Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

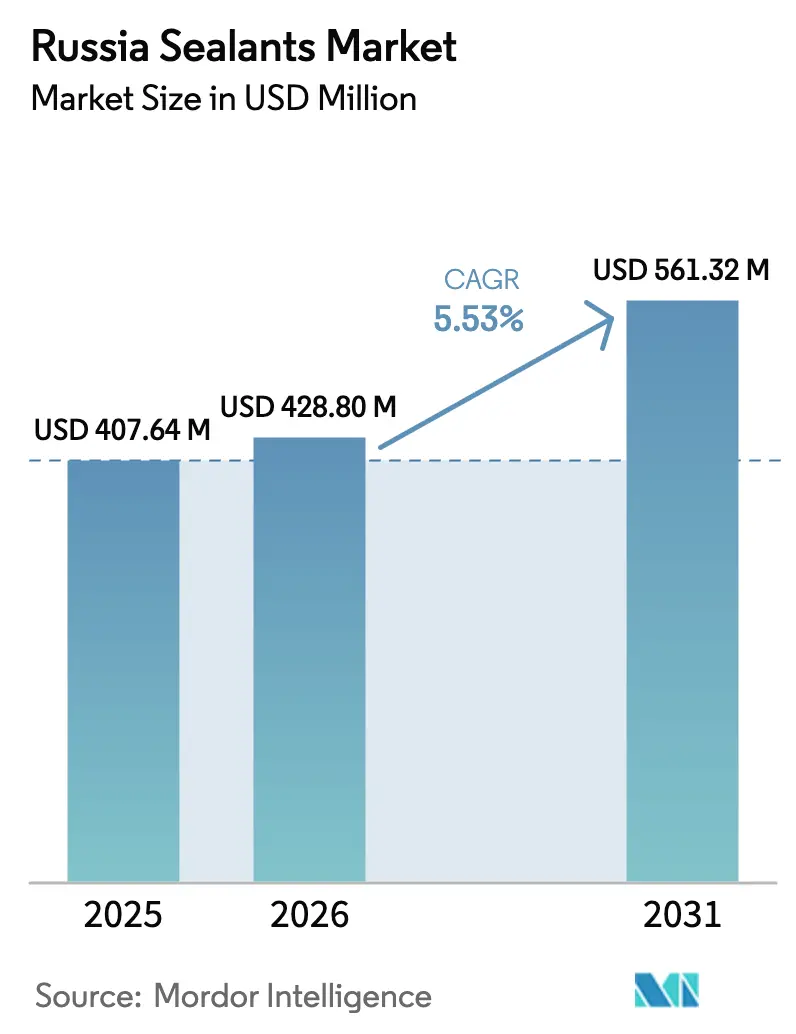

| Base Year Market Size (2025) | USD 407.64 Million |

| Market Size (2026) | USD 428.80 Million |

| Market Size (2031) | USD 561.32 Million |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Sealants Market Analysis by Mordor Intelligence

The Russia Sealants Market size was valued at USD 407.64 million in 2025 and is estimated to grow from USD 428.80 million in 2026 to reach USD 561.32 million by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). State-backed rail and highway corridors, a 42% jump in Moscow residential floor area launched in January 2026, and a 50% rise in February 2026 underpin solid volume growth, while labor shortages and a 25% ruble slide since mid-2024 keep cost pressures elevated. Silicone-based grades serve 219 skyscrapers scheduled for completion between 2025 and 2027, while polyurethane grades rated for -60°C to +70°C enjoy above-average demand from Arctic LNG 2 and similar cold-climate energy projects. On the supply side, Henkel, Sika, Dow, and Wacker Chemie rely on imports for 70-80% of silicone monomers, yet Ambrella Silicon and SIBUR are localizing intermediates that could narrow the currency exposure for domestic formulators by the end of 2027. Mergers such as Sika’s February 2026 purchase of Akkim add regional capacity that can be routed into Russia through Turkey and Kazakhstan, creating fresh competition for incumbent domestic brands.

Key Report Takeaways

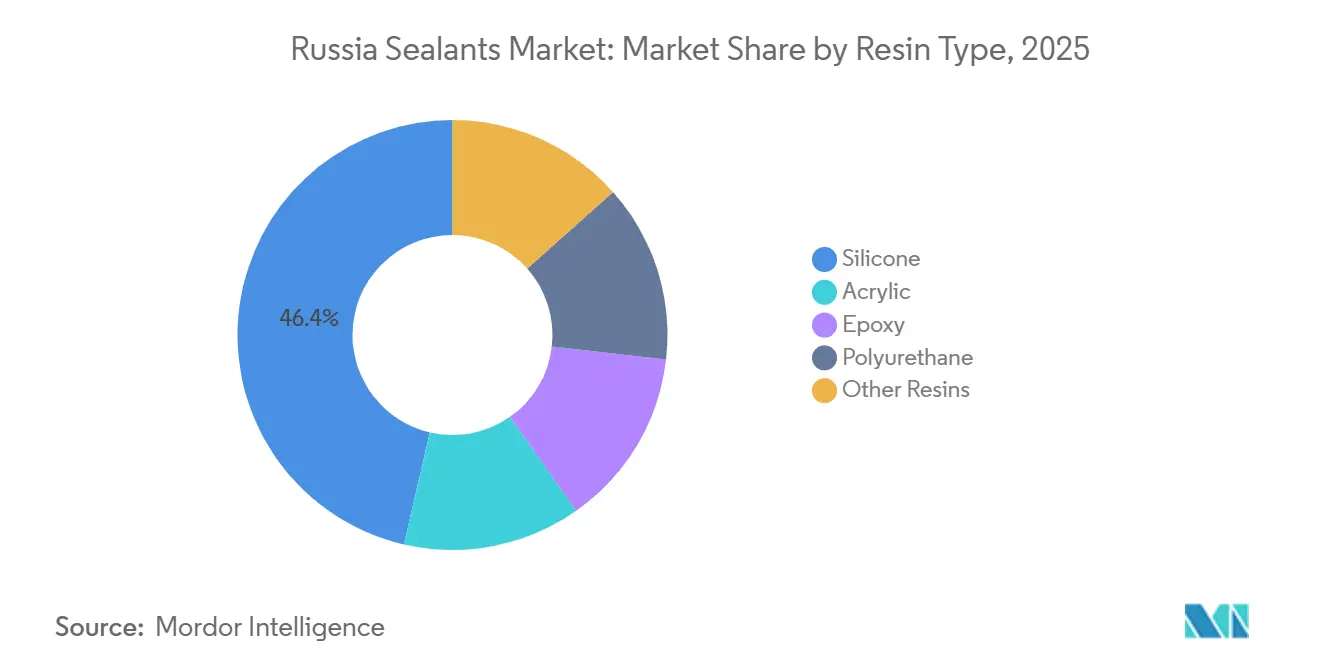

- By resin type, silicone had the largest share of 46.36% in 2025, and polyurethane's share is expected to increase with a CAGR of 6.45% during the forecast period (2026-2031).

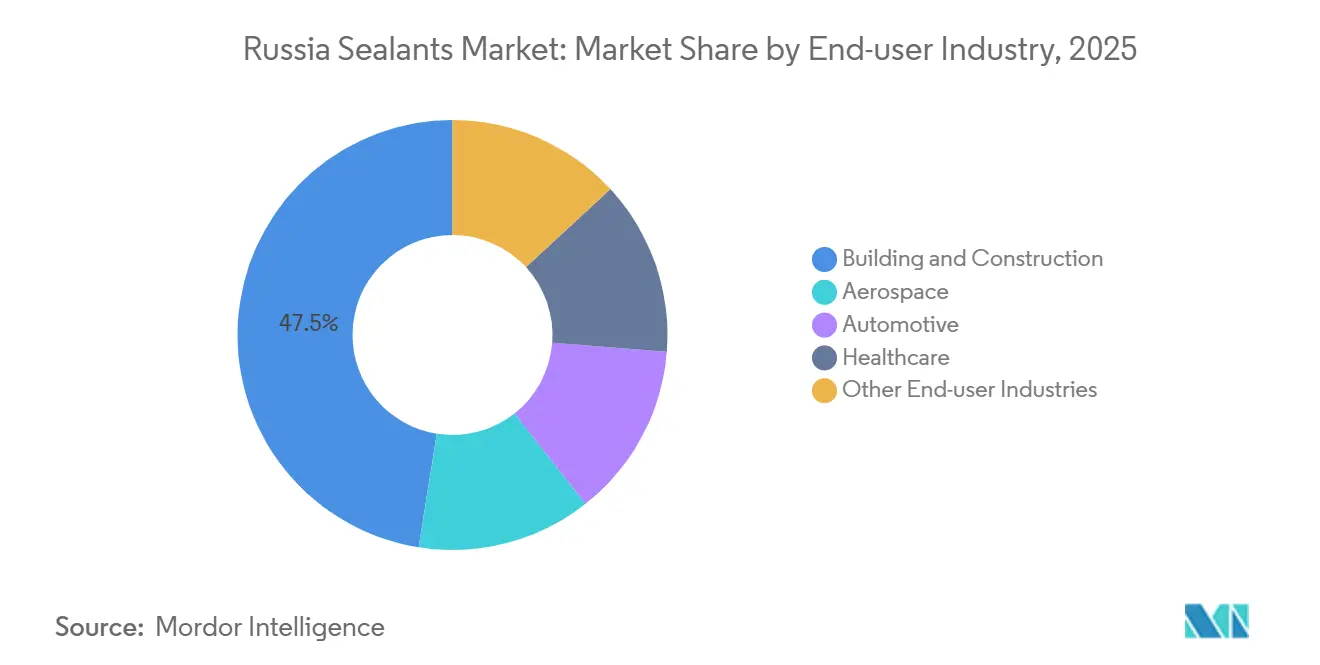

- By end-user industry, building and construction had the largest share of 47.50% in 2025, and healthcare's share is expected to increase with a CAGR of 6.76% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential high-rise construction boom | +1.8% | Moscow, St. Petersburg, regional capitals | Medium term (2–4 years) |

| Automotive production recovery | +0.9% | National, concentrated in Volga and Central Federal Districts | Short term (≤2 years) |

| Government-funded transport infrastructure | +1.5% | National, priority corridors (Moscow–St. Petersburg, M-12) | Long term (≥4 years) |

| Local silicone polymer capacity expansion | +0.7% | National, with production hubs in Vladimir, Perm regions | Medium term (2–4 years) |

| Arctic-grade energy projects | +0.6% | Far North, Yamal Peninsula, Sakhalin | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Residential High-Rise Construction Boom

Moscow developers introduced 356 buildings totaling 2.69 million m² in January 2026, a 42% jump from January 2025, and started 3.9 million m² in February 2026, up 50% year on year. Average heights have climbed to 22 stories, intensifying requirements for curtain wall glazing, movement joints, and weatherproof seals that cope with a -30°C to +30°C annual thermal swing. Silicone grades dominate because their 500% elongation and UV resistance outperform acrylics in dynamic joints, yet a 150,000-400,000 worker shortfall pushes contractors toward single-component, fast-cure systems that minimize jobsite hours[1]TASS Newsroom, “Construction Ministry Confirms 400 000 Worker Gap,” tass.ru. GOST 25621-2023, in force since August 2024, obliges builders to use formulations with verified low temperature flexibility, steering demand toward premium products carrying updated compliance certificates. Suppliers combining pre-tested kits and extended open times stand to capture incremental share as high-rise cycles accelerate through 2027.

Automotive Production Recovery

AVTOVAZ built 324 558 units in 2025 and targets 400,000 vehicles in 2026, a 23% gain that translates into an added 6,000-10,000 tons of annual sealant consumption based on 15-25 kg per car. Polyurethane is preferred for seam sealing and glazing because it bonds galvanized steel and aluminum, supporting the weight reduction mandated by new Russian fuel economy rules. Imported MDI and polyols are priced in foreign currency, so the 25% ruble depreciation since mid-2024 inflated raw material costs by roughly 8-10%, compressing margins unless OEMs accept cost pass-through. Dow Izolan’s Vladimir polyols plant gives domestic formulators a hedged alternative that lets them quote in rubles and shorten logistics lead times. Automakers committed to localized supply are negotiating multi-year offtake contracts that privilege vendors holding GOST 25945-87 low temperature certificates.

Government Funded Transport Infrastructure

The RUB 2.349 trillion Moscow-St Petersburg high-speed rail line, slated for a 2028 opening, demands fire-rated tunnel liners, ±25 mm expansion joints, and acoustic barriers, calling for two-component polysulfide or polyurethane systems with 20-year warranties[2]Russian Railways, “HSL Moscow–St Petersburg Technical Brief,” rzd.ru. The M-12 Vostok highway and the USD 86 billion North-Siberian Railway add bridge deck waterproofing and concrete pavement sealing that together underpin a multiyear, counter-cyclical base for Russia Sealants market growth. Public tenders allow only GOST 25621-2023 compliant formulations, so suppliers that secured early test reports now enjoy first-mover advantages during bid evaluations. As state capex exceeds RUB 3 trillion annually through 2030, infrastructure commitments are expected to maintain baseline demand even if residential momentum eases after 2027.

Local Silicone Polymer Capacity Expansion

Ambrella Silicon plans to start 700 tons per year of silicone in 2027, while SIBUR’s EP-600 ethylene propylene complex, commissioned in 2024, lifts domestic catalyst output. Russia currently imports 70-80% of silicone intermediates, often routed via China, Turkey, or Kazakhstan, since European volumes fell by two-thirds post-sanctions. A localized feedstock base shields formulators from further currency swings and logistics delays, but limited start-up volumes will command premium prices until plants scale. Early offtake agreements between Ambrella Silicon, SIBUR, and leading formulators promise a 15-20% cost edge versus spot importers, which could reshape vendor rankings by 2029.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicone monomer price volatility | -1.00% | National, with acute pressure on Moscow, Saint Petersburg, and Tatarstan manufacturing clusters | Short term (≤ 2 years) |

| Ruble depreciation on imported inputs | -1.30% | National, particularly affecting import-dependent producers in Central and Northwestern Federal Districts | Medium term (2-4 years) |

| Skilled-installer shortage | -0.70% | National, with early constraints in Moscow, Saint Petersburg, Yekaterinburg, and Novosibirsk construction markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Silicone Monomer Price Volatility

Spot quotations for dimethyldichlorosilane swung 30-40% between Q1 2024 and Q4 2025 as Chinese producers cycled furnaces on and off, leaving Russian buyers unable to lock costs beyond 90 days. With only 700 tons per year of domestic capacity scheduled, less than 10% of demand will be locally covered in 2027, so 90% of volumes remain tied to import prices. Formulators absorb margin erosion or pass through surcharges that risk substitution toward acrylic value lines. Large volume buyers such as TechnoNICOL and Selena Group have added quarterly price escalation clauses and are diversifying into polyurethane where MDI and polyol pricing trends are flatter. Until new plants scale, silicone volatility will keep shaving roughly 0.9 percentage points off the Russia sealants market CAGR.

Ruble Depreciation on Imported Inputs

The currency lost 25% against the dollar from mid-2024 to early 2026, including a 10% two day fall after November 2024 Gazprombank sanctions, and Central Bank data show every 10% depreciation lifts headline inflation by 0.6 points. Imported polyols, isocyanates, and silicone monomers therefore landed 20-30% higher in rubles, squeezing contractors that bid fixed price jobs months earlier. The Ministry of Finance lowered mandatory export revenue repatriation from 50% to 25%, keeping structural pressure on the currency through 2027. Formulators billing in rubles but settling raw materials in dollars face a persistent mismatch unless they hedge with forwards or pivot to domestic feedstocks. This drag deducts around 1.2 percentage points from forecast growth until the ruble stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Dominance Meets Polyurethane Momentum

Silicone products accounted for 46.36% of the Russia Sealants market share in 2025, owing to 500% elongation, long UV life, and GOST 25621-2023 compliance for façade joints. The Russia Sealants market size tied to polyurethane is poised to rise at 6.45% CAGR to 2031 as automotive, Arctic LNG 2, and bridge deck applications require -60°C flexibility. Epoxy, acrylic, polysulfide, and butyl mastics together fill specialized niches such as pharmaceutical flooring or insulating glass secondary seals, where moisture vapor impermeability or paintability governs selection. Ambrella Silicon’s debut capacity covers less than a tenth of silicone demand, so formulators remain exposed to Asian monomer pricing, whereas Dow Izolan’s Vladimir plant lets polyurethane suppliers invoice in rubles, offsetting currency risk.

Sensitivities differ across resins. Silicone feedstock costs follow chlor-alkali and metallurgical silicon cycles that China dominates, so vendors build contracts with 60-day price review windows. Polyurethane precursors rely on imported MDI, yet SIBUR’s EP-600 catalyzes potential domestic integration that could drive down polyurethane finished goods pricing by 10-12% once derivative plants emerge. Suppliers that lock long term ruble denominated silicone offtake or secure domestic MDI allocations will gain margin room for brisk competitive pricing, enabling faster share capture against pure importers as the Russia sealants market expands.

By End-user Industry: Construction Leads, Healthcare Accelerates

Building and construction absorbed 47.5% of the Russia Sealants market demand in 2025 as Moscow alone initiated 3.9 million m² of flats in February 2026, up 50% on the year. Healthcare is the fastest riser with a 6.76% CAGR through 2031 after RUB 999 billion of pharma plant investments in 2025 lifted cleanroom build rates. Medical device sites such as Gloreka-Pharma’s RUB 284.5 million facility opening in Q3 2026 need ISO 10993-compliant silicone and epoxy for sterile HVAC joints, favoring suppliers versed in Roszdravnadzor approvals.

Automotive output of 400,000 cars in 2026 contributes incremental polyurethane demand while aerospace, marine, and rail remain lower volume yet margin-rich niches featuring polysulfide and epoxy. The Russia Sealants market size linked to healthcare is projected to double its share by 2031 as GMP rules spread to nutraceutical and injectable plants. Vendors must therefore balance large volume but price-competitive construction lines with specialty, high-margin medical batches that impose extensive certification but deliver multi-year offtakes once validated.

Geography Analysis

Russia Sealants market consumption concentrates majorly in Moscow and the Central Federal District, where RUB 2.349 trillion worth of high-speed rail and a record 3.9 million m² of housing launched in February 2026 drive glazing and façade orders. The Northwestern District, powered by shipyard expansions and petrochemical revamps around St Petersburg and Ust-Luga, adds 17% of national demand. Volga’s automotive axis, anchored by AVTOVAZ, secures 13%, while the Urals metal basin provides 11% through industrial maintenance and new mining capacity.

Siberia and the Far East together hold the second largest share of the market, but clock the fastest growth because Arctic LNG 2, the North-Siberian Railway, and TechnoNICOL’s planned Khabarovsk stone wool factory push specialized cold climate specifications. Import routes realign via Vladivostok, Manzhouli, and Dostyk as Western chemical volumes fell 60-70% post-2022, so regional distributors hedge China risk by adding Indian polymer cargos.

Logistics strategy now favors hub and spoke: bulk silicone and polyurethane master batches ship to Moscow or St Petersburg for reformulation, then move in 20 t road tanks to Yekaterinburg, Novosibirsk, and Vladivostok that guarantee 48 hour delivery to four fifths of jobsites. This approach limits ruble exposure to domestic freight and cushions against rail congestion on the Baikal Amur Mainline when China import volumes spike seasonally.

Competitive Landscape

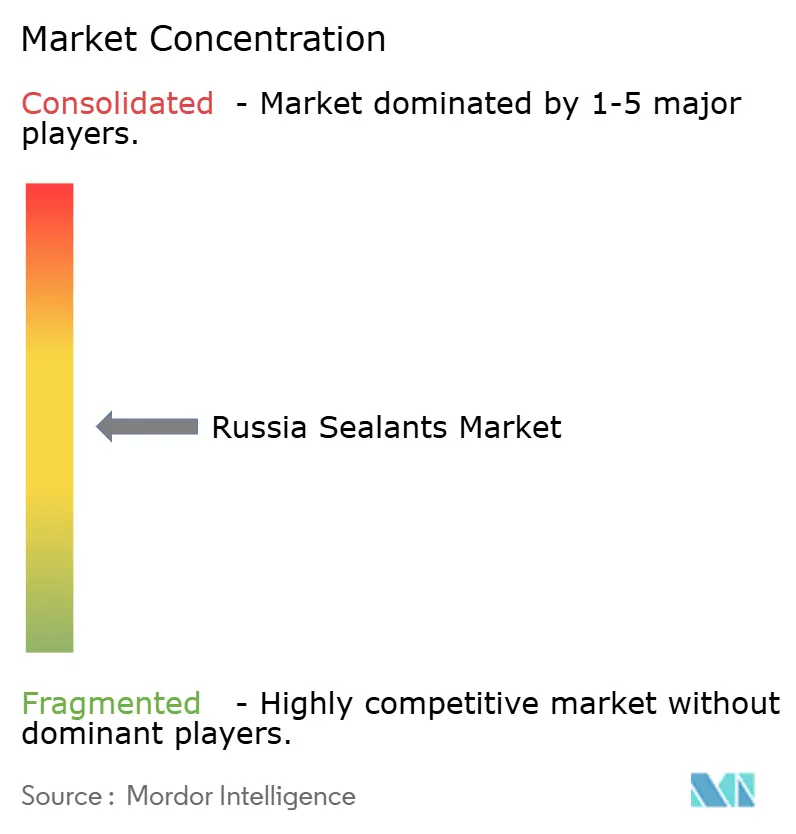

The Russia Sealants market is moderately fragmented. Despite sanctions, supply chain resilience is rising as Ambrella Silicon and SIBUR localize feedstocks, and as Dow Izolan scales polyol blends in Vladimir. These moves could lift combined domestic capacity to a third of national needs by 2030, tilting pricing power toward Russian formulators and eroding import led share by 6–8 points over the forecast window.

Russia Sealants Industry Leaders

Arkema Group

Henkel AG & Co. KGaA

MAPEI S.p.A.

Sika AG

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: MMK, one of Russia's biggest steelmakers, announced plans to cut 10% of its management personnel and pause new investment as it is operating at 60% capacity due to weak domestic demand for metals from Russia's construction, energy, automotive, and machinery manufacturing sectors. Such developments signal mounting challenges for the Russian sealants market.

- November 2025: Kremniy, Russia's largest silicon plant, revealed plans to halt production starting in 2026. The decision comes in response to dwindling demand and intensifying competition from more affordable imports. This move may pose challenges for the future of the Russian silicone sealants market.

Russia Sealants Market Report Scope

Sealants, flexible and paste-like, fill gaps, joints, and cracks between surfaces, effectively blocking air, water, moisture, and dust. Widely utilized in aerospace, construction, automotive, and healthcare, sealants protect joints. Unlike adhesives, sealants focus on providing water resistance and sealing, rather than structural bonding.

The Russia Sealants market report is segmented by resin and end-user industry. By resin, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, and other end-user industries. The market size and forecasts are provided in terms of value (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms