Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.06 Billion |

| Market Size (2026) | USD 9.29 Billion |

| Market Size (2031) | USD 10.52 Billion |

| Growth Rate (2026 - 2031) | 2.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slovakia Freight And Logistics Market Analysis by Mordor Intelligence

The Slovakia freight and logistics market size is expected to grow from USD 9.06 billion in 2025 to USD 9.29 billion in 2026 and is forecast to reach USD 10.52 billion by 2031 at 2.52% CAGR over 2026-2031. This growth is anchored in the country’s location at the crossroads of nine Trans-European Transport Network (TEN-T) corridors, consistent infrastructure spending, and a robust manufacturing base that keeps transport demand steady even when regional consumer sentiment softens. Digital adoption, especially in warehouse automation and fleet telematics, continues to lift productivity, while EU Green Deal incentives nudge shippers toward rail and inland-waterway alternatives. Consolidation among global third-party logistics (3PL) providers is raising competitive intensity, yet the prevalence of small and medium-sized domestic operators preserves a degree of market fragmentation. Together, these forces sustain the Slovakia freight and logistics market as a resilient, moderately expanding linchpin for Central European trade[1]“TEN-T Transport Infrastructure,” European Commission, transport.ec.europa.eu.

Key Report Takeaways

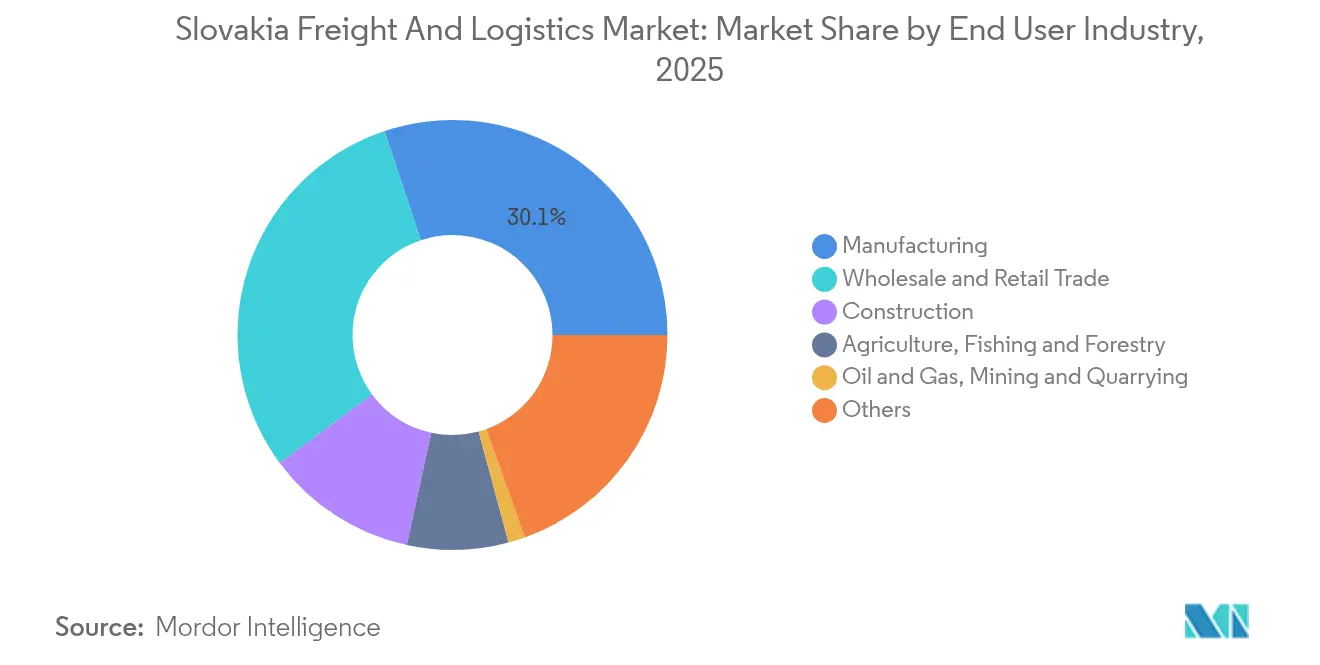

- By end user industry, manufacturing held 30.12% of the Slovakia freight and logistics market share in 2025, whereas wholesale and retail trade is expected to advance at a 2.66% CAGR between 2026-2031.

- By logistics function, freight transport led with 53.05% of the Slovakia freight and logistics market size in 2025, while courier, express, and parcel (CEP) services are expected to rise the fastest at a 2.96% CAGR between 2026-2031.

- By CEP type, domestic deliveries commanded 65.80% of the revenue share in 2025; international services show quicker anticipated momentum at a 2.98% CAGR between 2026-2031.

- By freight-forwarding mode, sea and inland waterways freight forwarding controlled 37.10% of the revenue share in 2025, and air freight forwarding is on track for a 5.74% CAGR between 2026-2031.

- By freight-transport mode, road freight transport accounted for 81.05% of the revenue share in 2025, whereas air freight transport is expected to record the strongest 5.18% CAGR between 2026-2031.

- By warehousing and storage, non-temperature controlled space captured 91.80% of the revenue share in 2025, but temperature-controlled capacity is expected to expand at a 2.41% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovakia Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitalization and supply‑chain integration driving network efficiency gains | +0.8% | National; concentrated in Bratislava and Kosice regions | Medium term (2-4 years) |

| Infrastructure upgrades advance along core TEN‑T transport corridors | +0.6% | Nationwide focus on Baltic-Adriatic and Orient/East-Med corridors | Long term (≥ 4 years) |

| Cross‑border trade facilitation strengthens Slovakia’s regional connectivity | +0.4% | EU border crossings, especially Bratislava–Vienna and Kosice–Budapest axes | Short term (≤ 2 years) |

| Automotive export cluster expansion sustains manufacturing trade volumes | +0.3% | Regional clusters in Trnava, Zilina, and Nitra | Medium term (2-4 years) |

| EU battery supply‑chain localization boosts industrial investment prospects | +0.2% | Lower Nitra and Trnava regions | Long term (≥ 4 years) |

| Rail‑freight incentives under EU Green Deal support modal shift | +0.2% | National; key cross-border rail corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digitalization and Supply-Chain Integration

Slovak logistics operators are accelerating the deployment of 5G, cloud, and artificial-intelligence tools promoted under the Digital Slovakia 2030 roadmap, which earmarks EUR 2.3 billion (USD 2.5 billion) for digital adoption incentives[2]“Digital Slovakia 2030,” Ministry of Investments, Regional Development and Informatization, mirri.gov.sk. Real-time visibility platforms enable predictive arrival times and proactive delay alerts, trimming idle fleets and cutting empty backhauls. Local technology supplier Twinzo reports that its smartphone-based digital-twin application reduced client vehicle use by 20% and lifted logistics efficiency by 45% in pilot deployments. E-invoicing and automated customs-documentation flows lower administrative overhead for small shippers that previously struggled with paper-heavy compliance. As these solutions proliferate, they collectively widen operating margins and raise service-quality expectations across the Slovakia freight and logistics market.

Infrastructure Upgrades Along TEN-T Corridors

Brussels approved EUR 7 billion (USD 7.7 billion) for Slovak transport projects under the Connecting Europe Facility, allocating four-fifths to rail over the next decade. Upgrades to the Poprad-Tatry–Vydrnik segment will double top speeds to 160 km/h and integrate European Rail Traffic Management System signaling. The Nove Mesto nad Váhom–Puchov modernization, already at 85% train-length compliance, is removing infrastructure bottlenecks on the Baltic-Adriatic corridor. These improvements shorten door-to-door lead times and bolster rail’s reliability, encouraging shippers to shift long-haul volume from road to more sustainable modes within the Slovakia freight and logistics market.

Cross-Border Trade Facilitation

Membership in the EU’s single market and Schengen Area removes physical customs checks on most intra-EU consignments, allowing trucks to clear borders such as Bratislava–Vienna or Kosice–Budapest in minutes rather than hours. Adoption of the European Electronic Toll Service unifies payments across member states, cutting administrative complexity for international haulers. Rail Freight Corridor 5 coordination time-sensitive slots to intermodal trains linking the Baltic Sea with Adriatic ports, reducing schedule variance for automotive exporters. Together, these measures enhance Slovakia’s appeal as a pivot for east-west European cargo flows, reinforcing volume growth in the Slovakia freight and logistics market.

Automotive Export Cluster Expansion

Slovakia assembled 1.05 million vehicles in 2024 and targets 1.2 million units by 2026, powered by Volvo’s forthcoming electric-vehicle plant in Valaliky and capacity additions at Stellantis, Kia, and Volkswagen sites. Automotive manufacturing contributes 49.5% of industrial sales and 9.5% of GDP, translating into dense inbound parts and outbound finished-vehicle flows that sustain warehouse demand around Trnava, Zilina, and Nitra. New battery investments worth EUR 1.2 billion (USD 1.3 billion) by Gotion-InoBat will add 1,311 jobs and elevate specialized transport needs for lithium-ion modules, thermal-control packaging, and hazardous-goods compliance[3]“Battery Production Investment,” Ministry of Economy of the Slovak Republic, mhsr.sk. As the electric-vehicle transition gathers pace, it anchors sustained freight volumes and value-added logistics services within the Slovakia freight and logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating costs intensify price pressure across logistics sector | -0.4% | National; most acute in Bratislava and Kosice metropolitan areas | Short term (≤ 2 years) |

| Driver shortage and ageing workforce challenge transport capacity growth | -0.3% | Nationwide; road-freight carriers most exposed | Medium term (2-4 years) |

| Warehouse vacancy tightens further in Bratislava distribution hotspot | -0.2% | Bratislava metropolitan area | Short term (≤ 2 years) |

| Danube low‑water levels disrupt inland shipping reliability and flows | -0.1% | Bratislava port and wider inland-waterway network | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operating Costs and Price Pressure

Fuel volatility, index-linked highway tolls, and rising warehouse-lease rates are eroding margins, especially for small fleets that lack purchasing leverage. Labor costs climbed alongside Slovakia’s tight employment market, placing wage inflation among the top competitiveness threats cited by the automotive association. Compliance spending also mounts as EU emissions regulations push carriers to modernize fleets or face surcharges. While regional 3PLs counterbalance with digital route optimization and shared-asset models, the overall effect trims profitability and tempers near-term expansion plans within the Slovakia freight and logistics market.

Driver Shortage and Aging Workforce

Road operators report vacancy rates that exceed 10% for heavy-vehicle drivers, aggravated by demographic aging and limited inflows of licensed young recruits. Regulations that cap weekly driving hours force carriers to add headcount or redesign networks, inflating cost structures. Vocational-training reforms introduced an Autotronic curriculum to prepare mechanics and drivers for electric-powertrain maintenance, yet uptake remains gradual. Until workforce gaps narrow, service reliability risks persist and could restrain long-run growth in the Slovakia freight and logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Leadership with Retail Trade Momentum

Manufacturing generated 30.12% of the Slovakia freight and logistics market in 2025, underpinned by automotive production exceeding 1 million units and robust demand for just-in-time parts supply. Freight flows for engine blocks, wiring harnesses, and stamped body panels sustain continuous trucking lanes between plant clusters and cross-dock sites. The segment benefits from EU incentives that localize battery output, prompting investments in specialized storage for lithium-ion cells and compliant hazmat transport services. Evolving supply-chain models, such as vendor-managed inventory, further tighten collaboration between OEMs and 3PL providers, reinforcing contract-logistics volumes in the Slovakia freight and logistics market.

Wholesale and retail trade is expected to grow at a 2.66% CAGR between 2026-2031 as e-commerce penetration climbs toward 85% of internet users. National retailers expand omnichannel fulfillment centers around Bratislava to enable same-day delivery, while cross-border merchants exploit Slovakia’s centrality for regional order consolidation. Apparel and grocery categories dominate parcel volumes, driving demand for automated sortation hubs and temperature-controlled last-mile vans. The two end-user groups together anchor more than half of all transport invoices issued within the Slovakia freight and logistics market.

By Logistics Function: Freight Transport Dominates Amid CEP Acceleration

Freight transport captured 53.05% of 2025 revenue, reflecting the continued prevalence of contract trucking and bulk rail moves that feed Slovakia’s export-oriented factories. Average road-haulage rates hovered around USD 0.121 per ton-km, while competitive rail tariffs near USD 0.046 per ton-km attracted more steel and lumber consignments. Carriers with integrated fleet-management telematics improved asset utilization, curbing empty backhaul kilometers and supporting profitability across the Slovakia freight and logistics market.

CEP services, though smaller in absolute value, are expected to log the fastest 2.96% CAGR (2026-2031) as parcel counts swell. Pick-up-drop-off networks exceeding 2,000 lockers shorten last-mile distances and widen rural reach. Fleet electrification pilots in Bratislava show promise, with lower operating costs offsetting higher vehicle purchase prices. Cross-border B2C volumes benefit from harmonized EU VAT thresholds, stimulating Slovak e-shops to ship seamlessly into neighboring Austria and the Czech Republic. This momentum ensures that CEP remains the standout growth engine among logistics functions in the Slovakia freight and logistics market.

By Courier, Express, and Parcel (CEP): Domestic Dominance with International Growth

Domestic parcels commanded 65.80% of the segment share in 2025, thanks to the country’s compact 49,035 km² territory that enables next-day delivery nationwide. Retailers leverage centralized Bratislava warehouses to reach 80% of households within 24 hours, supporting customer-experience benchmarks competitive with larger EU peers. Reverse-logistics lanes, particularly for fashion returns, now account for nearly one in five domestic parcel journeys, amplifying network density.

International CEP consignments are projected to grow at a matching 2.98% CAGR (2026-2031), spurred by EU single-market rules that strip away customs paperwork for most intra-community goods. Packeta’s cross-border relay points and consolidated line-hauls to Prague, Vienna, and Budapest cut per-parcel costs and open fresh sales channels for Slovak SMEs. With cross-border e-commerce trending upward, international parcel services are expected to erode domestic share incrementally, though domestic will still dominate overall volumes within the Slovakia freight and logistics market.

By Warehousing and Storage: Non-Temperature Controlled Dominance

Non-temperature-controlled facilities comprise 91.80% of the revenue share in 2025, catering to automotive skids, electronics, and general merchandise that require only ambient conditions. Developers clustered around D1 motorway interchanges introduce cross-dock formats with 40,000 pallet positions and mezzanine e-fulfillment zones, keeping vacancy under 3% in prime Bratislava parks.

Temperature-controlled space, although niche, is expected to grow at a 2.41% CAGR (2026-2031) as pharmaceutical wholesalers and grocery chains standardize GDP-compliant cold chain operations. Energy-efficient CO₂ refrigeration systems cut utility consumption by 15%, offsetting elevated capital expenditure. Warehouse operators deploy real-time thermal monitoring and IoT sensors to avert spoilage, elevating service quality in this emerging slice of the Slovakia freight and logistics market.

By Freight Transport: Road Freight Transport Dominance with Modal Shift Potential

Road freight transport handled 81.05% of freight transport revenue in 2025, favored for its flexibility and dense motorway grid that connects OEM campuses with Tier-1 suppliers in under three hours. Telematics upgrades delivered 8% fuel-efficiency gains, and eco-driving programs cut emissions in line with EU Fit-for-55 targets. Meanwhile, the rail share is poised to grow as ERTMS deployment lifts average speeds and track-access charges remain competitive, supporting the Slovakia freight and logistics market.

Air freight transport is expected to record a 5.18% CAGR (2026-2031), reflecting an uptick in time-critical shipments and express e-commerce parcels routed through Vienna and Budapest hubs. Waterway and pipeline modes maintain small but stable shares, constrained by seasonal Danube variability and mature petrochemical trade routes, respectively. Policymakers aim to nudge 5 percentage points of road volume toward rail and river by 2030, enhancing sustainability credentials for the Slovakia freight and logistics market.

By Freight Forwarding: Multimodal Integration Drives Efficiency

Sea and inland-waterway freight forwarding represented 37.10% of forwarding revenue in 2025, leveraging the Danube’s link to Black-Sea transshipment hubs for bulk steel, grain, and containerized consumer goods. Though low-water periods occasionally disrupt throughput, freight forwarders mitigate risk by integrating rail legs that bypass impassable stretches, preserving service reliability in the Slovakia freight and logistics market.

Air freight forwarding posts the highest projected 5.74% CAGR (2026-2031) as automotive electronics and high-value spare parts require 24- to 48-hour delivery into Western European assembly lines. Bratislava Airport’s freighter gate capacity expanded 40% in 2024 after Hellmann Worldwide Logistics inaugurated its dedicated cross-dock operation. Forwarders increasingly bundle air and road services with customs brokerage to present single-invoice solutions, strengthening customer retention in Slovakia’s competitive forwarding arena.

Geography Analysis

Bratislava dominates logistics value creation, benefiting from the convergence of D2, D4, and D1 motorways and proximity to Vienna International Airport. The region’s GDP per capita exceeds the EU average, translating into premium land rents and the country’s tightest warehouse vacancy below 2%. Multinationals establish regional control towers here, coordinating Central European distribution out of high-bay facilities with automated picking systems.

Kosice functions as the eastern gateway, anchoring the Rail Freight Corridor 5 links to Hungary and Ukraine. Volvo’s green-field electric-vehicle plant in nearby Valaliky is expected to pivot inbound logistics toward component flows from Scandinavia and Germany, diversifying traditional west-bound traffic. Government incentives, including corporate-tax relief and training grants, aim to balance Slovakia’s historically west-skewed economic map.

The Nitra and Zilina regions reinforce the country’s automotive triangle, housing Stellantis and Kia plants that depend on synchronized part deliveries. EU co-financed rail upgrades shorten transit to North Adriatic ports, helping exporters avoid congested Northern range terminals. As these regional nodes mature, they collectively cement Slovakia’s reputation as Central Europe’s nimble, multimodal gateway, sustaining volume expansion for the Slovakia freight and logistics market.

Competitive Landscape

The market remains moderately fragmented despite headline-grabbing mergers. DSV’s EUR 14.3 billion (USD 15.8 billion) acquisition of Schenker elevates its revenue base to EUR 41.6 billion (USD 45.9 billion) and grants deeper penetration into automotive and technology verticals. DHL renewed its five-year integrated-logistics mandate with Volkswagen Slovakia, underscoring the strategic importance of long-term contracts in safeguarding throughput.

Regional 3PLs such as Raben Group and Gebrüder Weiss counterbalance scale disadvantages through specialized services and sustainable-fleet rollouts. Eurowag’s digital-payment platform reinforces small-fleet competitiveness by bundling fuel, tolling, and VAT-reclaim services into one account. Technology adoption thus emerges as the central competitive variable, with providers integrating IoT sensors, warehouse robotics, and predictive analytics to secure contracts in the Slovakia freight and logistics market.

Sustainability metrics increasingly influence tender awards. Kuehne+Nagel’s new Trnava distribution center features rooftop photovoltaics and LED lighting that cut energy use by 35%. Rhenus leverages its Nitra contract-logistics campus to pilot electric forklifts and paper-free inventory systems . These moves, along with continuous consolidation, suggest a moderate yet intensifying competitive environment across the Slovakia freight and logistics market.

Slovakia Freight And Logistics Industry Leaders

DHL Group

Kuehne+Nagel

DSV A/S (Including DB Schenker)

Raben Group

CMA CGM Group (Including CEVA Logistics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MAN Truck & Bus announced a contract to deliver 1,200 TGX tractors to Gartner KG by 2028, outfitted with advanced driver-assistance systems.

- April 2025: DSV finalized the EUR 14.3 billion (USD 15.8 billion) purchase of Schenker, unlocking expected annual benefits of DKK 9 billion (USD 1.3 billion) by 2028.

- December 2024: Hellmann Worldwide Logistics reported 9% YoY revenue growth to EUR 3.8 billion (USD 4.2 billion), supported by the acquisition of PKZ Group in Slovakia and the Czech Republic.

- September 2024: DHL Supply Chain extended its integrated-logistics partnership with Volkswagen Slovakia for an additional five years.

Slovakia Freight And Logistics Market Report Scope

Freight logistics is the overseeing and management of a cost-effective operation and the delivery of goods. It combines logistics experience, human resources, and knowledge to ensure the smooth journey of goods between carriers and shippers.

A complete background analysis of the Slovakia freight and logistics market, which includes an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and logistics spending by the end-user industries and the impact of COVID - 19 on the market are covered in the report.

The Slovakia Freight and Logistics Market segmented by Function (Freight Transport, Freight Forwarding, Warehousing, and Value-added Services and Other Services) and End User (Manufacturing and Automotive, Oil and Gas, Mining, and Quarrying, Agriculture, Fishing, and Forestry, Construction, Distributive Trade, Healthcare and Pharmaceutical, and Other End Users). The report offers market size and forecast for the Slovakia Freight and Logistics Market in value (USD billion) for all the above segments.

End User Industry

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

Logistics Function

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Pipelines | ||

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | ||

| Other Services | ||

| End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

| Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Pipelines | |||

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled | |

| Temperature Controlled | |||

| Other Services | |||

Key Questions Answered in the Report

How large is the Slovakia freight and logistics market in 2026?

It is valued at USD 9.29 billion, with a forecast 2.52% CAGR (2026-2031) to reach USD 10.52 billion by 2031.

Which end-user sector drives the most logistics demand in Slovakia?

Manufacturing, led by automotive production, accounts for 30.12% of 2025 logistics spending.

What is the fastest-growing logistics function in the country?

Courier, express, and parcel services are expected to grow at a 2.96% CAGR between 2026-2031 due to e-commerce growth.

How dominant is road freight transport in Slovak freight movements?

Road freight transport carries 81.05% share, although policy initiatives aim to shift part of this volume to rail and waterways.

Which region hosts the tightest warehouse market?

The Bratislava region posts vacancy below 2% owing to concentrated demand and limited land availability.

What role do EU infrastructure funds play in Slovakia’s logistics outlook?

EUR 7 billion (USD 7.7 billion) of Connecting Europe Facility grants, mainly for rail, are modernizing corridors and improving cross-border connectivity.

Page last updated on: