Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

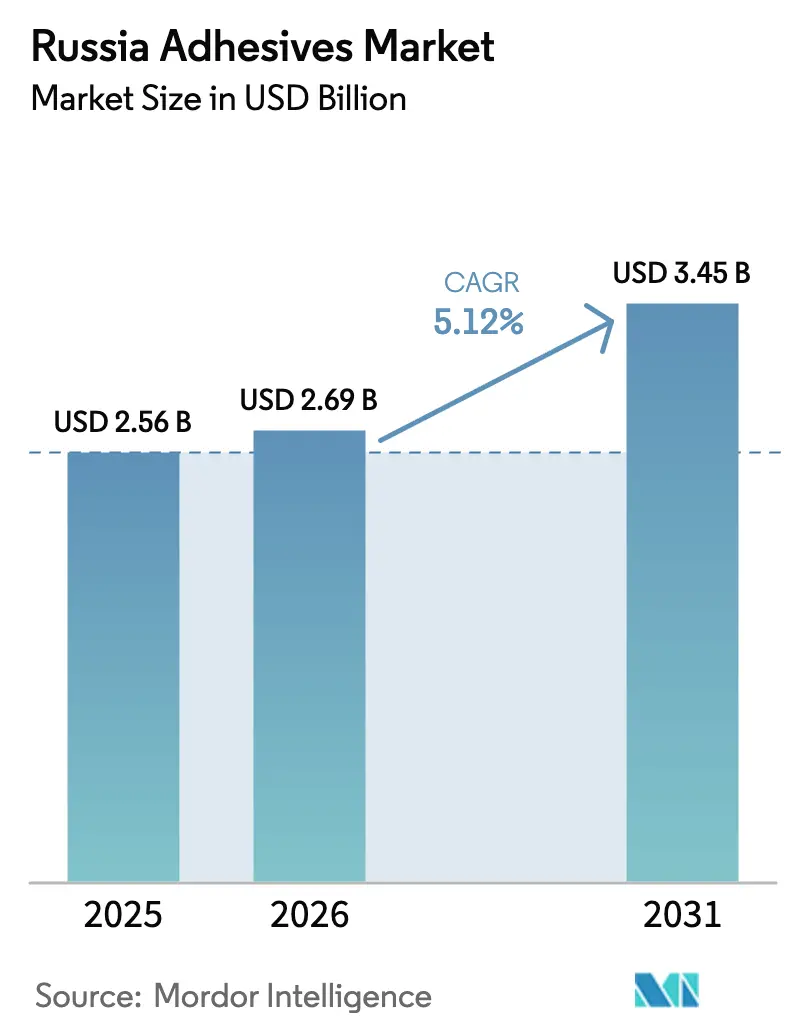

| Base Year Market Size (2025) | USD 2.56 Billion |

| Market Size (2026) | USD 2.69 Billion |

| Market Size (2031) | USD 3.45 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

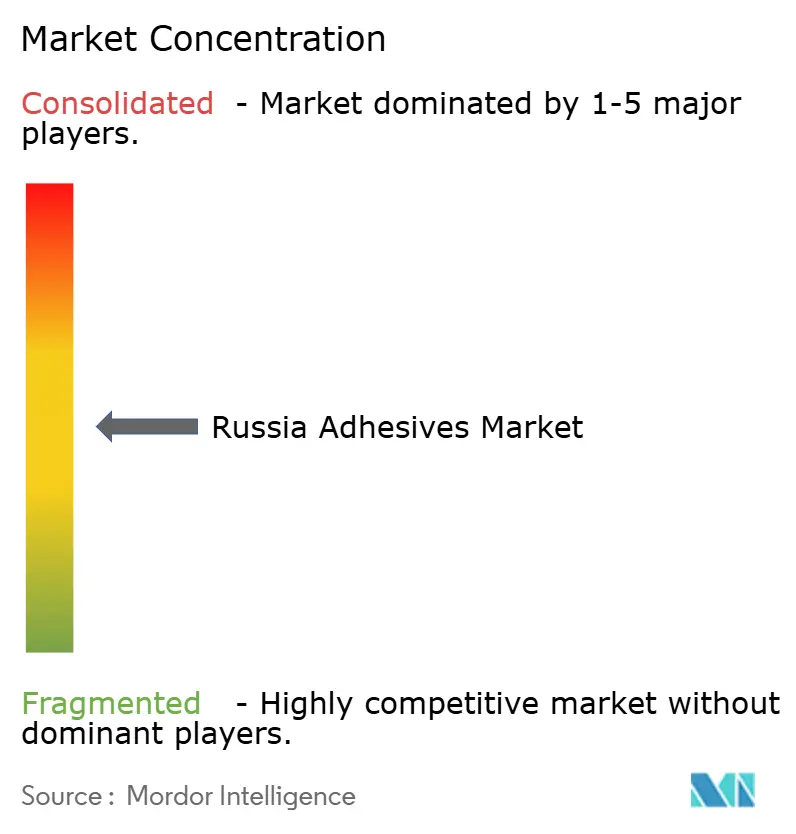

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Adhesives Market Analysis by Mordor Intelligence

The Russia Adhesives Market size is projected to grow from USD 2.56 billion in 2025 to USD 2.69 billion in 2026, and reach USD 3.45 billion by 2031, growing at a CAGR of 5.12% from 2026 to 2031. Robust import-substitution programs, persistent construction activity around Moscow and St. Petersburg, and rapid scale-up of battery manufacturing in Kaliningrad are sustaining baseline demand even as Western sanctions disrupt long-standing supply chains. Water-borne chemistries dominate day-to-day consumption thanks to lower volatile-organic-compound (VOC) emissions, while hot-melt grades are gaining share on automated packaging lines that serve Russia’s booming e-commerce sector. Domestic resin makers have rushed to localize acrylics, polyurethanes, and VAE/EVA copolymers, reducing the dependence on European feedstocks that once represented more than two-thirds of specialty raw-material inflows. Competition has intensified: multinationals such as Henkel, Sika, and MAPEI defend share with brand equity and broad portfolios, whereas state-backed newcomers leverage concessional financing to close technology gaps in automotive mastics, paper sizing agents, and electronics-grade conductive adhesives. Middle-market formulators that master regulatory registration under TR EAEU 041/2017 and secure stable additive supplies are positioned to outgrow the overall Russia adhesives market over the next five years.

Key Report Takeaways

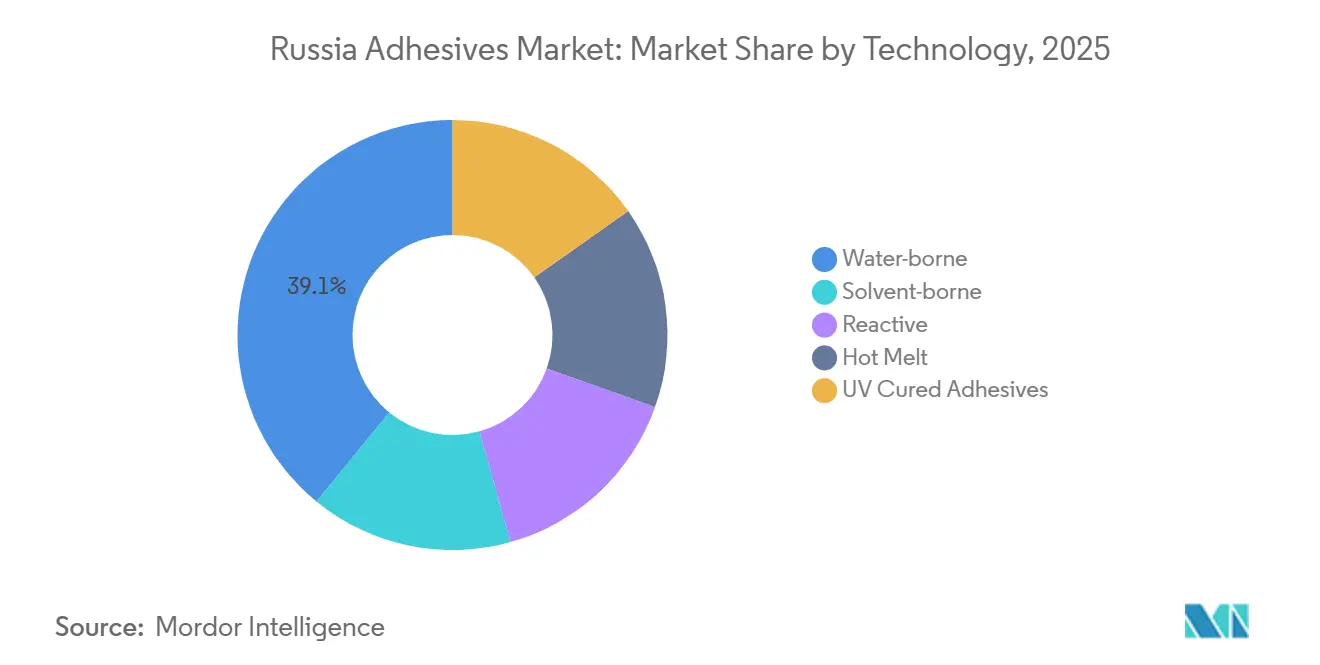

- By technology, water-borne adhesives led with 39.11% of the Russia adhesives market share in 2025, while hot-melt grades are forecast to expand at a 6.29% CAGR through 203.

- By resin, acrylic systems accounted for 22.12% of the Russia adhesives market share in 2025, whereas VAE/EVA copolymers are projected to grow at a 5.87% CAGR during 2026-2031.

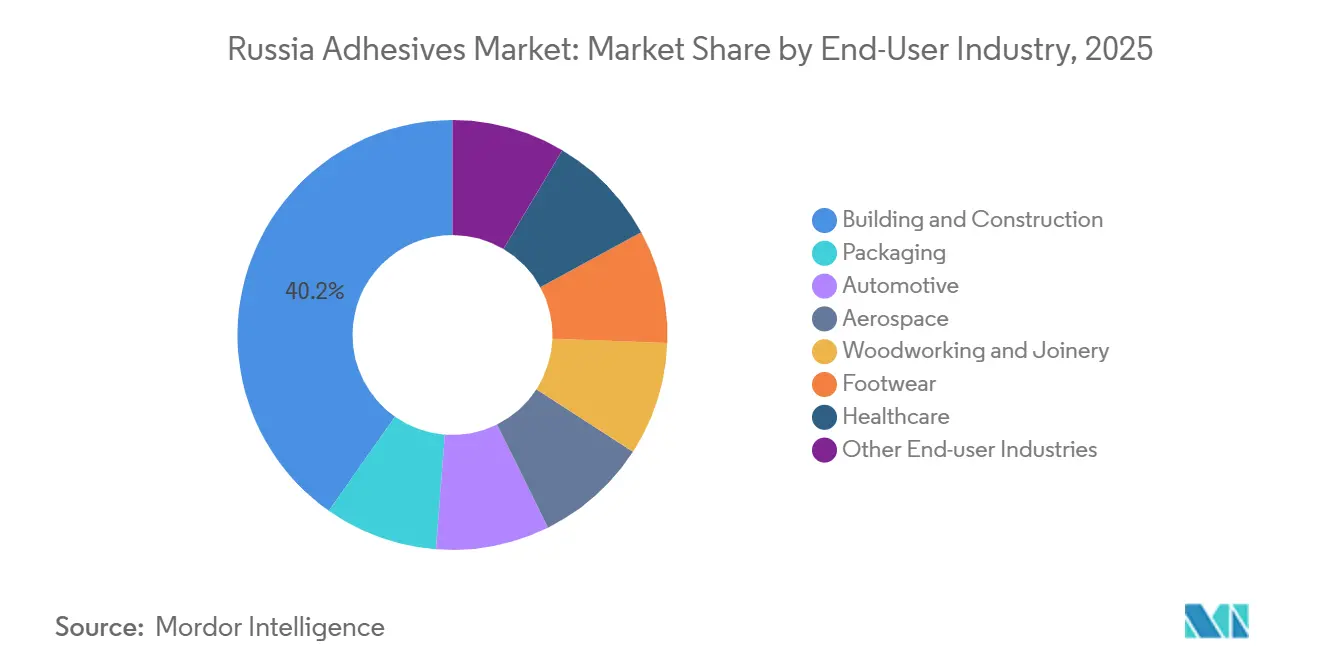

- By end-user industry, building and construction commanded 40.24% of the Russia adhesives market size in 2025; automotive applications are advancing at a 5.98% CAGR through 2031 as domestic vehicle output rebounds.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-substitution incentives spur domestic adhesive manufacturing | +1.8% | National, concentrated in Central and Volga Federal Districts | Medium term (2-4 years) |

| Rapid growth of e-commerce boosts packaging adhesives volumes | +1.2% | National, with early gains in Moscow, St. Petersburg, Yekaterinburg | Short term (≤ 2 years) |

| Local EV-battery makers adopt structural bonding solutions | +0.9% | Kaliningrad, Moscow region, spillover to automotive clusters | Medium term (2-4 years) |

| Shift to composites in defense aircraft drives high-temp epoxy uptake | +0.8% | APAC core (Ulyanovsk, Kazan, Komsomolsk-on-Amur), spillover to composite supply chain in Central Federal District | Long term (≥ 4 years) |

| Arctic LNG projects require cryogenic-grade epoxy systems | +0.7% | Gydan Peninsula, Yamal, Northern Sea Route infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import-Substitution Incentives Spur Domestic Adhesive Manufacturing

Federal concessional loans at 1-3% interest under the “Autocomponents” program financed Polad Group’s USD 2.0 million plant in Samara, which now produces 1,500 tons of mastics and 80 tons of automotive-grade adhesives annually at more than 80% localization. Homa has widened domestic PVA dispersion output to shield furniture and woodworking customers from hard-currency resin volatility, while Rostec’s Rosel division commercialized solvent-free conductive adhesives with thermal conductivity ≥10.5 W/m·K for ruggedized electronics. These projects collectively shorten supply chains, deepen local materials know-how, and channel demand away from formerly dominant European imports, providing a structural lift to the Russia adhesives market.

Rapid Growth of E-Commerce Boosts Packaging-Adhesive Volumes

Russia’s e-commerce parcel count rose by double digits in both 2024 and 2025, lifting consumption of corrugated boxes, flexible pouches, and carton-sealing tapes that rely heavily on water-borne and hot-melt adhesives. Kleit’s 500-ton-per-month eco-friendly line, certified to EMICODE EC1 PLUS, targets grocery and small-parcel shippers requiring fast-setting, odor-neutral grades. Tomsk State University’s alkenyl-succinic-anhydride project, scaled to 750 tons by end-2026, improves the wet-strength of paperboard used for meal-kit and fresh-produce delivery, cutting packaging failure rates during Moscow-region last-mile runs. These localized inputs lower cost bases for converters and underpin the steady expansion of the Russia adhesives market despite macro-economic headwinds.

Local EV-Battery Makers Adopt Structural-Bonding Solutions

Rosatom’s 4 GWh gigafactory reached commercial output in 2026, producing nearly one lithium-ion pouch cell per second and generating immediate pull-through for flame-retardant structural epoxies that can survive –40 °C to +85 °C duty cycles. The vertically integrated complex consumes conductive pastes for tab connections, thermally conductive gap fillers, and low-outgassing urethanes for housing seal-off. Polad Group has already qualified polyurethane mastics for the Lada Iskra and JAC T9 platforms, signaling a pivot toward domestically sourced bonding chemistries in next-generation Russian EVs. As battery capacity doubles over the forecast window, adhesive grams per kilowatt-hour rise, giving the Russia adhesives market an incremental growth vector that is relatively insulated from construction cyclicality.

Arctic LNG Projects Require Cryogenic-Grade Epoxy Systems

NOVATEK’s Arctic LNG 2 trains operate at –52 °C ambient temperatures for most of the year, demanding epoxy bonds with flexibilized amine curing agents that resist brittle fracture under cryogenic contraction. Russian TR CU 012 standards enforce low-temperature toughness and long-term creep testing, creating a high-barrier niche where certified suppliers can secure premium pricing. Structural bonding of pipe supports and insulation panels reduces weld count, shortens installation windows, and lowers risk in the strict seasonal build schedule on the Gydan Peninsula. Adoption of these specialty systems broadens the application envelope of the Russia adhesives market into previously underserved high-value segments.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Western additive and curing-agent embargoes strain supply chains | -1.1% | National, acute in advanced aerospace and electronics adhesives | Short term (≤ 2 years) |

| Research and development talent drain among polymer chemists | -0.6% | National, concentrated in Moscow, St. Petersburg research hubs | Medium term (2-4 years) |

| High TR 041/2017 registration costs for SMEs | -0.5% | National, disproportionately affects small and medium adhesive formulators in regional markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Western Additive and Curing-Agent Embargoes Strain Supply Chains

The U.S. Treasury’s 2024 sanctions on Russian sealant makers and logistics intermediaries restricted access to high-performance curing agents, impact modifiers, and flame retardants critical for aerospace and electronics adhesives[1]Office of Foreign Assets Control, “Russia-related Designations,” home.treasury.gov. Formal banking blocks on MOEX and NCC have lengthened payment cycles and dissuaded Asian suppliers from shipping specialty epoxies, forcing local formulators to qualify alternative raw materials with variable purity profiles. While capacity additions by regional chemical plants mitigate some shortages, lead times for qualifying new recipes have lengthened, capping short-term upside for premium volumes within the Russia adhesives market.

Research and Development Talent Drain Among Polymer Chemists

The migration of mid-career polymer scientists to Europe and Asia is tightening the domestic skills pool just as Russia’s adhesives industry pursues higher-performance and environmentally safer chemistries. University laboratories report delays in scaling pilot batches to production scale because access to nuclear magnetic-resonance (NMR) spectrometers and differential-scanning calorimeters is limited by export-control restrictions. Henkel’s Shanghai Inspiration Center, employing more than 500 researchers, showcases the infrastructure gap Russian firms must bridge to retain innovators[2]Henkel AG & Co. KGaA, “Henkel Opens Inspiration Center Shanghai,” henkel.com . Without competitive salaries and equipment, smaller enterprises risk slower formulation cycles, impeding the pace at which the Russia adhesives market can move up the value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Dominance Sustained as Hot-Melt Accelerates

Water-borne products captured 39.11% of the Russia adhesives market share in 2025, supported by low flammability and straightforward clean-up in construction tiling, woodworking, and bookbinding applications. MAPEI’s Keraflex MAXI S1 and Ultralite S2 lines, both meeting GOST R 56387-2018 and EMICODE EC1 PLUS, underscore how performance, not simply price, now anchors purchase decisions. Reactive polyurethanes and epoxies, though lower in tonnage, command price premiums in EV battery packs and composite aircraft panels where shear strength and thermal cycling resistance are essential.

Hot-melt formulations, on track for a 6.29% CAGR, suit the robotic carton sealers populating Moscow, Kazan, and Novosibirsk fulfillment centers. Their instant set obviates drying ovens, trimming line energy use by up to 15%, and raising uptime during peak shopping seasons. UV-cured acrylates are niche but rising in display-panel assembly, while solvent-borne systems retreat to specialist roles where rapid wetting of low-energy plastics offsets VOC compliance costs. Overall, technology diversification shields the Russia adhesives market from single-segment shocks and aligns domestic chemistries with global sustainability norms.

By Resin: Acrylic Versatility Leads, VAE/EVA Gains Momentum

Acrylic chemistries commanded 22.12% of the Russia adhesives market share in 2025, prized for weatherability and pressure-sensitive tack in construction tapes and labeling lines. Huntsman’s reformulated BPA-free Araldite range illustrates how regulatory-driven innovation can open opportunities for safer high-modulus epoxies that slot into rail-car, marine, and medical assemblies.

VAE/EVA resins, expanding at a 5.87% CAGR, bond polyethylene mailers, bubble wrap, and multilayer films that shield small parcels in Russia’s dynamic e-commerce pipeline. Polyurethanes retain dominance in windshield and footwear lamination, while silicone grades benefit from sensor miniaturization in next-generation vehicles. The Russia adhesives market size for epoxy resin systems is set to rise as Arctic energy and defense aerostructure programs widen demand for cryogenic and high-temperature grades.

By End-User Industry: Construction Still Commands, Automotive Emerges Fastest

Building and construction accounted for 40.24% of the Russia adhesives market size in 2025, driven by metro extensions in Moscow, residential refurbishments spurred by subsidy programs, and hotel upgrades ahead of international sporting events. Lightweight cementitious blends such as Ultralite S2, with a bulk density of 850 kg/m³, lower transport costs and lessen floor-load requirements in high-rise retrofits.

The automotive industry is projected to post the fastest 5.98% CAGR owing to localized production of Lada Granta, UAZ Patriot, and JAC pickups. Polad Group’s Samara plant supplies OEM-specified mastics that meet 480-hour salt-spray performance, while conductive pastes from Rosel secure battery-management electronics in newly assembled EV packs. Packaging, electronics, and healthcare add steady incremental volume, collectively buffering the Russia adhesives market from cyclic swings in single end-markets.

Geography Analysis

Russia’s adhesives production is highly clustered. Moscow and the surrounding Central Federal District hold the largest installed capacity, benefiting from dense construction pipelines, proximity to universities, and an unrivaled logistics backbone. Samara in the Volga Federal District hosts Polad Group’s flagship automotive-adhesive complex, enabling just-in-time deliveries to nearby AvtoVAZ and GAZ lines.

Kaliningrad anchors the Northwestern District with Rosatom’s 4 GWh battery plant that generates continuous demand for structural and thermal-interface materials. Far-eastern yards at Komsomolsk-on-Amur and Ulyanovsk absorb specialty epoxies for composite airframes, while Arctic LNG construction around the Gydan Peninsula pulls in cryogenic-grade systems during seasonal build windows. Siberian forestry clusters tap Tomsk-origin ASA sizing agents for moisture-resistant paperboard, exemplifying how regional resource bases shape localized adhesive demand patterns.

Cross-border trade inside the Eurasian Economic Union (EAEU) allows compliant Russian grades to flow into Belarus and Kazakhstan under a common TR EAEU 041/2017 framework. These outbound volumes, though still modest, demonstrate the export headroom available once domestic formulators meet cost and registration hurdles. The geographic mosaic therefore underpins the long-run resilience of the Russia adhesives market, dispersing growth drivers across multiple time zones and industry verticals.

Competitive Landscape

The Russian adhesives market is moderately consolidated. Domestic challengers thrive on import-substitution credits. Polad Group, 25% target share in OEM mastics, leverages 80% localized raw materials and proximity to Russia’s largest carplant cluster. Rosel’s newly commercialized conductive adhesive fills a void in high-heat electronics once served by Japanese imports, while Homa’s PVA dispersions supply furniture and panel-lamination shops across Central Russia. Barriers to entry include the cost of TR EAEU 041/2017 testing, in-country safety-data-sheet translation, and the need to self-insure for volatile pigment and additive imports. Strategic white spaces remain in thermal-interface materials for battery packs, low-temperature epoxies certified to TR CU 012 for Arctic applications, and EMICODE-compliant packaging grades demanded by multinational brand owners. Players that fuse deep research and development with regulatory agility are best placed to expand share as the Russia adhesives market advances toward the USD 3.45 billion mark by 2031.

Russia Adhesives Industry Leaders

Henkel AG & Co. KGaA

Sika AG

H.B. Fuller Company

RusTA LLC

Kiilto

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Rosaviatsia approved a major amendment to the MC-21 type certificate, allowing domestic composite materials in the vertical fin and horizontal stabilizer. Serial production is underway at KAPO-Composite; full certification of the all-Russian variant is targeted for end-2026.

- October 2025: Huntsman Advanced Materials launched a BPA-free Araldite epoxy range in Europe, replacing CMR-classified ingredients and introducing cartridges made with post-consumer recycled plastic that cut CO₂ emissions by up to 36%.

Russia Adhesives Market Report Scope

Adhesives are materials designed to bond surfaces together effectively, ensuring durability and resistance to separation. Various industries, including building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user sectors, rely on specific types of adhesives tailored to their composition and functional requirements.

The Russia adhesives market is segmented by technology, resin, and end-user industry. By technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV cured adhesives. By resin, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By end-user industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By End-User Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear |

| Healthcare |

| Other End-user Industries |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By End-User Industry | Building and Construction |

| Packaging | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms