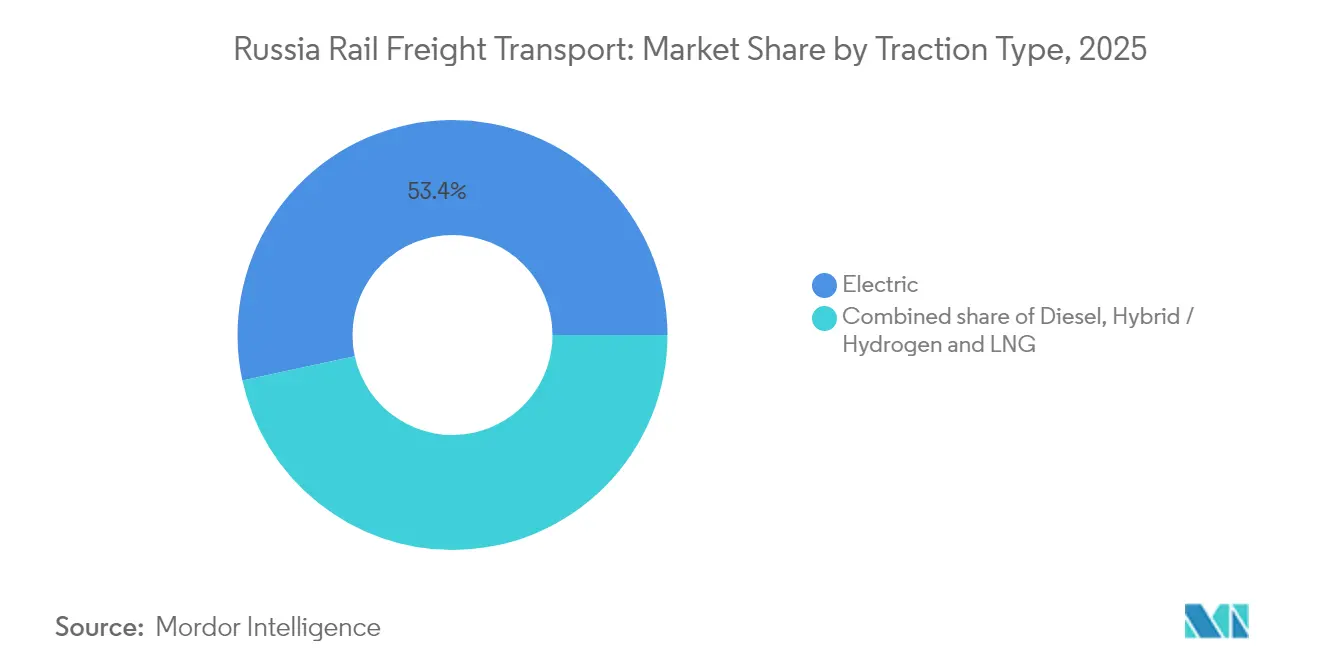

- By traction type, Electric locomotives commanded 53.40 % of the Russia Rail Freight Transport market share in 2025, and the Russia Rail Freight Transport market size derived from Hybrid/Hydrogen & LNG traction is anticipated to increase at a 9.86 % CAGR over the same period.

- By destination, Domestic movements dominated with a 89.25 % Russia Rail Freight Transport market share in 2025, while the Russia Rail Freight Transport market size for International/Cross-border flows is set to grow at a 6.82 % CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Rail Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on Market CAGR Forecast | Geographic Relevance | Timeline |

|---|---|---|---|

| Surge in Asia–Europe Transit Volumes via Russia | +0.80% | Trans-Siberian, Far East | Medium term (3-4 yrs) |

| Government Subsidies for Far-East Export Corridor | +0.70% | Eastern Siberia, Far East | Medium term (3-4 yrs) |

| Expansion of Northern Sea-Route Intermodal Hubs | +0.40% | Arctic Regions | Long term (≥ 5 yrs) |

| Digital Scheduling Platform Adoption | +0.30% | Nationwide | Short term (≤ 2 yrs) |

| Green transit shift from road to rail for bulk commodities | +0.20% | Nationwide mining belts | Long term (≥ 5 yrs) |

| Accelerated rolling-stock fleet modernisation programs | +0.30% | Depot clusters in Central & Far-East Russia | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Surge in Asia–Europe Transit Volumes via Russia

Rail traffic between Russia and China rose by 20 % in 2024, a jump attributed to shippers diverting cargo from disrupted maritime lanes. Transit times of 14-25 days on rail now compare favorably with longer ocean voyages, prompting freight forwarders to lock in multi-year block-train contracts. This demand spike spurs operators to lengthen trains and reserve wagon fleets, effectively deepening the rail corridor’s competitiveness even without large tariff reductions. Capacity pressures, however, highlight the need for additional passing tracks and digital slot allocation, a change that may funnel more investment into network optimization rather than pure track mileage.

Government Subsidies for Far-East Export Corridor

Moscow committed 366 billion rubles (USD 4.07 billion) for Trans-Siberian and Baikal-Amur upgrades in 2024 and plans further injections through 2032. Subsidized tariffs on east-bound export flows lower logistics costs for miners and grain traders, encouraging heavier train loads toward Pacific ports. Early evidence shows shorter queuing times at key yards, signaling that funds are easing operational choke points even before full project completion. A knock-on effect is that private wagon owners reposition assets eastward, subtly redistributing railcar availability across the wider network.

Expansion of Northern Sea-Route-linked Intermodal Hubs

Rail-to-sea interchanges in Arctic ports are under construction to connect the mainland grid with the Northern Sea Route, where ice-breakers extend the sailing season. Planned hubs aim to trim 30 %-50 % off Asia-to-Europe transit times once operational, giving exporters an incentive to bypass the Suez Canal. Even in pilot phase the scheme is steering container operators to test mixed rail-icebreaker service patterns that did not exist five years ago. The resulting freight data will likely influence future capacity planning decisions on both rail sidings and Arctic terminals.

Digital Scheduling Platform (RZD Digital Freight) Adoption

RZD’s Digital Freight platform brings real-time car tracking, automated slot booking, and dynamic pricing onto a single interface [1]Association “Digital Transport and Logistics,” “Digital Transformation of the Transport and Logistics Sector of the Russian Federation: Trends, Challenges, Solutions, Technologies,” dtla.ru . Early adopters report fewer empty-run kilometers, implying that asset turns, not sheer wagon counts, could become the primary utilisation metric. The state budget lines up 500 million rubles (USD 5.6 million) for wider rollout in 2025 tadviser.ru, underscoring official belief that software can unlock latent capacity faster than building new track. As more shippers migrate to electronic documents, customs clearance times are falling, reinforcing the competitive edge of digital-ready operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on Market CAGR Forecast | Geographic Relevance | Timeline |

|---|---|---|---|

| Western Sanctions Restricting Access to Advanced Locomotives | -0.60% | Network-wide, especially export routes | Medium term (3-4 yrs) |

| Congestion at China–Mongolia Border Crossings | -0.40% | Zabaikalsk–Manzhouli & related border posts | Short term (≤ 2 yrs) |

| Limited last-mile rail connectivity to Arctic ports | -0.30% | Northern Russia; Arctic hinterland | Long term (≥ 5 yrs) |

| Rising track-access tariffs for private operators | -0.30% | Nationwide, with sharper effect on secondary lines | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Western Sanctions Restricting Access to Advanced Locomotives

Sanctions cut off critical spare parts, leaving almost 50 000 trains delayed or suspended during 2024. The locomotive shortfall explains up to 93 % of the year’s loading decline, dwarfing other operational factors. In response, domestic manufacturers fast-track natural-gas locomotive lines, although ramp-up speed lags near-term demand curves. Until the new builds arrive, network planners must juggle tight power-unit allocations, often prioritizing higher-yield container flows over lower-margin bulk.

Congestion at China–Mongolia Border Crossings

Despite a 26 % traffic rise, the Zabaikalsk-Manzhouli checkpoint suffers recurrent queues tied to gauge changes and security checks. Automated inspection tools have cut document processing to five minutes in trial runs, yet physical siding limits still slow wagon turnover. Train planners increasingly schedule departures during off-peak cross-border windows, a workaround that improves punctuality but complicates domestic timetables. Investments in dual-gauge yards could smooth flow, though funding battles remain unresolved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Service Type: Transportation Dominates While Allied Services Gain Ground

Transportation services account for 87.35 % Russia Rail Freight Transport market share in 2025, reflecting the network’s core role in moving bulk and containerized goods over vast distances. Within this dominant slice, long-haul coal flows remain the single biggest revenue generator, but intermodal trainsets are gaining frequency on high-yield East-West corridors. Operators note that the new capacity funded for the eastern corridor is already pre-booked by coal, grain, and container customers, suggesting stable utilisation rates for the next investment cycle. An important nuance is that transport providers increasingly bundle guaranteed wagon availability with digital tracking, making service quality, not only price, the selling point.

Demand for wagon maintenance, storage, and switching rises as shippers diversify cargo types and routes, triggering a need for specialised yards and repair depots. RZD’s digital document workflow simplifies handoffs, which in turn raises customer expectations around 24/7 visibility and doorstep logistics. Consequently, allied-service providers invest in data analytics and cold-chain facilities, nudging the rail ecosystem toward full-stack logistics solutions.

Cargo Type: Bulk Commodities Reign While Containerization Accelerates

Dry bulk holds 57.10 % Russia Rail Freight Transport market share in 2025, underpinned by coal, ores, and grain exports that routinely travel 1,500 kilometers or more. The current wave of Asian demand encourages miners to sign multi-year contracts that stabilise wagon demand, reducing spot-rate volatility. Operators respond by deploying heavier axle-load wagons, extracting more ton-kilometers per locomotive under tight power-unit supply. Roughly half of new siding upgrades on the Baikal-Amur line now include bulk-friendly wagon tipplers, a subtle design choice that locks in future volume scalability.

Containerised and intermodal cargo grows fastest at an 7.88 % forecast CAGR, supported by new logistics hubs such as FESCO’s planned facility in Zabaikalsk valued at EUR 40 million (USD 44 million). Increasing e-commerce flows and just-in-time manufacturing imports from China accelerate the shift toward higher-value box traffic. Railcar pools are gradually adding 40-foot high-cube containers fitted for temperature-controlled goods, widening the appeal of rail for perishables. This segment’s expansion creates a buffer against commodity price swings, a diversification that benefits network cash-flow stability.

End-user Industry: Mining Leads While Retail Shows Strongest Growth

Mining and minerals command 35.45 % Russia Rail Freight Transport market share in 2025, mirroring the country’s resource-oriented economy. Haul lengths for ferrous metals exceed 1,900 kilometers, a distance that cements rail as the only economical mode for inland mine-to-port delivery. Producers that pivot cargo to Far-East ports now lock in slots two seasons ahead, indicating confidence in rail corridor reliability despite locomotive shortages. Network planners thus prioritise track-duplication projects near mining clusters to hedge against cyclical surges.

Retail and fast-moving consumer goods record the highest growth, forecast at 9.18 % CAGR through 2031. Online shopping boom and rising disposable income in secondary Russian cities generate new east-to-west backhaul opportunities for containers otherwise returning empty. Rail operators partner with fulfilment centres to create scheduled “e-commerce trains,” an initiative that improves wagon round-trip economics. The trend implies that consumer-driven traffic could one day offset part of the coal volume decline expected under decarbonisation scenarios.

Traction Type: Electric Dominance with Hydrogen Emerging as Game-Changer

Electric traction holds 53.40 % Russia Rail Freight Transport market size, due to a nationwide electrification share above 85 %. Electric locomotives anchor reliable, high-tonnage services, giving rail a cost and emissions edge on long hauls. Recent sub-station upgrades raise catenary capacity, enabling heavier trains without new rolling stock, a cost-effective productivity lever amid import restrictions. Operators also test energy-regeneration schemes where downhill braking feeds power back to the grid, an innovation that could shave operating costs further.

Hybrid, hydrogen, and LNG locomotives grow at 9.86 % forecast CAGR, albeit from a low base, stimulated by plans to convert 25 % of the fleet to natural gas by 2030. Pilot LNG routes already demonstrate 15-25 % fuel savings, a margin attractive to private wagon owners under tight rate environments. Hydrogen prototypes promise zero carbon tailpipe emissions, but comparable NOx levels to diesel keep regulators cautious. Nonetheless, the experimental units accumulate valuable performance data that will guide future fleet renewal cycles.

Destination: Domestic Market Prevails While Cross-border Shows Higher Growth

Domestic moves account for 89.25 % Russia Rail Freight Transport market share in 2025, a figure reflecting the country’s sheer landmass and inland resource deposits. Ongoing upgrades shorten average transit times between Western Siberia and Pacific ports, a reduction that helps domestic shippers compete in Asian coal tenders. As digital platforms standardise documentation, small and mid-sized Russian firms find domestic rail more accessible, broadening the user base beyond large conglomerates. This wider adoption helps smooth volume seasonality, particularly during agricultural peak seasons.

Cross-border freight of the Russian Rail Freight Transport industry is set to grow at 6.82 % CAGR to 2031. New Sino-Russian cooperation agreements streamline customs, while investments in the North-South Transport Corridor open access to Iran and India. Train services increasingly use unified tracking numbers valid across three countries, reducing administrative friction and boosting schedule reliability. Greater certainty, in turn, invites third-country forwarders to channel Europe-bound cargo through Russian land routes, diversifying customer portfolios for domestic operators.

Competitive Landscape

Russian Railways (RZD) owns the track infrastructure and sets access terms, giving it pivotal influence over the Russia Rail Freight Transport industry structure. Private operators such as Freight One, TransContainer, Globaltrans, and Federal Freight Company focus on wagon fleets and niche services, collectively controlling 88 % of market railcars [2]Globaltrans Investment PLC, “Our Markets,” globaltrans.com. Competitive advantage increasingly hinges on the ability to bundle rolling stock with digital scheduling, creating a service moat that is not easily replicated by late adopters.

Strategic alliances are reshaping value chains, illustrated by SIBUR and SG-trans forming a joint venture for LPG transport worth 9.4 billion rubles (USD 104.4 million) [3]SIBUR & SG-Trans, “SIBUR and SG-Trans Set Up a JV for Petrochemicals Transportation,” gulfoilandgas.com. Such vertical moves lock in captive cargo flows, reducing exposure to spot-market volatility and guaranteeing asset utilisation. Similar partnerships appear in refrigerated container pools targeting agricultural exports, indicating that product-specific rail solutions are gaining traction. These vertical plays subtly fragment market share, as integrated logistics groups capture portions previously serviced by general-purpose wagon operators.

Technology acts as a new battleground, with RZD rolling out artificial neural-network mass-measuring systems that remove the need for precise wheel positioning. Early adopters gain faster weighbridge throughput, reinforcing punctuality commitments to shippers. Meanwhile, smaller operators test blockchain-based asset-sharing platforms to maximise idle wagon days. As technology lowers entry barriers for service innovation, competitive dynamics may tilt toward agile firms that marry specialized hardware with flexible software, rather than scale alone.

Russia Rail Freight Transport Industry Leaders

Russian Railways (RZD)

TransContainer

Freight One (PGK)

Globaltrans Investment PLC

Federal Freight Company (FFC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: FESCO and Xi’an Free Trade Port agreed to build a EUR 40 million (USD 44 million) logistics and transportation centre in Zabaikalsk. The project targets a 26 % capacity increase at the border crossing and adds dedicated staging yards for refrigerated containers.

- May 2024: Russian Railways and China Railway signed a strategic cooperation pact focusing on new border infrastructure and a second track between Zabaikalsk and Manzhouli. The accord aims to ease congestion and boost bilateral freight slots.

- May 2024: Russian Railways (RZD) signed a comprehensive strategic cooperation agreement with China Railway during President Putin's visit to China, focusing on developing international transport corridors under China's Belt & Road initiative, enhancing border crossings, and constructing a second track between Zabaikalsk and Manzhouli Railway Gazette International.

- March 2024: Russian Railways (RZD) announced a massive infrastructure investment program with government backing of 366 billion rubles (USD 4 billion) for 2024 to upgrade the Trans-Siberian and Baikal-Amur Mainline railroads, with total planned investments of 2.7 trillion rubles (USD 30 billion) by 2032 to increase shipping capacity from 150.5 million tons to 255 million tons annually.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Russian rail freight transport market as the annual value earned from moving domestic and cross-border cargo over Russia's public railway network, together with allied switching, storage, and wagon maintenance services that rail operators invoice in rubles and are converted to U.S. dollars at prevailing yearly averages.

Passenger rail, pipeline flows, and revenues from private in-plant rail spurs are not counted.

Segmentation Overview

- By Service Type

- Transportation

- Services Allied to Transportation (Maintenance, Switching, Storage)

- By Cargo Type

- Containerised / Intermodal

- Dry Bulk (Coal, Ores, Grains)

- Liquid Bulk (Crude, Chemicals)

- Break-bulk & Project Cargo

- By End-user Industry

- Mining & Minerals

- Oil, Gas & Chemicals

- Agriculture & Food

- Manufacturing & Automotive

- Retail & FMCG

- Construction Materials & Others

- By Traction Type

- Diesel

- Electric

- Hybrid / Hydrogen & LNG

- By Destination

- Domestic

- International / Cross-border

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held interviews and pulse surveys with rolling-stock lessors, bulk commodity shippers across Siberia and the Northwest, third-party logistics planners, and metro-Moscow freight forwarders. These conversations clarified actual rate movements, traction-type cost differentials, and eastbound volume re-routing expectations that secondary sources alone could not quantify.

Desk Research

We began with trade and government datasets, such as Federal State Statistics Service ton-kilometer tables, Eurasian Economic Union customs summaries, and Ministry of Transport corridor investment updates, which outline cargo mix, tariff brackets, and corridor capacity shifts. Complementary context came from Russian Railways annual reports, Central Bank exchange bulletins, industry association notes (e.g. Union of Railwaymen), and reputable media captured through Dow Jones Factiva. According to Mordor Intelligence paid dashboards, historical wagon fleet inventories and average service prices were retrieved from D&B Hoovers and IMTMA where relevant. This list is illustrative; many other open and subscription sources were reviewed to confirm trends and fill data gaps.

Market-Sizing & Forecasting

A top-down build anchored on 2024 freight revenue declared by Russian Railways and major private operators was adjusted for captive traffic and re-expressed in USD. Results were cross-checked with a bottom-up sample of average service price multiplied by loaded wagon-days drawn from operator disclosures. Key model drivers include commodity export indices, wagon turnaround times, corridor utilization on the Trans-Siberian and BAM lines, average ruble-USD exchange, infrastructure CAPEX, and sanctioned trade re-direction toward Asia. Multivariate regression against these variables underpins the 2025-2030 forecast, while scenario analysis captures upside from accelerated eastern capacity expansion.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scanning, analyst peer audit, and sector lead sign-off. We refresh every twelve months, and interim updates are triggered when tariff revisions, sanction rounds, or large capital injections materially change any core driver.

Why Mordor's Russian Rail Freight Transport Baseline Warrants Trust

Published estimates often diverge because firms pick different service baskets, currency treatments, and refresh cadences.

Key gap drivers in this market are whether allied services are counted, the exchange rate year applied, and if captive in-house rail at mining sites is added or removed before reporting. Some providers roll logistics mark-ups into freight value, while others freeze the ruble at a fixed parity, and Mordor reports strictly rail-earned revenue, updates the FX each cycle, and disaggregates captive haulage.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.06 B (2025) | Mordor Intelligence | - |

| USD 71 B (2024) | Global Consultancy A | Includes wider logistics fees and uses blended 2023 FX |

| USD 16 B (2025) | Sector Analyst B | Counts some private in-plant rail and applies broader cargo coverage |

Taken together, the comparison shows that Mordor's disciplined scope selection, currency handling, and yearly source refresh give decision-makers a balanced, transparent baseline that is traceable to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the current Russia Rail Freight Transport market size?

The market is valued at USD 16.43 billion in 2026.

How fast is the Russia Rail Freight Transport industry expected to grow?

It is forecast to expand at a CAGR of 2.32 % between 2026 and 2031.

Which cargo type dominates the Russia Rail Freight Transport market share?

Dry bulk commodities, led by coal, ores, and grains, account for 57.10% of total volumes.

Why are eastern corridors a focus for investment?

They connect Russian exporters to rising Asian demand and relieve pressure from western sanction-affected routes.

How important is digitalisation to future rail competitiveness in Russia?

Digital scheduling and tracking platforms reduce empty runs and speed customs clearance, making them central to capacity and service quality gains.

What environmental advantage does Russian rail offer over road transport?

With 53.40 % electric traction, rail emits significantly fewer greenhouse gases on long hauls than diesel trucking, aligning with carbon-reduction goals.

Page last updated on: