Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

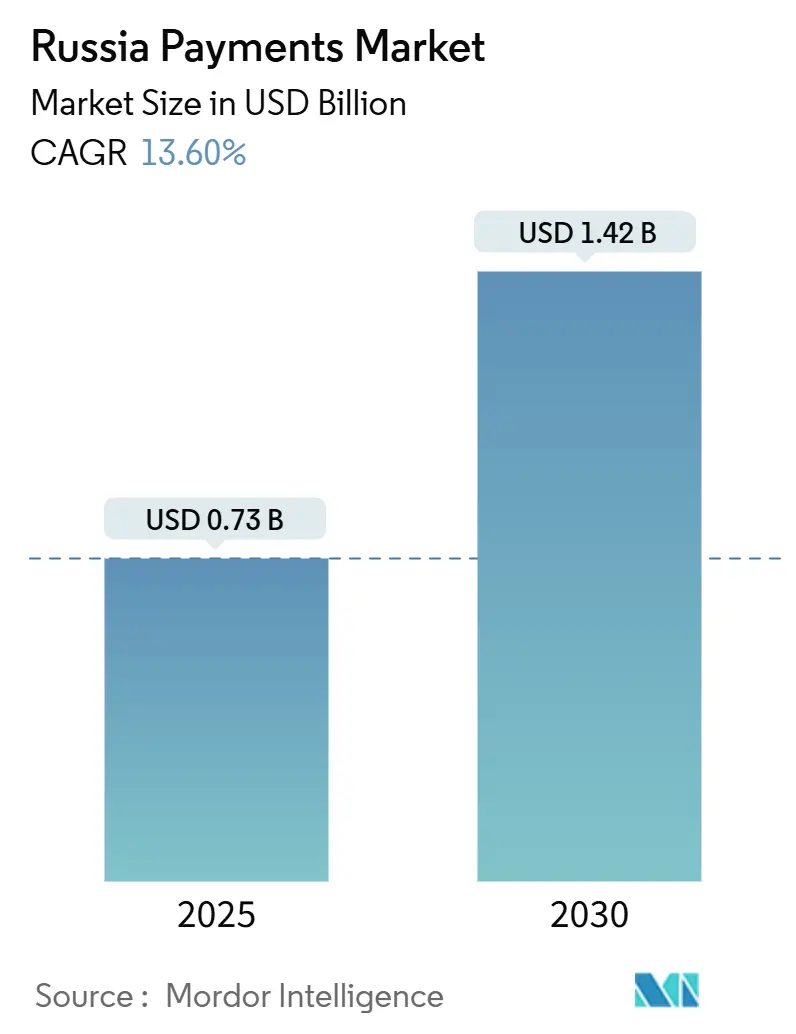

| Market Size (2025) | USD 0.73 Billion |

| Market Size (2030) | USD 1.42 Billion |

| Growth Rate (2025 - 2030) | 13.60% CAGR |

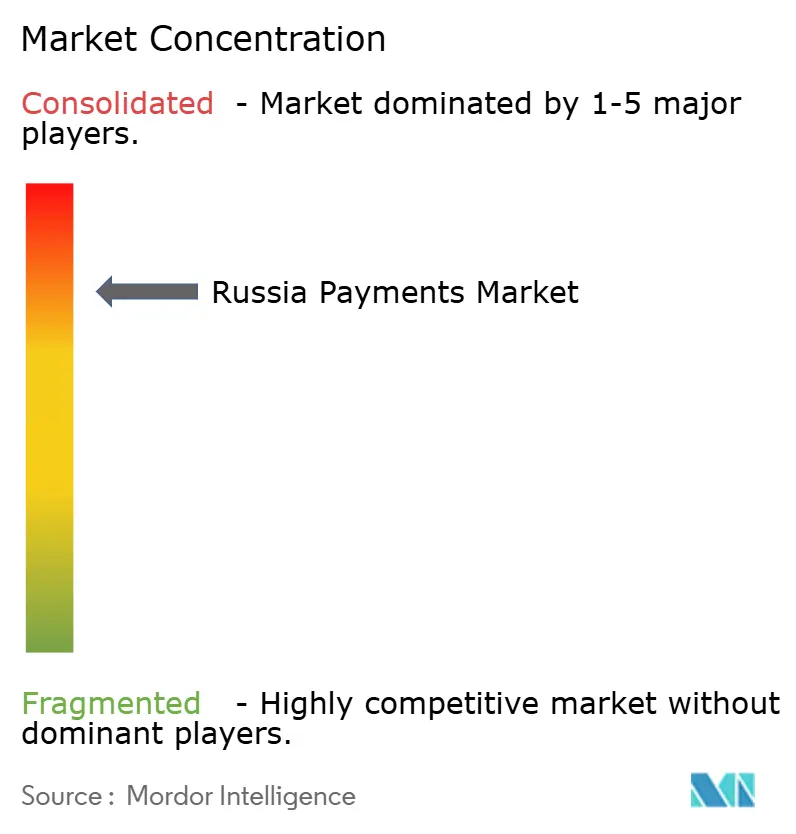

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Payments Market Analysis by Mordor Intelligence

The Russia payments market size reached USD 0.73 trillion in 2025 and is forecast to expand to USD 1.42 trillion by 2030, registering a 13.60% CAGR as domestic rails replace Western networks while mobile-first solutions mature. The Russia payments market is propelled by a forced quest for technological sovereignty following Visa and Mastercard’s withdrawal, state mandates that accelerate cashless public-sector disbursements, and a surge in regional e-commerce volumes that now penetrate Tier-2 cities. Government backing for the Mir scheme, fast-growing QR ecosystems, and the July 2025 digital-ruble launch combine to buffer cross-border shocks and draw users toward homegrown alternatives. Competitive behavior has turned oligopolistic: state-linked banks leverage balance-sheet heft and biometrics to set rapid adoption cycles, while telcos and fintechs exploit QR rails to win niches. Heightened cyber-risk and hardware bottlenecks temper the upside but also stimulate domestic chip design and crypto-ruble gateways that may later serve export markets.

Key Report Takeaways

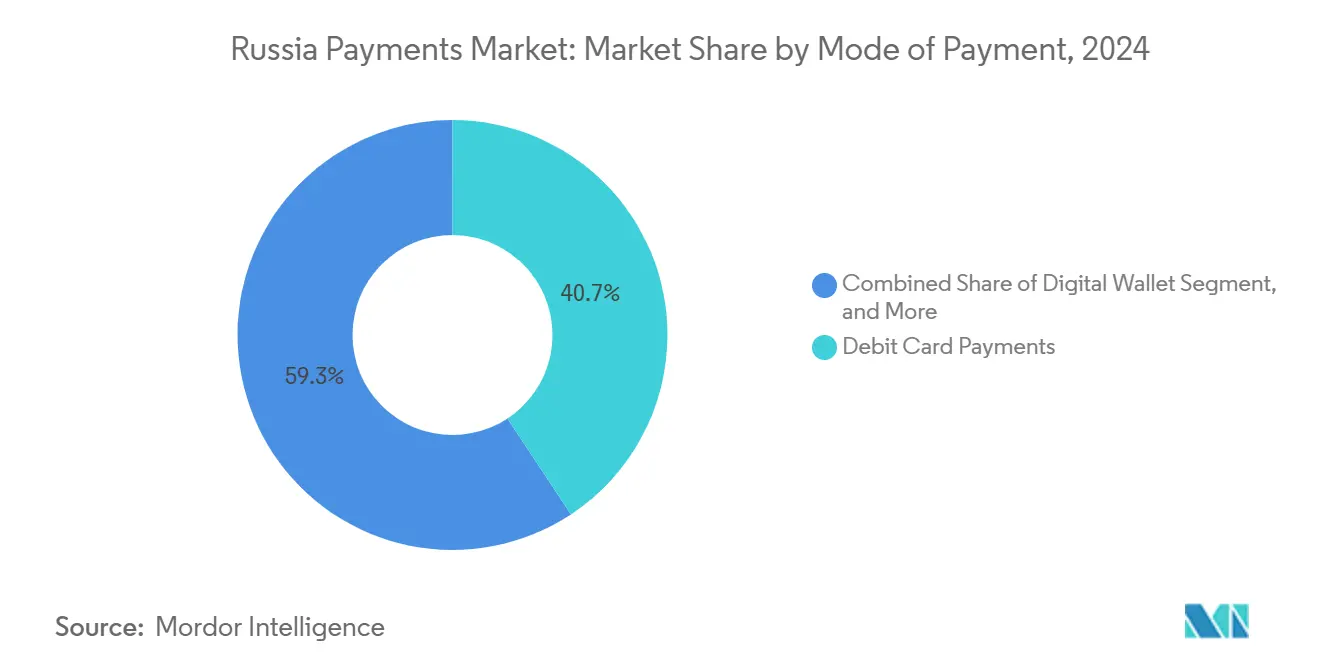

- By mode of payment, debit cards led with 40.71% of Russia payments market share in 2024; digital wallets are projected to expand at a 14.45% CAGR through 2030.

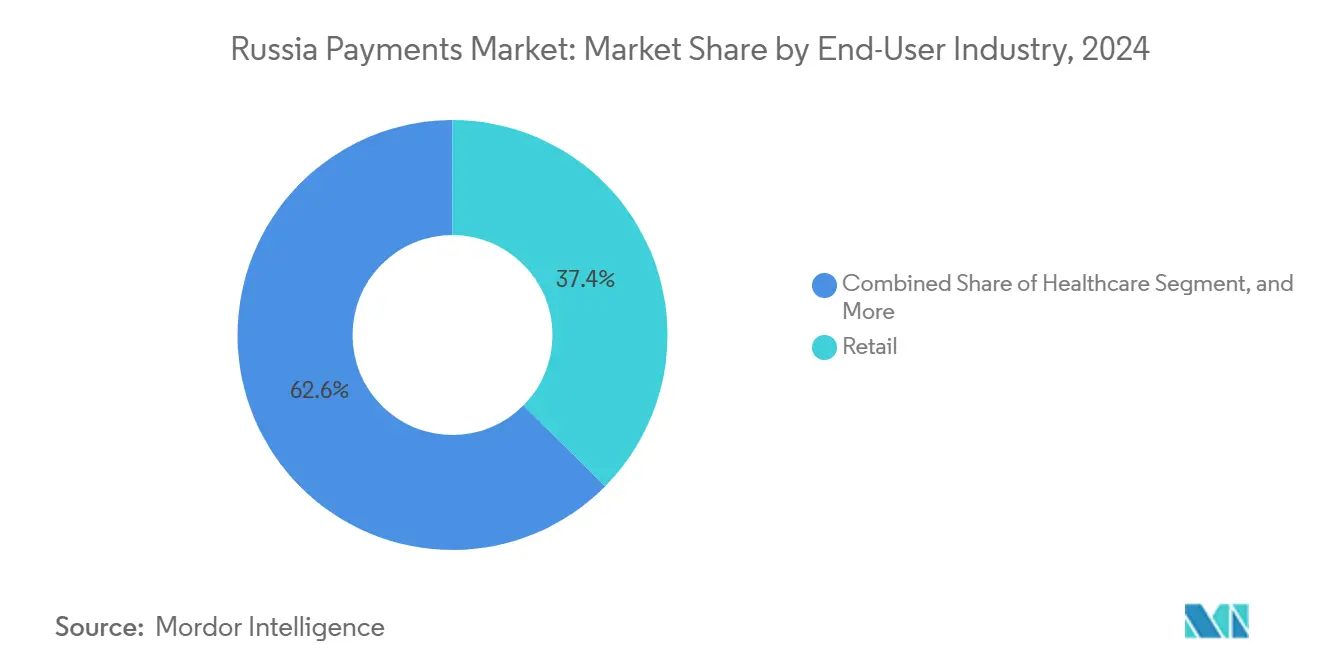

- By end-user industry, retail accounted for 37.42% of the Russia payments market size in 2024, while healthcare is advancing at a 14.19% CAGR through 2030.

- By company, Sberbank controlled 51% of the 2024 credit-card segment within the Russia payments market.

Russia Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Mir card acceptance network | +2.8% | National, with international expansion to Iran, Nicaragua, Uzbekistan | Medium term (2-4 years) |

| Rapid e-commerce penetration among regions | +3.2% | National, with strongest growth in Tier-2 cities | Short term (≤ 2 years) |

| Government push for cashless public-sector disbursements | +2.1% | National, with pilots in Tatarstan and Moscow | Medium term (2-4 years) |

| Rise of private label QR-code ecosystems in Tier-2 cities | +1.9% | Regional, concentrated in Sverdlovsk, Tatarstan, Kazan | Long term (≥ 4 years) |

| SME demand for crypto-ruble gateways after sanctions | +1.5% | National, with cross-border trade focus | Medium term (2-4 years) |

| Growth of domestic BNPL super-apps targeting Gen-Z | +1.8% | National, concentrated in major urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Mir Card Acceptance Network

Mir’s international roll-out now spans Iran, Uzbekistan, Nicaragua, and pilot corridors into Turkey, creating sanctioned-proof rails that recycle inbound and outbound spend without SWIFT or U.S. dollar exposure. Acceptance abroad lifts domestic clearing volumes, encourages Russian travelers to stay cashless, and offers a blueprint for South-South payment alliances. The Russia payments market therefore gains a dual dividend: foreign-policy leverage and incremental domestic fee income as every new corridor adds users.

Rapid E-commerce Penetration Among Regions

Online retail turnover jumped 45% in 2024 to 19.9 trillion rubles as regional platforms plugged straight into the Fast Payment System (SBP), cutting acquirer fees and speeding settlement. Tier-2 cities now match Moscow in year-on-year checkout-conversion gains, proving that inexpensive QR and account-to-account (A2A) rails broaden access. Marketplace banks already capture 40% of e-commerce flows, signaling a structural shift inside the Russia payments market toward platform-native finance.

Government Push for Cashless Public-Sector Disbursements

The digital ruble entered public circulation in July 2025, enabling ministries to send welfare, pensions, and tax refunds directly to citizens’ wallets, lowering cash‐handling costs and boosting audit trails.[1]Bank of Russia, “Digital Ruble Pilot Launch,” cbr.ru Pilot provinces such as Tatarstan show a drop in disbursement times from days to minutes, anchoring new recurring volumes for processors while reinforcing central-bank oversight.

Rise of Private-Label QR-Code Ecosystems in Tier-2 Cities

Local QR networks in Kazan, Yekaterinburg, and the wider Sverdlovsk region now cover public transport, utilities, and grocery chains. Telcos like MTS leverage subscriber bases to embed QR checkout inside “MTS Dengi,” removing card hardware from the equation and extending the Russia payments market into unbanked pockets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Withdrawal of Visa/Mastercard international services | -1.8% | National, with cross-border transaction impacts | Short term (≤ 2 years) |

| Heightened cyber-security and fraud incidents | -1.2% | National, concentrated in major financial centers | Medium term (2-4 years) |

| Shortage of imported POS hardware and NFC chips | -0.9% | National, with acute impacts in Tier-2 cities | Medium term (2-4 years) |

| Rising interchange-fee caps on Mir transactions | -0.7% | National, affecting all Mir card transactions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Withdrawal of Visa/Mastercard International Services

When Visa and Mastercard suspended Russian operations, cross-border card volumes evaporated, forcing a messy pivot to UnionPay and Mir co-badge workarounds. Merchants scrambled to update POS certificates, and consumers faced friction paying abroad. Short-term pain shaved growth off the Russia payments market, yet the hiatus fast-tracked domestic scheme adoption and fortified strategic independence.

Heightened Cyber-Security and Fraud Incidents

Digital take-up widened the attack surface. Large-scale DDoS events, such as a 13-hour siege on Sberbank in July 2024, raised compliance burdens and drove the Central Bank to mandate real-time fraud reporting from October 2025. Banks now budget more for domestic cryptography and customer-protection tooling, a temporary drag on margins but a long-run trust accelerator for the Russia payments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital Wallets Gain Momentum

Digital wallets are growing at a 14.45% CAGR to 2030, while debit cards retain a 40.71% slice of Russia payments market share in 2024. That split confirms that mobile-first behavior is no longer confined to metro areas; the “super-app” proposition bundles payments, BNPL, and loyalty in one gesture. The Russia payments market size for wallets benefits from SberPay reaching 1.7 million terminals, and from SBP’s zero-to-low-fee transfers that lure merchants away from legacy acquiring.

Credit cards suffer from the loss of Visa/Mastercard rails, capping cross-border utility. Meanwhile, account-to-account volumes via SBP rise as over 200 institutions join the scheme. YooMoney’s RUB 23.7 billion fintech revenue shows how wallet providers monetize beyond pure payment processing.[2]Наталья Заруцкая, “СБП: что такое система быстрых платежей и как ей воспользоваться,” Vedomosti, vedomosti.ru Crypto-ruble gateways are also embedding inside wallets, offering small exporters sanctioned-proof settlement paths that enlarge addressable demand within the Russia payments market.

By End-User Industry: Healthcare Surges Ahead

Retail kept the largest 37.42% share of Russia payments market size in 2024 thanks to entrenched in-store and e-commerce rails. Yet healthcare is on track to post the fastest 14.19% CAGR as telemedicine, remote prescription fulfillment, and insurer pay-outs migrate to digital ruble channels. The Russia payments market now sees clinics integrating SBP kiosks and QR scripts to collect co-pays instantly, trimming claims cycles and boosting throughput.

Public-service payments are another growth node; agencies now distribute benefits via programmable rubles, bypassing intermediary bank hurdles. Entertainment and hospitality adjust to new inbound tourist pools from “friendly” economies; Mir-accepting terminals at hotels and attractions recapture spend that once flowed through foreign schemes. Transportation and utilities add QR fare boxes, lowering cash leakage. Together, these vertical pivots spread the Russia payments market across use cases once deemed peripheral.

Geography Analysis

Moscow and St. Petersburg still anchor the largest absolute volumes, yet Tier-2 cities now supply the steepest growth slopes. Kazan leads biometric checkout installations across metro stations, while Yekaterinburg prototypes distance-based bus fares settled through SBP QR codes. This polycentric advance reduces concentration risk, letting the Russia payments market operate if any single hub faces sanctions or outages.

Tatarstan acts as a sandbox for CBDC payroll and welfare use, feeding empirical insights back to the Central Bank. Sverdlovsk’s roll-out of QR transport payments shows regional authorities can leapfrog older card validators, aligning cost structures with local budgets. In cross-border corridors, VTB’s Tehran office clears Mir card imports for Russian tourists, while bilateral trade with Belarus and Kazakhstan taps local switch agreements to skirt dollar settlements.

Far East gateways targeting Chinese tourists experiment with UnionPay-Mir co-branded cards that rebate in digital rubles. Northwestern regions align with Baltic cargo routes where crypto-enabled gateways speed SME import payments. That geographic mosaic converts sanctions into a distributed R&D lab, deepening the resilience of the Russia payments market.

Competitive Landscape

State-affiliated behemoths frame an oligopoly: Sberbank holds 51% of the credit-card pool and uses its 110 million-plus client base to seed biometric-payment pilots, from grocery chains to subway gates. Tinkoff follows with 18%, leveraging a lifestyle super-app to retain high-frequency users, while Alfa-Bank’s 11% slice gained lift from a February 2025 purchase of Pay-Me fintech, bolstering mobile-payment depth.

Qiwi’s early-2025 acquisition of Otkritie Bank’s acquiring arm formed one of Russia’s largest independent merchant-service providers, giving mid-tier retailers an option outside bank oligarchs. Telecommunications carriers such as MTS push into payments by bundling QR checkout within data plans, courting unbanked demographics, and edging the Russia payments market toward telco-fintech convergence.

Strategic focus is on domestic stacks: firms deploy local chips, in-house cryptography, and Russian facial-recognition engines to sidestep import controls. Cross-border innovation, meanwhile, tilts to blockchain settlement consortia; BRICS Pay pilots in Moscow hint at a multi-CBDC clearing layer that could reroute trade invoicing away from the dollar.[3]BRICS Pay, “DemoMoscow,” brics-pay.com Overall, competitive success now hinges on political alignment, domestic tech mastery, and the agility to convert sanctions risk into first-mover advantage.

Russia Payments Industry Leaders

Ingenco LLC

2Checkout.com Inc. (Verifone)

OnePay LLC

YooMoney LLC

Tinkoff Pay (TCS Group Holding PLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Rosselhozbank launched biometric metro payments in Kazan with RUB 15 cashback per ride, marking Russia’s first interbank bio-acquiring rollout with nationwide expansion scheduled by year-end.

- February 2025: MTS enabled QR payments through its “MTS Dengi” Android app, linking to the Fast Payment System for fee-free merchant acceptance.

- February 2025: Alfa-Bank closed the Pay-Me acquisition, adding white-label mobile-payment modules for SME merchants.

- January 2025: Qiwi finalized the purchase of Otkritie Bank’s acquiring assets, doubling its merchant network and strengthening wallet-to-merchant interoperability.

Russia Payments Market Report Scope

The Russian payments market includes various types of payments, including point-of-sale and e-commerce, card payments, and contactless payments. E-commerce payments include online purchases of goods and services. Purchase on the e-commerce website and book travel and accommodation online. For POS, all transactions made at physical sales are included in the following market scope: payment by credit card or debit card. This consists of all face-to-face dealings, not just traditional in-store transactions, regardless of where they occur. In both cases, cash payments are also considered (cash payments for e-commerce sales).

Mode of Payment

| Point-of-Sale | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash | |

| Other Point-of-Sale Payment Modes | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Sale Payment Modes |

End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Public Services |

| Other End-User Industries |

| Mode of Payment | Point-of-Sale | Debit Card Payments |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point-of-Sale Payment Modes | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Sale Payment Modes | ||

| End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Public Services | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the Russia payments market in 2025?

It stood at USD 0.73 trillion in 2025 and is projected to hit USD 1.42 trillion by 2030.

What drives the strongest growth inside Russia’s payment modes?

Digital wallets, supported by SBP fees near zero and biometric checkout, are growing at a 14.45% CAGR through 2030.

Which industry vertical is the fastest adopter of new payment tech?

Healthcare leads with a 14.19% CAGR as telemedicine and e-prescription platforms integrate instant settlement.

How is the digital ruble changing government transactions?

Launched nationwide in July 2025, the CBDC lets agencies push benefits, salaries, and tax refunds directly to citizens’ wallets, slashing disbursement times.

Who holds the dominant position among Russian payment providers?

Sberbank controls roughly 51% of the credit-card segment and uses biometric tech to cement its lead.

Page last updated on: